Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

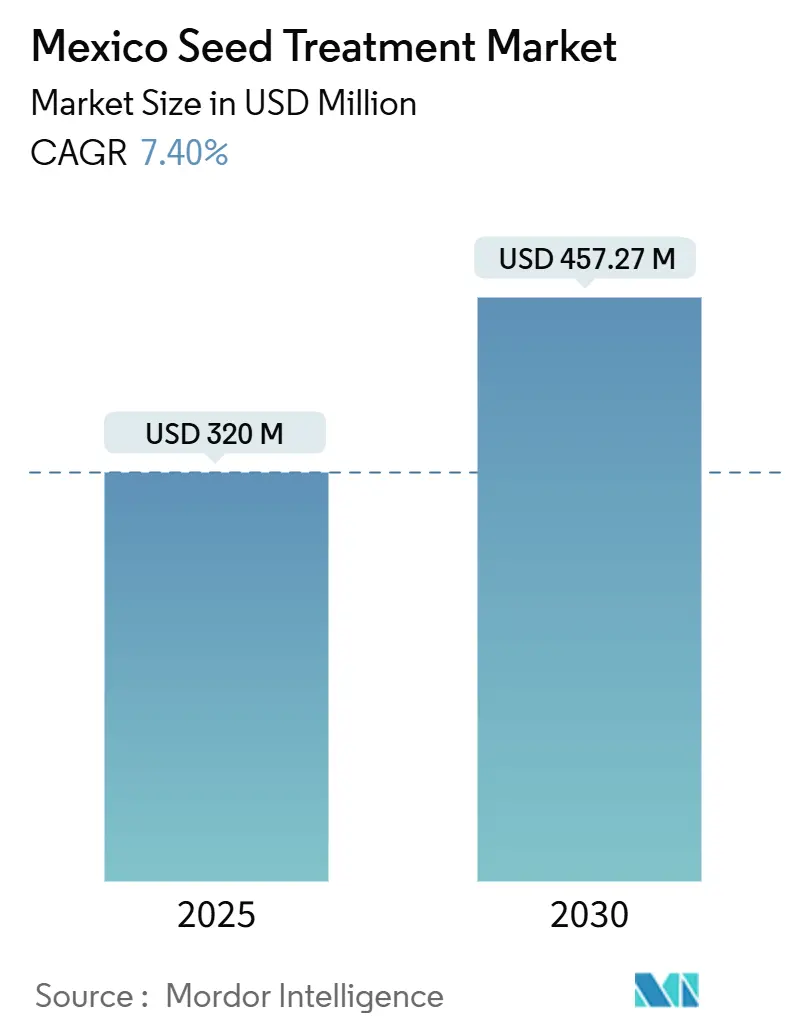

| Market Size (2025) | USD 320 Million |

| Market Size (2030) | USD 457.27 Million |

| Growth Rate (2025 - 2030) | 7.40% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Seed Treatment Market Analysis by Mordor Intelligence

The Mexico seed treatment market size is estimated at USD 320 million in 2025 and is projected to reach USD 457.27 million by 2030, growing at a 7.4% CAGR over the forecast period. The accelerated uptake of precision chemistries and data-enabled application methods anchors this expansion trajectory, even as constitutional limits on genetically modified (GM) corn spur a heightened reliance on external crop-protection inputs. Rising pest pressure, regulatory scrutiny of neonicotinoids, and a robust pipeline of diamide-based and bio-derived actives collectively shape the outlook for the Mexico seed treatment market. Continued mechanization, coupled with mobile-enabled advisory services, positions small and mid-scale growers to adopt treated seed as a front-line defense against shifting precipitation regimes. The market, therefore, reflects both a hedge against agronomic volatility and a pathway to meet increasingly stringent export quality standards.

Key Report Takeaways

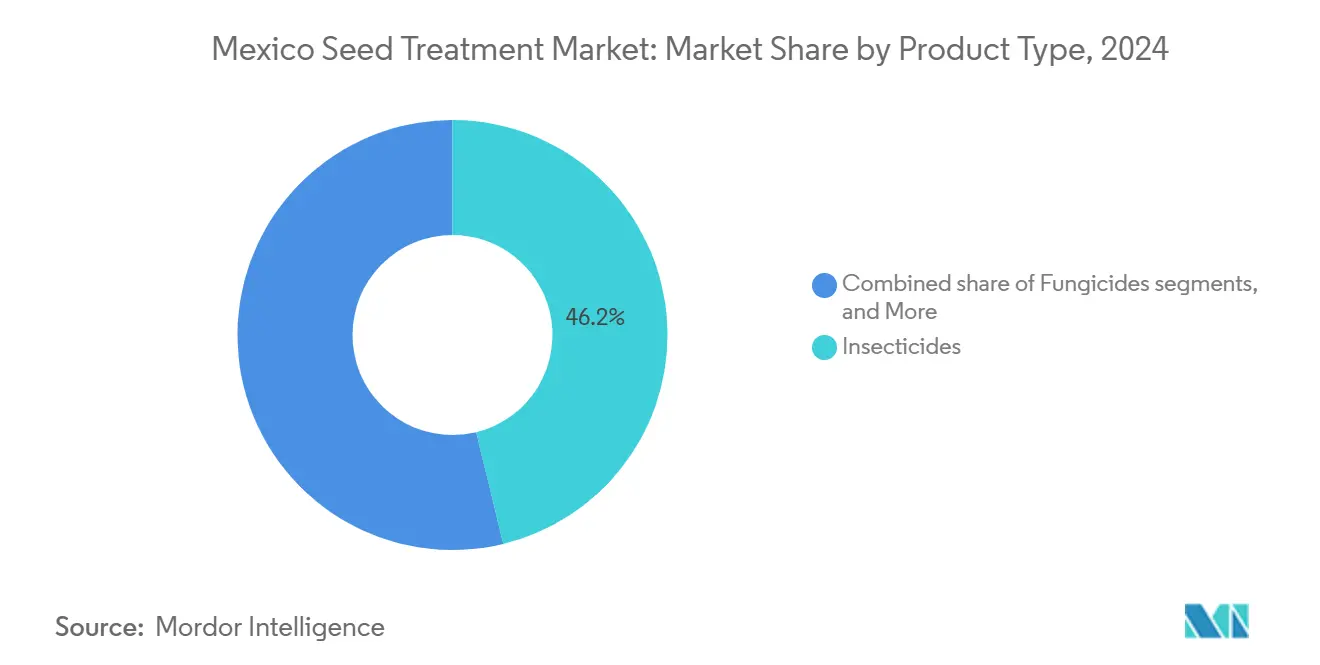

- By product type, insecticides led with 46.20% of the Mexico seed treatment market share in 2024, while nematicides recorded the fastest CAGR at 11.80% to 2030.

- By formulation type, liquid flowable products held 67.20% of the Mexico seed treatment market share in 2024, while polymer-based coatings are forecast to expand at a 9.70% CAGR through 2030.

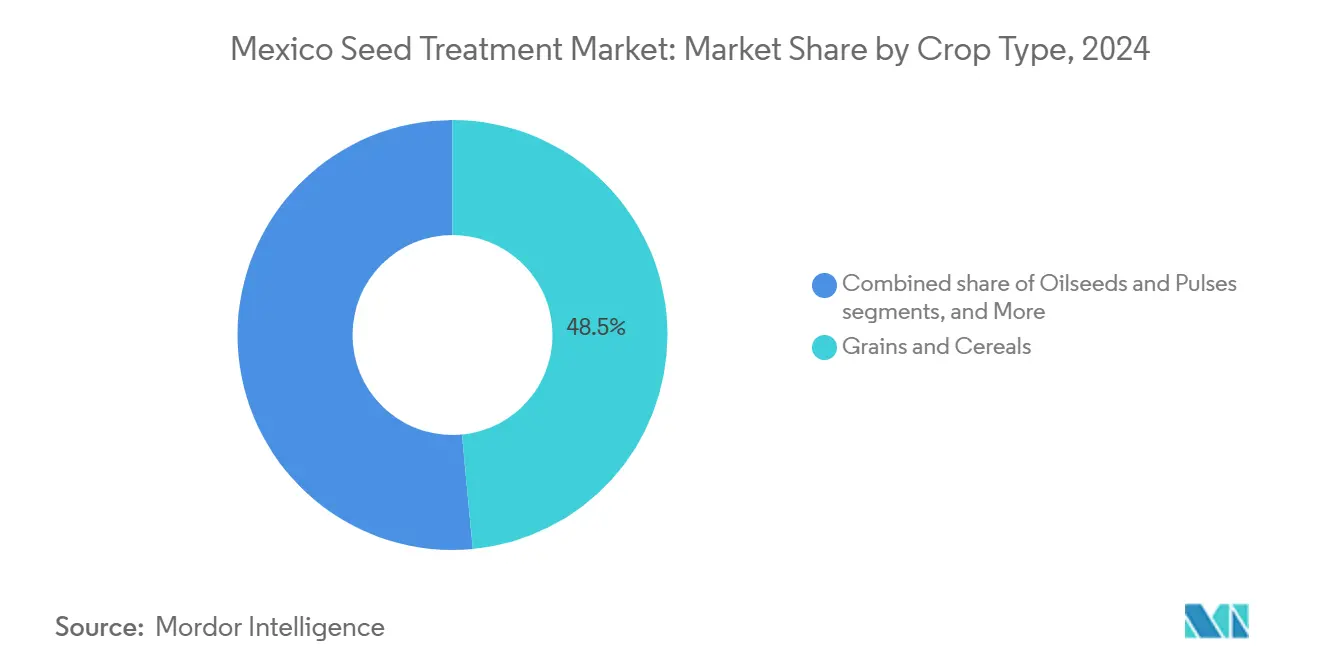

- By crop type, grains and cereals accounted for 48.50% of the Mexico seed treatment market size in 2024. Fruits and vegetables are projected to grow at a 9.40% CAGR through 2030.

Mexico Seed Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated early-planting risk under climate volatility | +1.2% | National, with the highest impact in northern states (Sinaloa, Sonora, Chihuahua) | Medium term (2-4 years) |

| Carbon-credit programs rewarding treated seed for stand uniformity | +0.8% | National, with early gains in export-oriented regions (Michoacán, Jalisco) | Long term (≥ 4 years) |

| Mandatory re-registration of neonics driving premium alternative chemistries | +1.5% | National, with accelerated adoption in high-value crop zones | Short term (≤ 2 years) |

| Surge in coatings for regenerative farming systems | +1.1% | National, with concentration in organic-certified production areas | Medium term (2-4 years) |

| Generic chlorantraniliprole price crash expanding diamide seed blends | +0.9% | National, particularly in corn and soybean production regions | Short term (≤ 2 years) |

| On-planter additive boom amid decline in in-furrow systems | +0.7% | National, with focus on mechanized farming operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated Early-Planting Risk Under Climate Volatility

Shifting temperature and rainfall regimes compress planting windows, forcing earlier sowing into cooler soils and amplifying vulnerability to seed- and soil-borne pathogens. Northern Mexico is projected to face temperature rises of 1.8–2.1 °C by 2040, which will expand semi-arid zones and prolong germination stress periods[1]Source: Ríos-Romero et al., “Climate change impact on rain-fed agriculture of Northern Mexico,” Modeling Earth Systems and Environment, researchgate.net. The adoption of sedaxane-based Succinate Dehydrogenase Inhibitor (SDHI) fungicides and stress tolerance enhancers, therefore, gains momentum across the Mexico seed treatment market as growers seek insurance against emergence failures. The Servicio Nacional de Sanidad, Inocuidad y Calidad Agroalimentaria (SENASICA) has streamlined approvals for climate-adapted chemistries, further accelerating product penetration and making early-season protection a baseline agronomic practice.

Carbon-Credit Programs Rewarding Treated Seed for Stand Uniformity

Mexico’s linkage to international carbon markets monetizes uniform emergence by reducing the need for replanting operations. Digital platforms verify stand counts via satellite, assigning credits that offset input costs. Inoculants delivering vigorous root development win favor because they carry no chemical-residue penalties. Consequently, the Mexico seed treatment market experiences a structural demand pull for bio-coated seed that combines agronomic consistency with measurable emissions reductions. The convergence of precision agriculture with carbon accounting creates premium pricing opportunities for seed treatment technologies that deliver both agronomic and environmental benefits.

Mandatory Re-registration of Neonics Driving Premium Alternative Chemistries

Comisión Federal para la Protección contra Riesgos Sanitarios (COFEPRIS) now requires comprehensive environmental and pollinator-impact dossiers for neonicotinoid renewals, prompting a pivot toward isocycloseram and diamide insecticides. Multinationals with deep regulatory resources speed alternatives to market, while smaller distributors retrench. The scarcity of re-registered neonics boosts short-term prices, supporting the growth of the Mexico seed treatment market as growers pay premiums for compliant formulations that safeguard export channels. The transition period creates temporary supply constraints that support premium pricing for approved alternatives.

Surge in Coatings for Regenerative Farming Systems

Consumer demand for residue-free produce and the spread of organic certification accelerate interest in microbial seed coatings. Trials in Guanajuato showed 44–46% yield gains when Pseudomonas fluorescens, Azospirillum brasilense, and Bacillus subtilis strains were combined in endophytic formulations[2]Source: Gutiérrez-Benicio et al., “Growth, Health, Quality, and Production of Onions Inoculated with Systemic Biological Products,” Microorganisms, mdpi.com. Lower regulatory hurdles for speed commercialization, making bio-seed treatments a cornerstone of regenerative agriculture and adding depth to the Mexico seed treatment market. Regulatory pathways for products remain more streamlined than synthetic alternatives, encouraging innovation in microbial formulations. The trend aligns with consumer demand for residue-free produce and export market requirements, particularly in organic-certified production systems.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-level neonic restrictions | -0.8% | Regional, with the strongest impact in environmentally sensitive zones | Short term (≤ 2 years) |

| Farmer uncertainty on Return on Investment (ROI) as corn-soy margins tighten | -1.2% | National, with the highest impact in commodity-focused regions | Medium term (2-4 years) |

| Limited availability of untreated GMO seed for risk-based IPM | -0.9% | National, affecting integrated pest management adoption | Long term (≥ 4 years) |

| USDA research staffing cuts slowing label innovation | -0.6% | Cross-border, affecting technology transfer and regulatory harmonization | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

State-Level Neonic Restrictions

Ecologically focused states impose limitations exceeding federal rules, fragmenting product labeling and forcing region-specific logistics. Added compliance raises distributor inventory costs, constraining short-run supply and tempering growth in the Mexico seed treatment market[3]Source: U.S. Environmental Protection Agency, “Pesticide Product Registration; Receipt of Applications for New Active Ingredients,” federalregister.gov. Yet the same measures open windows for diamide alternatives, somewhat offsetting lost neonic volume. The restrictions particularly impact seed treatment applications where neonicotinoids historically provided cost-effective systemic protection.

Farmer uncertainty on Return on Investment (ROI) as corn-soy margins tighten

Post-GM corn restrictions have left growers facing yield limitations while managing increasing fertilizer costs, which erode their margins. Financial Institutions Regulatory Act's (FIRA) cost calculators now flag seed treatment as a discretionary expense, pressuring suppliers to document payback within a single season. Value-oriented, single-mode coatings are gaining traction, slowing the adoption of premium stacks and restraining the expansion of the Mexico seed treatment market. The trend favors value-oriented formulations and companies that can demonstrate clear economic returns through field demonstration programs.

Segment Analysis

By Product Type: Insecticides Lead Amid Chemistry Transitions

Insecticide coatings retained 46.20% of the Mexico seed treatment market share in 2024. The neonic reset channels demand toward chlorantraniliprole, cyantraniliprole, and early-stage isocycloseram, collectively expanding the Mexico seed treatment market size for high-efficacy actives. Fungicides remain a mature segment, yet SDHI classes keep values buoyant as growers seek broad-spectrum protection. Nematicides illustrate the fastest climb, posting an 11.80% CAGR on the back of moisture-stress root-lesion outbreaks.

Bio-derived plant growth regulators and micronutrient polymers are increasingly incorporated into customized on-planter additive kits, enhancing revenue per hectare. The decline in generic chlorantraniliprole prices has led to a rise in domestic formulation tolling, enabling local blenders to provide competitively priced diamide packages. However, stringent COFEPRIS dossier requirements continue to restrict new market entrants, maintaining incumbents' 70% share of the Mexico seed treatment market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Formulation Type: Liquid Dominance Faces Coating Innovation

Liquid flowable products held 67.20% of the Mexico seed treatment market share in 2024, aided by mechanized farms that value pump-friendly viscosities and precise dosing control. Existing seed-conditioning lines in Sinaloa, Jalisco, and Guanajuato are optimized for liquid throughput, reinforcing incumbent preferences and anchoring the Mexico seed treatment market size at processing hubs. Powder and granular formats remain serviceable in niche scenarios, yet dust concerns and handling inefficiencies gradually erode their footprint.

Polymer-based coatings chart the fastest path forward at a 9.70% CAGR through 2030, propelled by microplastic-reduction mandates and moisture-management advantages in drought-prone soils. Lucent BioSciences’ Nutreos biodegradable micronutrient layer exemplifies the sustainability-led innovation wave, demonstrating gains in seed flowability alongside environmental compatibility in 2024. Advanced polymer matrices synchronize active-ingredient release with critical phenological stages, helping growers navigate Mexico’s erratic precipitation.

By Crop Type: Grains Drive Volume, Specialty Crops Fuel Growth

Grains and cereals accounted for 48.50% of the Mexico seed treatment market size in 2024 on the strength of corn and robust durum wheat programs in Sonora. Yield anxiety linked to GM corn prohibitions nudges growers toward multi-site fungicidal and insecticidal suites, even as output inches downward. Fruits and vegetables exhibit a 9.40% CAGR, carving headroom for coatings suited to export-grade berries and avocado orchards.

Oilseeds and pulses enjoy policy tailwinds, which subsidize certified bean seed and associated microbial dressings. Commercial crops, such as cotton, tap diamide, and biofungicide blends, are used to satisfy United States residue thresholds, whereas turf and ornamentals sustain a niche but steady uptake around hospitality hubs. Across all categories, WhatsApp extension groups accelerate knowledge diffusion, indirectly boosting overall adoption in the Mexico seed treatment industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Mexico seed treatment market exhibits strong regional concentration patterns driven by agricultural production density and infrastructure development. Northern states, including Sinaloa, Sonora, and Chihuahua, dominate market volume through large-scale grain production and advanced mechanization levels that facilitate seed treatment adoption. Sinaloa projects a high yield of beans in 2025, channeling capital toward SDHI and diamide packages to secure export-class grade.

The Bajío region, encompassing Guanajuato, Jalisco, and Michoacán, represents the fastest-growing market segment through diversified crop production and proximity to processing facilities. Western states benefit from export-oriented fruit and vegetable production that demands premium seed treatment technologies to meet international quality standards. Central Mexico, including the State of Mexico and surrounding areas, serves as a distribution hub while maintaining significant production of specialty crops and protected agricultural systems. The region's greenhouse expansion drives demand for precision seed treatment applications compatible with controlled environment production.

Southern and southeastern states exhibit lower adoption rates due to the prevalence of smallholder farming structures and limited access to credit and technical services. However, government programs, including PEMEX's (Mexican Petroleum) fertilizer distribution to over 2 million farmers, create opportunities for integrated input packages that include seed treatments. Climate change impacts vary regionally, with northern areas facing increased drought stress while southern regions experience altered precipitation patterns that affect disease pressure and treatment timing requirements.

Competitive Landscape

The Mexico seed treatment market exhibits moderate consolidation, with multinational corporations controlling a major share through established distribution networks and regulatory expertise. Bayer’s USD 176 million capital expenditure targets seed-conditioning expansions across Sinaloa, Jalisco, and Guanajuato, signaling a bid to strengthen supply chain control in 2022. UPL’s 2023 launch of a Global NPP Research Center in Mexico underscores localization as a differentiator. Syngenta’s divestiture of the FarMore vegetable platform to Gowan SeedTech in late 2024 reflects portfolio realignment that frees capital for next-generation actives.

Regulatory competency emerges as the pivotal success factor, with COFEPRIS approval queues stretching past 12 months for new molecules. Firms that maintain in-country toxicology teams and digital dossier pipelines secure a decisive edge. Hardware partnerships round out the strategy, and DJI’s Agras T40 drones have trimmed application time on agave by up to 95%, opening service-provider revenue streams tied to specific seed-treatment SKUs.

Start-up innovators like Lucent BioSciences penetrate via biodegradable coatings that bypass microplastic bans, although scaling remains contingent on toll-manufacturing alliances with incumbents. Opportunities exist in integrated digital advisory services, particularly for companies that can navigate Mexico's complex regulatory environment while delivering measurable agronomic and economic benefits to cost-sensitive farmers.

Mexico Seed Treatment Industry Leaders

-

Corteva Agriscience

-

FMC Corporation

-

Syngenta Group

-

Bayer AG

-

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Mexico’s Chamber of Deputies banned GM corn cultivation, intensifying demand for conventional seed enhancements while stoking supply-chain uncertainty for trait-linked treatments.

- January 2025: Secretariat of Environment and Natural Resources (SEMARNAT) rolled out the Environmental Electronic Platform (VEA), digitizing permit submissions and accelerating paperwork for seed treatment facilities.

- January 2024: Lucent BioSciences launched Nutreos, a biodegradable micronutrient seed coating, as a microplastic-free alternative to conventional treatments. The company targets environmental compliance and sustainable agriculture markets, with planned manufacturing expansion in North America.

Mexico Seed Treatment Market Report Scope

Seed treatment is a process where chemicals are used to treat or dress seeds before planting. The Mexico Seed Treatment Market is segmented by Product Type (Insecticides, Fungicides, and Nematicides) and Crop Type (Grains & Cereals, Oilseeds & Pulses, Fruits & Vegetables, Commercial Crops, and Turf & Ornamentals). The report provides market size and forecasts in USD value for these segments.

By Product Type

| Insecticides |

| Fungicides |

| Nematicides |

| Other Chemical Classes |

By Formulation Type

| Liquid Flowable |

| Dry Powder |

| Polymer-based Coating |

| Microencapsulated |

By Crop Type

| Grains and Cereals |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Commercial Crops |

| Turf and Ornamentals |

| By Product Type | Insecticides |

| Fungicides | |

| Nematicides | |

| Other Chemical Classes | |

| By Formulation Type | Liquid Flowable |

| Dry Powder | |

| Polymer-based Coating | |

| Microencapsulated | |

| By Crop Type | Grains and Cereals |

| Oilseeds and Pulses | |

| Fruits and Vegetables | |

| Commercial Crops | |

| Turf and Ornamentals |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Mexico seed treatment market in 2025?

The market is valued at USD 320 million in 2025 and is forecast to reach USD 457.27 million by 2030.

What is driving recent growth in treated seed adoption?

Climate-induced early planting risks, neonic re-registration pressures, and rising demand for biological coatings collectively fuel uptake.

Which segment grows fastest through 2030?

Nematicide coatings expand at an 11.80% CAGR, propelled by heightened soil-borne pathogen incidence in moisture-stressed regions.

How do GM corn restrictions affect demand for seed treatments?

The cultivation ban removes built-in trait protection, making external seed treatments a primary defense against pests and diseases.

What role do carbon credits play in market expansion?

Verified stand uniformity from treated seed enables growers to monetize carbon savings, effectively subsidizing input costs.

Who are the leading companies?

Bayer AG, Syngenta Group, Corteva Agriscience, FMC Corporation and UPL Limited collectively hold majority of the market share, leveraging regulatory capacity and localized R&D investments.

Page last updated on: