| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 7.98 Billion |

| Market Size (2030) | USD 11.83 Billion |

| CAGR (2025 - 2030) | 8.21 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players Systems Market Major Players")

*Disclaimer: Major Players sorted in no particular order |

Systems Market Size")

Zero Liquid Discharge (ZLD) Systems Market Analysis

The Zero Liquid Discharge Systems Market size is estimated at USD 7.98 billion in 2025, and is expected to reach USD 11.83 billion by 2030, at a CAGR of 8.21% during the forecast period (2025-2030).

The zero liquid discharge (ZLD) systems market is experiencing significant transformation driven by rapid industrialization and evolving environmental consciousness across major industries. The chemical sector, one of the largest end-users of ZLD systems, has demonstrated remarkable growth, with Germany's chemical industry revenue projected to reach EUR 220 billion by 2022, representing a 15.5% increase from 2020 levels. This growth in industrial activities has led to increased water consumption and a subsequent need for advanced industrial water treatment solutions, particularly in regions facing water scarcity challenges.

The market is witnessing substantial technological advancement in both thermal and membrane filtration systems, with a notable shift toward more energy-efficient systems. The integration of advanced technologies like High-Efficiency Reverse Osmosis (HERO) and mechanical vapor recompression has significantly improved recovery rates, with modern systems achieving water recovery rates exceeding 95% in most applications. This technological evolution has been particularly evident in the power generation sector, where the implementation of wastewater treatment systems has become crucial for managing wastewater from cooling towers and flue-gas desulfurization processes.

The industry landscape is characterized by increasing consolidation and strategic partnerships among key players to enhance technological capabilities and market reach. For instance, in 2023, IDE Technologies and Chem Process Systems Private Limited formed a strategic partnership to provide end-to-end zero liquid discharge systems solutions, combining IDE's desalination expertise with Chem Process's crystallization technologies. This trend toward consolidation has been accompanied by significant investments in research and development, focusing on reducing operational costs and improving system efficiency.

The market is also being shaped by the rapid expansion of water-intensive industries, particularly in emerging economies. The steel industry, a major consumer of industrial water conservation solutions, has shown remarkable growth, with global crude steel production reaching significant levels in recent years. Additionally, the petrochemical sector has witnessed substantial investments, with Abu Dhabi National Oil Company signing an agreement in March 2022 to establish the UAE's first methanol production facility with an annual capacity of 1.8 million tons, incorporating advanced water treatment systems including water recovery systems.

Zero Liquid Discharge (ZLD) Systems Market Trends

INCREASING DEMAND FOR FRESHWATER

The growing scarcity of freshwater resources has become a critical global concern, with less than 0.01% of the Earth's freshwater found in lakes, swamps, and rivers. The overuse of water, particularly in industrial applications, has been threatening these limited resources, as two-thirds of the Earth's surface comprises water but less than 3% is fresh. Industrial effluents discharged into water bodies are increasingly polluting freshwater sources and creating severe shortages, especially affecting food production, power generation, manufacturing, and sanitation needs. According to the United Nations Environment Program (UNEP), approximately 1.8 billion people are projected to live in regions with absolute water scarcity by 2025, with two-thirds of the global population expected to face water-stressed conditions.

The demand for freshwater has been rapidly intensifying due to mechanization and food safety requirements, creating an ecological imbalance as wastewater from industrial processes and sewage is discarded into freshwater resources. It is estimated that there will be about 1 billion more mouths to feed worldwide by 2025, requiring an additional 1 trillion cubic meters of water per year for agriculture alone—equivalent to the annual flow of 20 Niles or 100 Colorado Rivers. This massive increase in water demand, coupled with the deteriorating quality of existing water sources, has made water conservation and treatment technologies like management of industrial wastewater and Zero Liquid Discharge (ZLD) systems increasingly crucial for industrial operations and environmental sustainability.

Understand The Key Trends Shaping This Market

Download PDF

MORE STRINGENT REGULATIONS FOR WASTEWATER DISPOSAL

Environmental regulations governing wastewater disposal have become progressively stringent across the globe, particularly in developed and developing nations concerned with environmental sustainability. In the United States, the Environmental Protection Agency's current effluent guidelines set the first federal limits on the levels of heavy metals in wastewater discharged from power plants, calling for zero discharge of pollutants from fly ash and bottom ash waste streams. Similarly, the European Union has implemented increasingly strict environmental policies governing air, soil, and water quality, affecting various industries' operations and driving the adoption of advanced systems for effluent treatment.

The regulatory landscape has witnessed significant evolution in emerging economies as well, with countries implementing comprehensive frameworks for management of industrial wastewater. For instance, the provincial Government of Shanxi in China has mandated the installation of ZLD systems for all industrial wastewater from power, coking, and coal washing operations. In India, the Central Pollution Control Board has released guidelines on the techno-economic feasibility of implementing zero-liquid discharge for water-polluting industries, making ZLD systems mandatory for textile plants generating more than 25 metric cubic meters of wastewater per day. These regulations, coupled with growing environmental awareness and corporate responsibility initiatives, have created a strong impetus for industries to adopt ZLD systems as a sustainable solution for wastewater management. Furthermore, the integration of purification of industrial water and management of liquid waste technologies is becoming essential to meet these stringent regulations and ensure compliance.

Segment Analysis: TECHNOLOGY

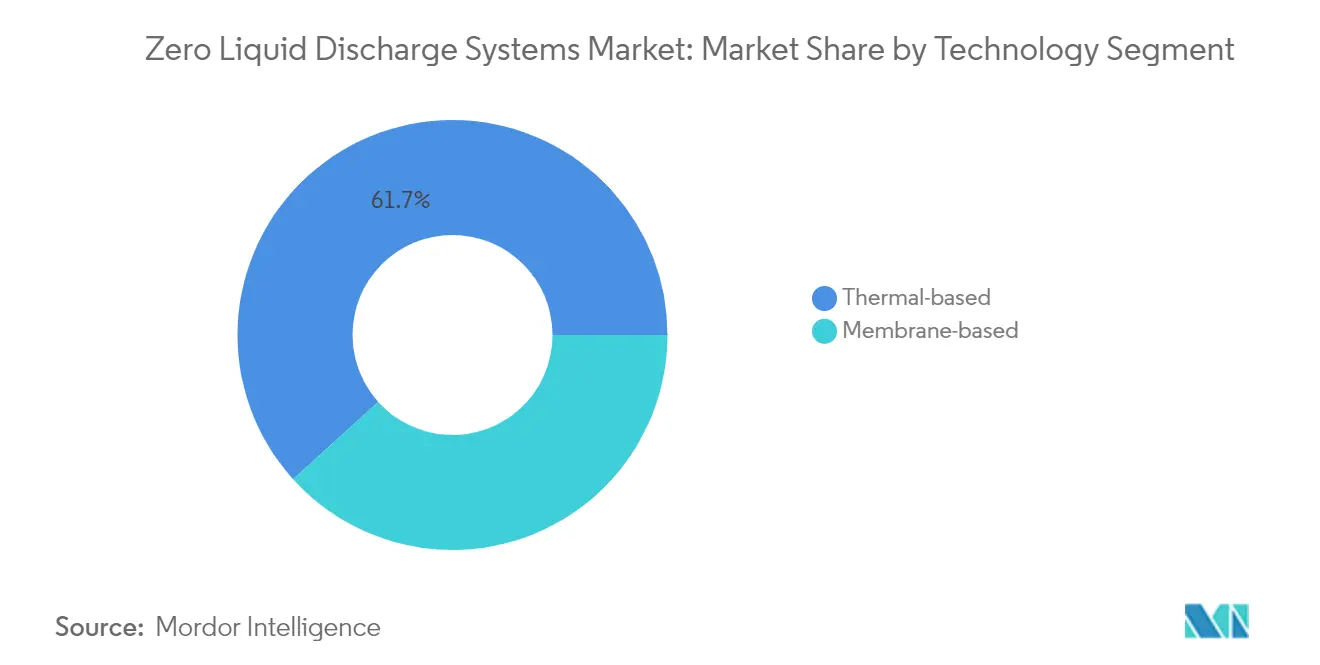

Thermal-based Segment in Zero Liquid Discharge Systems Market

The thermal-based technology segment continues to dominate the zero liquid discharge (ZLD) systems market, holding approximately 62% of the total market share in 2024. This significant market position is attributed to thermal-based systems being the oldest and most widely adopted ZLD technology across various industries worldwide. The segment's dominance is particularly evident in the coal chemical industry, where these systems are extensively used for wastewater treatment due to their proven reliability and effectiveness. Thermal-based ZLD systems incorporate critical components like heat exchangers and utilize processes such as evaporation systems, concentration, product cooling, and crystallization systems. Brine concentration plays a vital role in these systems, primarily employed in mechanical vapor compression methods for evaporation, making them particularly effective for handling complex industrial wastewater streams.

Membrane-based Segment in Zero Liquid Discharge Systems Market

The membrane-based technology segment is emerging as the most dynamic sector in the ZLD systems market, projected to grow at approximately 9% during 2024-2029. This growth trajectory is driven by several technological advantages, including relatively lower capital costs compared to traditional thermal-based systems and more efficient sizing of evaporation systems. The segment's expansion is further supported by key processes such as Electrodialysis (ED), Forward Osmosis (FO), and Membrane Distillation (MD), which offer enhanced performance in treating various types of wastewater. The technology's lower fouling tendency in Forward Osmosis compared to Reverse Osmosis, coupled with Electrodialysis's superior desalination capabilities, is driving increased adoption across industries. Despite higher energy consumption compared to thermal processes, the technology's superior cleaning efficiency and operational benefits are making it increasingly attractive to end-users.

Segment Analysis: END-USER INDUSTRY

Power Segment in Zero Liquid Discharge Systems Market

The power generation industry dominates the zero liquid discharge systems market, holding approximately 37% of the total market share in 2024. This significant market position is driven by stringent environmental regulations requiring power plants to implement advanced wastewater treatment solutions. The sector's dominance is particularly evident in thermal and nuclear power plants, where water management is given high priority by plant owners. The implementation of ZLD systems has become crucial for power plants as it eliminates wastewater discharge and allows processed water to be reclaimed and reused. This is especially relevant for coal-fired power plants, which have greater water demands and face more challenging water discharge requirements due to the presence of heavy metals from flue-gas desulfurization (FGD). The power sector's leadership in ZLD adoption is further strengthened by the growing focus on environmental sustainability and the need to comply with increasingly strict discharge permits.

Chemicals and Petrochemicals Segment in Zero Liquid Discharge Systems Market

The chemicals and petrochemicals segment represents a rapidly evolving sector in the zero liquid discharge systems market. This segment's growth is driven by the increasing need for water conservation in chemical manufacturing processes and stricter environmental regulations worldwide. Chemical plants are implementing ZLD systems to handle the high volumes of wastewater generated during manufacturing processes, which often contain various conventional parameters and chemical constituents harmful to the environment. The industry's commitment to sustainable practices and the rising focus on water reuse in chemical processing operations are key factors propelling the adoption of ZLD systems. Additionally, the expansion of chemical manufacturing facilities globally, particularly in emerging economies, is creating new opportunities for ZLD system implementations.

Remaining Segments in End-User Industry

The other significant segments in the ZLD systems market include metallurgy and mining, pharmaceutical, and oil and gas industries. The metallurgy and mining sector utilizes ZLD systems for treating water with high chlorides and sulfates, while the pharmaceutical industry implements these systems to handle wastewater containing various chemicals and laboratory effluents. The oil and gas sector employs ZLD systems primarily in upstream operations for treating produced water and frac water. Each of these segments contributes uniquely to the market's growth, driven by their specific water treatment requirements and environmental compliance needs. The diverse applications across these industries demonstrate the versatility and growing importance of ZLD systems in industrial water recycling systems.

Zero Liquid Discharge (ZLD) Systems Market Geography Segment Analysis

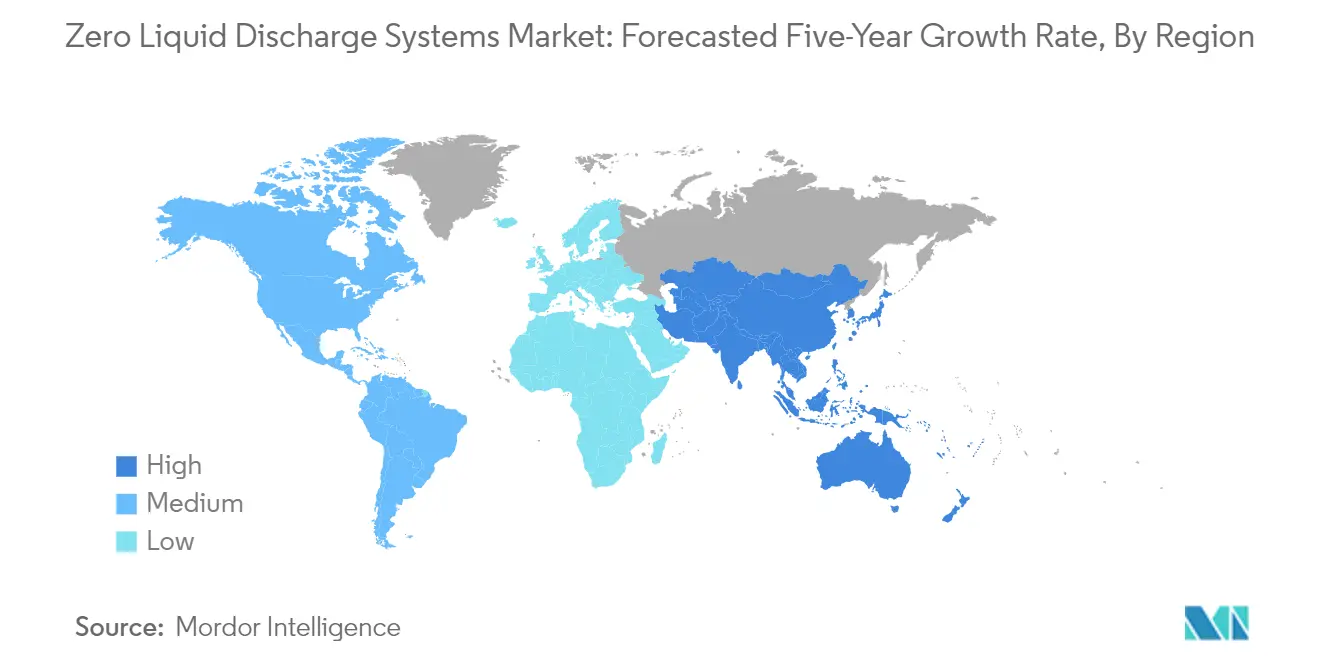

Zero Liquid Discharge Systems Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for zero liquid discharge systems, driven by rapid industrialization and stringent environmental regulations. Countries like China, India, Japan, South Korea, and the ASEAN nations are making significant investments in ZLD technologies across various industries, including power generation, chemicals, and petrochemicals. The region's focus on sustainable water management practices and the need to address water scarcity issues have led to increased adoption of ZLD systems. Industrial growth coupled with environmental concerns has created a strong demand for these systems, particularly in sectors like thermal power plants, steel manufacturing, and chemical processing.

Zero Liquid Discharge Systems Market in China

China dominates the Asia-Pacific ZLD systems market, holding approximately 41% of the regional market share. The country's robust industrial sector, particularly in chemical manufacturing and power generation, drives significant demand for ZLD systems. China's commitment to environmental protection through stringent wastewater discharge regulations has accelerated the adoption of these systems. The country's extensive network of thermal power plants and growing chemical industry continues to create substantial opportunities for ZLD system deployments. The government's focus on sustainable industrial development and water conservation has further strengthened the market position of ZLD systems in China.

Zero Liquid Discharge Systems Market Growth in China

China is also leading the growth trajectory in the Asia-Pacific region with a projected growth rate of approximately 11% during 2024-2029. The country's aggressive environmental protection policies and continued industrial expansion are key drivers of this growth. Investments in new power generation facilities and chemical manufacturing plants are creating sustained demand for ZLD systems. The implementation of stricter environmental regulations and the government's push towards sustainable industrial practices continue to drive the adoption of ZLD technologies across various sectors.

Zero Liquid Discharge Systems Market in North America

North America represents a mature market for zero liquid discharge systems, characterized by advanced technological adoption and strict environmental regulations. The United States, Canada, and Mexico comprise the key markets in this region, with significant deployment across power generation, oil and gas, and chemical processing industries. The region's focus on sustainable industrial practices and water conservation has driven the adoption of ZLD systems. The presence of major industry players and continuous technological innovations has further strengthened the market landscape.

Zero Liquid Discharge Systems Market in United States

The United States leads the North American market, commanding approximately 82% of the regional market share. The country's extensive industrial base, particularly in power generation and chemical processing, drives substantial demand for ZLD systems. Stringent environmental regulations and the need for sustainable water management solutions have made ZLD systems integral to industrial operations. The presence of major technology providers and continuous investments in research and development have established the United States as a key market for advanced ZLD solutions.

Zero Liquid Discharge Systems Market Growth in Mexico

Mexico is emerging as the fastest-growing market in North America with an expected growth rate of approximately 7% during 2024-2029. The country's expanding industrial sector, particularly in manufacturing and chemical processing, is driving increased adoption of ZLD systems. Government initiatives promoting sustainable industrial practices and water conservation are creating new opportunities for ZLD system deployments. The growing focus on environmental compliance and water management in industrial operations continues to boost market growth.

Zero Liquid Discharge Systems Market in Europe

Europe maintains a strong position in the global ZLD systems market, supported by stringent environmental regulations and advanced industrial infrastructure. The region encompasses key markets including Germany, the United Kingdom, France, and Italy, each contributing significantly to market growth. The European Union's strict environmental policies and emphasis on sustainable industrial practices have created a robust demand for ZLD systems. The region's focus on reducing industrial water pollution and promoting water reuse has accelerated the adoption of these systems across various industries.

Zero Liquid Discharge Systems Market in Germany

Germany stands as the largest market for ZLD systems in Europe, with its advanced industrial infrastructure and strong focus on environmental protection. The country's leadership in chemical manufacturing and power generation sectors has created substantial demand for ZLD solutions. German industries' commitment to sustainable practices and water conservation has driven widespread adoption of these systems. The presence of major technology providers and continuous innovation in water treatment technologies has further strengthened Germany's position in the market.

Zero Liquid Discharge Systems Market Growth in Germany

Germany also leads the growth trajectory in Europe's ZLD systems market, demonstrating the region's strongest expansion potential. The country's ongoing industrial modernization and increasing focus on environmental sustainability continue to drive market growth. Investments in advanced manufacturing facilities and stricter environmental regulations are creating new opportunities for ZLD system deployments. The government's support for sustainable industrial practices and water conservation initiatives further accelerates market development.

Zero Liquid Discharge Systems Market in South America

The South American market for zero liquid discharge systems is experiencing steady growth, primarily driven by developments in Brazil and Argentina. The region's expanding industrial sector, particularly in mining, oil and gas, and chemical processing, has increased the demand for ZLD systems. Brazil emerges as both the largest and fastest-growing market in the region, supported by its robust industrial base and increasing environmental regulations. The region's focus on sustainable water management and growing environmental awareness continues to drive the adoption of ZLD technologies across various industrial sectors.

Zero Liquid Discharge Systems Market in Middle East & Africa

The Middle East & Africa region presents significant opportunities for zero liquid discharge systems, driven by water scarcity concerns and growing industrial activities. Countries like Saudi Arabia and South Africa are key markets in this region, with applications primarily in power generation, oil and gas, and chemical processing industries. South Africa leads the market size in the region, while Saudi Arabia shows the fastest growth potential. The region's focus on water conservation and sustainable industrial practices, particularly in the oil and gas sector, continues to drive the adoption of ZLD systems.

Get Analysis on Important Geographic Markets

Download PDF

Zero Liquid Discharge (ZLD) Systems Industry Overview

Top Companies in Zero Liquid Discharge (ZLD) Systems Market

The zero liquid discharge systems market is characterized by continuous product innovation focused on improving energy efficiency and reducing operational costs. Leading companies are investing heavily in research and development to enhance system performance and develop more sustainable solutions. Strategic partnerships and collaborations, particularly with regional players, have become increasingly common to expand geographical reach and technological capabilities. Companies are also focusing on vertical integration across the value chain to strengthen their market position and control costs. The emphasis on operational agility is evident through the development of customized solutions and rapid responses to changing regulatory requirements. Market leaders are expanding their service offerings to include comprehensive maintenance and operational support, creating additional revenue streams while building stronger customer relationships.

Consolidated Market Led By Global Players

The ZLD systems market exhibits a consolidated structure dominated by established global players like Veolia, SUEZ, and GEA Group Aktiengesellschaft, who possess extensive technological expertise and worldwide presence. These companies leverage their broad product portfolios, established distribution networks, and strong financial capabilities to maintain their market positions. The market is characterized by high entry barriers due to significant capital requirements, technological complexity, and the need for established customer relationships, particularly in industries like power generation, oil and gas, and chemicals.

Recent years have witnessed significant merger and acquisition activity, with major players acquiring smaller specialized companies to enhance their technological capabilities and expand their regional presence. The acquisition of SUEZ by Veolia, though later divested to a consortium of investors, exemplifies the dynamic nature of market consolidation. Regional players are increasingly forming strategic partnerships with global leaders to access advanced technologies and expand their market reach, while global players benefit from local market knowledge and established customer relationships.

Innovation and Service Excellence Drive Success

Success in the ZLD systems market increasingly depends on companies' ability to offer innovative, energy-efficient solutions while maintaining competitive pricing. Incumbent players must focus on developing next-generation technologies that reduce operational costs and environmental impact while expanding their service capabilities to provide comprehensive industrial water treatment solutions. The ability to offer flexible financing options and demonstrate a clear return on investment has become crucial, particularly when dealing with price-sensitive markets and industries facing stringent environmental regulations.

Market contenders can gain ground by focusing on specific industry verticals or regional markets where they can build specialized expertise and strong customer relationships. The development of modular and scalable solutions that can be customized to specific industry requirements presents opportunities for newer players to establish themselves. Companies must also consider potential regulatory changes, particularly regarding water discharge standards and environmental protection, which could significantly impact market dynamics. Building strong relationships with end-users through excellent service delivery and technical support remains crucial for long-term success in this market.

Zero Liquid Discharge (ZLD) Systems Market Leaders

-

Veolia Water Technologies Inc.

-

Aquatech International LLC

-

SUEZ

-

Evoqua Water Technologies LLC

-

GEA Group Aktiengesellschaft

- *Disclaimer: Major Players sorted in no particular order

_Systems_Market.webp)

Need More Details on Market Players and Competiters?

Download PDF

Zero Liquid Discharge (ZLD) Systems Market News

- In February 2022, Veolia announced the completion of the sale of the New Suez to the consortium of investors composed of Meridiam, GIP, CDC Group, and CNP assurances for an unchanged enterprise value.

- In December 2021, the European Commission approved the acquisition of Suez by Veolia. This was a decisive step in the creation of a global champion of ecological transformation.

Zero Liquid Discharge (ZLD) Systems Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Increasing Demand for Freshwater

- 4.1.2 More Stringent Regulations for Wastewater Disposal

-

4.2 Restraints

- 4.2.1 High Capital and Energy Cost of Technology

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 Technology

- 5.1.1 Thermal-based

- 5.1.2 Membrane-based

-

5.2 End-user Industry

- 5.2.1 Power

- 5.2.2 Oil and Gas

- 5.2.3 Metallurgy and Mining

- 5.2.4 Chemicals and Petrochemicals

- 5.2.5 Pharmaceutical

- 5.2.6 Other End-user Industries

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 ALFA LAVAL

- 6.4.2 AQUARION AG

- 6.4.3 Aquatech International LLC

- 6.4.4 Evoqua Water Technologies LLC

- 6.4.5 GEA Group Aktiengesellschaft

- 6.4.6 H2O GmbH

- 6.4.7 IDE Water Technologies.

- 6.4.8 Mitsubishi Power Ltd

- 6.4.9 Praj Industries

- 6.4.10 SafBon Water Technology.

- 6.4.11 Saltworks Technologies Inc.

- 6.4.12 SUEZ

- 6.4.13 Thermax Limited

- 6.4.14 Toshiba

- 6.4.15 Veolia Water Technologies Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 More Investments in the Deployment of ZLD Systems

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Zero Liquid Discharge (ZLD) Systems Industry Segmentation

Zero Liquid Discharge (ZLD) is a water treatment process in which all wastewater is purified and recycled. Thus, leaving zero discharge at the end of the treatment cycle. ZLD treatment is majorly done through thermal or membrane processes. These processes require the utilization of decanters, separators, concentrators, evaporators, and crystallizers, among others. The zero liquid discharge (ZLD) systems market is segmented by technology, end-user industry, and geography. By technology, the market is segmented into thermal-based and membrane-based. By end-user industry, the market is segmented into power, oil and gas, metallurgy and mining, chemicals and petrochemicals, pharmaceutical, and other end-user industries. The report also covers the market size and forecasts for the zero-liquid discharge (ZLD) systems market in 16 countries across the major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

| Technology | Thermal-based | ||

| Membrane-based | |||

| End-user Industry | Power | ||

| Oil and Gas | |||

| Metallurgy and Mining | |||

| Chemicals and Petrochemicals | |||

| Pharmaceutical | |||

| Other End-user Industries | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Zero Liquid Discharge (ZLD) Systems Market Research FAQs

How big is the Zero Liquid Discharge (ZLD) Systems Market?

The Zero Liquid Discharge (ZLD) Systems Market size is expected to reach USD 7.98 billion in 2025 and grow at a CAGR of 8.21% to reach USD 11.83 billion by 2030.

What is the current Zero Liquid Discharge (ZLD) Systems Market size?

In 2025, the Zero Liquid Discharge (ZLD) Systems Market size is expected to reach USD 7.98 billion.

Who are the key players in Zero Liquid Discharge (ZLD) Systems Market?

Veolia Water Technologies Inc., Aquatech International LLC, SUEZ, Evoqua Water Technologies LLC and GEA Group Aktiengesellschaft are the major companies operating in the Zero Liquid Discharge (ZLD) Systems Market.

Which is the fastest growing region in Zero Liquid Discharge (ZLD) Systems Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Zero Liquid Discharge (ZLD) Systems Market?

In 2025, the North America accounts for the largest market share in Zero Liquid Discharge (ZLD) Systems Market.

What years does this Zero Liquid Discharge (ZLD) Systems Market cover, and what was the market size in 2024?

In 2024, the Zero Liquid Discharge (ZLD) Systems Market size was estimated at USD 7.32 billion. The report covers the Zero Liquid Discharge (ZLD) Systems Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Zero Liquid Discharge (ZLD) Systems Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Zero Liquid Discharge (ZLD) Systems Market Research

Mordor Intelligence provides comprehensive insights into the rapidly evolving zero liquid discharge systems industry. We leverage our extensive expertise in industrial wastewater management and industrial water treatment. Our detailed analysis covers the complete spectrum of ZLD systems, including advanced membrane filtration systems and evaporation systems. This analysis offers stakeholders crucial data in an easy-to-access report PDF format. The research encompasses cutting-edge technologies in industrial water purification and liquid waste management. It offers a detailed examination of brine concentration processes and crystallization systems.

Our in-depth report, available for immediate download, equips decision-makers with valuable insights into wastewater treatment systems and effluent treatment systems. It explores innovative approaches to industrial water conservation. The analysis covers emerging trends in water reuse systems and industrial water recycling systems, providing comprehensive coverage of wastewater evaporation technologies. Stakeholders benefit from detailed evaluations of water recovery systems implementation strategies. These evaluations are supported by case studies demonstrating successful industrial water recycling initiatives across various sectors. The report delivers actionable intelligence for organizations seeking to optimize their liquid waste management operations. It also helps enhance their competitive positioning in the industrial water treatment market.