Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Volume (2025) | 200.10 Million liters |

| Market Volume (2030) | 243.21 Million liters |

| Growth Rate (2025 - 2030) | 3.98% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Colombia Automotive Lubricants Market Analysis by Mordor Intelligence

The Colombia Automotive Lubricants Market size is estimated at 200.10 million liters in 2025 and is expected to reach 243.21 million liters by 2030, at a CAGR of 3.98% during the forecast period (2025-2030). Growth remains moderate because a weakening peso and lingering inflation have increased lubricant prices since 2023; however, older engines still require short drain intervals, which sustain demand for volume. Commercial fleet modernization, tied to Euro VI adoption, the continuing motorcycle boom in dense urban corridors, and the expansion of quick-lube outlets in secondary cities, combine to widen aftermarket opportunities, even as counterfeit activity diverts a portion of the total volume. Currency depreciation has sparked down-trading toward mineral oils, but OEM-specified synthetics are gaining share among premium consumers, underscoring a two-tier product landscape within the Colombia automotive lubricants market.

Key Report Takeaways

- By product type, automotive engine oil led with a 61.78% share of the Colombia automotive lubricants market in 2024; automatic transmission fluids are projected to post the fastest 4.25% CAGR through 2030.

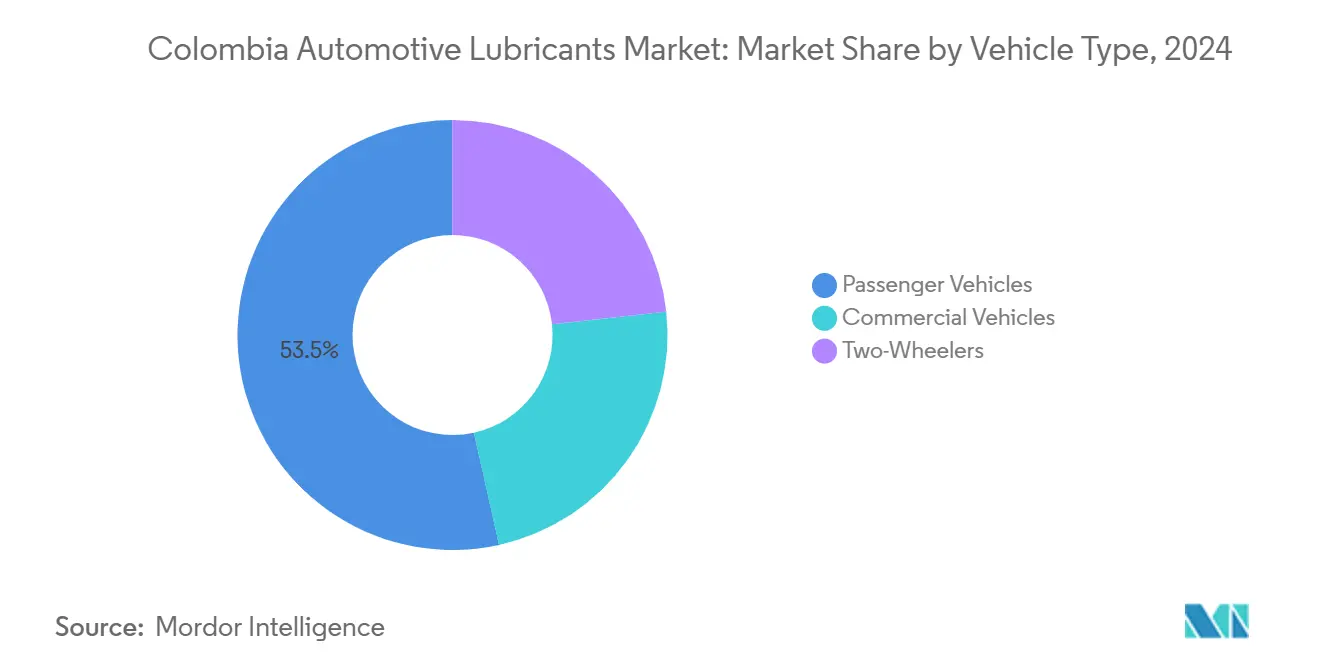

- By vehicle type, passenger vehicles accounted for 53.47% of the 2024 volume, whereas commercial vehicles are forecast to register the strongest growth rate of 4.41% from 2024 to 2030.

Colombia Automotive Lubricants Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising motorization and motorcycle boom | +1.2% | Bogotá, Medellín, Cali corridors | Medium term (2-4 years) |

| Aging fleet and higher oil-change frequency | +0.9% | National, stronger in rural areas | Long term (≥ 4 years) |

| Expansion of quick-lube and e-commerce channels | +0.7% | Urban and secondary cities | Short term (≤ 2 years) |

| Shift to premium synthetics and low-viscosity oils | +0.5% | Affluent urban segments | Medium term (2-4 years) |

| OEM-linked service contracts for fleets | +0.4% | Commercial and mining corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Motorization and Motorcycle Boom

Motorcycles make up for majority of Colombia’s vehicle parc, which keeps the Colombia automotive lubricants market firmly tied to two-wheeler usage patterns. Dense traffic, scarce parking, and a thriving last-mile delivery ecosystem in Bogotá, Medellín, and Cali push households and gig-economy riders toward affordable two-wheelers that need JASO T903-compliant oils for wet-clutch protection. Although each bike consumes far less lubricant than a car, high utilization—especially among delivery fleets—raises aggregate demand because oil change intervals can fall below 2,500 km under stop-and-go conditions. Motorcycle owners show willingness to pay moderate premiums for branded products that guard against ethanol-blended fuel corrosion, a dynamic that lifts value per liter compared with entry-level passenger-car oils. As e-commerce platforms broaden direct-to-consumer sales, rural riders also gain access to branded two-stroke and four-stroke formulations, reinforcing nationwide volume growth for the Colombia automotive lubricants market[1]MobilityPlaza, “Terpel expands LPG reach with new station in Colombia,” mobilityplaza.org .

Aging Fleet and Higher Oil-Change Frequency

Colombia’s 15.8-year average fleet age keeps conventional engine oils at the center of preventive maintenance culture and underpins a dependable demand floor for the Colombia automotive lubricants market. Older engines experience blow-by, worn seals, and elevated combustion deposits, which compel motorists to adhere to 3,000-5,000 km drain practices, resisting the extended intervals common in markets with newer vehicles. Rural areas that rely on aging pickups and SUVs for agricultural transportation magnify this effect, recording even higher average vehicle ages than their urban counterparts. Heavy-duty units in mining and agriculture often exceed 25 years of service, which amplifies lubricant consumption due to severe duty cycles and dusty environments that accelerate oil degradation. Budget-constrained owners of legacy fleets frequently opt for multi-grade 20W-50 or 15W-40 mineral oils that balance cost and protection, ensuring that value-tier brands remain highly relevant within the Colombia automotive lubricants market.

Expansion of Quick-Lube and E-Commerce Channels

Fast-service chains and online storefronts are shrinking service gaps created by Colombia’s challenging topography, thereby unlocking incremental litres for the Colombia automotive lubricants market. Quick-lube outlets in metropolitan service stations complete an engine oil change in under 30 minutes, contrasting with traditional talleres that can take half a day and require advance appointments. Parallel e-commerce growth enables suppliers to reach secondary cities, such as Bucaramanga and Villavicencio, where brick-and-mortar distribution remains limited, often offering same-week delivery and bundled filter kits that foster customer loyalty. Together, these channels elevate brand visibility, widen the availability of premium offerings, and increase the frequency of change by simplifying access to OEM-approved products, further energizing the Colombia automotive lubricants market.

Shift to Premium Synthetics and Low-Viscosity Oils

Despite household budget strain, Colombian consumers buying late-model vehicles are encountering API SP and ILSAC GF-6A/B factory fills that require 0W-20 or 5W-20 synthetic oils, nudging demand toward higher-value SKUs within the Colombia automotive lubricants market. Chevrolet, Kia, and Ford dealers bundle first-service coupons that lock customers into synthetic usage cycles, while independent garages in affluent districts of Bogotá adhere to these specifications to maintain warranty compliance. Chevron manufactures Havoline PRO-DS domestically, meeting Ford WSS and GM dexos1 Gen 3 approvals, thereby lowering price barriers against imported synthetics that face a weak peso. Even so, persistent inflation prompts many drivers to alternate between synthetic and mineral fills, reflecting a tiered market where premium adoption rises in urban centers but conventional products remain dominant nationally. Over the forecast period, broader fuel-economy mandates are expected to increase synthetic penetration, underpinning mix improvements for the Colombia automotive lubricants market.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic slowdown and inflation | -0.8% | National, stronger in rural areas | Short term (≤ 2 years) |

| Stricter waste-oil disposal regulation | -0.3% | Major cities | Medium term (2-4 years) |

| Counterfeit and grey-market lubricant penetration | -0.5% | Border and informal channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic Slowdown and Inflation

The peso’s slide against the USD since 2023 and consumer-price inflation have forced households to delay maintenance and extend oil drains, curbing near-term volume for the Colombia automotive lubricants market. Import-heavy base-oil supply chains transmit exchange-rate weakness directly into shelf prices, thereby widening the gap between synthetics and mineral oils and accelerating a shift in consumer preference toward value tiers. Commercial transport operators hedge by bulk-buying during favorable currency windows; however, many small fleets simply lengthen their maintenance cycles, eroding premium throughput. Inflation cuts discretionary spend on vehicle upgrades, dampening new-car imports that typically rely on low-viscosity synthetics, thereby postponing mix upgrades. Although inflation is projected to settle below 4% by 2026, the immediate drag on disposable income remains the single largest short-term headwind for the Colombia automotive lubricants market.

Stricter Waste-Oil Disposal Regulation

ANLA’s tighter enforcement of Decreto 1076 de 2015 increases handling costs by mandating licensed collection, storage tanks with secondary containment, and cradle-to-grave documentation, which many small garages struggle to finance. Collection rates lag far behind those in developed markets, prompting regulators to require proof of waste-oil pickup before renewing environmental permits. Larger blenders may integrate in-house rerefining or contract with certified recyclers to turn used oil back into base stock, potentially unlocking a circular-economy margin, but this approach also raises capital expenditure. Informal workshops that fail to meet new standards risk closure or migration to illicit dumping, which would reduce the sales of legal lubricants captured in official statistics. Over the medium term, compliance investments by organized players are expected to strengthen brand trust and filter out non-compliant competitors, gradually stabilizing the Colombia automotive lubricants market[2]Autoridad Nacional de Licencias Ambientales (ANLA), “¿Qué es el PARP?,” anla.gov.co .

Segment Analysis

By Product Type: Engine Oil Dominance Amid Transmission Fluid Growth

Automotive engine oil captured 61.78% of the Colombia automotive lubricants market share in 2024, thanks to the country’s aging fleet and short drain intervals. Within that base, 15W-40 SAE multigrades remain the workhorse for legacy gasoline and diesel engines, while 0W-20 synthetics for turbocharged gasoline units are gaining ground from a low base. Automatic transmission fluid volume is projected to outpace all other products at a 4.25% CAGR through 2030, reflecting the rising share of imported passenger cars equipped with six- and eight-speed automatics and the late-cycle adoption of continuously variable transmissions. Gear-box complexity lifts per-vehicle fill requirements and shortens change intervals, supporting segment revenues even as unit counts plateau. Manual transmission and differential oils continue to serve enduring demand in light commercial fleets and rural pickups, which still favor stick-shift drivetrains. Meanwhile, brake fluids are experiencing a gradual shift from DOT 3 to DOT 4 as ABS penetration increases. Automotive greases cater to chassis, CV-joint, and industrial uses, dominated by NLGI Grade 2 lithium-complex formulations that tolerate Colombia’s hot, humid lowlands and cooler Andean altitudes.

Price sensitivity shapes product bifurcation within the Colombia automotive lubricants market. Synthetics claim growing market share because OEM warranty clauses for late-model SUVs and crossovers specify API SP 0W-20 or 5W-30, yet mineral oils retain a dominant market share where parity alloy engines run on less sophisticated additive packages. Domestic blending by Chevron and Terpel mitigates forex exposure for synthetic SKUs, narrowing the price gap with imports from the United States or Singapore and easing adoption barriers. Small-batch blenders competing at the economy end flood the market with 20W-50 monogrades that attract cost-conscious taxi drivers despite lower fuel-economy performance.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: Commercial Vehicles Drive Growth Despite Passenger Car Dominance

Passenger vehicles generated 53.47% of the 2024 volume; however, subdued new-car imports and rising drain intervals in modern engines limit the segment’s litre growth. Conversely, commercial vehicles, ranging from Class 3 pickups serving agro-logistics to Class 8 tractor-trailers hauling coal, are projected to register a 4.41% CAGR through 2030, outstripping all other categories within the Colombia automotive lubricants market. Euro VI adoption under the upcoming diesel emission norms requires higher-tier CK-4 oils to handle stricter soot limitations and extended 40,000-km intervals, while lifting the per-fill value even as the lube frequency declines slightly. Mining fleets operating in the Cesar and Antioquia departments subject their engines to high loads, dusty air, and rugged topography, which accelerates oil oxidation and necessitates more frequent changes, despite the use of better formulations. Government fleet-renewal tenders for buses and refuse trucks stipulate the use of OEM-approved synthetics, reinforcing premium-tier volumes that are independent of consumer purchasing cycles.

Two-wheelers form the largest absolute vehicle count but contribute a lower absolute volume of litres; however, their rapid parc expansion makes them material to medium-term growth for the Colombia automotive lubricants market size at the segment level. Delivery companies and ride-hailing platforms conduct oil changes every 2,000-3,000 km, escalating per-bike consumption beyond that of recreational riders. Most bikes require 10W-30 or 20W-40 JASO MA oils that safeguard wet clutches, providing blender differentiation through friction modifiers and ethanol resistance. While electric motorcycles are entering pilot fleets, their share is unlikely to significantly impact lubricant demand before 2030, given the limited charging infrastructure and higher upfront costs associated with them. Collectively, the commercial-vehicle corridor, bolstered by mining, logistics, and public-transport upgrades, provides the most resilient growth pocket for the Colombia automotive lubricants market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Bogotá, Medellín, and Cali account for a significant portion of national lubricant consumption, driven by dense vehicle populations, robust disposable income, and full-service stations that promote premium SKUs. Within these cities, the Colombia automotive lubricants market size benefits from dealer-installed synthetics and quick-lube chains clustered near residential hubs. The Andean freight corridor linking Bogotá to the Caribbean port of Cartagena funnels heavy-truck traffic that elevates CK-4 diesel-engine oil demand, while express bus operators headquartered in Bogotá favor 10W-40 low-SAPS synthetics to comply with Euro VI. Coastal regions leverage port proximity to import base stocks and finished oils; yet, Buenaventura simultaneously acts as the primary gateway for counterfeit oil, especially for low-priced 20W-50 products targeting informal retailers along the Pacific coastal belt.

Rural departments rely on conventional multigrade oils sold through hardware stores because distribution chains are fragmented and purchasing power is lower; nonetheless, agricultural mechanization and government road-building efforts drive rising consumption of hydraulic fluids, greases, and heavy-duty engine oils in these regions. Mining clusters in Cesar, La Guajira, and Antioquia create a lumpy but sizable offtake for severe-duty lubricants, with on-site bulk tanks replenished via contracted tanker trucks to minimize downtime. The Pacific corridor experiences constrained road quality and higher logistics costs, which reduce brand diversity. Regional players with small blending lines in Cali and Palmira fulfill immediate demand more efficiently than multinational brands shipping from Bogotá or Barranquilla. Border zones with Venezuela and Ecuador experience heavy grey-market infiltration due to tariff differentials, which suppresses formal-sector volumes and complicates enforcement for the Colombia automotive lubricants market.

Competitive Landscape

The Colombia automotive lubricants market remains moderately consolidated. Terpel capitalizes on its stations to bundle quick-lube services, loyalty apps, and co-branded credit cards, ensuring visibility across all income brackets. White-space opportunities lie in motorcycle-specific lubricants, waste-oil rerefining, and digital-only distribution; however, success depends on navigating ANLA permitting, anti-counterfeit traceability, and logistics across the Andes. E-commerce-first entrants offer national shipping and QR authentication, but struggle with after-sales service and returns, which has limited their share gains so far. Counterfeiting remains the most persistent competitive threat, eroding trust and margins; legitimate players have responded with holographic seals, SMS verification, and dealership audits, but enforcement gaps keep grey-market volumes elevated. The Colombia automotive lubricants market, therefore, balances stable volumes in a sizable aftermarket against structural challenges from economic volatility, regulatory burden, and illicit competition.

Colombia Automotive Lubricants Industry Leaders

-

Terpel

-

Shell plc

-

Chevron Corporation

-

BP p.l.c.

-

BioMax

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: BP p.l.c. has initiated the divestment process for its Castrol lubricants division, valued at up to USD 10 billion, a move that could significantly reshape the supply dynamics for premium synthetic lubricants in Latin America.

- March 2025: Saudi Arabian Oil Co., bolstering its foothold in Colombia's automotive lubricants market, has completed its USD 3.5 billion acquisition of Primax, gaining control of 914 active service stations.

Colombia Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will Colombia’s automotive lubricant demand be by 2030?

Consumption is forecast to reach 243.21 million liters by 2030, expanding at a 3.98% CAGR from 2025 levels.

Which product accounts for the most lubricant litres today?

Engine oil dominates with 61.78% of the 2024 volume because frequent changes are common for the 15.8-year-old national fleet.

What is driving the fastest growth among lubricant products?

Automatic transmission fluids are projected to post the strongest 4.25% CAGR through 2030, as the number of imported cars with advanced gearboxes increases.

Why are commercial vehicles a key growth segment?

Euro VI adoption and mining-sector expansion push heavy-duty fleets toward premium extended-drain lubricants, supporting a 4.41% CAGR.

What role do quick-lube stations play in demand?

Express bays attached to fuel stations shorten service times to under 30 minutes, increasing the frequency of changes and premium-product uptake across urban centers.

Page last updated on: