Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

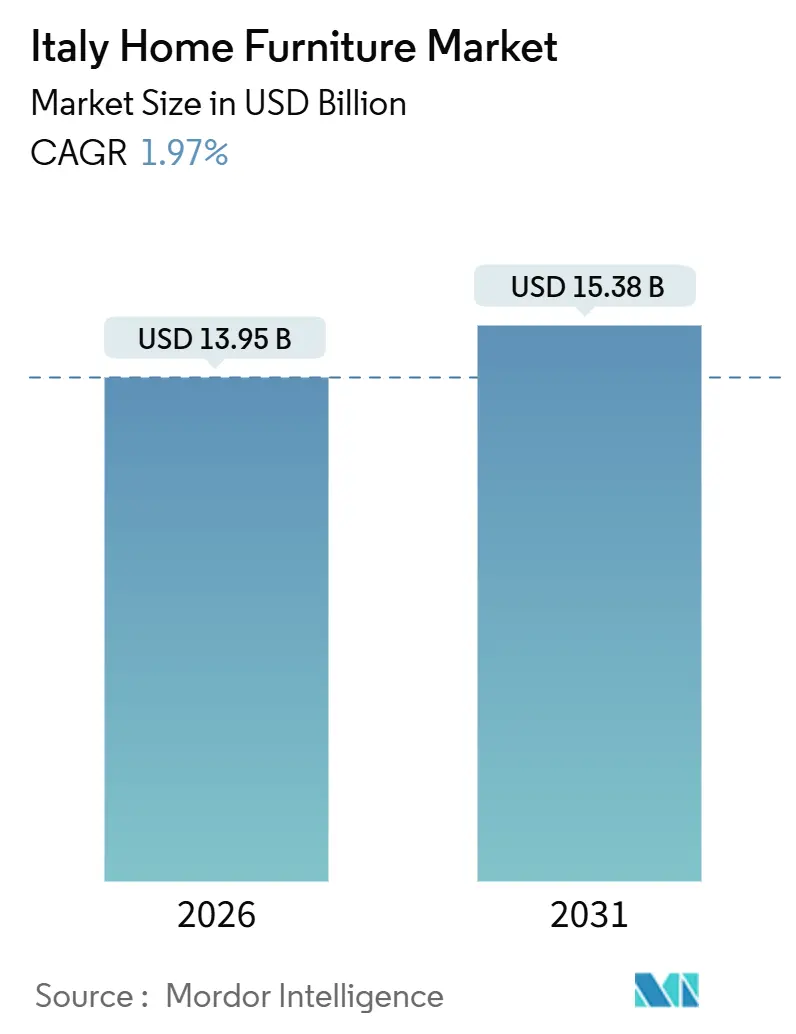

| Market Size (2026) | USD 13.95 Billion |

| Market Size (2031) | USD 15.38 Billion |

| Growth Rate (2026 - 2031) | 1.97% CAGR |

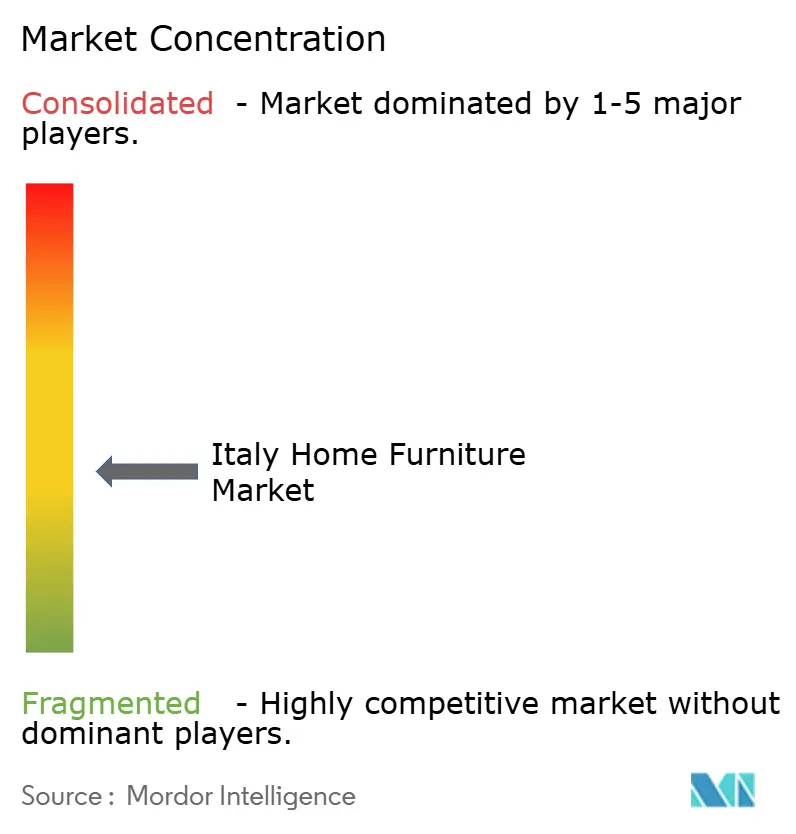

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Home Furniture Market Analysis by Mordor Intelligence

The Italy home furniture market size stands at USD 13.95 billion in 2026 and is projected to reach USD 15.38 billion by 2031, reflecting a forecast CAGR of 1.97%. This trajectory signals a measured normalization after the post-pandemic surge, with structural demand supported by renovation-linked incentives and resilient premium spending that distinguishes the Italy home furniture market from broader manufacturing cycles. Regulatory tailwinds, including the Minimum Environmental Criteria frameworks effective for public purchases, embed recyclability, low emissions, and disassembly into product development, lifting compliance and sustainability standards in the Italy home furniture market. Policy execution under the National Strategy for the Circular Economy and related implementation plans sustains circular design priorities while preparing producers for wider EU product rules. Digital traceability and safety obligations under EU product safety frameworks apply equally to e-commerce and stores, which helps the Italy home furniture market reduce perceived risk in online purchases as platforms professionalize operations.

Key Report Takeaways

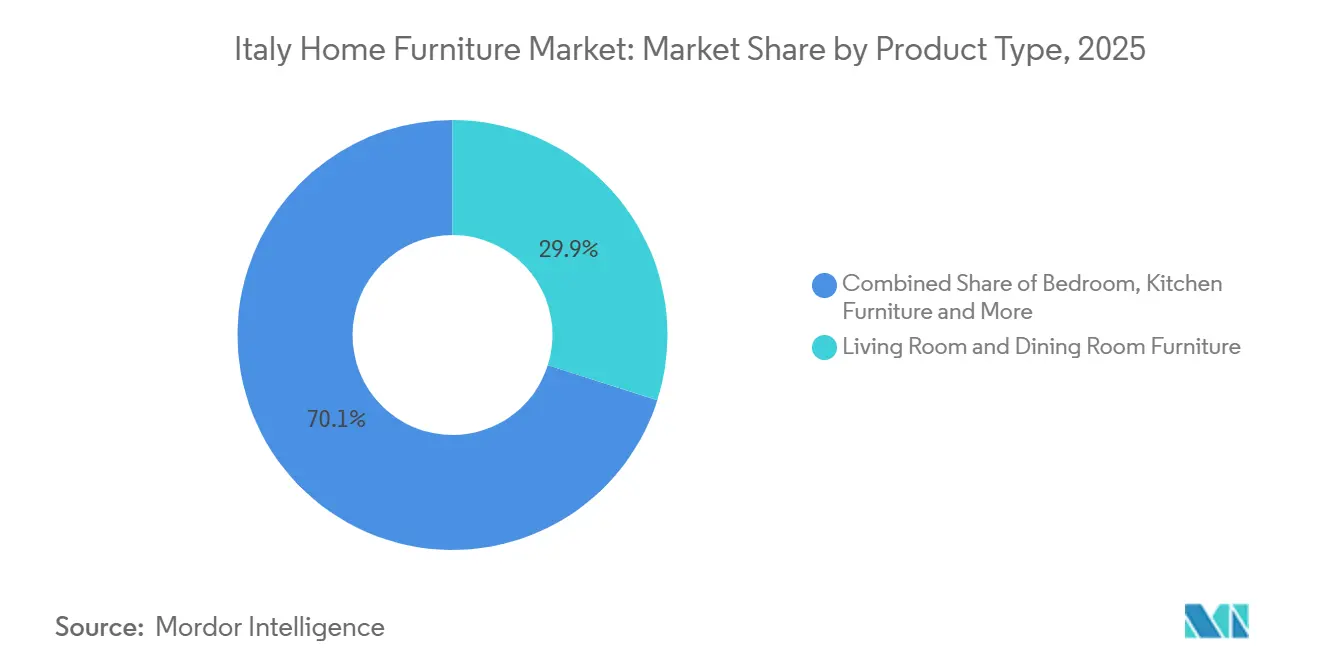

- By product type, living room and dining room furniture captured 29.91% of the Italy home furniture market share in 2026 and bedroom furniture is projected to grow at 3.73% CAGR between 2026-2031.

- By material, wood captured 52.23% of the Italy home furniture market share in 2026 and plastic and polymer are projected to grow at 3.20% CAGR between 2026-2031.

- By price range, the mid-range segment captured 48.93% of the Italy home furniture market in 2026 and the premium segment is projected to grow at 3.36% CAGR between 2026-2031.

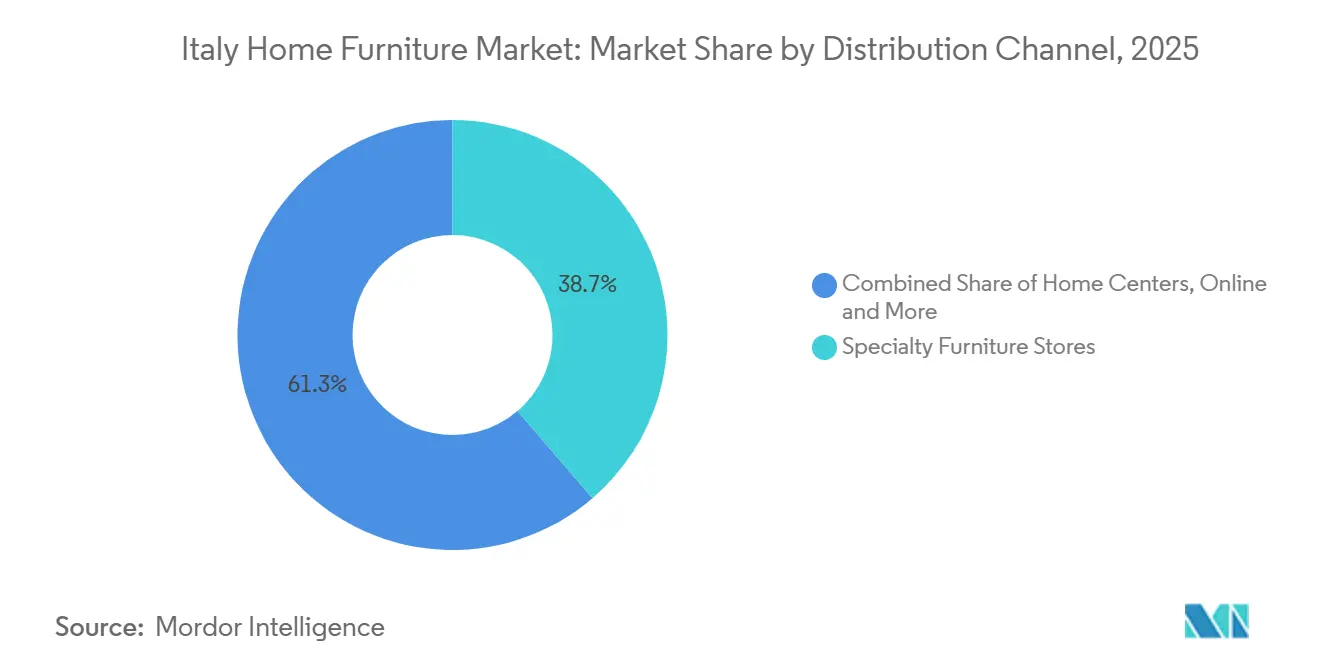

- By distribution channel, specialty furniture stores captured 38.72% of the Italy home furniture market in 2026 and online channels are projected to grow at 4.24% CAGR between 2026-2031.

- By geography, North Italy captured 52.34% of the Italy home furniture market in 2026 and Central Italy is projected to grow at 3.27% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Home Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extension of "Furniture Bonus" tax relief | +0.4% | North Italy & Central Italy | Short term (≤ 2 years) |

| Growing penetration of online furniture retail | +0.5% | National, with early gains in Milan, Rome, Turin | Medium term (2-4 years) |

| Rising renovation activity in historic housing stock | +0.3% | Central Italy, spill-over to North Italy | Medium term (2-4 years) |

| Upsurge in demand for modular, space-saving solutions | +0.3% | National, concentrated in metropolitan areas | Short term (≤ 2 years) |

| Ageing population driving demand for senior-friendly ergonomics | +0.2% | National, stronger in North Italy | Long term (≥ 4 years) |

| National circular-economy targets boosting recycled-material furniture | +0.3% | National, led by FederlegnoArredo consortium | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extension of "Furniture Bonus" Tax Relief

The Furniture Bonus remains active through December 31, 2025, maintaining a 50% personal income tax deduction for purchases linked to renovation with a maximum eligible spend of EUR 5,000 (USD 5207.8) per household, which keeps replacement cycles steady even as new-build activity moderates[1]SALONEMILANO.IT https://www.salonemilano.it/en/articles/furniture-bonus-2025-how-it-works-and-how-make-most-it. . Budget rules confirm the deduction structure and multi-year installment mechanism, which sustains affordability and supports the Italy home furniture market during a period of macro normalization. Istat recorded a contraction in housing investment in early 2025 due to the phaseout of broader construction incentives; however, non-residential investment increased strongly, which stabilized order flow for contract and office producers while household demand remained anchored by the Furniture Bonus. Eligibility requirements and traceable payment rules channel consumer decisions toward compliant models and energy-efficient appliances that often trigger coordinated purchases of kitchens, bedrooms, and living room sets in the Italy home furniture market. Regions with higher incomes, notably in the North and parts of the Center, benefit more from the incentive’s structure because households can pre-finance renovation and then recover deductions over time, which reinforces the regional concentration of sales in the Italy home furniture market.

Growing Penetration of Online Furniture Retail

Digital infrastructure, improved last-mile services, and richer visualization tools are making online purchasing more practical for large items, which supports the steady expansion of e-commerce in the Italy home furniture market. Online platforms are subject to EU product safety and traceability requirements, including the presence of a responsible person established in the EU and standardized compliance documentation, which raises trust and aligns with consumer expectations for safety and sustainability[2]EUROFINS.COM https://www.eurofins.com/toys-hardlines/resources/articles/furniture-compliance-in-the-european-union.. Compliance with REACH reporting through the SCIP database also increases chemical transparency for upholstered seating, storage, and children’s furniture, which has become an important reassurance for digital buyers who cannot evaluate products physically before purchase in the Italy home furniture market. Retailers that integrate delivery to the floor, assembly options, and flexible returns narrow the experiential gap with stores, which is especially relevant for urban households that prioritize convenience. As these service layers standardize, purchase friction declines, and steady share gains for online channels continue to layer on top of the core base of specialty stores in the Italy home furniture market.

Upsurge in Demand for Modular, Space-Saving Solutions

Housing constraints in large metropolitan areas and hybrid work patterns are encouraging households to maximize functionality per square meter using modular, transformable, and wall-mounted furniture, which adds momentum to innovative systems across living and bedroom environments in the Italy home furniture market. Industry policy and the National Strategy for the Circular Economy prioritize eco design, durability, reparability, and reuse, which dovetails with modular design principles that extend useful life as spaces and needs evolve[3]MASE.GOV.IT https://www.mase.gov.it/portale/documents/d/guest/relazione-cronoprogramma-sec_31_10_2025-eng-pdf. . The European Environment Agency profile confirms Italy’s advanced positioning on circularity, which strengthens the integration of recovered materials into modular panel systems and supports local innovation in design for disassembly[4]EEA.EUROPA.EU https://www.eea.europa.eu/en/topics/in-depth/circular-economy/country-profiles-on-circular-economy/circular-economy-country-profiles-2024/italy_2024-ce-country-profile_final.pdf/@@download/file. Dedicated funding in 2025 for the wood furniture supply chain to adopt machinery, digital technologies, and sustainable processing further enables scalable mass customization for space-saving solutions in the Italy home furniture market. As transformable furniture diffuses from premium segments into mid-range collections, adoption broadens and reinforces the Italy home furniture market’s product mix shift toward adaptable systems.

Ageing Population Driving Demand for Senior-Friendly Ergonomics

Italy’s demographic profile creates a durable need for furniture that supports mobility, posture, and accessibility, which expands opportunities in seating, bedroom, and storage categories with features that assist daily living in the Italy home furniture market. Institutional demand from assisted living and care facilities requires compliance with national fire reaction and durability standards for upholstered products, which ensures that contract lines incorporate safety and cleanability without sacrificing comfort. Public procurement governed by Minimum Environmental Criteria pushes developers toward products that combine recycled content, low emissions, and design for disassembly, which aligns well with the long life and serviceable design needed for senior environments. For residential settings, age-adaptive solutions focus on aesthetics as well as function, which preserves dignity and avoids institutional cues while meeting mobility needs within the Italy home furniture market. The evolving policy landscape in Europe that will formalize durability and repairability through product rules also reinforces the direction of travel for senior-friendly furniture designed to last and be serviced over time.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of lumber, metals, and upholstery inputs | -0.4% | National, acute in export-dependent North | Short term (≤ 2 years) |

| Global supply-chain disruptions are lengthening lead times | -0.3% | National, export-oriented firms in Veneto, Friuli-Venezia Giulia | Medium term (2-4 years) |

| Shrinking average dwelling sizes are limiting bulky furniture demand | -0.2% | Metropolitan areas, Milan, Rome | Long term (≥ 4 years) |

| Shortage of skilled artisans is inflating labour costs | -0.3% | National, critical in Brianza and Manzano districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Lumber, Metals, and Upholstery Inputs

Producers face persistent volatility across wood, metal, and textile inputs, which complicates pricing and compresses margins in the Italy home furniture market when retail pass-through is limited. Firms use long-term contracts, selective vertical integration, and greater use of recycled materials to mitigate cost shocks, which helps stabilize panel-based lines and reduces exposure to virgin inputs. Strengthening domestic capabilities through 2025 measures targeting machinery, digitalization, and sustainable processing for wood and forestry operations should also help build resilience over time in the Italy home furniture market. Italy’s high circular material use and strong recovered wood flows into chipboard panels support cost control strategies for case goods, which helps balance commodity cycles. Over the forecast period, the combination of recycled inputs and targeted investments should temper the restraint on the Italy home furniture market even as global commodity conditions remain variable.

Shortage of Skilled Artisans Inflating Labour Costs

Succession gaps and a declining artisan base increase wage pressure for in-demand skills in joinery, upholstery, and finishing, which creates selective bottlenecks for bespoke and high finish production in the Italy home furniture market. Larger firms deploy automation in repetitive steps to preserve scarce craftsmanship for high-value stages, while smaller workshops rely on specialization and service quality to defend niches. Training and upskilling are scaling through academic and association efforts with a focus on eco design and transparency competencies that are necessary under sustainability frameworks, which support workforce renewal in the Italy home furniture market. Regional clusters with dense furniture ecosystems continue to attract and retain skills, and the sector’s export orientation sustains demand for high-quality workmanship. This restraint is likely to persist through the forecast horizon, although process investments and the maturing training pipeline should progressively reduce the pressure on the Italy home furniture market.

Segment Analysis

By Product Type: Living Room and Dining Room Furniture Commands Share; Bedroom Furniture Accelerates

Living room and dining room furniture accounts for 29.91% share in 2026, reflecting the central place of social and hosting spaces in Italian households and sustained aesthetic spending in the Italy home furniture market. The bedroom segment holds a smaller base in 2026 but has the fastest trajectory with a 3.73% CAGR through 2031 as hybrid work increases the need for multipurpose layouts in the Italy home furniture market. Category design and specification continue to align with public procurement rules for materials and emissions, which indirectly shape private market expectations on quality and sustainability. Steady household income trends and renovation incentives reinforce coordinated purchases across seating, tables, storage, and bedroom systems in the Italy home furniture market.

Bedroom’s growth reflects the blend of sleeping and working needs, which prioritizes ergonomics, integrated storage, and light footprint desks that do not overcrowd smaller rooms in the Italy home furniture market. Home office furniture adjacent to the bedroom upgrades benefits from attention to posture, mobility, and material performance, which is consistent with a broader shift to functional comfort. Kitchen and bathroom maintain stable replacement cycles that are closely tied to renovations and incentive-driven upgrades, while outdoor lines retain a loyal base with seasonal patterns that are well understood by retailers. The Italy home furniture industry competes on design, finish quality, and compliance alongside price, and this balance continues to define category strategies in the forecast period. As the Italy home furniture market matures, product differentiation centers on adaptability and easy maintenance, which enhance longevity and repeat purchase satisfaction.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Wood Dominates; Plastic and Polymer Gain Ground on Bio-Based Innovations

Wood leads with 52.23% share in 2026, supported by strong recycled wood panel flows that reduce dependence on virgin timber and underpin competitive case goods in the Italy home furniture market. Italy’s circular material systems channel recovered wood into chipboard, with a high recycling performance that sustains the panel supply needed by furniture producers. Certification and low-emission requirements in public procurement have become baseline expectations across many residential lines, which raises the material quality bar. Solid wood lines remain positioned in premium and heritage-led ranges where durability, repairability, and tactile value justify higher prices in the Italy home furniture market.

Plastics and polymers post the fastest growth with a 3.20% CAGR through 2031, driven by innovations in recycled and bio-based resins that align with circularity targets and industrial regeneration. Producers are integrating polymer components in seating, storage, and accessories to achieve strength-to-weight benefits and streamlined maintenance while improving end of life outcomes through design for disassembly. Metals continue to serve contract, office, and outdoor applications where durability and corrosion resistance are essential, and coatings shift toward low VOC and water based finishes. The Italy home furniture industry balances multi material construction with simpler disassembly pathways to meet procurement and eco design expectations. Over the forecast period, material strategy will remain a lever for differentiation in the Italy home furniture market, especially where recycled content and emissions profiles factor into buyer criteria.

By Price Range: Mid-Range Anchors Volume; Premium Segment Accelerates on Craftsmanship Appeal

The mid-range segment captures 48.93% share in 2026, reflecting value-seeking preferences for contemporary designs, reliable quality, and credible sustainability attributes in the Italy home furniture market. This tier absorbs steady renovation-linked demand and balances price, finish, and service support across specialty stores and online channels. Online growth adds selection and convenience that complement store-based advice and services, which sustains the mid-range volume core in the Italy home furniture market. The economy tier remains relevant for entry buyers and renters, and compliance rules enhance baseline safety and traceability across all price points.

The premium segment records the fastest growth at a 3.36% CAGR through 2031, supported by brand heritage, design leadership, and sustainability credentials that command pricing power in the Italy home furniture market. High-end demand is reinforced by Italy’s global design reputation and the expansion of export channels for Bello e Ben Fatto products, which broaden the addressable base for premium lines. Premium manufacturers continue to invest in materials transparency and EPD pathways that are increasingly valued by professional buyers and consumers. Over time, the premium tier’s design-led innovations diffuse into mid-range collections, which raises product expectations across the Italy home furniture market and supports broader quality upgrades.

By Distribution Channel: Specialty Stores Retain Share; Online Surges on Digital Infrastructure

Specialty furniture stores hold 38.72% share in 2026, reflecting the enduring value of curated displays, sales consultation, and after-sales services in the Italy home furniture market. These retailers anchor discovery and specification for complex purchases and coordinate delivery and assembly, which remains central for multi-piece rooms. Specialty networks continue to partner with designers and contractors, which keeps them relevant for renovation and small contract projects in the Italy home furniture market. Policy-driven sustainability criteria influence assortments and private label development as retailers align with buyer expectations.

Online channels deliver the fastest expansion with a 4.24% CAGR through 2031, supported by improved logistics, augmented reality visualization, and aligned compliance practices that strengthen consumer trust in the Italy home furniture market. EU product safety frameworks require a responsible person in the Union and standardized traceability information, which supports the shift to digital carts for large items. Retailers that offer delivery to the floor, assembly services, and flexible returns narrow the gap with showrooms, which supports the omnichannel direction of the Italy home furniture market. Public procurement expectations on materials and emissions further shape both store and online assortments without constraining innovation.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

North Italy leads with a 52.34% share in 2026, anchored by dense supply chains, export-ready capabilities, and premium brand clusters that continue to draw investment and talent in the Italy home furniture market. The region’s firms leverage process automation and design capacity to serve domestic renovations and contract orders, supported by stable incentive frameworks that encourage replacement cycles. NRRP projects enhance infrastructure and logistics, which help northern manufacturers maintain delivery reliability for export and domestic customers in the Italy home furniture market. The area’s combination of industrial scale and premium craftsmanship supports balanced portfolios across mid-range and luxury categories.

Central Italy grows fastest with a 3.27% CAGR through 2031, benefiting from cultural heritage tourism recovery, boutique hospitality refurbishments, and artisan networks that command premium pricing in the Italy home furniture market. Renovation intensity in historic centers lifts demand for custom joinery and period-sensitive interior solutions, with eco design and low-emission materials increasingly used to meet contemporary standards. Infrastructure improvements under the recovery program strengthen regional connectivity and shorten lead times, which expand the viable reach of central clusters into wider domestic and export channels in the Italy home furniture market. The region’s producers blend artisan provenance with compliance, which resonates with higher income buyers and professional specifiers.

South Italy and Islands post a 2.84% CAGR from a smaller base, with growth supported by remote work setups at home, selective contract opportunities in hospitality, and pockets of upholstery expertise that supply both domestic and export demand in the Italy home furniture market. Spending levels reflect local income and access to credit, yet the combination of online assortment breadth and policy-aligned product standards raises product availability and trust. As procurement and eco design norms continue to standardize, southern manufacturers can leverage niche specializations while improving documentation and certification, which supports prudent capacity additions in the Italy home furniture market. Public investment in logistics and energy projects under the recovery framework should provide incremental operating advantages as projects reach completion.

Competitive Landscape

The Italy home furniture market features a balanced mix of industrial-scale producers and artisan-driven firms, with premium brands, kitchen specialists, and upholstery leaders serving complementary segments across domestic and export channels. Product strategies emphasize design, material transparency, and durability to align with procurement and eco design expectations that are now mainstream in the Italy home furniture market. EU safety and compliance regimes apply across channels, which support quality parity online and in stores and reinforce documented assurance for buyers. Sector investments in digital production and mass customization capabilities continue where scale supports capital deployment, while specialized workshops defend niches through bespoke craftsmanship and service.

Manufacturers are aligning with the furniture PCR framework launched in 2024 to scale EPDs, which supports transparent communication of environmental impacts to professional and consumer markets in the Italy home furniture market. Seating and upholstery lines adapt to the revised EN 12520:2024 standard on domestic seating, which updates durability and safety tests that influence design and component selection. Public procurement’s Minimum Environmental Criteria continue to motivate recycled content, low emissions, and circular design, encouraging companies to formalize supplier selection and verification processes in the Italy home furniture market.

Policy developments and targeted funding reinforce competitive dynamics by easing technology adoption and strengthening upstream wood processing, which can improve material availability and cost control in the Italy home furniture market. The recovery plan enhances rail, road, and digital infrastructure that also supports exports and domestic logistics reliability, improving service levels for contract projects and retail networks. As Digital Product Passport requirements under EU eco design rules take shape, early adopters in the Italy home furniture market are positioned to benefit from supply chain visibility and streamlined documentation for tenders and cross-border trade.

Italy Home Furniture Industry Leaders

IKEA Italia

Natuzzi S.p.A

Poltronesofà S.p.A.

Scavolini S.p.A.

Calligaris S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Dexelance completed the acquisition of 65% of Mohd, integrating a major player in global design retail with revenues around USD 82.34 (EUR 70 million) in 2024.

- April 2025: During Milan Design Week, Natuzzi Italia launched the "Rooted in Harmony" collection, featuring new pieces like the Amama island furniture by Andrea Steidl and extensions to the Memoria bedroom line by Karim Rashid.

- April 2025: B&B Italia presented expansions to its outdoor collections at Milan Design Week, emphasizing innovative designs for enhanced outdoor living.

- April 2025: Minotti showcased new upholstered furniture with organic lines and fluid forms, including updates to seating and modular systems at Salone del Mobile.

Italy Home Furniture Market Report Scope

Home furniture comprises all movable articles or apparatus, like chairs, tables, sofas, mattresses, and other items for equipping a residence.

The Italy Home Furniture Market Report is Segmented by Product (Living Room & Dining Room, Bedroom, Kitchen, Home Office, Bathroom, Outdoor, Other Furniture), Material (Wood, Metal, Plastic & Polymer, Others), Price Range (Economy, Mid Range, Premium), Distribution Channel (Home Centers, Specialty Stores, Online, Others), and Geography (North Italy, Central Italy, South Italy & Islands). Market Forecasts are in Value (USD).

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores |

| Online |

| Other Distribution Channels |

By Geography

| North Italy |

| Central Italy |

| South Italy & Islands |

| By Product | Living Room & Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home Office Furniture | |

| Bathroom Furniture | |

| Outdoor Furniture | |

| Other Furniture | |

| By Material | Wood |

| Metal | |

| Plastic & Polymer | |

| Others | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Distribution Channel | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | North Italy |

| Central Italy | |

| South Italy & Islands |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the Italy home furniture market size and growth outlook to 2031?

The Italy home furniture market size is USD 13.95 billion in 2026 and is projected to reach USD 15.38 billion by 2031 at a 1.97% CAGR, reflecting steady normalization after the post pandemic surge.

Which product categories lead demand in the Italy home furniture market?

Living room and dining room furniture lead with 29.91% share in 2026, while bedroom furniture is the fastest mover with a projected 3.73% CAGR through 2031 as homes adapt to hybrid work.

Which materials will see the fastest gains in the Italy home furniture market?

Wood retains leadership with a 52.23% share, and plastic and polymer lines post the fastest growth with a 3.20% CAGR through 2031 as recycled and bio-based resins scale.

How are channels shifting in the Italy home furniture market?

Specialty stores remain primary at 38.72% share in 2026, while online channels expand fastest with a 4.24% CAGR through 2031 on the back of better logistics and compliance led trust.