Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

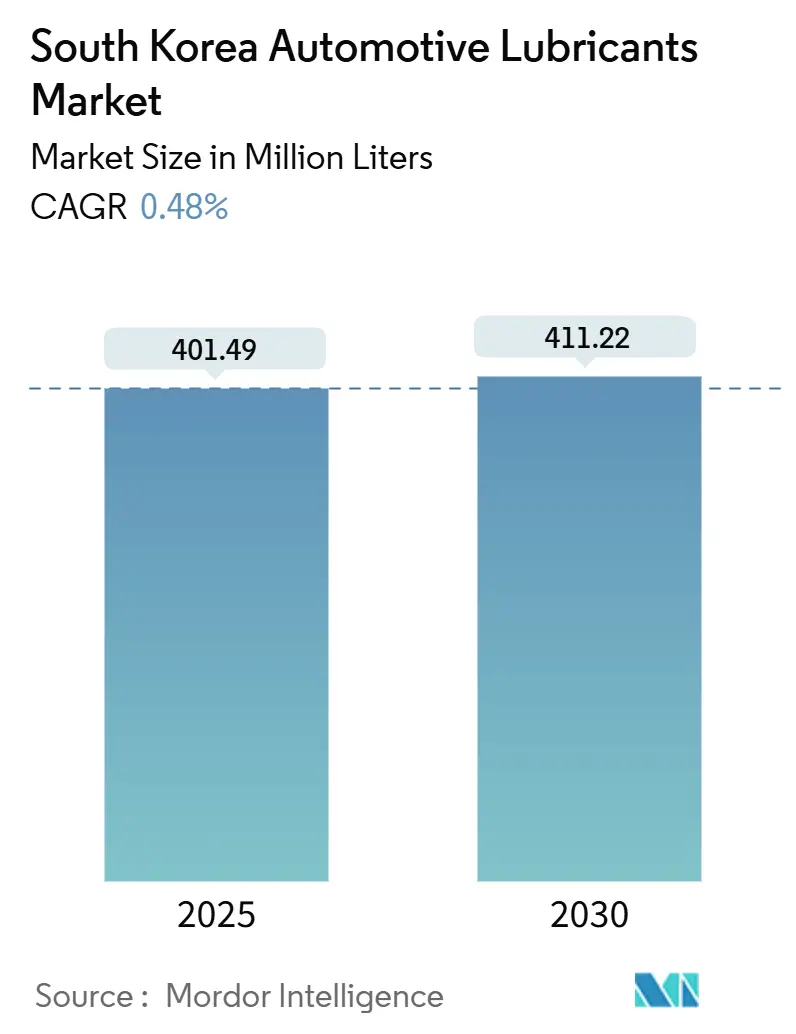

| Market Volume (2025) | 401.49 Million Liters |

| Market Volume (2030) | 411.22 Million Liters |

| Growth Rate (2025 - 2030) | 0.48% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Automotive Lubricants Market Analysis by Mordor Intelligence

The South Korea Automotive Lubricants Market size is estimated at 401.49 Million Liters in 2025, and is expected to reach 411.22 Million Liters by 2030, at a CAGR of 0.48% during the forecast period (2025-2030). Stable volumes mirror a mature light-vehicle parc, but tightening fuel-economy rules and the 2025 introduction of API SQ and ILSAC GF-7 standards nudge users toward higher-value synthetics. Engine oil retains dominance on the strength of a 25 million-unit fleet and regimented service schedules, yet automatic transmission fluid (ATF) is the fastest-advancing product as eight-speed and hybrid gearboxes proliferate. Commercial fleets tied to e-commerce create incremental demand through high-mileage operating patterns, while motorsports culture magnifies premium-grade pull in urban centers. Competitive intensity stays moderate: global majors contest share with vertically integrated refiners such as SK Enmove, HD Hyundai Oilbank, GS Caltex, and S-Oil, each leveraging domestic base-oil capacity and nationwide service channels.

Key Report Takeaways

- By product type, automotive engine oil commanded 62.12% of the South Korea automotive lubricants market share in 2024. Automatic transmission fluid is projected to expand at a 0.51% CAGR through 2030.

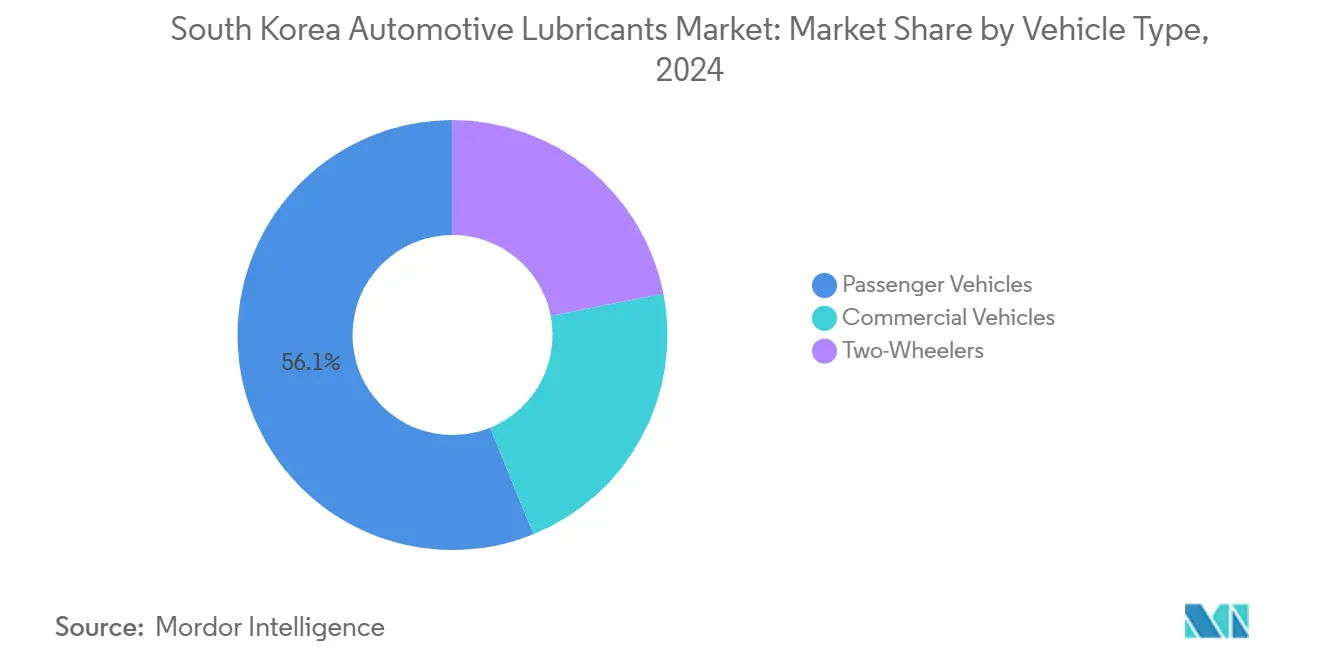

- By vehicle type, passenger vehicles held 56.14% share of the South Korea automotive lubricants market size in 2024. Commercial vehicles are advancing at a 0.62% CAGR through 2030.

South Korea Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing average vehicle age and mileage | +0.10% | National, Seoul-Incheon focus | Medium term (2-4 years) |

| Shift toward low-viscosity synthetic formulations | +0.05% | National, premium uptake in metro areas | Long term (≥ 4 years) |

| E-commerce-driven light-duty truck utilization surge | +0.03% | National, logistics hubs | Short term (≤ 2 years) |

| OEM warranty-linked lubricant specification compliance | +0.02% | National, Hyundai-Kia networks | Medium term (2-4 years) |

| Motorsports and performance-tuning culture | +0.01% | Metro concentrations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Average Vehicle Age and Mileage

Older cars now average over 10 years on Korean roads, doubling the frequency of lubricant changes as seals harden and oil oxidation accelerates. Hyundai service manuals cut suggested drain intervals to 7,500 km for severe use, compared with 15,000 km under normal conditions, effectively doubling annual engine oil demand per high-mileage vehicle [hyundai.com]. Prolonged ownership favors multi-grade formulations with seal-conditioning additives that combat leaks and sludge in worn engines. Rural fleets that once replaced vehicles at eight-year intervals now stretch retention past a decade, pushing cumulative lubricant volumes upward. Multigrade SAE 5W-30 still dominates, but high-mileage variants are gaining popularity within aftermarket workshops. The pattern remains most intense in the Seoul-Incheon corridor, where stop-and-go traffic raises engine stress and oil degradation.

Shift Toward Low-Viscosity Synthetic Formulations

Fuel-economy regulations are tightening each model year, steering OEMs toward 0W-20 and 0W-16 grades for hybrids and small-displacement turbo engines. HD Hyundai Oilbank became the first domestic refiner to secure API SQ and ILSAC GF-7 certification in January 2025, positioning itself at the front of premium supply[1]HD Hyundai Oilbank, “Company Press Release on API SQ Certification,” hyundaioilbank.com. Synthetics, priced 15-25% above mineral oils, now represent a double-digit share of trade-channel volumes, a margin sweet spot for marketers. Hybrid powertrains amplify cold-start events that benefit thin-film oils, while S-Oil’s Shaheen base-oil complex—slated for 2026—promises Group III+ output tailored to ultra-low-viscosity demand. Broad synthetic adoption supports extended drain intervals, reducing the need for workshop visits and promoting direct-to-consumer e-commerce channels for packaged lubricants.

E-commerce Driven Light-Duty Truck Utilization Surge

Parcel traffic from online retail climbed sharply post-pandemic, sending 1- to 3-ton trucks into congested urban loops that triple daily ignition cycles. Korea Energy Economics Institute data show logistics-fleet mileage rising faster than passenger-car usage, translating into earlier lubricant breakdown and frequent hydraulic-fluid changes for tail-gate lifts[2]Korea Energy Economics Institute, “Logistics Fuel Demand Analysis,” keei.re.kr. Operators increasingly specify premium ATF and low-SAPS engine oils, aiming to claw back fuel savings and downtime. National courier brands negotiate bundled lubricant contracts with refiners, while telematics analytics flag oil degradation in real time, tightening the link between mileage and maintenance purchases. Service chains around Incheon’s cargo district emerge as high-volume nodes for the South Korea automotive lubricants market.

OEM Warranty-Linked Lubricant Specification Compliance

Hyundai-Kia warranty terms explicitly require API SQ or higher oils, carrying internal approval codes, which directs vehicle owners to dealership bays or licensed aftermarket brands. The American Petroleum Institute’s adoption timeline for ILSAC GF-7 in 2025 cements OEM leverage over the aftermarket. Korean Industrial Standards embed these approvals into national quality law, creating a moat for brands that clear the certification hurdle. Premium pricing of 20-30% persists because consumers equate OEM endorsement with engine protection during the crucial 5-year/100,000 km warranty window. Approved blenders reciprocate by co-developing additive packages tuned to emerging powertrain nuances such as split-cycle turbo-hybrids.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and low-quality lubricant penetration | -0.04% | National, concentrated in aftermarket channels | Short term (≤ 2 years) |

| Crude-oil price volatility impacting feedstock costs | -0.03% | National, affecting all market participants | Medium term (2-4 years) |

| Under-developed used-oil collection and rerefining ecosystem | -0.02% | National, with regional collection gaps in rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Low-Quality Lubricant Penetration

The Korea Fair Trade Commission uncovered illegal blending rings in 2024, levying fines exceeding KRW 100 million and seizing drums that mimicked leading brands. Counterfeit packaging undercuts genuine products by 30-50%, luring price-sensitive drivers yet risking engine damage and warranty voidance. Online marketplaces amplify exposure, enabling anonymous merchants to sell unverified oils in small quantities. Reputable players counter with QR-code authentication and tamper-proof caps, but enforcement gaps remain in rural garages. Persistent quality concerns slow premiumization momentum and shave 0.04 percentage points off the South Korea automotive lubricants market's CAGR forecast.

Crude-Oil Price Volatility Impacting Feedstock Costs

Base-oil margins swing with Brent movements, and Korean refiners cite one- to two-week lags in passing cost changes to downstream blenders. The government’s 2024 fuel-tax adjustment—cutting the gasoline discount from 25% to 20%—exposed retailers to sudden price resets, compressing working-capital cycles. Smaller, independent blenders that import Group II/III base stocks face a foreign-exchange risk in addition to crude oil price fluctuations. Hedging strategies and flexible formulary planning become essential to shield EBITDA; however, price fluctuations remain a negative factor affecting volume growth.

Segment Analysis

By Product Type: Engine Oil Dominance Faces Synthetic Transition

Automotive engine oils accounted for 62.12% of 2024 consumption. Group III-based SAE 5W-30 and 0W-20 formulations rose the fastest within the bucket, as hybrid models demanded lower viscosities for fuel-economy compliance. The 2025 regulatory shift to API SQ/ILSAC GF-7 accelerates the move away from conventional 10W-30 mineral oils, allowing marketers to upsell synthetics carrying doubled drain intervals. Automatic transmission fluid, though just 12 million liters, logs the highest 0.51% CAGR due to multi-speed gearboxes and electrified drivetrains that heat ATF more severely than legacy four-speed units. Brake-fluid upgrades from DOT-3 to DOT-4 add small but high-margin liters, while electric power-steering fluid volumes wane as EPS adoption nears saturation.

The South Korea automotive lubricants market share structure inside engine oils tilts toward factory-fill alliances: SK Enmove supplies Hyundai-Kia assembly plants, HD Hyundai Oilbank services Renault Korea, and BP’s Castrol captures the imported European luxury car niche. The South Korea automotive lubricants market size for greases and specialty fluids remains under 5% but sees green-shoot growth as EVs require dielectric coolants for battery packs. Korean Industrial Standards help segregate premium GF-7-approved SK-branded oils from low-tier generics, sustaining high loyalty among drivers regarding oil-change brand selection.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: Commercial Expansion Outpaces Passenger Stability

Commercial vehicles accounted for just 43.9% of the total volume, yet are forecasted to rise at a 0.62% CAGR, the quickest among vehicle classes. Last-mile delivery fleets are pushing the frequency of engine oil changes from quarterly to bimonthly, as stop-start cycles cause the lubricant to break down sooner. Fleet managers adopt telematics-driven condition monitoring, ensuring oils are drained on measured viscosity loss rather than calendar months, thereby shifting spending from low-cost bulk to premium long-life synthetics. In contrast, passenger cars delivered 225.2 million liters, reflecting a stable replacement market with a 56.14% share but limited unit growth.

The South Korea automotive lubricants market size tied to two-wheelers stays marginal; however, 100% electric scooter mandates in select urban zones squeeze mineral two-stroke oil sales. Bus and heavy-truck operators are pivoting to low-SAPS CK-4/FA-4 diesel oils to meet the requirements of Euro VI import engines, thereby opening up cross-selling opportunities for SCR-fluid (DEF) providers. South Korea automotive lubricants market share across vehicle categories also mirrors warranty binding: 80% of Hyundai passenger vehicles return to dealer bays during the first five years, locking in brand-approved oils, whereas only 45% of small commercial trucks do so, leaving aftermarket players a wider hunting ground.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Greater Seoul-Incheon generated roughly one-third of South Korea automotive lubricants market volume in 2024, reflecting the highest vehicle density and congested driving that accelerates oil deterioration. Busan-Ulsan, anchored by port logistics and large refineries, claimed another 22% and benefits from its proximity to SK Energy and S-Oil base-oil plants, which trim freight costs on bulk deliveries. Central provinces, including Daejeon and Chungcheong, display lower per-capita consumption yet host a growing share of commercial-vehicle depots serving nationwide parcel routes.

The South Korea automotive lubricants market share for synthetics peaks in Gangnam and Bundang districts, where hybrid penetration tops 35%. Urban congestion here raises idle time, incentivizing drivers to adopt 0W-20 oils that mitigate fuel loss. In the southeast, heavy industrial sites in Ulsan drive bulk diesel-engine oil demand, while Hyundai Heavy Industries’ shipyards periodically drain marine gear oils that are formulated from automotive oils.

Refining capacity centered in Ulsan (1.1 million b/d) and Seosan (650,000 b/d) secures domestic base-oil supply, allowing exporters to ship surplus Group III to ASEAN markets. Once S-Oil’s Shaheen project comes online in 2026, Group III+ output will exceed local needs, potentially lowering domestic prices and making South Korea a regional hub for premium base stocks. Government carbon-neutrality policy pushes used-oil collection programs nationwide, with pilot re-refining plants in Gyeonggi delivering recycled base-oil streams that feed carbon-offset lubricant lines.

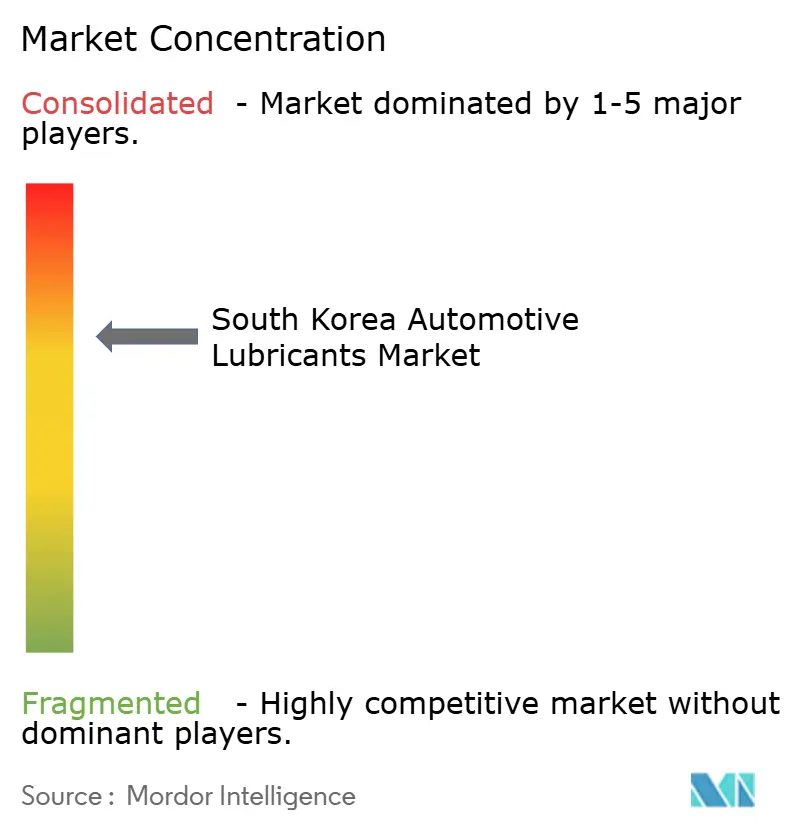

Competitive Landscape

The South Korea Automotive Lubricants Market is consolidated. International majors—Shell, BP, ExxonMobil—focus on imported premium packs sold through European and US vehicle dealer networks and big-box accessory chains. Meanwhile, counterfeit risk motivates brand owners to roll out blockchain-powered authenticity tags that are scanned at the point of sale. Cooperative R&D with Hyundai and Kia remains the prime moat: oils securing factory-fill status enjoy multi-year aftersales pull, locking rivals out of warranty-period volume.

South Korea Automotive Lubricants Industry Leaders

-

ExxonMobil Corporation

-

GS Caltex

-

S-Oil Corporation

-

SK inc.

-

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Auto components maker Gabriel India has formed a joint venture with South Korea's SK Enmove to diversify its product portfolio, incorporating lubricants and automotive engine oils. The strategic partnership represents a significant step forward in SK Enmove's revenue generation and expansion into new markets.

- June 2025: HD Hyundai Oilbank and Shell announced plans to enter the high-performance Group III base oil market. Their joint company, HD Hyundai Shell Base Oil, plans to commence full-scale commercial production of Group III base oils in South Korea by 2027. This will benefit the South Korean Automotive Engine Oils Market.

South Korea Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current volume outlook for South Korea automotive lubricants through 2030?

Demand will edge up from 401.49 million liters in 2025 to 411.22 million liters by 2030, a 0.48% CAGR driven by commercial-fleet mileage and synthetic-grade premiumization.

Which product category is expanding quickest in South Korea?

Automatic transmission fluid is the fastest-growing line, advancing at a 0.51% CAGR as multi-speed and hybrid gearboxes increase fill requirements.

How does vehicle age influence lubricant consumption patterns?

With the average car now older than 10 years, drain intervals tighten, doubling per-vehicle oil usage under severe driving, especially in Seoul-Incheon traffic.

Why are low-viscosity oils gaining share?

New fuel-economy rules and hybrid adoption push OEMs to specify 0W-20 and 0W-16 grades that reduce pumping losses and enable extended service intervals.

What risks do counterfeit lubricants pose?

Counterfeit oils, typically 30-50% cheaper, can void OEM warranties and accelerate engine wear, prompting regulators to intensify enforcement and brands to introduce authentication technologies.

Page last updated on: