Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

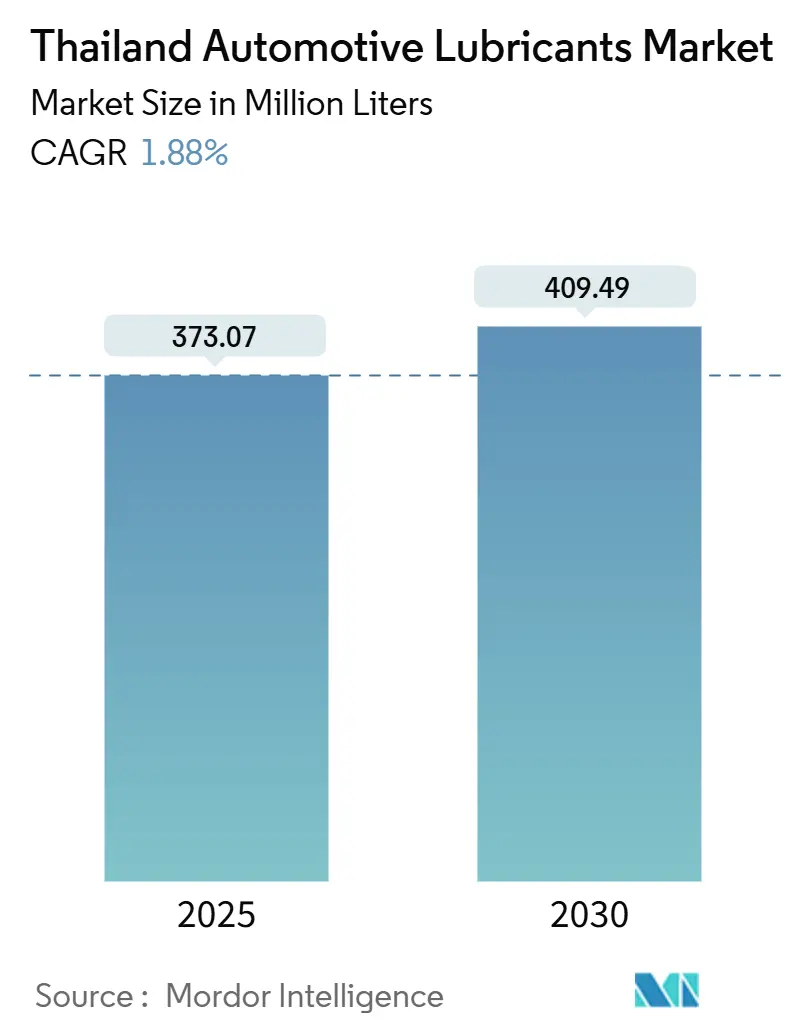

| Market Volume (2025) | 373.07 Million liters |

| Market Volume (2030) | 409.49 Million liters |

| Growth Rate (2025 - 2030) | 1.88% CAGR |

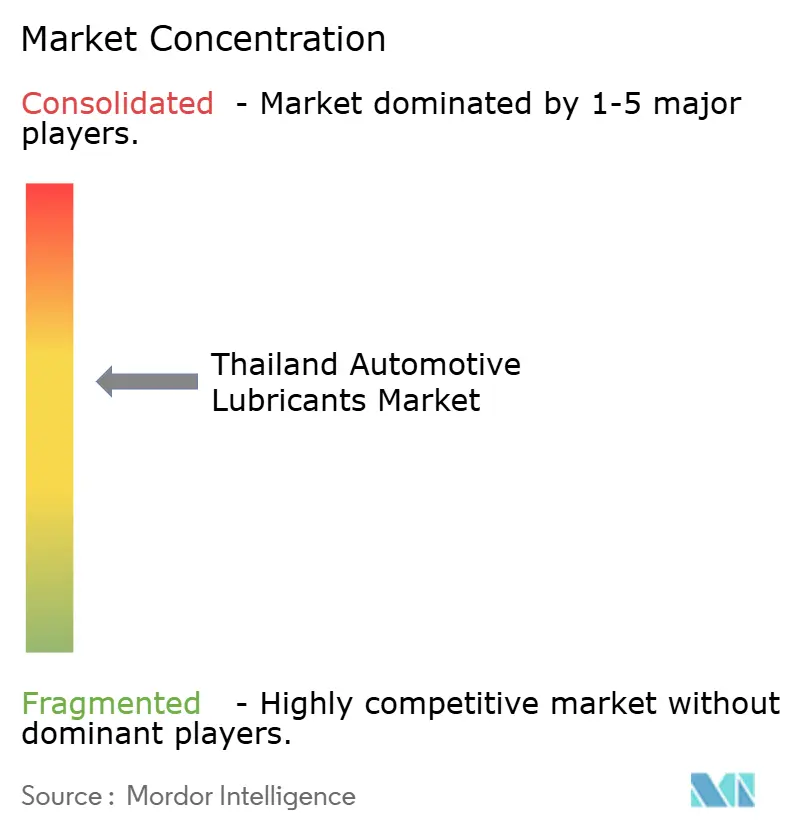

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Automotive Lubricants Market Analysis by Mordor Intelligence

The Thailand Automotive Lubricants Market size is estimated at 373.07 million liters in 2025, and is expected to reach 409.49 million liters by 2030, at a CAGR of 1.88% during the forecast period (2025-2030). Healthy demand stems from Thailand’s role as Southeast Asia’s leading vehicle production center, the government’s 30@30 zero-emission vehicle target, and the continued dominance of two-wheelers, which together keep lubricant consumption resilient despite pressures from electrification. Switching to synthetic low-viscosity oils, logistics fleet expansion, and rigorous enforcement against counterfeit products are pivotal forces shaping competition. Major suppliers differentiate through OEM-approved formulations, solar-powered manufacturing, and extended-drain technologies that lower the total cost of ownership for fleets. Margin management remains critical as base-oil price swings and foreign-exchange shifts add raw-material risk, prompting smaller blenders to adopt consolidation or partnership strategies to secure scale.

Key Report Takeaways

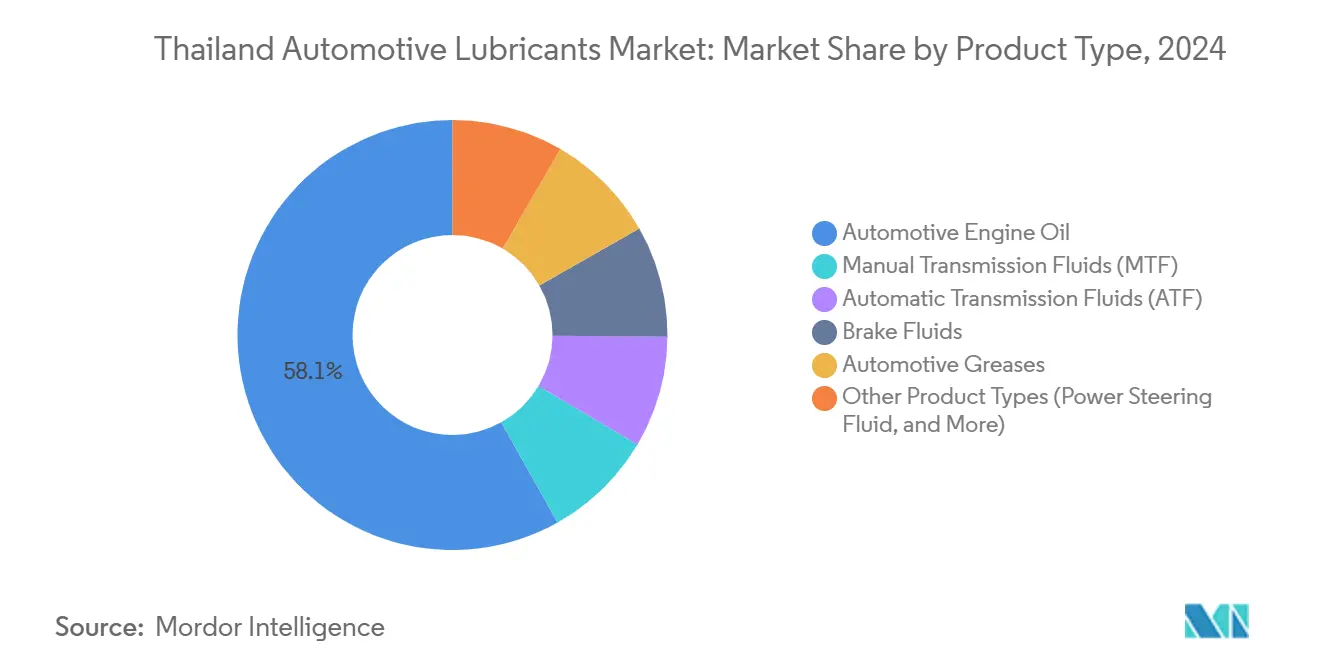

- By product type, automotive engine oil accounted for 58.12% of the market share in 2024; however, the demand for automatic transmission fluids (ATF) is expected to rise at the fastest CAGR of 2.12% during the forecast period (2025-2030).

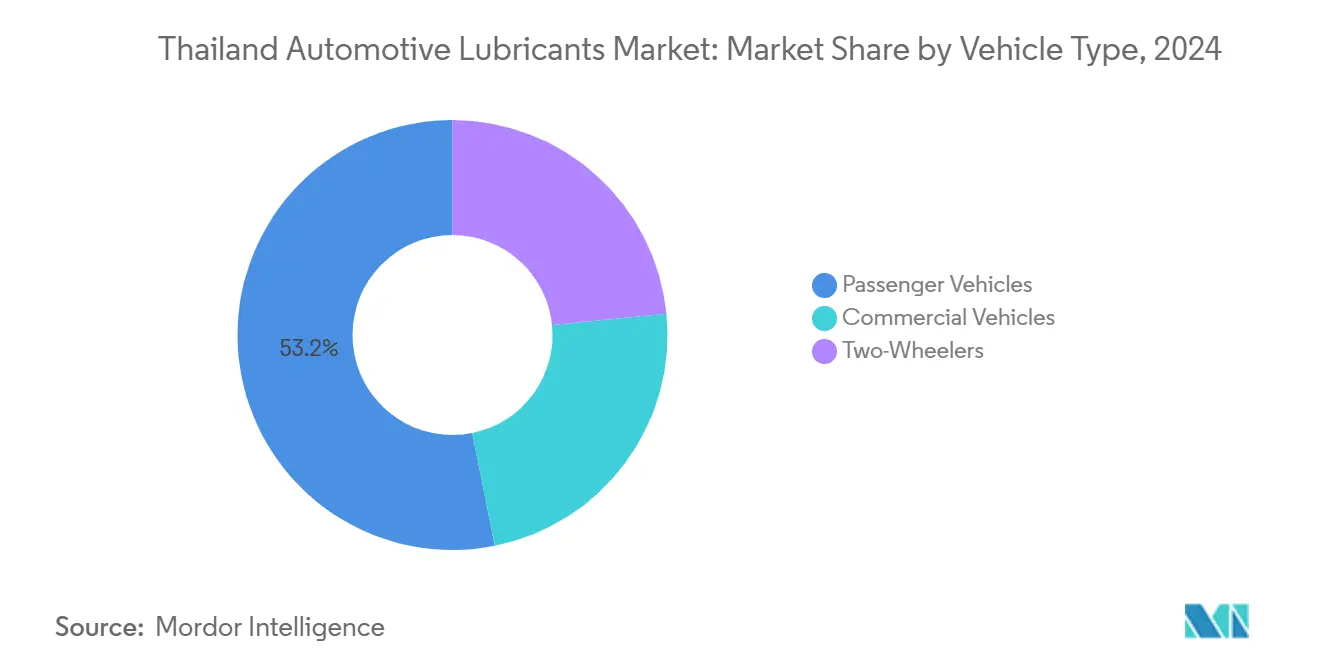

- By vehicle type, passenger vehicles held the largest share of the market at 53.15% in 2024. However, the lubricant demand for commercial vehicles is expected to grow at a CAGR of 2.25% during the forecast period (2025-2030).

Thailand Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding commercial-vehicle fleet and infrastructure spend | +0.4% | National, with concentration in Bangkok, Eastern Economic Corridor | Medium term (2-4 years) |

| Rising shift toward synthetic, low-viscosity engine oils | +0.3% | National, with premium adoption in urban centers | Long term (≥ 4 years) |

| Growing motorcycle population and ride-hailing mileage | +0.5% | National, with highest intensity in Bangkok, Chiang Mai, Phuket | Short term (≤ 2 years) |

| OEM extended-drain service packages boosting high-margin oil uptake | +0.2% | National, focused on authorized dealer networks | Medium term (2-4 years) |

| Thailand's export-hub strategy for blending and re-export of lubes | +0.3% | Regional, serving ASEAN, India, and broader Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Commercial-Vehicle Fleet and Infrastructure Spend

Commercial freight tonnage continues to rise as rail-road projects and warehouse construction progress inside the Eastern Economic Corridor. Fleet operators demand longer-life, fuel-saving lubricants to reduce downtime, leading to bulk-order contracts that lock in product specifications across mixed truck brands[1]PTT Lubricants, “Corporate Presentation 2025,” pttlubricants.com. Suppliers offering digital oil analytics garner a competitive advantage because predictive maintenance shortens workshop visits, a clear benefit for high-utilization route trucks. PTT Lubricants recorded a capacity utilization of over 260 million liters in 2025, driven by procurement from hauling companies linked to e-commerce networks. Foreign majors leverage Thailand’s free-trade access to backhaul packaged products across mainland ASEAN, creating incremental export volume while stabilizing domestic plant throughput. The trend is projected to preserve a positive lubricant demand baseline even as passenger-vehicle oil volumes plateau.

Rising Shift Toward Synthetic, Low-Viscosity Engine Oils

Tighter Euro 5 equivalent standards and rising pump prices are driving a consumer shift toward SAE 0W-20 and 5W-30 multigrade synthetics, which deliver measurable fuel savings. ExxonMobil targets a 10% annual sales growth in Thailand for Mobil 1, highlighting 15,000 km drain intervals and the benefits of improved engine cleanliness. Shell’s solar-powered grease plant exemplifies brand repositioning around sustainability credentials, reinforcing premium price points through environmental messaging. Authorized dealers bundle genuine oil into prepaid maintenance packages to capture aftermarket margins while assuring OEM warranty compliance. Although synthetics command higher shelf prices, the total cost of ownership favors the switch because fewer services offset the upfront expense. This dynamic gradually dilutes the mineral-oil volume share yet raises revenue per liter, supporting value growth within the Thai automotive lubricants market.

Growing Motorcycle Population and Ride-Hailing Mileage

Thailand registered 22.94 million motorcycles in 2024, with sub-125 cc commuters accounting for more than four-fifths of the output, thereby anchoring consistent demand for four-stroke engine oils. Delivery-app riders clock twice the monthly distance of private users, requiring more frequent oil changes that boost workshop traffic and retail sales. Automatic scooter output expanded 8.3% year-over-year, accelerating demand for scooter-specific transmission fluids optimized for continuously variable gearboxes. Lubricant brands with a deep penetration into convenience stores and independent garages remain best positioned, as these channels dominate refill purchases. Value-added packs, such as 1 liter plus a free spark-plug, drive loyalty among cost-conscious riders and reinforce volume resilience despite broader electrification narratives.

OEM Extended-Drain Service Packages

Global automakers competing for showroom share in Thailand promote service intervals of 15,000 to 20,000 km as a lifestyle convenience differentiator. PETRONAS co-developed premium formulations with Mercedes-Benz to meet the standards for turbocharged engine cleanliness, routing those fluids exclusively through branded workshops. Shell’s multi-year BMW contract secures factory fill and aftersales supply across dealerships, locking rivals out of high-margin segments[2]Shell, “BMW Global Supply Agreement Extension,” shell.com. Extended drains shift lubricant selection authority toward OEMs and away from drivers, rewarding suppliers with formal approvals and penalizing unlicensed blends that cannot document durability claims. While drain-interval lengthening slightly curbs liter demand, elevated per-unit prices compensate and reinforce premiumization within the Thailand automotive lubricants market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Base-oil price volatility and Foreign Exchange risk | -0.3% | National, with higher impact on import-dependent blenders | Short term (≤ 2 years) |

| Counterfeit / low-quality domestic brands eroding margins | -0.2% | National, with concentration in rural and price-sensitive segments | Medium term (2-4 years) |

| EV-subsidy programmes reducing long-term ICE-oil demand | -0.4% | National, with accelerated impact in urban centers and fleet segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Base-Oil Price Volatility and Foreign-Exchange Risk

Imported Group III base oils saw spot premiums widen in early 2025 after upstream refinery outages, squeezing gross margins for small blenders that lack term contracts. A stronger baht lowers import costs, yet currency whiplash complicates selling-price resets, especially in fragmented retail channels that resist frequent list-price changes. Integrated refiners counter swings by swapping cargos internally, whereas non-refining players hedge through futures or pass-through clauses in fleet contracts. Persistent volatility accelerates mergers as scale becomes vital for negotiating supply and absorbing inventory losses, thereby tilting competitive leverage toward major companies.

EV-Subsidy Programs Reducing Long-Term ICE-Oil Demand

Government incentives covering up to THB 10,000 per battery-electric car, along with local content mandates, support a rising share of zero-tailpipe-emission vehicles; penetration reached 19% by May 2025. Pure EVs eliminate the need for crankcase oil, placing a ceiling on future engine oil volume. Hybrid powertrains mitigate the impact by retaining smaller sump capacities; however, the direct electrification of taxi and delivery van fleets cannibalizes diesel oil demand. Lubricant makers respond by funding R&D for EV-thermal-management fluids and reduction-gear greases, aiming to offset declining ICE oil revenue streams after 2030 in the Thai automotive lubricants market.

Segment Analysis

By Product Type: Engine-Oil Leadership Sustains, ATF Outpaces

Automotive Engine Oil contributed 58.12% of 2024 volume, underscoring its foundational role inside the Thailand automotive lubricants market size for core maintenance cycles. Motorcycle commuter fleets, passenger cars, and light pickups use multigrade mineral and semi-synthetic blends that accommodate tropical driving temperatures. The Thailand automotive lubricants market share for engine oil is expected to decline slightly as other fluids grow faster, yet absolute volumes remain substantial because the average vehicle age hovers near 11 years, and older models retain short drain intervals. Suppliers refresh portfolios with SP-grade formulations, zinc-phosphorus additives for cam-wear defense, and detergent packages designed for biodiesel blends prevalent in the Thai diesel pool.

Automatic Transmission Fluids posted a leading 2.12% CAGR outlook to 2030 as consumers embrace automatic gearboxes in city traffic. The automatic-scooter boom and rising CVT bikes extend ATF demand beyond passenger cars. Global OEMs jointly engineer proprietary friction modifiers to mitigate shudder and thermal breakdown, prompting Thai assemblers to specify factory-fill series that must be matched at service intervals. Local blenders pursue licensing deals to replicate additive chemistry under OEM code to retain dealership shelf access. Manual Transmission and Brake Fluids keep steady, while specialty steering fluids occupy a niche driven by premium models adding electric-hydraulic assist.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: Passenger Car Dominance, Commercial Fleet Momentum

Passenger Vehicles captured 53.15% of 2024 demand, mirroring Thailand’s mature car parc and active used-car trade that drives steady oil changes through independent service outlets. The segment’s Thailand automotive lubricants market size has gradually shifted from mineral 15W-40 toward 0W-20 synthetic, widening unit margins even as liters decline per service. Dealer-backed extended-drain packages and warranty-tied lubricants foster brand loyalty in newer cars, while older vehicles remain price-sensitive, providing independent garages with room to promote private-label blends. Two-wheelers remain volume stalwarts; however, high-mileage ride-hailing bikes intensify per-unit consumption, with several courier fleets adopting branded high-temperature formulations to mitigate the thermal stress caused by frequent stop-starts.

Commercial Vehicles are set to expand at a 2.25% CAGR through 2030, the fastest rate among vehicle classes. Freight modernization and the development of East-West economic corridors require longer-haul trucks to run higher average daily kilometers, compelling fleet owners to prioritize extended drain and fuel-efficient oils. The Thailand automotive lubricants market share of commercial vehicles therefore rises gradually, supported by engine-oil viscosity migration to CK-4 10W-30 that balances fuel savings with wear control. Bus operators in Bangkok’s clean-air program embrace low-ash formulations compatible with particulate filters, another area where suppliers with API FA-4 approvals can differentiate. This vehicle-mix transition underscores momentum toward performance-centric lubricants destined for heavy-duty cycles.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Bangkok’s metropolitan cluster accounts for more than one-third of the national lubricant turnover, driven by dense passenger-car ownership, an 8-million-strong motorcycle parc, and a hub-and-spoke freight network that feeds ecommerce warehouses. Dealers in the capital actively upsell synthetics, reflecting higher disposable income and traffic congestion that favors automatic gearboxes, which in turn lifts ATF volume. The adjacent Eastern Economic Corridor hosts engine and transmission plants that consume significant quantities of factory fill and process oils, linking domestic demand to export vehicle volumes. Central Plains provinces supply agricultural machinery that relies on diesel engine oils and hydraulic fluids, ensuring a rural baseline consumption across harvest cycles.

Northern tourist centers, such as Chiang Mai, generate significant turnover through rental scooters and ride-sharing fleets that rack up high mileage. Seasonal haze episodes encourage consumers to adhere to manufacturer drain intervals, bolstering workshop activity. Southern coastal zones, including Phuket, present similar two-wheeler intensity and marine-engine lubricant niches, enabling suppliers to diversify with corrosion-resistant multi-purpose greases. Cross-border trade lines funnel packaged oils into Laos, Myanmar, and Cambodia, making Thai distribution depots pivotal staging points for hinterland markets.

Export orientation further shapes geographic production patterns; Shell’s grease facility in Rayong ships to more than 40 Asia-Pacific destinations, while Thai Oil’s TOPNEXT International channels base oil cargoes to Vietnam and India, integrating Thailand into regional supply chains. Nationwide, the Thai Industrial Standards Institute enforces product quality through the AI-powered TISI Watch tool that flagged nearly 100,000 suspect online listings within five months, leveling the playing field in rural provinces previously vulnerable to counterfeit sales. As digital monitoring extends, legitimate brands gain from homogenous compliance standards across all customer catchments in the Thailand automotive lubricants market.

Competitive Landscape

The Thailand Automotive Lubricants Market is moderately consolidated. Shell, ExxonMobil, and PETRONAS contest premium segments by linking lubricant technology to global OEM endorsements, embedding their products within warranty terms for BMW, Mercedes-Benz, and Honda. These alliances secure captive demand streams and raise entry barriers for challenger brands. Counterfeit suppression through TISI Watch tilts the battlefield in favor of brands that can verify authenticity using QR-code bottle seals, thereby narrowing gray-market leakage. Overall, competitive intensity is shifting toward technology, compliance, and multi-channel distribution models, collectively shaping the Thai automotive lubricants market.

Thailand Automotive Lubricants Industry Leaders

-

ExxonMobil Corporation

-

PTT Lubricants

-

Shell plc

-

BP p.l.c.

-

Chevron Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: At the 2025 MotoGP in Thailand, Shell Lubricants unveiled their upgraded full-synthetic lubricant, Shell Advance Ultra with API SP, a premium choice for motorcycle and scooter riders globally.

- July 2024: Shell announced a strategic investment to enhance the production capacity and efficiency of its grease manufacturing plant in Thailand. With a threefold increase in production capacity – from 5,000 tons to 15,000 tons annually – the plant is poised to meet over half of Thailand's domestic demand and cater to markets in more than 40 countries across the Asia-Pacific region.

Thailand Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Thailand automotive lubricants market?

The market recorded 373.07 million liters in 2025 and is projected to reach 409.49 million liters by 2030.

How fast is the market expected to grow?

Volume is forecast to expand at a 1.88% CAGR between 2025 and 2030, supported by fleet expansion and synthetic-oil adoption.

Which product type dominates consumption?

Engine Oil leads with 58.12% share of 2024 sales, driven by Thailand’s large motorcycle and passenger-car parc.

Why are automatic transmission fluids growing faster?

Rising adoption of automatic gearboxes in cars and scooters pushes ATF demand at a forecast 2.12% CAGR through 2030.

How will EV adoption affect lubricant demand?

Electric vehicles cut engine-oil volumes long term, yet new opportunities emerge for EV-specific thermal-management fluids.

Page last updated on: