Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

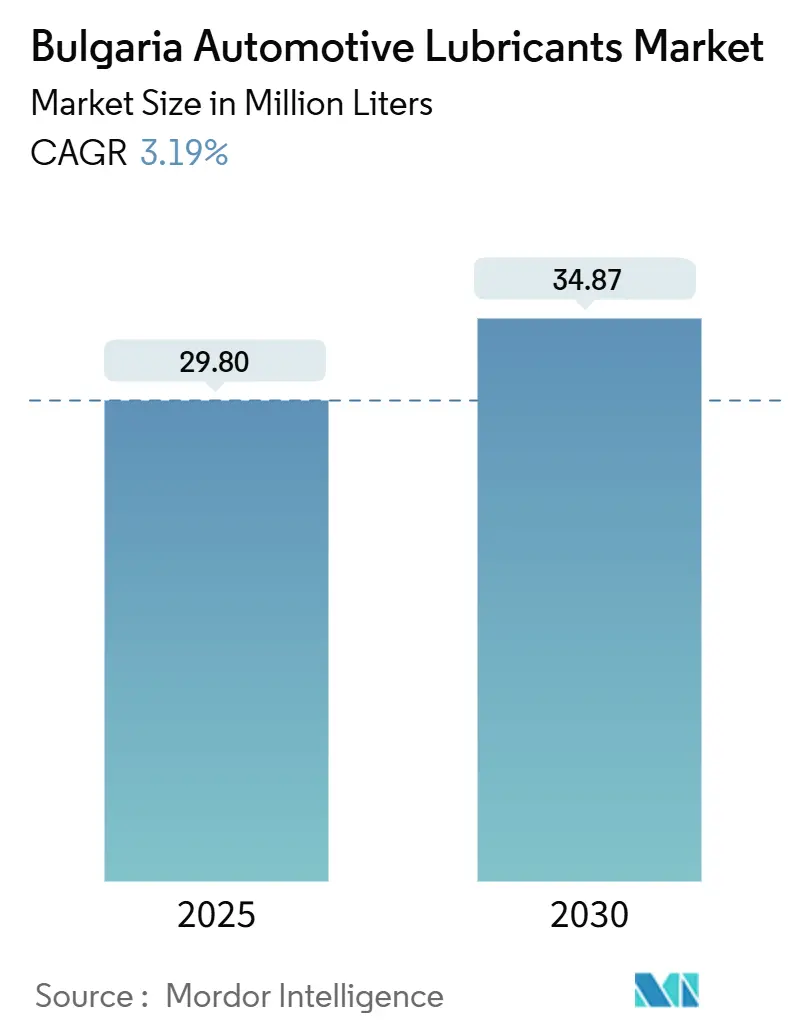

| Market Volume (2025) | 29.80 Million liters |

| Market Volume (2030) | 34.87 Million liters |

| Growth Rate (2025 - 2030) | 3.19% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bulgaria Automotive Lubricants Market Analysis by Mordor Intelligence

The Bulgarian Automotive Lubricants Market size is estimated at 29.80 million liters in 2025, and is expected to reach 34.87 million liters by 2030, at a CAGR of 3.19% during the forecast period (2025-2030). Strategic placement along the EU–Balkan freight corridor, an aging vehicle fleet, and delayed electrification compared with Western Europe anchor steady volume growth. International freight operations account majority of domestic road-transport activity, so long-haul trucks sustain demand for premium heavy-duty engine oils. Passenger-car owners are increasingly adopting extended-drain synthetics, yet high vehicle age keeps total lubricant consumption relatively resilient. Preparations for Euro 7 emission rules are accelerating the switch to low-viscosity, additive-rich formulations. Online direct-to-consumer channels expand access to branded products, while bio-based additive innovations enable brands to differentiate themselves under stricter EU Ecolabel criteria.

Key Report Takeaways

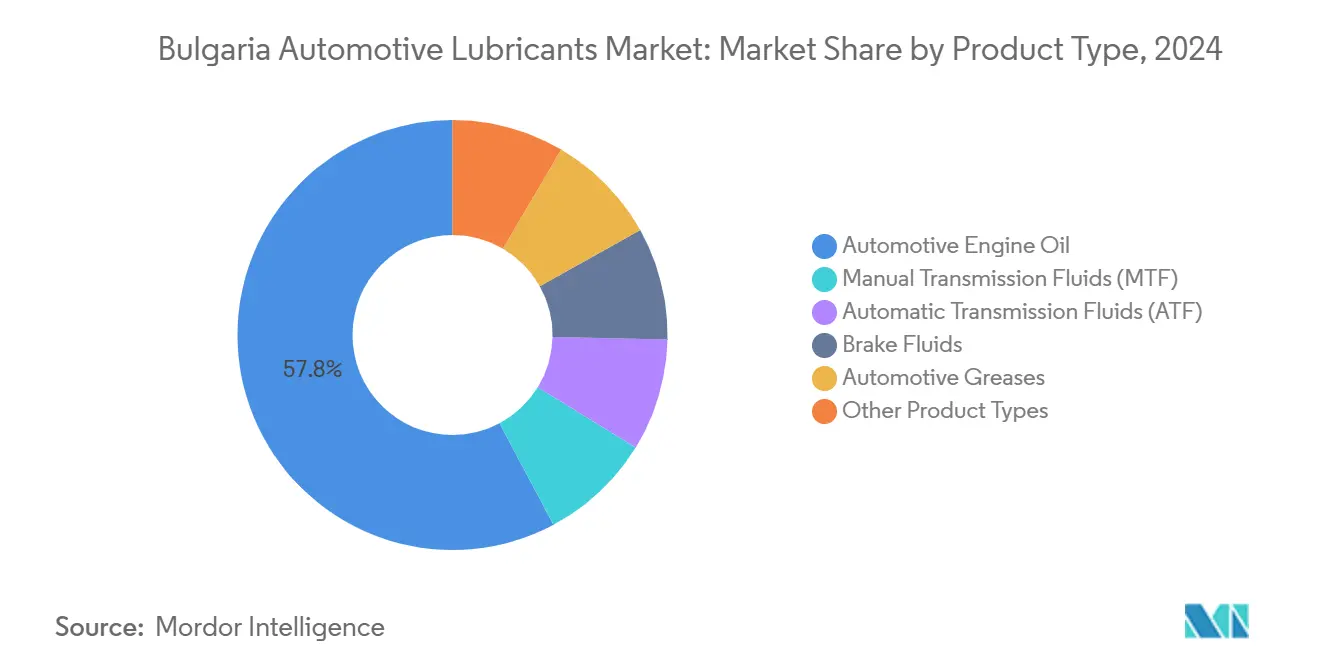

- By product type, engine oil led the Bulgarian automotive lubricants market with a 57.78% share in 2024, whereas automatic transmission fluids were projected to record the fastest growth at a 3.37% CAGR through 2030.

- By vehicle type, passenger vehicles accounted for 59.23% of the Bulgarian automotive lubricants market size in 2024, while commercial vehicles posted the highest 3.42% CAGR during the forecast period.

Bulgaria Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing passenger-car parc and longer drain intervals | +0.8% | Sofia, Plovdiv metros and national fleet | Medium term (2-4 years) |

| Post-COVID freight boom in EU–Balkan corridor | +1.2% | National; spillover to Romania, Serbia, Greece | Short term (≤ 2 years) |

| EU Euro 7 low-viscosity compliance push | +0.6% | EU-wide with early adoption in commercial fleet | Long term (≥ 4 years) |

| Growing online DIY motor-oil culture | +0.4% | Urban centers, expanding to rural via e-commerce | Medium term (2-4 years) |

| Bio-based additive breakthroughs | +0.3% | EU regulatory space; Bulgaria rollout 2025-2027 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Passenger-Car Parc and Longer Drain Intervals

The average Bulgarian passenger car typically operates well beyond its recommended retirement age, so owners prioritize cost-effective maintenance over vehicle replacement. Synthetics that allow service intervals of 15,000 km or more are gaining popularity; however, harsh stop-and-go city traffic often necessitates earlier oil changes. Higher-quality formulations, therefore, move in greater volumes per service, offsetting any downward effect from reduced workshop visits.

Post-COVID Freight Boom in EU–Balkan Corridor

Bulgarian heavy-goods vehicles now average 129,500 km annually, with cross-trade trips above 1,000 km[1]Eurostat, “Road freight transport by journey characteristics,” ec.europa.eu. Long-haul intensity demands multigrade engine oils and transmission fluids that meet a diverse slate of ACEA and OEM approvals, favoring brands with Europe-wide recognition. The freight surge lifts the Bulgarian automotive lubricants market through elevated drain frequency and higher average fill volumes.

EU Euro 7 Low-Viscosity Compliance Push

Euro 7 introduces crankcase emission monitoring down to 10 nm particles and extends durability targets to 160,000 km[2]Official Journal of the European Union, “Regulation (EU) 2024/1257 (Euro 7),” eur-lex.europa.eu. Lubricants must meet OEM specifications under real-world driving emissions tests, thereby elevating demand for low-viscosity 0W-20 and 0W-30 grades with robust antioxidant and antiwear packages. Suppliers that document sensor compatibility and particulate-filter protection gain a competitive edge in the Bulgarian automotive lubricants market.

Growing Online DIY Motor-Oil Culture

E-commerce platforms deliver wider choice and competitive pricing, encouraging motorists to perform basic oil changes at home. Instructional content improves product-selection accuracy, expanding premium-grade uptake beyond large cities. However, vendors must reinforce usage guidance to avoid warranty conflicts, particularly as Euro 7 rolls out.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV adoption in Sofia and Plovdiv | –0.4% | Urban charging-infrastructure hubs | Medium term (2-4 years) |

| Shrinking two-wheeler parc | –0.2% | National, acute in cities | Short term (≤ 2 years) |

| Surge in counterfeit lubricants via gray imports | –0.3% | Border regions, price-sensitive buyers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV Adoption in Sofia and Plovdiv

Battery-electric vehicle registrations declined in 2024, yet policy grants and charger rollouts in major cities indicate potential future volume gains. While the immediate impact on the Bulgarian automotive lubricants market is small, drivetrain electrification is gradually eroding demand for engine oils, shifting the focus toward e-axle gear oils, thermal-management fluids, and brake fluids compatible with regenerative systems.

Shrinking Two-Wheeler Parc

Urban modal shifts toward more comfortable passenger cars and improved public transit are reducing motorcycle registrations. Although two-wheelers consume modest lubricant volumes, their decline marginally restrains market growth.

Segment Analysis

By Product Type: Engine Oil Dominance Drives Volume Growth

Automotive engine oil captured 57.78% of the Bulgarian automotive lubricants market share in 2024, a level sustained by dense freight traffic and an aged passenger-car fleet. Demand concentrates in multigrade SAE 10W-40 and 5W-30 synthetics that satisfy mixed fleets spanning Euro 3 to Euro 6 emission tiers. Automatic transmission fluids are expected to advance at a 3.37% CAGR, reflecting the rising consumer preference for automatic gearboxes and the shift in technology to eight- and ten-speed units that require specialist friction modifiers.

Synthetic and semi-synthetic blends continue to displace mineral formulations as Euro 7 promotes low-viscosity oils for fuel economy gains. Brake-fluid uptake benefits from the mandatory fitment of ABS and ESC, while power-steering fluid volumes decrease as electric steering systems proliferate. Niche greases for chassis and wheel bearings post stable gains tied to fleet expansion rather than technological change. Suppliers with broad ACEA C-grade portfolios and multipack SKUs retain an edge across Bulgaria’s fragmented retail landscape.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: Commercial Segment Accelerates Growth

Passenger cars accounted for 59.23% of the Bulgarian automotive lubricants market volume in 2024, driven by growth in new registrations and the dominance of ICE powertrains. Commercial vehicles, however, are poised for a faster 3.42% CAGR through 2030, as cross-trade heavy trucks average more than 129,000 km each year. High utilization rates result in shorter drain intervals and increased per-vehicle consumption of heavy-duty engine oils and driveline fluids.

Two-wheeler lubricant demand is under pressure from declining registrations, though rural delivery and agricultural niches sustain limited volumes. Future segment growth hinges on extended-drain synthetic penetration among light-duty vans and the introduction of Euro VI-E heavy-duty oil specifications, which emphasize lower sulfated ash and phosphorus levels to protect after-treatment devices.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Sofia accounts for the largest share of passenger-vehicle lubricant purchases, supported by higher household incomes and a dense network of service stations. Burgas anchors supply security through the Neftohim refinery, allowing consistent availability of both mineral and synthetic grades. Cross-border corridors with Romania, Serbia, and Greece generate continuous demand for heavy-duty lubricants that meet multiple OEM approvals, reinforcing the importance of pan-European brands in the Bulgarian automotive lubricants market.

Coastal regions combine maritime freight, tourism, vehicle traffic, and agricultural machinery, creating a diverse product mix profile. Mountainous areas impose extreme temperature swings and steep gradients, which favor premium multigrade synthetics with enhanced thermal stability. Border districts are grappling with counterfeit inflows, which lead to regional sales spikes for lower-priced, unverified products and prompt licensed distributors to intensify their education efforts.

EU cohesion fund road upgrade projects and Recovery and Resilience Plan financing will widen highways and logistics hubs, indirectly increasing lubricant volumes by stimulating commercial vehicle traffic. Nevertheless, uneven enforcement of waste-oil collection targets limits re-refined base-oil availability outside major cities, requiring brands to truck products back to centralized facilities for recycling.

Competitive Landscape

The Bulgarian automotive lubricants market is moderately consolidated. OMV employs a supply-chain security narrative, leveraging three regional refineries and robust warehousing to ensure delivery even during geopolitical disruptions. Across all tiers, firms invest in QR-based authenticity labels, e-commerce storefronts, and lubricant-condition monitoring as value-added services. Sustainability orientation now shapes competitive positioning. Brands capable of meeting EU-mandated 25% bio-carbon thresholds and supplying recycled-content packaging stand to gain shelf preference in major chains. Technical support for fleet Euro 7 compliance, coupled with countrywide used-oil take-back programs, further differentiates market leaders in Bulgaria’s environmentally evolving supply environment.

Bulgaria Automotive Lubricants Industry Leaders

-

Prista Oil

-

Shell plc

-

TotalEnergies

-

Exxon Mobil Corporation

-

Lukoil

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: BP p.l.c. announced plans to divest its Castrol lubricants unit, valued up to USD 10 billion, signaling a strategic pivot toward upstream hydrocarbons. The potential sale could reshape Castrol’s distribution footprint in Bulgaria’s automotive engine oil segment.

- March 2024: Alpha Bulgaria shareholders approved the purchase of up to 200,000 shares in Prista Oil Holding for BGN 20 million (USD 11.1 million), aiming to strengthen domestic lubricant production capacity and export reach.

Bulgaria Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current volume of lubricants sold for vehicles in Bulgaria?

The Bulgarian automotive lubricants market size is 29.80 million liters in 2025.

How fast will demand grow over the next five years?

Total volume is forecast to post a 3.19% CAGR, reaching 34.87 million liters by 2030.

Which product category dominates domestic sales?

Engine oil accounts for 57.78% of the overall volume, largely due to an older fleet of ICE-heavy vehicles.

Why are commercial vehicles the fastest-growing segment?

Post-COVID freight expansion pushes heavy trucks to average 129,500 km annually, lifting lubricant change frequency.

How will Euro 7 regulations affect lubricant specifications?

Euro 7 drives the adoption of low-viscosity synthetics with advanced additive systems to meet tighter crankcase emission limits.

Page last updated on: