Zero Trust Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 48.43 Billion |

| Market Size (2031) | USD 102.01 Billion |

| Growth Rate (2026 - 2031) | 16.07% CAGR |

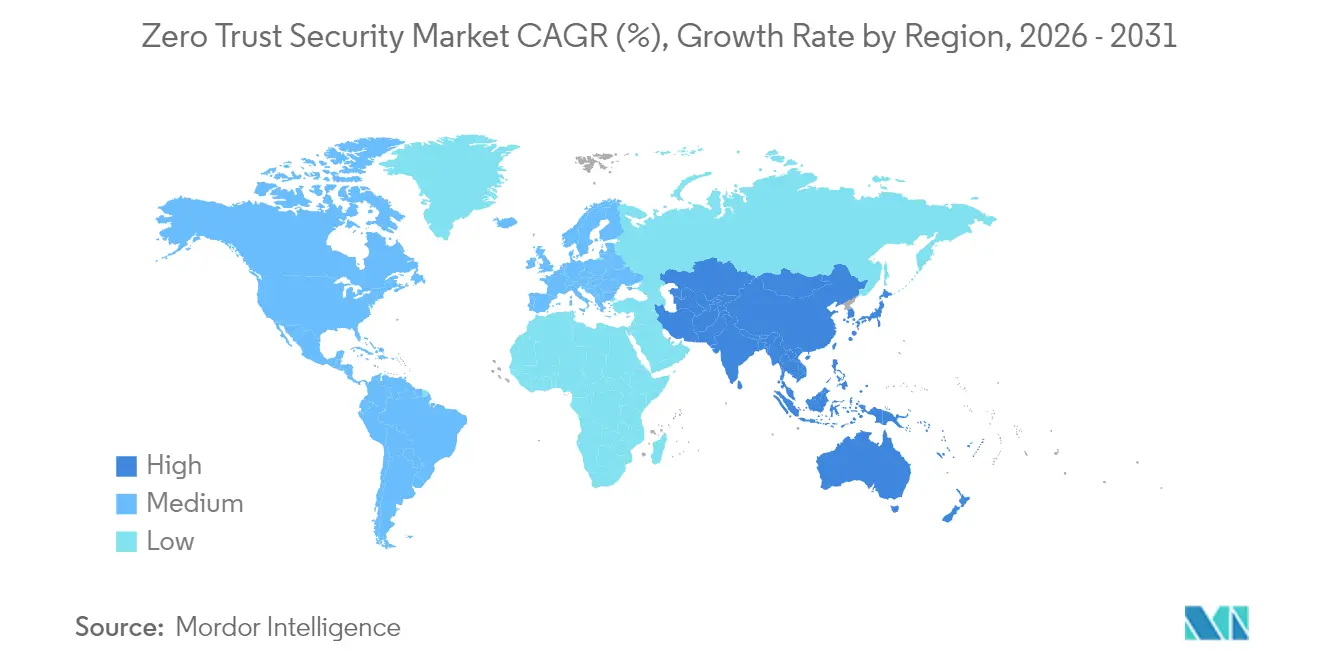

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

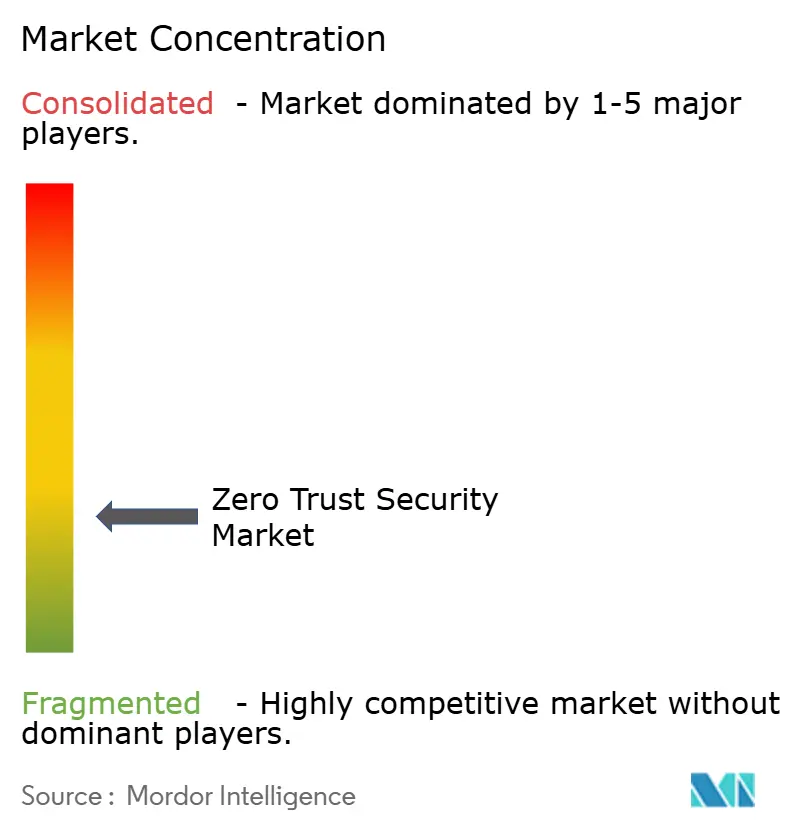

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zero Trust Security Market Analysis by Mordor Intelligence

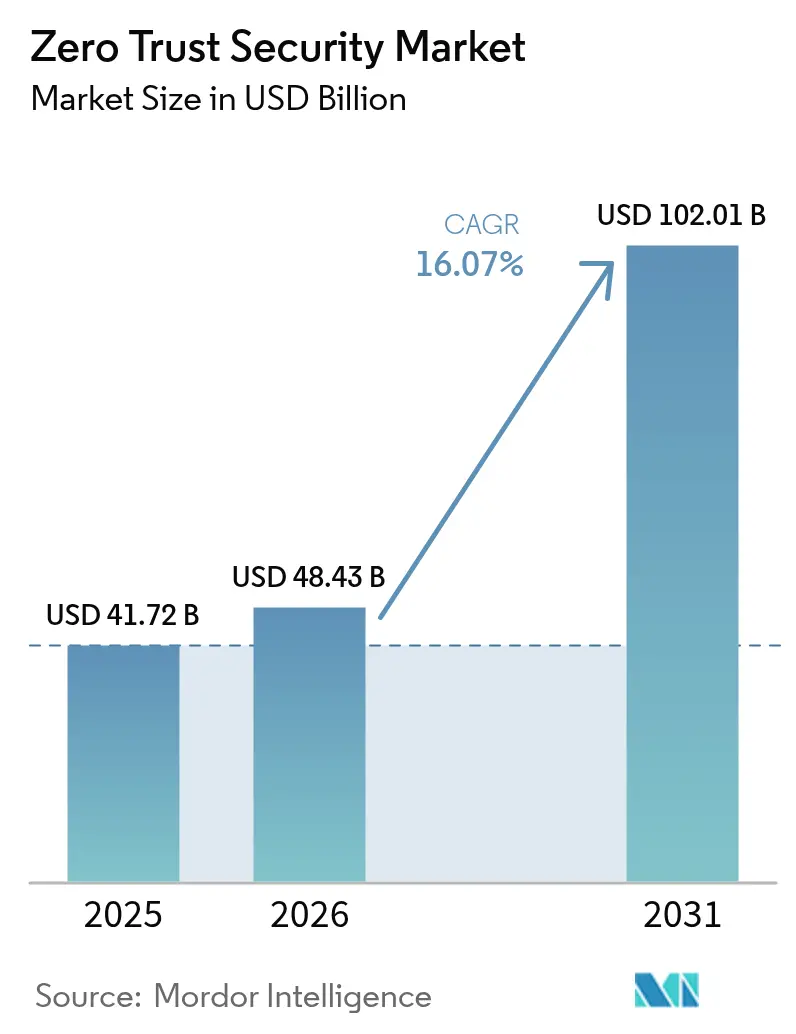

The Zero Trust Security market size is expected to grow from USD 41.72 billion in 2025 to USD 48.43 billion in 2026 and is forecast to reach USD 102.01 billion by 2031 at 16.07% CAGR over 2026-2031. Remote work permanence, cloud-native architectures, and escalating breach costs push organizations away from perimeter-centric defenses toward continuous verification models that harden every asset. Regulatory mandates—from the 2021 United States executive order to evolving data-protection rules in Europe and Asia—continue to codify zero trust requirements. Enterprises also confront a surge in machine-to-machine traffic that exposes unsecured APIs, while ransomware incidents now touch virtually every industry segment. Vendors respond by embedding identity, network, and endpoint controls into unified cloud platforms, driving a steady shift from product sales to outcome-based service engagements.

Key Report Takeaways

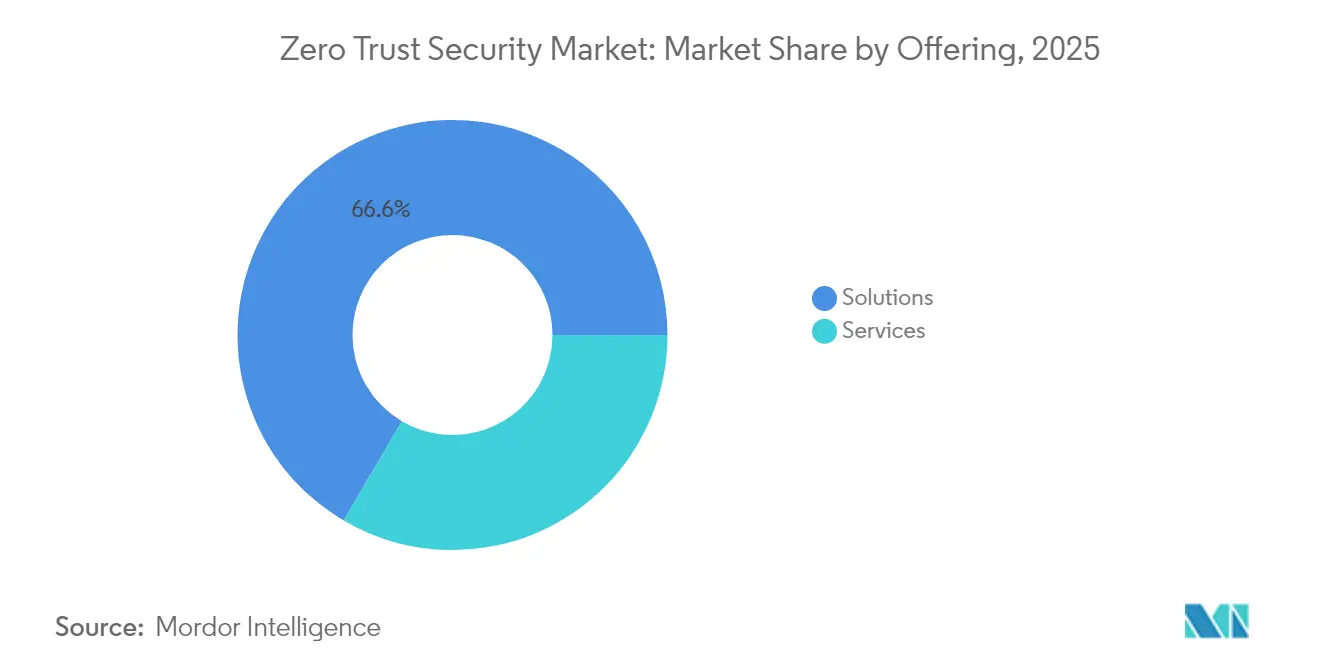

- By offering, Solutions led with 66.55% revenue share in 2025, yet Services are forecast to advance at a 19.05% CAGR through 2031.

- By deployment mode, On-premise held 53.85% of the zero trust security market share in 2025, while Cloud deployments are expanding at a 19.66% CAGR to 2031.

- By organization size, Large enterprises accounted for 59.62% of spending in 2025; small and medium-sized enterprises (SMEs) are poised to grow at an 18.02% CAGR.

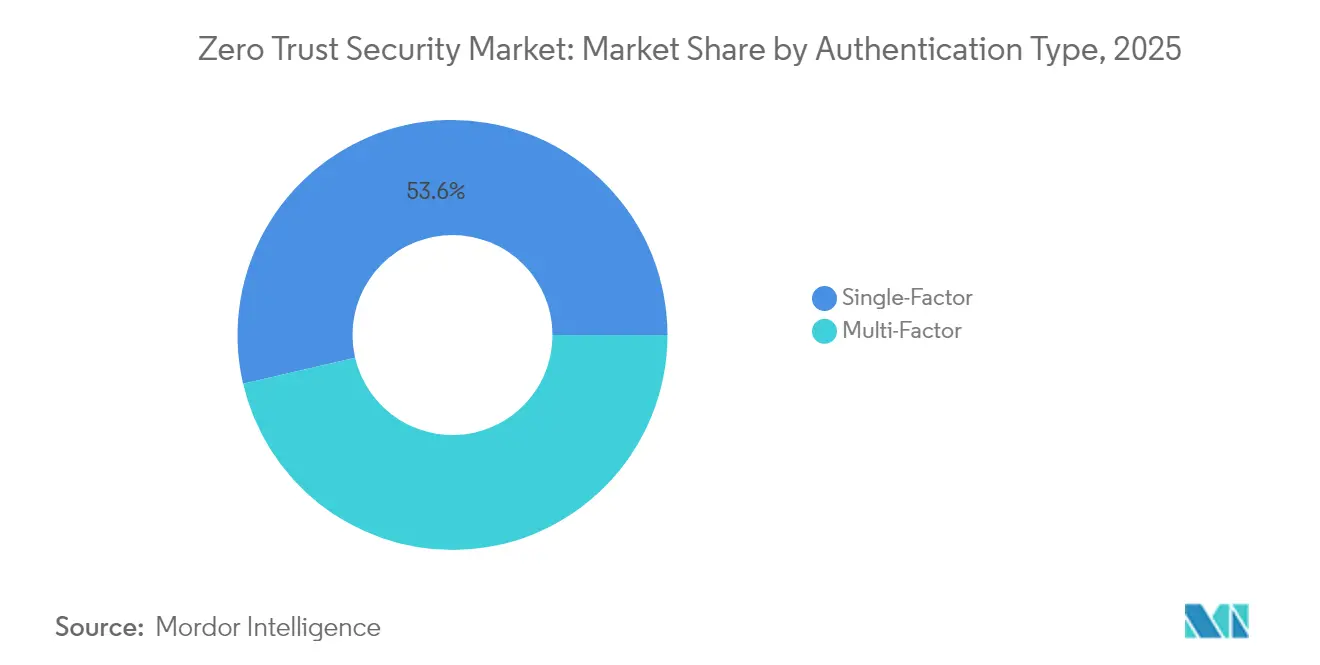

- By authentication type, Single-factor methods retained a 53.64% share in 2025 as multi-factor options increase at a 19.78% CAGR.

- By end-user industry, Banking, financial services, and insurance (BFSI) captured 23.12% share in 2025, whereas Healthcare shows the fastest trajectory at an 18.21% CAGR.

- By geography, North America contributed 34.72% of 2025 revenue, yet Asia-Pacific is projected to climb at a 18.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Zero Trust Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing number of data breaches | +3.2% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Expansion of remote/hybrid workforces | +2.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising regulatory mandates | +2.1% | North America and EU primary, APAC emerging | Long term (≥ 4 years) |

| Explosion of machine & API traffic | +1.9% | Global, concentrated in cloud-native regions | Medium term (2-4 years) |

| Smart-NIC micro-segmentation | +1.4% | North America and APAC core markets | Long term (≥ 4 years) |

| Identity-network convergence | +1.6% | Global, with early adoption in enterprise segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing number of data breaches

Zero-day vulnerabilities tripled in 2024, and ransomware represented one-third of all breaches across 92% of industries. [1]Verizon, “2024 Data Breach Investigations Report,” verizon.com Human factors contributed to 68% of incidents, pressing enterprises to adopt continuous verification that assumes internal compromise. Third-party weaknesses climbed 68%, forcing organizations to extend zero trust principles to suppliers. Insider threats cost financial institutions USD 16.2 million per event on average. Breach economics, therefore, favor preventative spending on zero trust controls over expensive post-incident remediation.

Expansion of remote/hybrid workforces

Permanent remote work invalidates VPN-centric access. Organizations that adopted zero trust architectures saw an 83% cut in incident-response times and an 80% drop in successful breaches. NTT DATA’s rollout connected 50,000 users in 30 days, proving cloud-delivered scalability. Remote Browser Isolation tools further protect distributed staff without hindering productivity, fueling sustained demand for zero-trust network access.

Rising regulatory mandates

The U.S. executive order obliges all federal agencies to transition to zero trust, spurring private-sector copycat programs. PCI DSS updates in finance and HIPAA refinements in healthcare promote continuous verification over perimeter checks. Supply-chain security laws increasingly require vendors to prove zero trust compliance, favoring integrated platforms that simplify audit evidence.

Explosion of machine and API traffic

API calls now outnumber human web requests, exposing unattended endpoints. Platforms embed AI to profile real-time traffic and flag anomalies. Akamai’s 2024 acquisitions of Neosec and Noname Security underscored growing demand for API-centric defenses. [2]Akamai Technologies, “Annual Report 2024,” akamai.com Manufacturers use zero-trust micro-segmentation to shield industrial IoT devices, maintaining uptime while limiting lateral movement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy integration hurdles | -2.1% | Global, more pronounced in established enterprises | Medium term (2-4 years) |

| High up-front architecture cost | -1.8% | SME segments globally, emerging markets | Short term (≤ 2 years) |

| Shadow-IT SaaS bypass | -1.2% | North America & Europe primarily | Short term (≤ 2 years) |

| Supplier data-sharing clauses | -0.9% | Global, regulatory compliance regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy integration hurdles

Decades-old applications often lack modern authentication hooks, forcing custom connectors that extend deployment schedules. Healthcare facilities struggle to retrofit network-enabled medical devices built without security in mind. [3]Gigamon, “Guide to Zero Trust for Healthcare Organizations,” gigamon.com Manufacturers face similar constraints with operational technology, where uptime trumps security. Vendors that package pre-configured integrations ease friction and shorten project payback.

High up-front architecture cost

Comprehensive zero-trust programs require identity orchestration, network segmentation, and automated policy engines. Capital intensity can deter SMEs, even though a single breach routinely eclipses initial spending. Subscription-based cloud services mitigate capital hurdles, enabling pay-as-you-go adoption. Still, organizations must weigh deployment scope against resource limits, reinforcing the value of managed service offerings that bundle technology and expertise.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Surge Despite Solutions Dominance

Solutions accounted for 66.55% of 2025 revenue, anchoring the zero trust security market through integrated policy engines and analytics dashboards. However, services are rising at a 19.05% CAGR as enterprises rely on partners to design, deploy, and fine-tune architectures across hybrid landscapes.

Professional services guide strategy, while managed offerings deliver continuous optimization without ballooning headcount. High-profile rollouts—such as Cimpress transforming global access controls—underline the organizational change management needed alongside technology shifts, explaining why the zero trust security market continues to pivot toward service-led value delivery.

By Deployment Mode: Cloud Acceleration Challenges On-Premise Dominance

On-premise solutions preserved 53.85% of 2025 spending, reflecting regulated workloads that remain inside corporate data centers. Cloud deployments, growing at 19.66% CAGR, attract firms seeking instant scalability and simplified updates.

Hybrid patterns dominate: sensitive data stays on-site while SaaS gateways manage identity and policy logic. As compliance frameworks evolve to recognize cloud residency controls, the zero trust security market size attached to cloud models is expected to expand rapidly, narrowing the on-premise lead over the forecast period.

By Organisation Size: SME Adoption Accelerates Despite Enterprise Dominance

Large enterprises captured 59.62% of outlays in 2025, leveraging budgets to build bespoke zero-trust blueprints. SMEs, advancing at an 18.02% CAGR, increasingly consume right-sized SaaS bundles that collapse identity, network, and endpoint security into a single pane.

Cost-distributed subscriptions flatten entry barriers, letting smaller firms enjoy enterprise-grade protection. Vendors that automate policy creation and furnish 24×7 SOC oversight resonate strongly with resource-constrained buyers, reinforcing growth momentum within this segment of the zero trust security market.

By Authentication Type: Multi-Factor Growth Challenges Single-Factor Persistence

Single-factor approaches still hold a 53.64% share, a legacy of password-centric systems and user-experience fears. Multi-factor usage, expanding at 19.78% CAGR, gains traction as breach costs climb and regulators advocate layered checks.

Modern zero trust platforms weave biometrics, device fingerprinting, and behavior analytics to maintain frictionless experiences. This convergence is shrinking the password stronghold, indicating that the zero trust security market share of single-factor methods will erode steadily through 2031.

By End-user Industry: Healthcare Acceleration Challenges BFSI Leadership

BFSI owned 23.12% of 2025 revenue thanks to early adoption and strict oversight. Healthcare is pacing an 18.21% CAGR as ransomware targets patient data and life-critical systems.

Manufacturing, energy, and government follow, driven by operational technology exposure. Retail and e-commerce deploy zero trust to secure expanding digital storefronts. Cross-industry momentum confirms that zero trust has progressed from niche pilot to mainstream risk-management standard across the zero trust security industry.

Geography Analysis

North America secured 34.72% of 2025 revenue through mature regulations, extensive cloud adoption, and vendor density. Federal mandates push agencies and contractors toward consistent architectures, while financial hubs in New York and Toronto showcase reference deployments that ripple across other verticals. Competitive pressure, however, is intensifying as newer cloud-native entrants challenge incumbents on price and automation.

Asia-Pacific commands the fastest CAGR at 18.63% to 2031. Governments from Singapore to Japan enact cybersecurity roadmaps that embed zero trust principles, letting firms leapfrog legacy firewalls in favor of cloud-delivered controls. Manufacturing clusters rely on micro-segmentation to protect converged IT/OT environments, further expanding the zero-trust security market in the region.

Europe’s steady progression stems from GDPR and sector-specific directives that favor privacy-preserving architectures. Vendors that provide granular audit trails and EU-based data centers gain traction. Meanwhile, the Middle East and Africa register emerging potential as digital governments fund modernization, though adoption still lags due to limited local skill sets and infrastructure.

Competitive Landscape

The zero trust security market hosts a blend of platform giants and agile specialists. Palo Alto Networks, Cisco, and Fortinet layer identity, network, and endpoint controls into consolidated suites. Zscaler processes more than half a trillion daily transactions through its cloud-native Zero Trust Exchange, reinforcing scale advantages.

Strategic moves illustrate consolidation: Arista integrated zero-trust features into CloudVision for automated network segmentation. Akamai absorbed Neosec and Noname Security to fortify API protection. Veeam and Microsoft co-developed AI-powered resilience aligned with zero-trust tenets.

Innovation centers on AI-driven behavior scoring; Cloudflare’s recent patent for multi-domain application mapping exemplifies the focus on automated policy decisions. Emerging players such as Zero Networks advance automated micro-segmentation that installs in minutes, winning mindshare among resource-strained teams. [4]Zero Networks, “Zero Networks Achieves Five-Fold Revenue Growth,” zeronetworks.com The competitive narrative, therefore, pivots on speed, automation, and breadth of ecosystem integrations rather than on standalone feature depth.

Zero Trust Security Industry Leaders

Palo Alto Networks Inc.

Cisco Systems Inc.

Zscaler Inc.

Okta Inc.

Fortinet Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Veeam and Microsoft expanded their collaboration to launch AI-enabled data-resilience services grounded in zero-trust principles.

- January 2025: IBM announced USD 5 billion in generative AI revenue, with consulting engagements frequently tied to zero trust deployments.

- November 2024: Arista Networks posted USD 1.811 billion Q3 2024 revenue and highlighted zero trust additions to CloudVision.

- September 2024: Zscaler and CrowdStrike integrated AI threat detection across their platforms for coordinated zero-trust response.

- September 2024: ExtraHop won CrowdStrike Ecosystem Innovator of the Year for capabilities that enhance zero-trust analytics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the zero-trust security market as all licensed software, hardware, and managed modules that continuously verify user, device, and workload identity before granting access across enterprise, cloud, and edge assets. Revenues cover ZTNA gateways, micro-segmentation platforms, identity and policy engines, context-aware MFA, and supporting analytics consumed by commercial, public-sector, and industrial buyers worldwide.

Scope exclusion: spending tied to broad managed security service contracts that only mention zero trust as an add-on is left outside the base.

Segmentation Overview

- By Offering

- Solutions

- Services

- By Deployment Mode

- On-premise

- Cloud

- By Organisation Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Authentication Type

- Single-Factor

- Multi-Factor

- By End-user Industry

- IT and Telecom

- BFSI

- Manufacturing

- Healthcare

- Energy and Utilities

- Retail and E-commerce

- Government and Defense

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Singapore

- Malaysia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Conversations with CISOs, zero-trust architects, identity platform specialists, and value-added resellers across North America, Europe, and key Asia-Pacific hubs help us validate penetration rates, average selling prices, and deployment hurdles that rarely surface in documents. Follow-up surveys with small-enterprise IT heads enrich the view on budget share shifts.

Desk Research

Our analysts start with publicly available cornerstone sources such as NIST-800 series guidance, U.S. Executive Order 14028 budget updates, ENISA threat bulletins, OECD ICT spending tables, and global breach reports from Verizon DBIR; these frame the adoption curve and sizing boundaries. Company 10-Ks, Form 20-Fs, vendor investor decks, procurement portals, and patent searches on Questel supplement segment splits, while shipment and price traces are collected through Dow Jones Factiva and D&B Hoovers. The sources cited here illustrate, not exhaust, the wider literature reviewed.

Market-Sizing & Forecasting

A top-down model converts annual cybersecurity spend by industry into a zero-trust-addressable pool using tracked penetration ratios, then cross-checks totals with a bottom-up sample of vendor revenue roll-ups and channel checks. Key variables include: 1) security spend as a share of total IT outlay, 2) share of remote workers, 3) MFA user coverage, 4) cloud workload proportion, and 5) disclosed average breach cost. Multivariate regression combined with exponential smoothing projects each driver through 2030, while gaps in vendor disclosures are bridged via sampled ASP times deployment volume benchmarks agreed during interviews.

Data Validation & Update Cycle

Outputs pass anomaly scans, variance thresholds, and a senior analyst review before sign-off. Models refresh annually, with rapid revisions triggered by material events such as major regulatory mandates or a landmark supply-side merger; clients therefore receive a freshly verified baseline at purchase.

Why our Zero Trust Security Baseline earns trust

Published estimates vary because firms select different component baskets, currency years, and refresh cadences.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 41.72 B (2025) | Mordor Intelligence | - |

| USD 36.50 B (2024) | Global Consultancy A | Excludes identity engines and uses 2023 exchange rates |

| USD 42.91 B (2025) | Industry Data Firm B | Relies on vendor press releases without primary cross-checks |

| USD 42.28 B (2025) | Regional Consultancy C | Counts bundled MSSP revenue, inflating totals |

The comparison shows that when scope, currency alignment, and direct expert validation are applied together, Mordor's figure provides a balanced, reproducible starting point for technology planners and investors.

Key Questions Answered in the Report

What is the current value of the zero trust security market?

The zero trust security market size is valued at USD 48.43 billion in 2026.

How fast is the zero trust security market expected to grow?

It is forecast to expand at a 16.07% CAGR, reaching USD 102.01 billion by 2031.

Which segment of the market is growing the quickest?

Cloud deployments are advancing at a 19.66% CAGR as organizations migrate security control planes to SaaS models.

Why are services gaining traction within zero trust programs?

Complex strategy, integration, and continuous optimization requirements push enterprises to rely on professional and managed services, which are growing at a 19.05% CAGR.

Which region shows the highest growth rate?

Asia-Pacific exhibits the fastest expected CAGR at 18.63%, driven by digital-transformation initiatives and supportive regulatory actions.

What primary factor drives zero trust adoption?

Rising data-breach volumes and associated costs compel firms to replace perimeter defenses with continuous verification frameworks.

Page last updated on: