Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

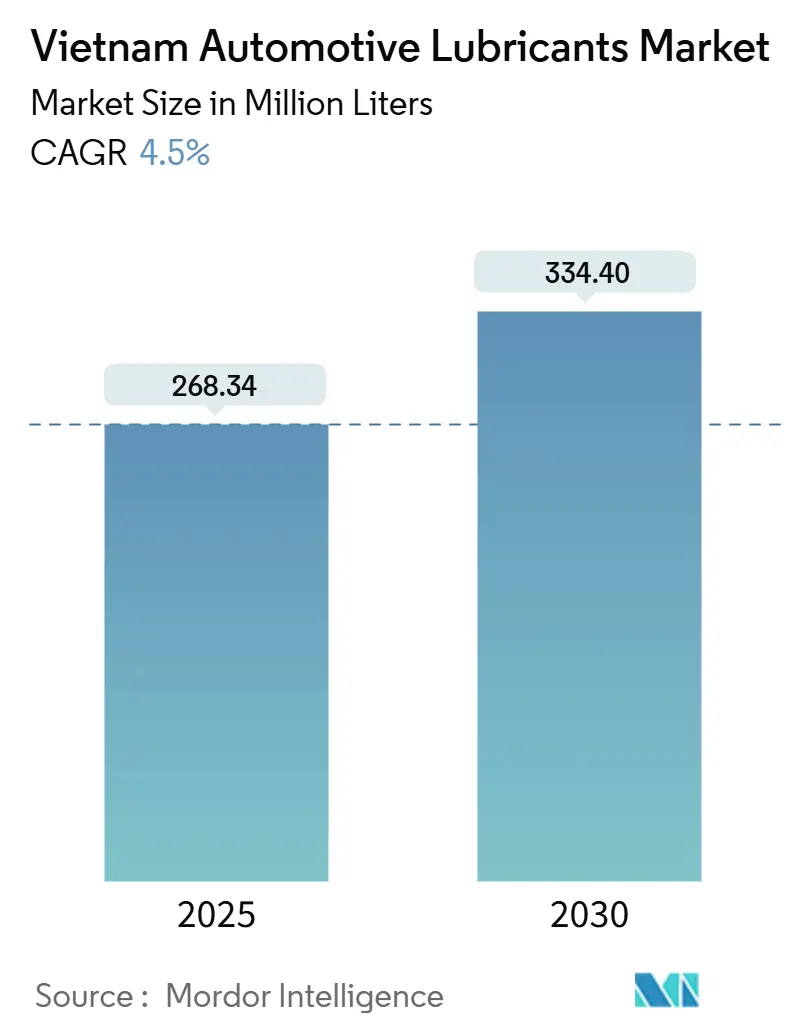

| Market Volume (2025) | 268.34 Million liters |

| Market Volume (2030) | 334.40 Million liters |

| Growth Rate (2025 - 2030) | 4.50% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Automotive Lubricants Market Analysis by Mordor Intelligence

The Vietnam Automotive Lubricants Market size is estimated at 268.34 million liters in 2025, and is expected to reach 334.40 million liters by 2030, at a CAGR of 4.5% during the forecast period (2025-2030). Robust freight activity, an aging vehicle parc, and expanding e-commerce fleets underpin this growth, even as electrification policies begin to reshape long-term demand. Distribution dominance by Petrolimex, combined with localized blending investments from Shell, BP/Castrol, and Motul, sustains supply resiliency while intensifying competitive differentiation. The rapid adoption of premium synthetics, longer drain intervals mandated by OEMs, and stricter crackdowns on counterfeit products are increasing average selling prices and encouraging margin expansion. At the same time, Hanoi’s impending ban on fossil-fuel motorcycles inside Ring Road 1 and Ho Chi Minh City’s Low Emission Zone signal regulatory pressure on legacy two-wheeler demand.

Key Report Takeaways

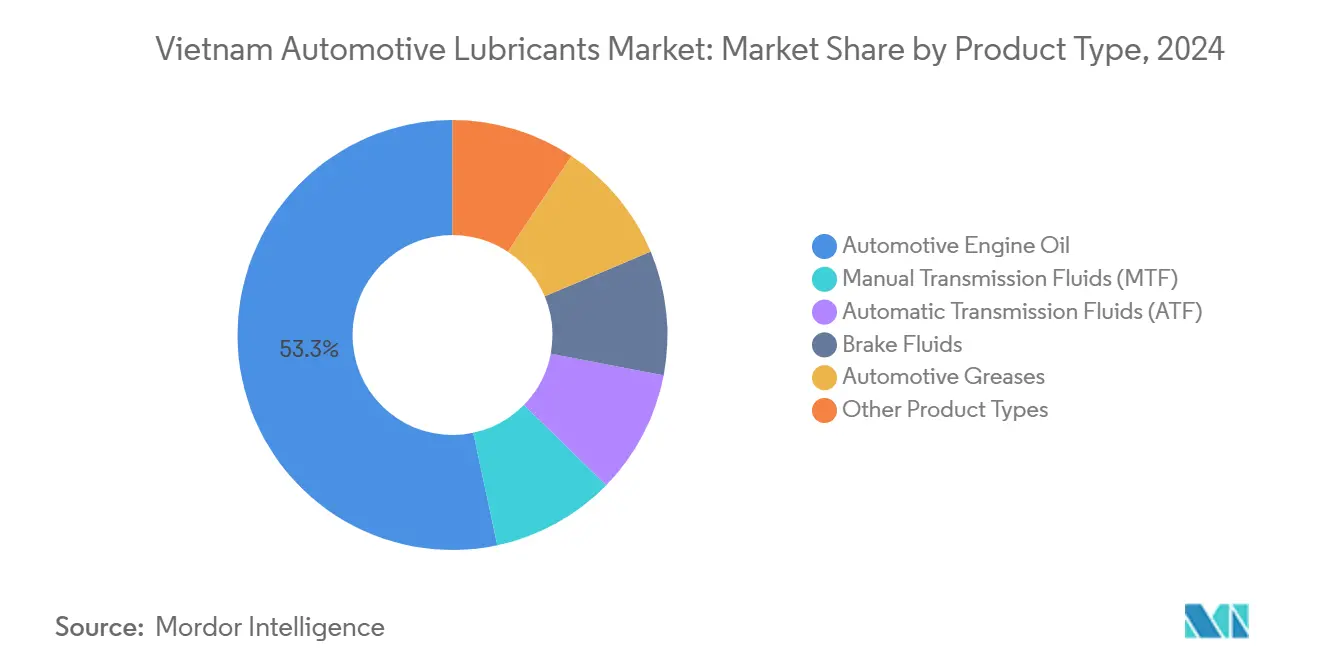

- By product type, automotive engine oil captured 53.34% of the Vietnam automotive lubricants market share in 2024, while automatic transmission fluids are projected to advance at a 4.68% CAGR through 2030.

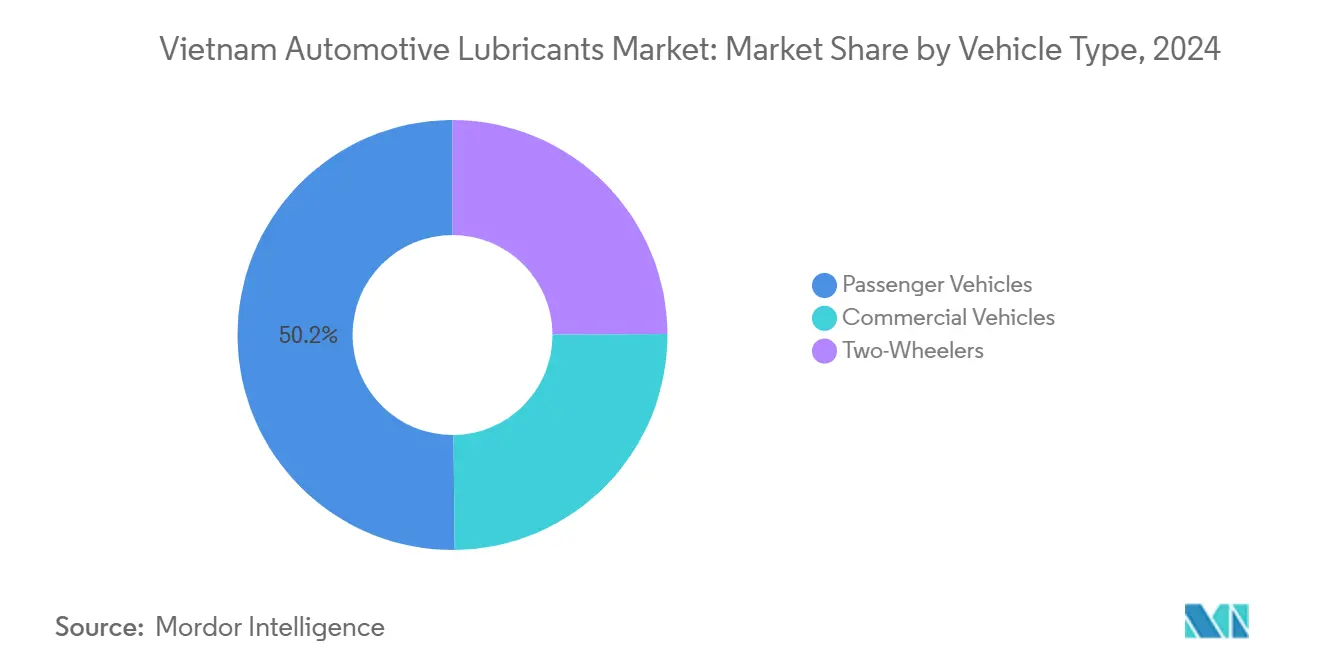

- By vehicle type, passenger vehicles accounted for 50.17% of the Vietnam automotive lubricants market size in 2024; commercial vehicles are projected to grow at a 4.89% CAGR through 2030.

Vietnam Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle parc and average age | +1.8% | National, concentrated in urban centers | Medium term (2-4 years) |

| Two-wheeler dominance in urban mobility | +1.2% | Urban areas, particularly HCMC and Hanoi | Short term (≤ 2 years) |

| Surge in e-commerce logistics fleets | +0.8% | Major cities and industrial zones | Medium term (2-4 years) |

| OEM extended-drain interval specifications | +0.4% | National, OEM service networks | Long term (≥ 4 years) |

| Rapid growth of ride-hailing motorbike rentals | +0.3% | Urban centers, expanding to secondary cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Parc and Average Age Drive Sustained Lubricant Demand

National vehicle registrations continue to rise. A growing proportion of models are seven years or older, requiring more frequent oil replacements due to degradation and blow-by. Trucking remains fragmented; the majority of commercial vehicles are under 5 tons and average just five trucks per firm, which magnifies service incidents[1]World Bank, “Strengthening Vietnam’s Trucking Sector,” worldbank.org . These factors collectively sustain the Vietnam automotive lubricants market on an upward volume trajectory, despite the headwinds from the electrification trend.

Two-Wheeler Market Dynamics Shape Urban Lubricant Consumption

Although Vietnam became the world’s second-largest electric two-wheeler market in 2025, Honda still projects selling 2.2 million ICE motorcycles that year. Routine oil services conducted at ubiquitous roadside washes yield high-frequency lubricant turnover. Legislated bans, such as Hanoi’s 2026 exclusion of fossil-fuel motorcycles inside Ring Road 1, begin to narrow urban demand yet leave a vast in-use fleet elsewhere, allowing the Vietnam automotive lubricants market to retain two-wheeler volume support into 2030.

E-Commerce Logistics Fleet Expansion Drives Commercial Lubricant Growth

Vietnam’s e-commerce parcel volume climbed at double-digit rates in 2024, pressuring logistics operators to expand light-truck and van fleets. Stop-start urban routing exacerbates thermal stress, leading to an increased frequency of oil and driveline fluid changes. Bulk purchase contracts signed by digital freight aggregators add scale opportunities for premium synthetics within the Vietnam automotive lubricants market.

OEM Extended-Drain Interval Specifications Reshape Product Mix

API SP and JASO GLV-2 oils enabling 10,000–15,000 km drains are now standard for new passenger models. Consumers gravitate toward synthetic SKUs that reduce annual service visits, pushing average selling prices higher. Lubricant blenders must upgrade additive packages and anti-oxidation chemistries, raising formulation costs but unlocking margin expansion across the Vietnam automotive lubricants market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EV adoption in passenger-car segment | -1.1% | Urban centers, expanding nationally | Medium term (2-4 years) |

| Price-sensitive consumer base favouring low-grade mineral oils | -0.7% | National, particularly rural areas | Short term (≤ 2 years) |

| Growing counterfeit lubricant trade | -0.4% | National, concentrated in e-commerce channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electric Vehicle Adoption Accelerates ICE Displacement

VinFast shipped 97,399 battery EVs in 2024 and targets 150,700 units in 2025. Because BEVs eliminate engine oil usage and reduce transmission-fluid needs, the Vietnam automotive lubricants market faces structural demand erosion, especially in urban car fleets. Yet thermal-management coolants and specialized e-greases open new high-value niches.

Growing Counterfeit Lubricant Trade Undermines Market Integrity

Police dismantled a Ho Chi Minh City ring in 2025 that produced counterfeit oil cans, masquerading as those of Castrol, Motul, Honda, and Yamaha. Counterfeits cause engine damage and erode consumer trust, prompting genuine brands to invest in QR traceability and tamper-proof caps, which incrementally raise compliance costs in the Vietnamese automotive lubricants market.

Segment Analysis

By Product Type: Engine-Oil Dominance With Transmission-Fluid Momentum

Automotive engine oil accounted for 53.34% of the Vietnam automotive lubricants market share in 2024. Embedded usage across cars, motorcycles, and trucks ensures volume leadership. However, automatic transmission fluid (ATF) displays the steepest growth trajectory at a 4.68% CAGR, benefiting from rising passenger-car automatic transmission penetration and intensified parts-warranty compliance. Manual transmission fluid still holds a share in light-duty trucks, whereas brake fluids maintain steady mid-single-digit contributions.

Persistent counterfeit activity forces branded suppliers to embed overt and covert security markers on premium SKUs, adding costs but preserving brand equity. Blenders also incorporate Group III base oils and high-performance additive chemistries to comply with API SP and Euro 6 requirements. Motul’s Vietnamese plant has begun commercial trials of Re-Refined Base Oil blends, promising a reduction in carbon footprint compared to virgin Group II stocks[2]Motul Asia Pacific, “Sustainability Report 2024,” motul.com. These innovations reinforce competitive positioning and align with evolving OEM partnerships inside the Vietnam automotive lubricants industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: Commercial Vehicle Growth Outpaces Passenger Segment

Passenger cars accounted for 50.17% of total lubricant volumes in 2024. Nevertheless, the commercial-vehicle sub-sector is set to expand at the fastest rate, with a 4.89% CAGR to 2030, as e-commerce logistics and infrastructure development boost diesel fleet utilization. High idle times, stop-start routes, and heavier loads accelerate oil oxidation, which is why premium long-drain synthetics with higher TBN retention are recommended.

Two-wheelers will gradually surrender share to electrics in major cities but hold a sizable rural maintenance base. Ride-hailing fleets such as GrabBike and BeBike average oil changes every 1,500 km, fostering continuous aftermarket turnover. Meanwhile, tighter Euro 5 diesel import standards from 2027 are encouraging trucking firms to adopt low-sulfur engine oils, nudging formulators toward advanced detergent-dispersant packages within the Vietnamese automotive lubricants market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Ho Chi Minh City contributed the largest regional demand in 2025, driven by dense logistics operations. Hanoi followed, though its incoming Inner-City Motorcycle Ban may shave volumes from 2026 onward. The Southeast Economic Corridor, including Dong Nai and Binh Duong, registers the fastest growth due to export-oriented manufacturing clusters that require intense trucking activity. Northern provinces such as Hai Phong leverage deep-sea port expansion to boost commercial-vehicle lubricant demand.

Petrolimex’s 5,500+ retail stations provide it with geographic breadth, while joint-venture blending plants near Hai Phong and Nha Be drive logistical efficiencies for international entrants. Motul exports its output from the Dong Nai complex to ASEAN neighbors, highlighting Vietnam’s role as a regional hub for synthetic lubricant supply. Coastal highway upgrades funded under the 2021–2030 Public–Private Partnership scheme are projected to increase long-haul trucking kilometers, reducing diesel engine oil consumption along National Route 1A. Rural Mekong Delta provinces remain more price-sensitive, sustaining demand for SAE 40 monogrades blended from domestic base oils. Overall, the Vietnam automotive lubricants market maintains diverse regional profiles shaped by urban policy, industrial localization, and strategic road corridors.

Competitive Landscape

Vietnam’s automotive lubricants market is moderately consolidated. International majors command the premium synthetic tier through OEM alliances and differentiated additive technologies. Castrol’s Magnatec and GTX Ultra range enjoys top-of-mind urban brand recognition, supported by more than 1,000 branded workshops nationwide. Competitive intensity also plays out in sponsorships; TotalEnergies renewed its deal with VinFast’s electric racing program in 2025, signaling a pivot toward EV coolants and e-greases. Meanwhile, domestic challenger introduced RRBO-based economy engine oils positioned 12% below imported synthetics, stimulating price competition without compromising on API SN compliance. Overall, brand equity, channel reach, and sustainable product portfolios significantly influence positioning in the Vietnamese automotive lubricants market.

Vietnam Automotive Lubricants Industry Leaders

-

BP p.l.c.

-

Shell Plc

-

Petrolimex (PLX)

-

TotalEnergies

-

AP SAIGON PETRO

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: TotalEnergies subsidiary Lubrilog launched the PFAS-free Plastogrease range for automotive actuators, anticipating regulator restrictions on per- and polyfluoroalkyl substances.

- June 2025: BP p.l.c. initiated a process to divest its Castrol lubricants arm, valued at up to USD 10 billion, as part of a wider USD 20 billion disposal program scheduled before 2027.

Vietnam Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the size of the Vietnam automotive lubricants market in 2025?

The market reached 268.34 million liters in 2025, with a forecasted growth rate of 4.50% CAGR to 334.40 million liters by 2030.

Which product category currently dominates sales?

Engine oil accounts for 53.34% of the total 2024 volume, making it the largest segment.

What is the fastest-growing vehicle segment for lubricants?

Commercial vehicles are projected to expand at a 4.89% CAGR between 2025 and 2030 due to e-commerce logistics growth.

How will electric vehicles impact lubricant demand?

BEVs remove engine oil consumption, creating a structural headwind, but open niches for thermal-management fluids and e-axle greases.

What measures combat counterfeit lubricants?

Brands are deploying QR code traceability, tamper-proof caps, and police collaborations to reduce the circulation of counterfeit oil.

Page last updated on: