Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

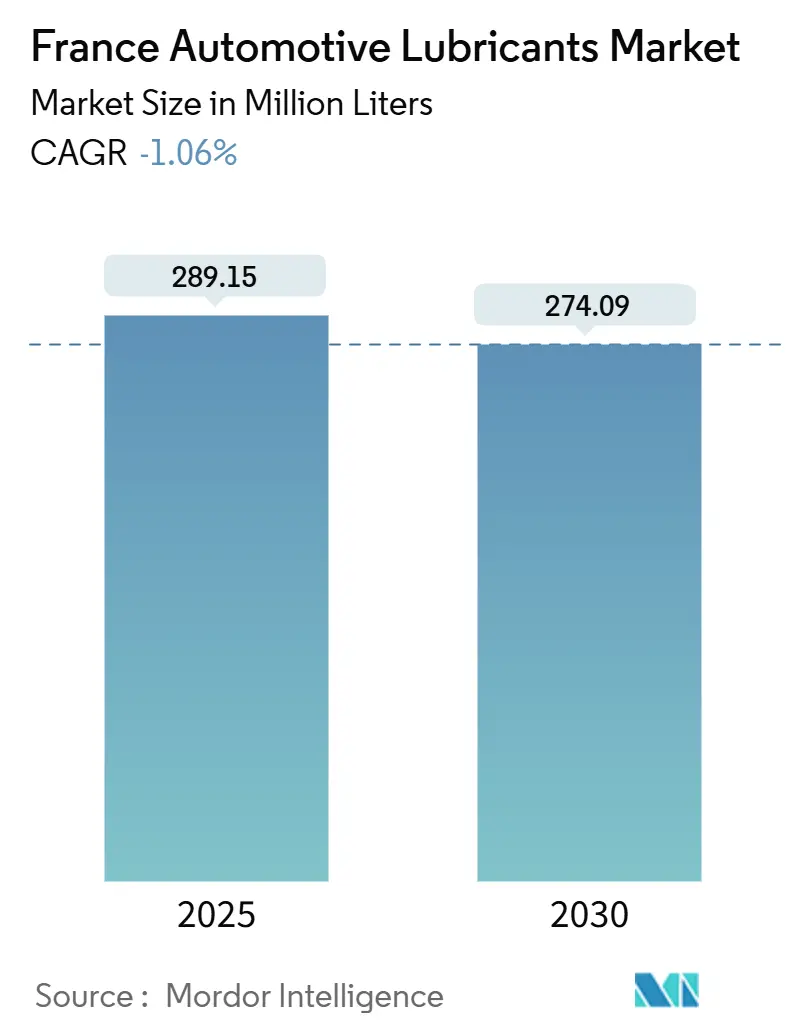

| Market Volume (2025) | 289.15 Million liters |

| Market Volume (2030) | 274.09 Million liters |

| Growth Rate (2025 - 2030) | -1.06% CAGR |

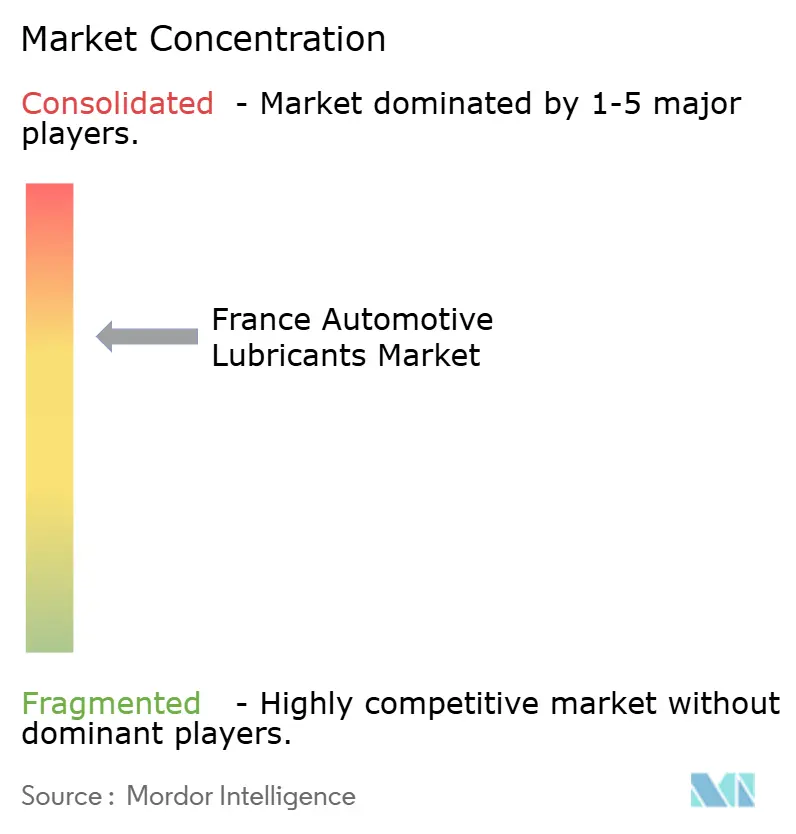

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Automotive Lubricants Market Analysis by Mordor Intelligence

The France Automotive Lubricants Market size is estimated at 289.15 million liters in 2025, and is expected to decline to 274.09 million liters by 2030, at a CAGR of -1.06% during the forecast period (2025-2030). This shrinkage signals a decisive pivot from volume expansion toward value-driven specialization as electrification, longer drain intervals, and Euro-7 regulations converge. Despite falling volumes, premium synthetic formulations, re-refined base oils, and digitally enabled service packages sustain supplier profitability. Commercial fleets continue to generate relatively stable demand, thanks to resilient goods movement activity and higher lubricant intensity per vehicle. Urban logistics growth, regulatory pushes for circularity, and the shift to telematics-based predictive maintenance collectively reshape route-to-market strategies across the France automotive lubricants market.

Key Report Takeaways

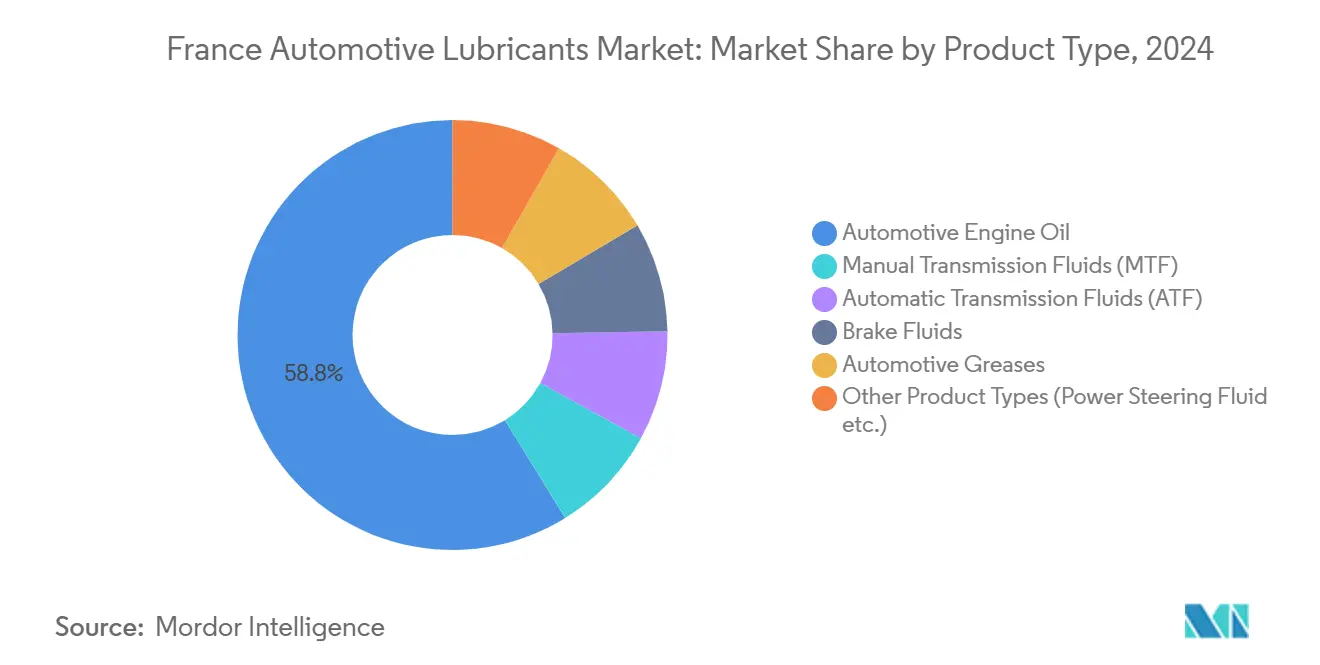

- By product type, automotive engine oil led with 58.78% of the France automotive lubricants market share in 2024. Automatic transmission fluids experienced the fastest decline, at a –0.89% CAGR, through 2030.

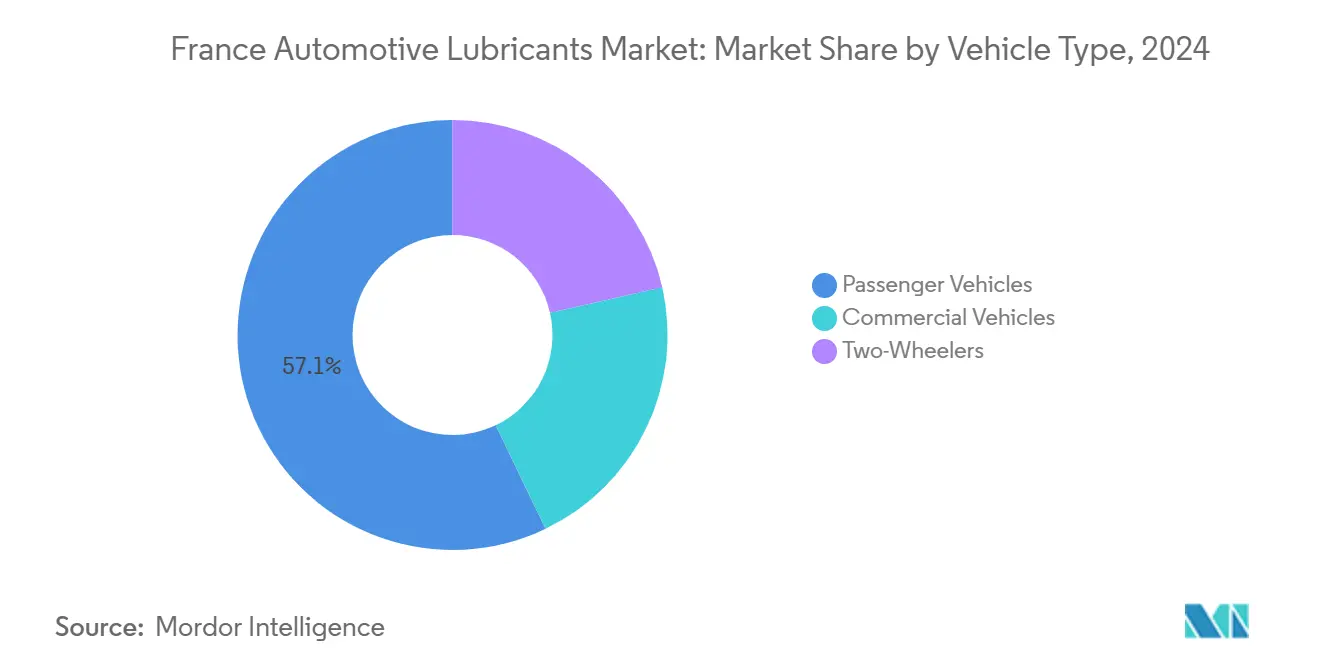

- By vehicle type, passenger vehicles accounted for 57.12% of the France automotive lubricants market size in 2024. Commercial vehicles posted the most resilient trajectory with a –0.67% CAGR through 2030.

France Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID rebound in new-vehicle registrations | +0.3% | National with spillover to adjacent EU markets | Short term (≤ 2 years) |

| Stricter Euro-7 limits driving low-viscosity oils | +0.2% | EU-wide with early uptake in France and Germany | Medium term (2-4 years) |

| Boom in last-mile delivery fleets | +0.4% | Paris, Lyon, Marseille, secondary cities | Medium term (2-4 years) |

| Expansion of car-sharing and subscription fleets | +0.1% | Metropolitan France | Long term (≥ 4 years) |

| Circular-economy law accelerating re-refined base-oil adoption | +0.2% | National and EU-aligned | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-COVID rebound in new-vehicle registrations

Commercial vehicle registrations in 2024 grew. The uptick in logistics trucks and vans is driven by the expansion of e-commerce and the reshoring of supply chains. Heavy-duty lubricants, therefore, maintain relevance as fleet operators prioritize uptime and reliability. Longer replacement cycles, typically five to seven years, help stabilize lubricant demand even as the total light-duty fleet electrifies more rapidly. Suppliers are channeling resources toward premium diesel engine oils, long-life coolants, and axle fluids specifically designed for high-load applications. As passenger car volumes dip, commercial fleets become the focal customer group across the France automotive lubricants market.

Stricter Euro-7 limits driving low-viscosity formulations

Euro-7 standards, effective in November 2026, introduce particle-number thresholds down to 10 nm and mandate emissions durability over extended lifespans[1]Jan Dornoff and Felipe Rodríguez, “Euro 7: The New Emission Standard for Light- and Heavy-Duty Vehicles in the European Union,” International Council on Clean Transportation, theicct.org. To comply, French OEMs are homologating 0W-20 and 0W-16 grades that cut friction and improve fuel economy by up to 2%. These light viscosities also carry low-SAPS additive packages to protect after-treatment systems. Synthetic base oils with high oxidative stability now dominate new-fill factory approvals, prompting blenders to reformulate portfolios. The regulation thereby elevates the value proposition of premium synthetics within the France automotive lubricants market.

Boom in last-mile delivery fleets

Urban delivery vans typically cover 200–300 kilometers daily under stop-start conditions. Telematics platforms capture real-time oil quality data, extending drain intervals by 15–25% through condition-based maintenance. Consequently, demand shifts from high-volume conventional grades to longer-lasting PAO- or GTL-based synthetics. Integrated service contracts, bundling lubricant supply, analytics, and filter management, create new revenue pools that offset the reduction in liters sold. Major service integrators negotiate national tenders, an arrangement that intensifies competition on technical support rather than on price alone within the France automotive lubricants market.

Expansion of car-sharing and subscription fleets

Shared vehicles accumulate triple or quadruple the mileage of privately owned cars, which amplifies lubricant consumption per unit even as total fleet size contracts. Operators demand factory-approved oils with documented performance over varied driving cycles to protect residual values. Extended-drain 0W-20 synthetics, combined with sensor-driven monitoring, help fleets meet availability targets while trimming workshop downtime. Suppliers winning these contracts typically bundle training, oil-sampling kits, and digital dashboards. The heightened utilization pattern thus supports premiumization despite overall volume pressure in the France automotive lubricants market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM-mandated extended drain intervals | –0.8% | EU premium brands | Medium term (2-4 years) |

| Rise of sealed oil-free e-axles | –0.4% | Global, accelerating in EU | Long term (≥ 4 years) |

| Telematics-based predictive maintenance reducing oil changes | –0.3% | Commercial fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OEM-mandated extended drain intervals

Premium European brands now approve 30,000-kilometer service intervals, cutting annual oil demand. The specifications require robust oxidative resistance and TBN retention, spurring a shift toward mid-SAPS and full-SAPS synthetics. French OEMs follow the pattern to lower warranty expenses. Workshops consequently see fewer visits and compensate by upselling higher-grade oils and ancillary services. While per-liter margins improve, the restraint remains the largest drag on volumes in the France automotive lubricants market.

Rise of sealed, oil-free e-axles

Integrated e-axles supplied by ZF and Bosch arrive factory-filled with lifetime greases, removing traditional gear oil requirements. Warranty coverage spans 200,000–300,000 kilometers, practically eliminating service-fill opportunities. This technological migration erodes demand for hypoid-gear oils but simultaneously opens niches for dielectric fluids and specialty greases. Suppliers diversify into these segments to cushion the impact on the France automotive lubricants market.

Segment Analysis

By Product Type: Engine oils retain dominance but face elective pressure

The French automotive lubricants market size for engine oils accounts for 58.78% of the total volume. A large ICE parc with an average age of 9.2 years supports baseline demand. Euro-7 promotes the mix toward 0W-20 and 0W-16 grades, thereby increasing synthetic oil penetration. Power steering fluids decline as EPS becomes universal, while brake fluids remain stable due to mandatory change intervals. Automatic transmission fluids post the steepest fall at –0.89% as sealed dual-clutch units proliferate.

Synthetic engine oils capture a growing share by meeting low-SAPS and volatility limits that safeguard particulate filters. Blenders deploy Group III+ and poly-alpha-olefin base stocks to ensure oxidation stability over 20,000- to 30,000-kilometer intervals. Long-life formulations enable workshops to compensate for fewer oil changes by charging premium rates. Re-refined content also rises, driven by incentives from the circular economy. Greases enjoy steady demand for wheel bearings, chassis points, and EV motor bearings, balancing reductions elsewhere within the France automotive lubricants market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: Commercial vehicles cushion overall decline

Passenger cars represented 57.12% of France's automotive lubricants market share in 2024; however, they are expected to shoulder the sharpest decline due to electrification and extended drain intervals. Hybrid powertrains further compress lubricant intensity by operating engines intermittently. Conversely, commercial vehicles exhibit a milder –0.67% CAGR through 2030. Long-haul trucks and buses consume two to three times more oil per vehicle than cars, preserving demand for 15W-40 and 10W-30 diesel oils certified for Euro VI‐E after-treatment systems.

Urban delivery vans transition steadily to electric powertrains, especially for routes under 200 kilometers. However, highway freight remains diesel-dependent given battery weight and charging constraints. As a result, the segment bifurcates: inner-city fleets shift to low-volume but high-margin specialty fluids, while inter-city fleets sustain large volumes of conventional grades. Two-wheelers maintain niche relevance, particularly in rural regions where commuter motorcycles rely on JASO-MA 10W-40 oils. Collectively, these dynamics moderate the volume contraction across the France automotive lubricants market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Production hubs in Île-de-France, Auvergne-Rhône-Alpes, and Hauts-de-France account for the bulk of domestic lubricant blending and automotive manufacturing. The proximity between Stellantis plants and TotalEnergies blending facilities reduces logistics costs and supports agile formulation changes aligned with the Euro-7 rollouts. Paris, Lyon, and Marseille anchor last-mile delivery activity, promoting demand for long-life 5W-30 diesels and synthetic greases. The Atlantic port cluster around Le Havre facilitates the import of Group II base oils, complementing ExxonMobil’s local re-refining output.

Rural regions exhibit higher ICE density, sustaining sales of mineral multigrades. Government scrappage schemes channel replacement toward hybrid or electric cars, gradually diluting those volumes. Cross-border trade with Belgium and Germany introduces competitive pressure from pan-European brands, yet domestic players leverage familiarity with French warranty and emissions rules. ADEME’s producer-responsibility framework ensures used-oil collection rates above 90%, funneling feedstock into re-refining facilities that underpin circular ambitions in the France automotive lubricants market.

Competitive Landscape

The France automotive lubricants industry is moderately consolidated. TotalEnergies pairs its refining integration with partnerships, such as the Point S service chain agreement. BP p.l.c. announced a strategic review of its Castrol unit, which could potentially reshape competitive dynamics across Europe[2]Jean-Guy Debord, “BP launches strategic review of global lubricants business,” Europétrole, euro-petrole.com. Re-refined base-oil initiatives create white-space for mid-tier blenders. Companies leverage motorsport pedigree to secure performance niches. New entrants specialized in EV thermal management fluids emerge, though current volumes remain small. Digitalization drives a pivot from product selling to service bundling, with suppliers embedding sensors and analytics in lubricant contracts. The combination of falling liters and rising service complexity intensifies competition on technical capability rather than on price within the France automotive lubricants market.

France Automotive Lubricants Industry Leaders

-

TotalEnergies

-

Shell plc

-

BP p.l.c.

-

Exxon Mobil Corporation

-

Motul

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: BP p.l.c. initiated the potential divestment of its Castrol lubricants division, valued at nearly USD 10 billion, as part of a USD 20 billion asset-rotation plan.

- May 2025: ExxonMobil France Holding is in exclusive talks to sell its 82.89% stake in Esso S.A.F. and its 100% stake in ExxonMobil Chemical France SAS to North Atlantic France SAS. While the Esso brand will remain at ~750 retail fuel stations, ExxonMobil will continue marketing lubricants, chemicals, and specialty products in France.

France Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast volume for automotive lubricants in France by 2030?

The France automotive lubricants market volume is projected to be 274.09 million liters by 2030, reflecting a -1.06% CAGR.

Which product category holds the highest share today?

Engine oils hold 58.78% of France's automotive lubricants market share, maintaining leadership despite declining volumes.

How will Euro-7 rules influence lubricant formulations?

Euro-7 drives adoption of low-viscosity 0W-20 and 0W-16 synthetics with low-SAPS additives to meet stricter particulate and durability limits.

Why are commercial fleets critical for future lubricant demand?

Commercial vehicles use two to three times more oil per unit than passenger cars and electrify more slowly, cushioning volume decline.

What role do re-refined base oils play in France?

Government circular-economy policy and new capacity at Gravenchon refinery make re-refined Group II stocks a growing feedstock for premium blends.

How are suppliers countering extended drain intervals?

Suppliers bundle digital monitoring, predictive analytics, and premium synthetics to capture higher value per liter despite fewer oil changes.

Page last updated on: