Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

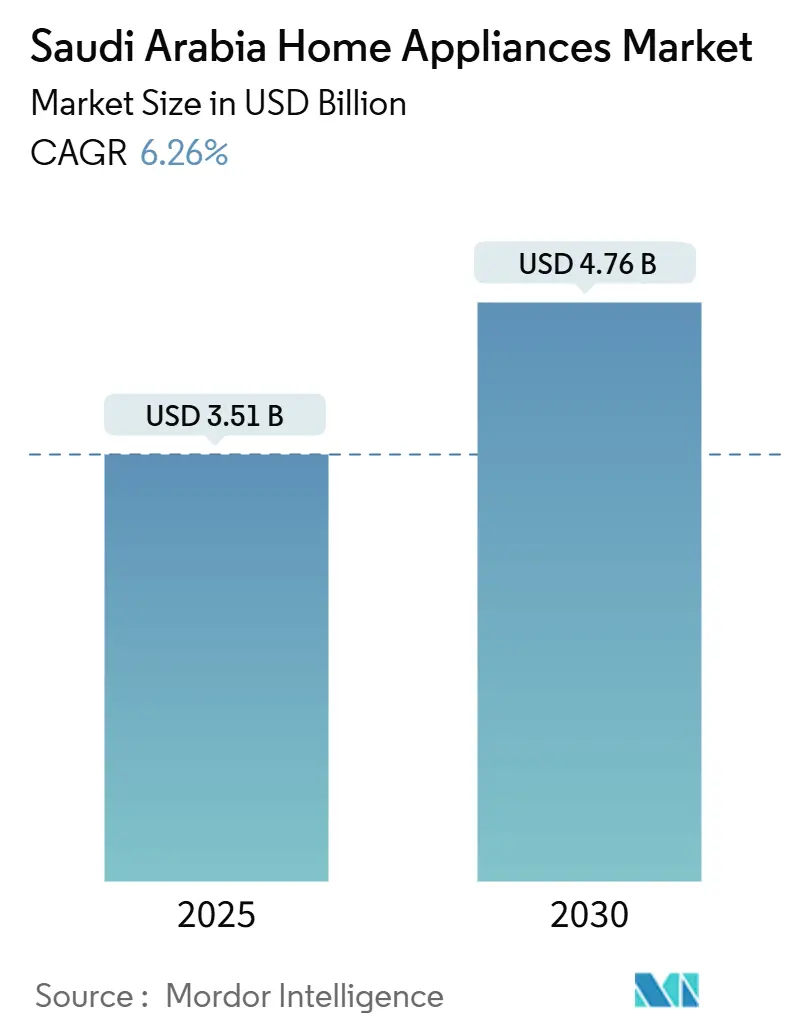

| Market Size (2025) | USD 3.51 Billion |

| Market Size (2030) | USD 4.76 Billion |

| Growth Rate (2025 - 2030) | 6.26% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Home Appliances Market Analysis by Mordor Intelligence

The Saudi Arabia home appliances market size stands at USD 3.51 billion in 2025 and, at a forecast CAGR of 6.26%, is set to climb to USD 4.76 billion by 2030. This momentum mirrors Vision 2030’s economic diversification agenda, which accelerates residential construction, smart-city roll-outs, and infrastructure upgrades across the Kingdom. The surge in giga-projects such as NEOM, Diriyah, and ROSHN developments feeds sustained demand for premium, connected appliances, while stricter Saudi Standards, Metrology, and Quality Organization (SASO) efficiency rules hasten replacement cycles and boost sales of inverter-grade air conditioners and A-rated refrigerators. Disposable-income gains, reflected in national homeownership rising to 65.4% in 2024, encourage premiumization across built-in kitchen suites and smart washing machines. Omnichannel retailing reshapes the competitive field as e-commerce captures incremental share on the back of 32% annual growth in Saudi online spending. Meanwhile, localized production—backed by Alat, MODON, and private-sector joint ventures—reduces import exposure and fosters technology transfer, yet leaves manufacturers exposed to near-term input-cost volatility and logistics hurdles.

Key Report Takeaways

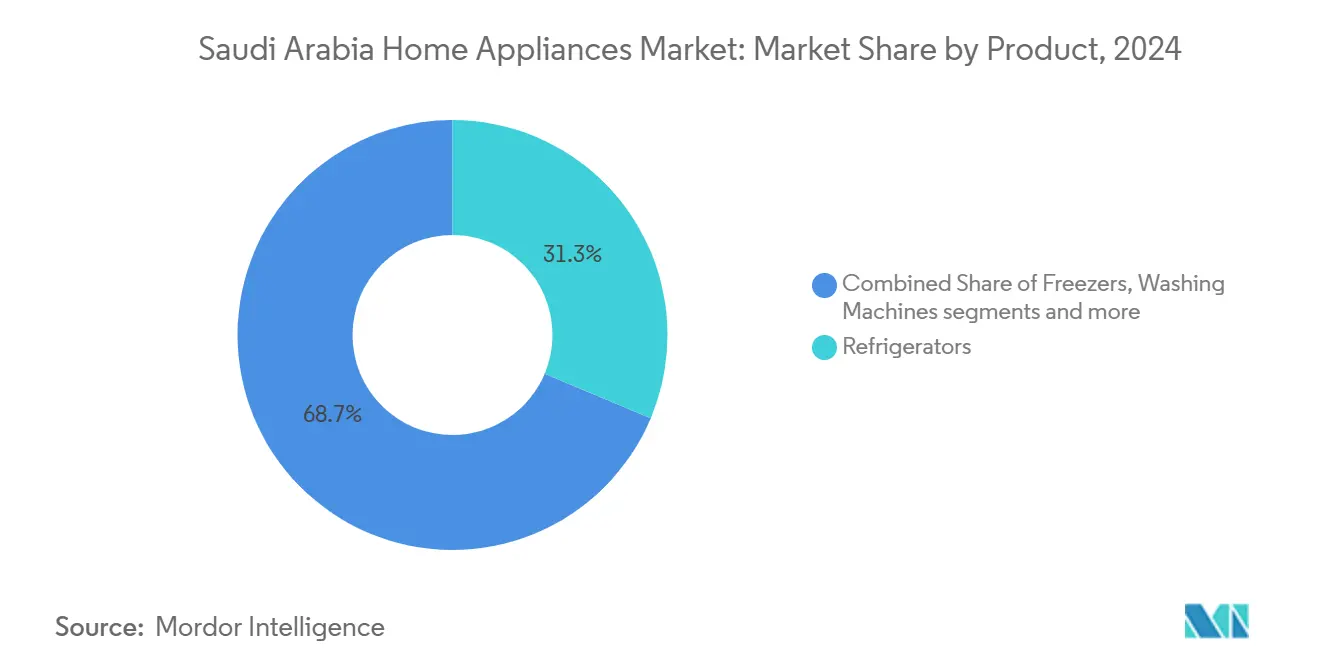

- By product type, refrigerators led with 31.32% of the Saudi Arabia home appliances market share in 2024; air fryers are advancing at a 6.90% CAGR through 2030.

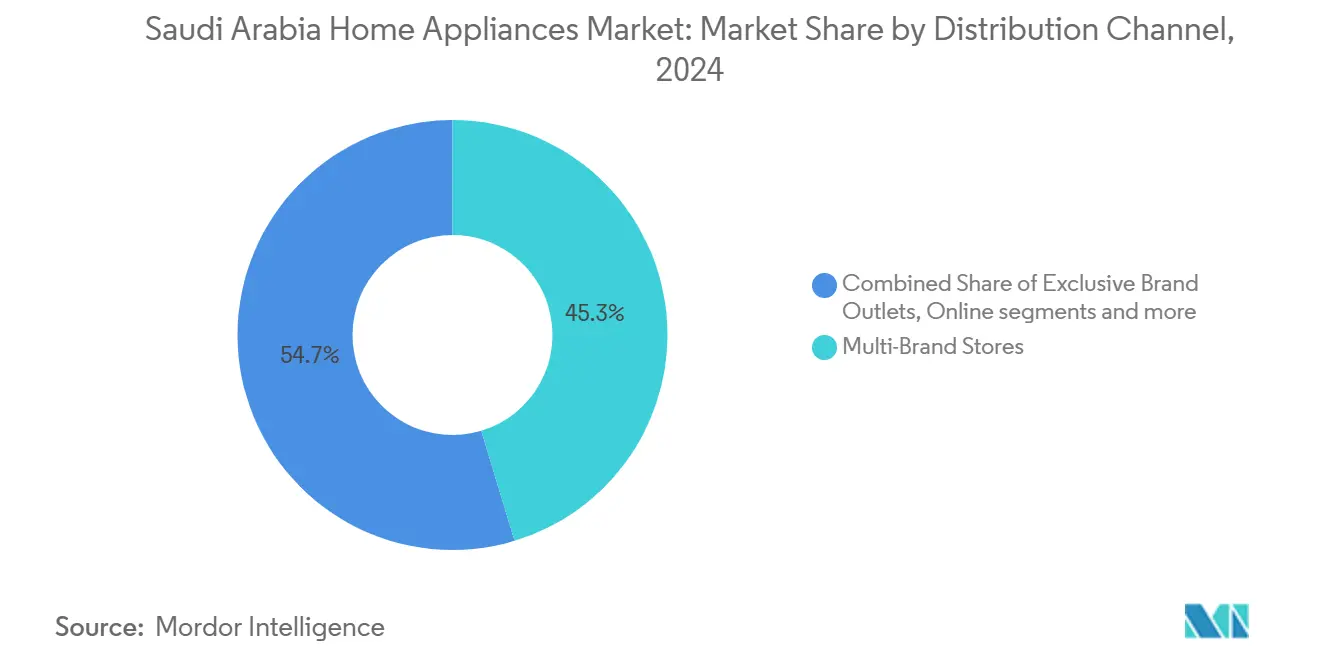

- By distribution channel, multi-brand stores held 45.34% of the Saudi Arabia home appliances market size in 2024, while online retail is expanding at a 7.24% CAGR to 2030.

- By geography, Riyadh Province commanded 31.63% of the Saudi Arabian home appliances market share in 2024; Makkah & Jeddah Provinces are projected to grow at a 6.57% CAGR during the forecast period.

Saudi Arabia Home Appliances Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga-projects accelerating smart-home adoption | +2.1% | National, early gains in NEOM, Riyadh, Diriyah | Long term (≥ 4 years) |

| Rising disposable income & premiumization | +1.8% | National, strongest in Riyadh & Eastern Province | Medium term (2-4 years) |

| Energy-efficiency regulations spurring replacement sales | +1.4% | National, stricter in major cities | Short term (≤ 2 years) |

| E-commerce & omnichannel retail growth | +0.9% | National, the highest in urban centers | Short term (≤ 2 years) |

| Urbanisation & housing expansion | +1.2% | National, Vision 2030 zones | Medium term (2-4 years) |

| Residential solar rollout driving inverter-grade demand | +0.8% | National, focus on NEOM & green cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 giga-projects accelerating smart-home adoption

Giga-projects are embedding smart-infrastructure blueprints that require connected refrigerators, dishwashers, and HVAC systems able to interface with energy-management platforms. NEOM’s ENOWA-operated grid already pilots appliance-level demand response that trims peak loads by remote adjustment[1]“2025 Vision: NEOM’s High-Voltage Smart Grid Blueprint,” saudienergyconsulting.com. The USD 5 billion AI data-center venture between NEOM and DataVolt, slated for 2028, underpins ultra-low-latency services for appliance voice control and predictive maintenance. Six Saudi cities now rank in the IMD Smart-City index, reinforcing the nationwide backbone for IoT-appliance deployment. The state-backed Alat initiative adds a dedicated “Smart Appliances” business unit forecasting 39,000 direct jobs by 2030, catalyzing local design of Matter-enabled devices. Manufacturers that certify appliances for these platforms secure preferred-supplier status in giga-project residential clusters and hospitality zones.

Energy-efficiency regulations spurring replacement sales

SASO broadens minimum-performance thresholds and stand-by power limits across televisions, dryers, and microwaves, referencing EU ErP standards EN 50564 and EN 50643[2]Nemko, “Saudi Arabia introducing Off/Stand-by energy requirements,” nemko.com. Draft SASO 2874 for large-capacity air conditioners introduces 10% tolerance windows between rated and tested performance to smooth compliance pathways while tightening real-world energy use. A national window-A/C swap program launched in April 2025 targets the removal of legacy R-22 units, redirecting demand to inverter-driven R-410A systems that command higher price points. Enforcement success—91% compliance in 2024—has made energy labels a core purchase criterion and nudged households toward premium models with smart energy dashboards.

Rising disposable income & premiumization

Saudi Arabia’s real-estate transaction value escalated from SAR 170 billion to SAR 850 billion in 2024, mirroring wage gains that underpin higher per-home appliance outlays. ROSHN sold out all phase-1 villas at SEDRA and approaches 7,000 cumulative sales across flagship communities, each furnished with built-in cooker suites and side-by-side refrigerators. Foreign investment flows to construction now exceed 16% of inbound capital, elevating demand for imported premium brands. Knight Frank estimates 305,000 new Riyadh homes are required this decade, ensuring a long reflux of replacement and new-install volumes. Premiumization gathers pace in smart refrigerators with steel-alloy internal linings, turbo cooling, and Wi-Fi recipe applications that match evolving dietary trends.

E-commerce & omnichannel retail growth

Online channels leverage fulfillment networks and flexible payment schemes to capture mid-single-digit share gains annually. The washing machine segment alone should log USD 282.8 million in online revenue by 2029 as penetration rises to 72.1%. Retailer Extra integrates app-based order tracking, installation scheduling, and Shariah-compliant installment plans, reducing the perceived risk of large-ticket e-purchases. Multi-brand chains push click-and-collect services, while brands like Samsung augment their Saudi web stores with AI chatbots for model selection. Data analytics from omnichannel traffic feed inventory optimization and predictive promotion calendars, compressing stock-turn cycles and lowering carrying costs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain price volatility | -1.2% | National, higher on import-dependent segments | Short term (≤ 2 years) |

| Water-scarcity rules limiting high-water washers | -0.7% | National, stricter in water-stressed regions | Medium term (2-4 years) |

| Category saturation in tier-1 cities | -0.5% | Riyadh, Jeddah, Dammam metros | Medium term (2-4 years) |

| Domestic-helper culture is dampening certain SDAs | -0.3% | National, higher in affluent areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-chain price volatility

Ocean-freight swings and commodity shocks compress margins as the Kingdom imports most finished goods and sub-assemblies. Additional compliance layers—such as mandatory USB-C chargers from January 2025—raise certification costs and complicate production planning. Chinese OEM overcapacity triggers unpredictable export pricing, demonstrated by lithium-carbonate declines that cut storage-module quotes below 0.5 CNY/Wh, unsettling appliance battery suppliers. While MODON’s USD 14.9 billion in localization deals aims to shorten supply lines, greenfield factories will not contribute meaningful volumes until later in the decade. Brands hedge risk via multi-origin sourcing and currency-hedging programs; however, near-term retail pricing stays sensitive to global cost spikes, tempering volume growth.

Water scarcity rules limiting high-water washers

Per-capita water use near 360 liters daily pressures regulators to tighten water-efficiency scores for laundry appliances[3]U.S. Department of Commerce, “Saudi Arabia – Water,” trade.gov. Labels already cap flow rates for sanitary fixtures, signaling that washer drum capacities above 12 kg may soon face stricter benchmarks. The Ministry of Environment, Water, and Agriculture’s USD 80 billion infrastructure plan underscores urgency, while academic studies reveal 135 million m³ annual residential water consumed for power and cooling alone. Manufacturers innovate with recirculation pumps and sensor-based load detection to satisfy cultural preferences for large-volume abaya washing without breaching forthcoming thresholds.

Segment Analysis

By Product Type: Dominance of refrigerators amid rapid air-fryer uptake

Refrigerators retained a 31.32% Saudi Arabia home appliances market share in 2024, thanks to indispensability and rising floor-area standards in new housing. Energy-rating upgrades and demand for larger French-door formats sustain value growth. Air fryers, posting a 6.90% forecast CAGR, epitomize health-conscious meal-prep trends and benefit from promotional pricing—Midea units retail between SAR 279 and SAR 439 after discounts. The Saudi Arabia home appliances market size for small-appliance categories advances fastest as consumers replace legacy cooking methods. Washing machines command a stable share, driven by cultural preferences for high-capacity front loaders with abaya cycles. Regulatory pushes toward eco-detergent compatibility and lower stand-by power spur premium launches such as TCL’s P680 washer-dryer with Wi-Fi diagnostics. Dishwashers, once niche, gain traction in newly built apartments where space-saving built-ins complement modern cabinetry.

Manufacturers differentiate via refrigerant transitions, vitality-cool zones, and AI freshness algorithms. Samsung’s R-410A line achieves higher SEER values than legacy R-22 systems, responding to SASO mandates and enabling premium price positioning. Meanwhile, fast-cycle innovation in kettles, blenders, and food processors captures casual cooks and expatriate professionals seeking time-saving gadgets.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Online gains reshape retail hierarchies

Multi-brand stores contributed 45.34% of the Saudi Arabian home appliances market size in 2024, leveraging nationwide footprints, live demos, and bundled after-sales service. These outlets use aggressive festival promotions, warranty extensions, and installation support to retain foot traffic even as digital options proliferate. Their physical presence also anchors click-and-collect functions for retailers’ mobile apps, giving shoppers same-day pickup and real-time inventory visibility. Extra, for instance, integrates loyalty rewards across its 47 outlets and online storefront to deepen customer retention while field technicians handle on-site set-up and maintenance. Exclusive brand boutiques remain important in high-income districts but face margin pressure from the broader assortments and frequent discounting available at multi-brand rivals.

Online channels forecast to grow at 7.24% CAGR, disrupt price discovery, and expand reach into tier-2 and tier-3 cities where brick-and-mortar coverage is thin. E-commerce penetration in washing machines is set to rise from 55.4% to 72.1% by 2029, signaling consumer confidence in transacting big-ticket goods over digital platforms. Platforms such as Tamkeen Stores offer 30-day returns, zero-interest installments, and nationwide delivery, narrowing service-quality gaps with physical stores. Jarir’s pivot from books to electronics shows how trusted brands can migrate customer loyalty into appliance categories, while brand-owned Saudi web shops push bundled accessories and extended warranties. Improved logistics hubs in Riyadh and Jeddah shorten delivery windows to under 48 hours, and last-mile partners provide optional installation, eroding traditional stores’ historic service advantage. As a result, future share shifts hinge on each retailer’s ability to synchronize inventory, pricing, and promotion strategies across both physical and digital channels.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Riyadh Province, holding 31.63% of the Saudi Arabian home appliances market share in 2024, benefits from Vision 2030 budgets, corporate relocation mandates, and higher disposable incomes. Diriyah alone adds 20,000 luxury units, and Wadi Safar financing injects USD 1.6 billion into premium villas that favor built-in cookers and smart refrigerators. JLL’s Q3 2024 retail audit shows Riyadh outperforming Jeddah across occupancy and rent metrics, strengthening retailer balance sheets. Oracle’s USD 1.5 billion cloud campus furnishes a digital infrastructure backbone supporting IoT-appliance data flows.

Makkah & Jeddah Province posts the highest growth at 6.57% CAGR, propelled by religious-tourism hospitality and Red Sea coastal resorts. Residential sales skyrocketed 53% in 2024 to 28,072 transactions, with apartment prices stable at SAR 4,215/m²—maintaining affordability for first-time apartment buyers[4]“Saudi Arabia’s housing supply likely to hit 3.9 M units by 2028,” argaam.com. ROSHN’s ALAROUS megaproject spans 4 million m², channeling concentrated appliance demand. Johnson Controls Arabia’s KAEC plant supplies 80% of domestic HVAC demand, illustrating how local manufacture feeds both residential and commercial markets.

The Eastern Province leverages petrochemical wealth and industrial clusters in Dammam and Jubail. Basic Electronics’ 70,000 m² HVAC smart factory employs 2,000 staff, amplifying demand for industrial refrigerators and staff housing appliances. Export corridors via the King Fahd Causeway enable re-export of finished goods to Bahrain and Kuwait, boosting factory utilization.

Madinah Province and the Rest of Saudi Arabia represent emerging opportunities as government initiatives develop secondary cities and rural areas, though growth depends on infrastructure investments and income development that may lag behind major urban centers.

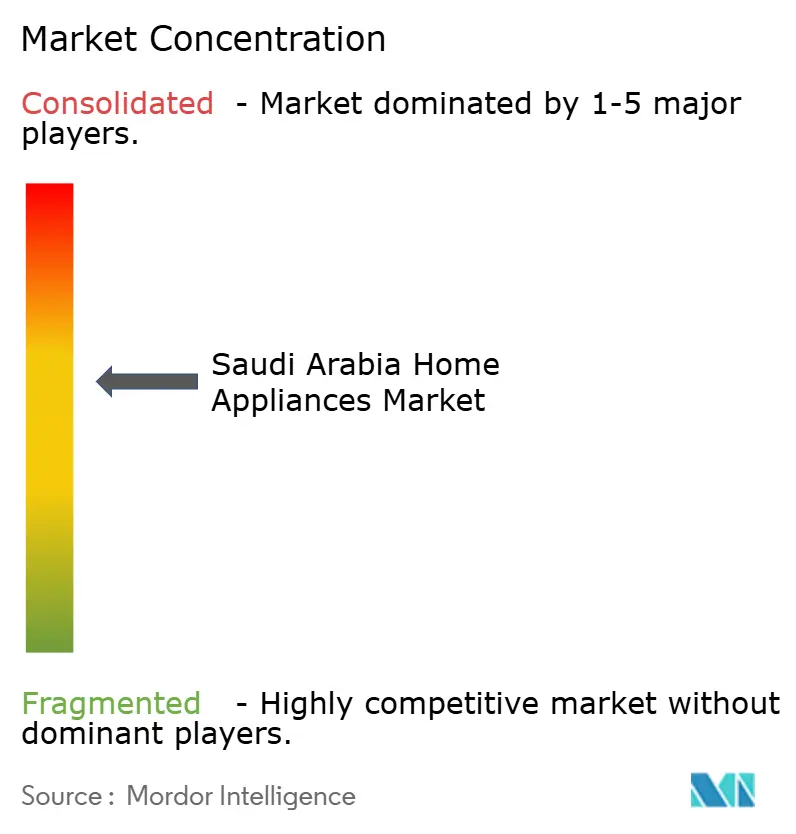

Competitive Landscape

Competition remains moderate—with the top five brands controlling roughly half of retail revenue—yet intensifying as localization mandates spur new entrants. LG, Samsung, Whirlpool, and Haier defend share via R&D in AI fault-diagnostics and adaptive cooling. LG and Shaker Group celebrated 30 years of collaboration, marking local production of MULTI V 5 HVAC systems that feed integrated home-comfort bundles. Chinese challengers—Hisense, TCL, Midea—capitalize on aggressive pricing and fast model rotations; Hisense claims over 70% domestic solar-compatible A/C share. Local firms such as Basic Electronics and Al Essa Industries scale assembly lines through joint ventures with Gree and Panasonic, using MODON incentives to secure land and utilities.

Product connectivity sets the next competitive frontier. BSH debuted the Matter-ready Bosch 100 Series French-door fridge, enabling cross-brand home-network integration and seamless voice control via Alexa. TCL’s FreshIN 3.0 air conditioners feature self-cleaning heat-exchangers and VOC-sensor algorithms to differentiate indoor air quality. Compliance with SASO energy tiers offers marketing clout; brands exceeding minimum SEER by 15% highlight lifetime operating-cost savings to justify premiums. Price wars loom in entry-level segments as supply-chain fluctuations trickle through, yet localization buffers foreign-exchange exposure and strengthens after-sales networks.

Service quality and financing flexibility are becoming critical factors influencing brand perception, driving strategic partnerships with leading retailers and fintech platforms. Panasonic’s collaboration with Al Essa Industries in 2025 is expected to enhance its nationwide service network while introducing zero-interest installment plans to attract mid-income consumers. This initiative aligns with the growing demand for affordable financing options in the market. Similarly, Johnson Controls Arabia has partnered with ROSHN to integrate VRF cooling systems into master-planned communities. This collaboration is anticipated to secure long-term replacement cycles and generate consistent aftermarket parts revenue. Such strategic moves highlight the increasing focus on value-added services and customer-centric solutions to strengthen market positioning.

Saudi Arabia Home Appliances Industry Leaders

-

Haier

-

LG Electronics

-

Samsung Electronics

-

Whirlpool Corporation

-

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: LG Electronics and Shaker Group celebrated 30 years of partnership, highlighting sustained collaboration in HVAC innovation and distribution across Saudi Arabia. The milestone underscores LG’s commitment to local manufacturing, including production of the MULTI V 5 air solution at the LG-Shaker factory. The partners plan to expand R&D programs around inverter technology to meet rising energy-efficiency targets.

- March 2025: Asheil Versatile Lighting Technologies secured 6,800 m² of land in Shaqraa Industrial City to build an advanced LED lighting facility. The project supports Vision 2030’s industrial localization drive and addresses Saudi demand projected to lift the LED lighting market from USD 2.3 billion to USD 4.8 billion by 2030. Construction is slated to begin in Q4 2025, with commercial operations expected within two years.

- February 2025: ROSHN and Johnson Controls Arabia signed a strategic agreement to introduce variable refrigerant flow cooling technology in Saudi communities. The partnership targets 90% local content by end-2024 and supports ROSHN’s plan to integrate energy-efficient HVAC systems across upcoming residential projects. Joint training initiatives will upskill Saudi technicians in VRF installation and maintenance.

- January 2025: BSH announced the launch of Matter-enabled home appliances at CES 2025, including the Bosch 100 Series French-door refrigerator with Amazon Alexa compatibility. The release positions BSH at the forefront of smart-home interoperability standards and allows consumers to manage multiple appliance brands through a single voice platform. Retail rollout in Saudi Arabia is scheduled for Q3 2025.

Saudi Arabia Home Appliances Market Report Scope

A home appliance is a device that helps users do household chores, including cooking, cleaning, and food preservation.

The Saudi Arabian home appliances market is segmented by major appliances (refrigerators, freezers, dishwashers, washing machines, ovens, and air conditioners), small appliances (coffee or tea makers, food processors, grills and roasters, and vacuum cleaners), and distribution channels (supermarkets and hypermarkets, specialty stores, and e-commerce). The report offers market size and forecasts for the Saudi Arabian home appliances market in USD for all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Countertop Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| Riyadh Province |

| Makkah & Jeddah Province |

| Eastern Province |

| Madinah Province |

| Rest of Saudi Arabia |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | Riyadh Province | |

| Makkah & Jeddah Province | ||

| Eastern Province | ||

| Madinah Province | ||

| Rest of Saudi Arabia | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Saudi Arabia home appliances market in 2025?

The market is valued at USD 3.51 billion in 2025 and is projected to reach USD 4.76 billion by 2030 at a 6.26% CAGR.

Which product category leads sales?

Refrigerators hold the top spot with 31.32% share of 2024 revenue, supported by housing expansion and premium-feature upgrades.

What is the fastest-growing product?

Air fryers show the highest growth, advancing at a 6.90% CAGR through 2030 as health-focused cooking gains popularity.

Which region will expand quickest?

Makkah & Jeddah Province is forecast to grow at a 6.57% CAGR, benefiting from tourism infrastructure and Red Sea Project developments.

How are energy regulations affecting demand?

Tightened SASO standards accelerate replacement of older units with inverter-grade, A-rated models, boosting premium appliance sales.

What role does e-commerce play?

Online channels are projected to grow at a 7.24% CAGR, pushing washing machine online penetration to 72.1% by 2029 and reshaping retail strategies.

Page last updated on: