Xerostomia (Dry Mouth Disease) Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

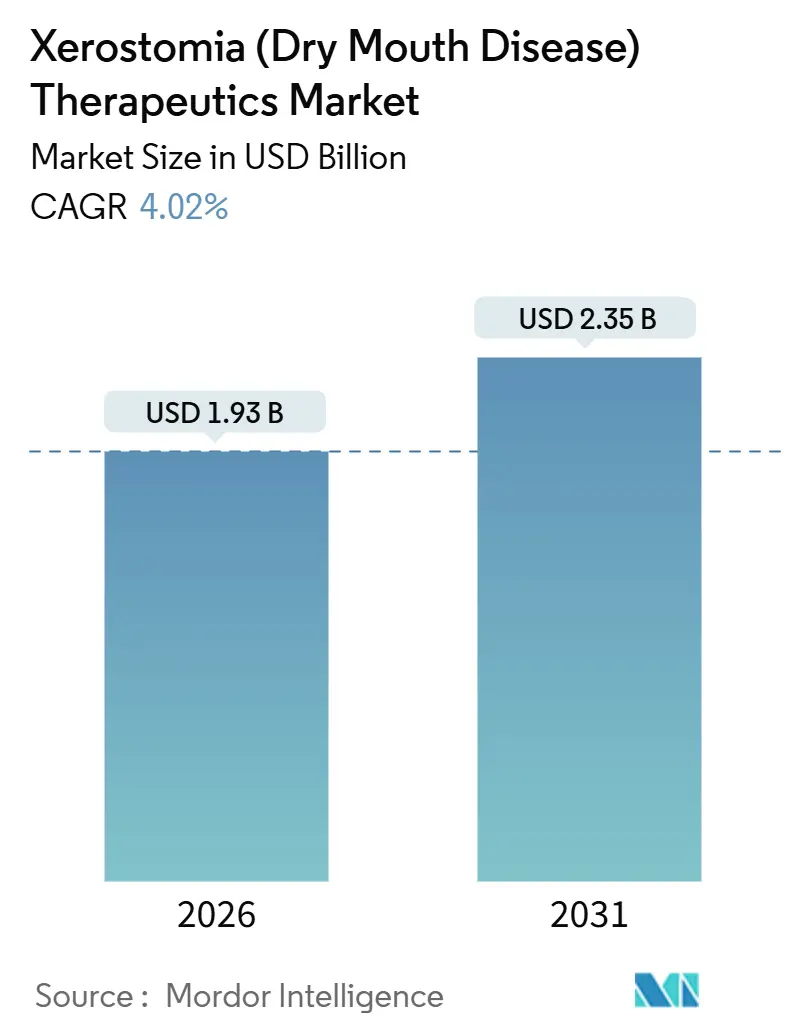

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 2.35 Billion |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

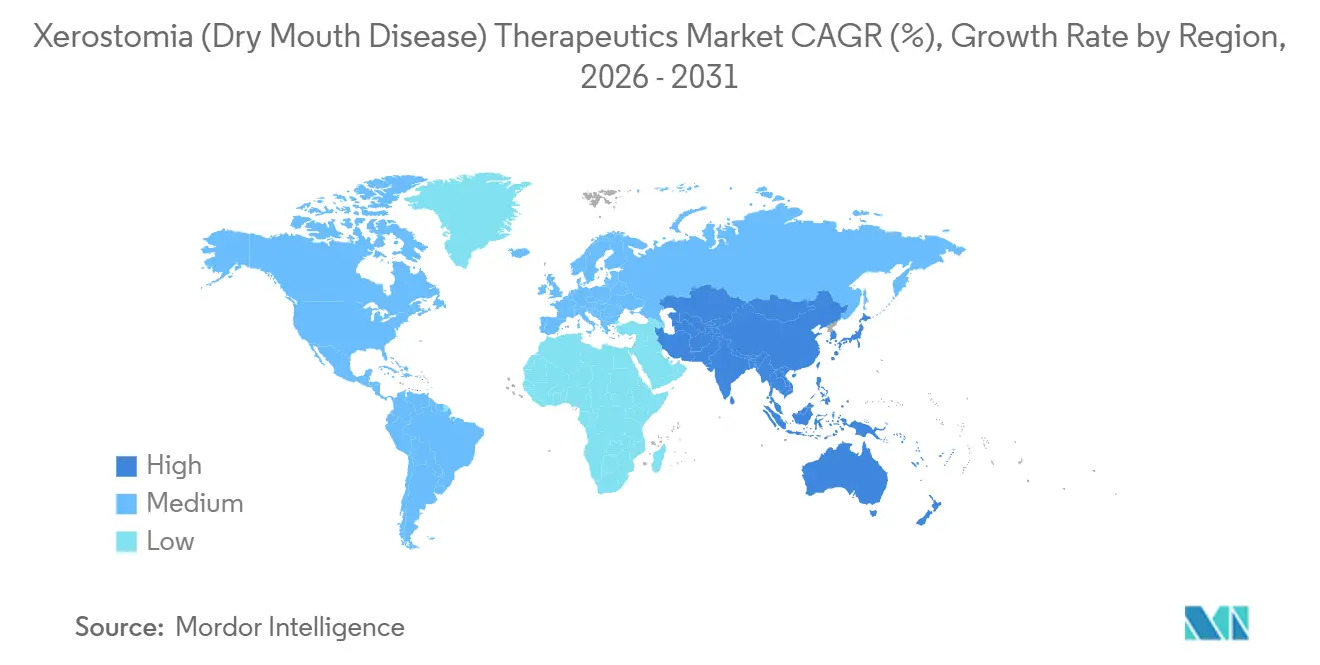

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Xerostomia (Dry Mouth Disease) Therapeutics Market Analysis by Mordor Intelligence

The Xerostomia Therapeutics Market size is estimated at USD 1.93 billion in 2026, and is expected to reach USD 2.35 billion by 2031, at a CAGR of 4.02% during the forecast period (2026-2031).

Three structural forces anchor this measured expansion. The population aged 65 and above, which is most vulnerable to polypharmacy-related dry mouth, continues to rise, swelling the addressable patient pool in every developed region. The 2024-2025 reclassification of several saliva substitutes from prescription to OTC status has shortened patient access paths and widened commercial reach, particularly through e-commerce channels. In parallel, the clinical validation of electrostimulation devices provides physicians with a reimbursable alternative that bypasses the reapplication burden of topical sprays and gels. Collectively, these shifts move the xerostomia therapeutics market from commodity substitutes toward multi-modal, technology-enabled care models.

Key Report Takeaways

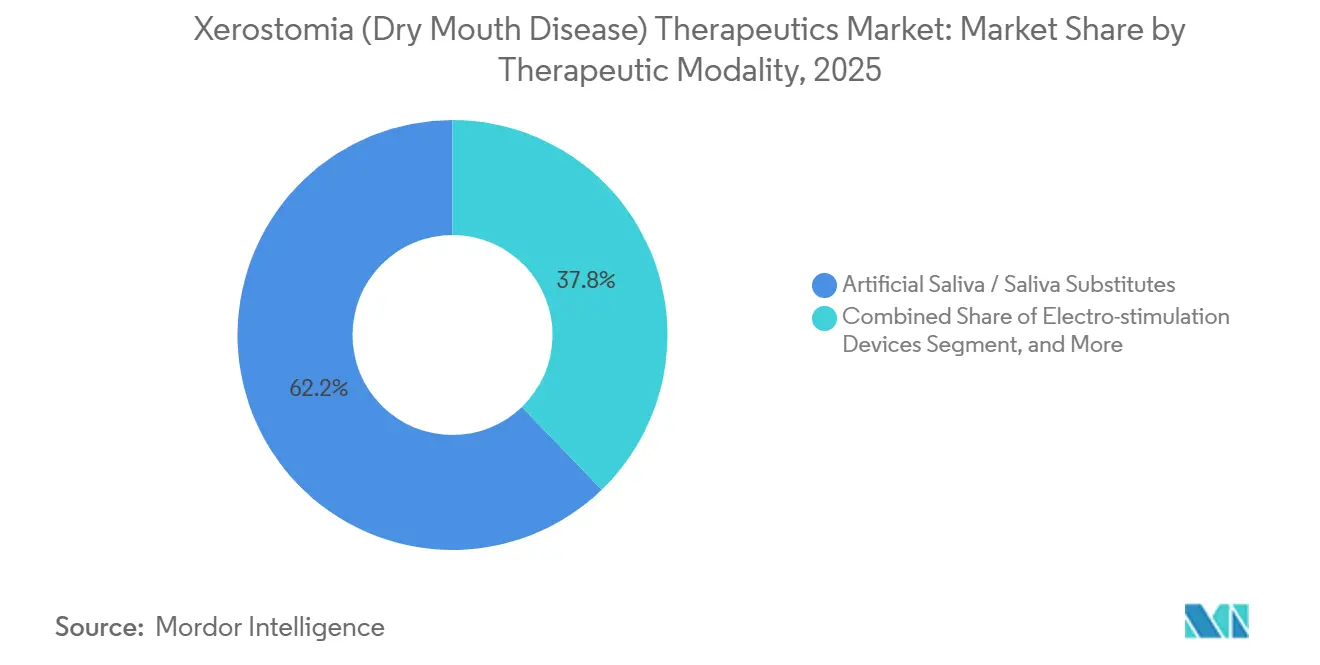

- By therapeutic modality, artificial saliva and saliva substitutes captured 62.21% of the xerostomia therapeutics market share in 2025, while electro-stimulation devices are advancing at a 7.02% CAGR through 2031.

- By product form, sprays accounted for 46.73% of the xerostomia therapeutics market size in 2025, whereas mouthwashes and rinses are projected to grow at a 7.48% CAGR through 2031.

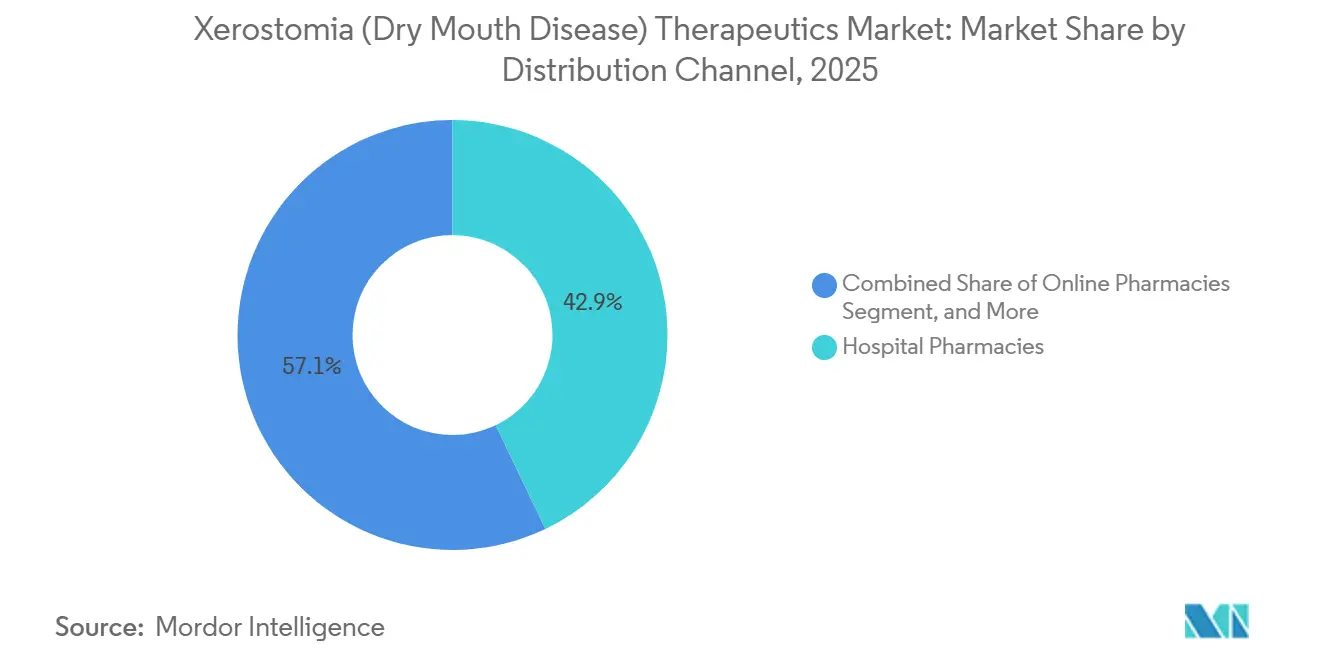

- By end user, hospital pharmacies accounted for 42.88% of the xerostomia therapeutics market size in 2025; however, online pharmacies recorded the fastest channel growth at a 6.13% CAGR for 2026-2031.

- By geography, North America held a 39.16% xerostomia therapeutics market share in 2025, while the Asia-Pacific region is set for the quickest regional growth with an 8.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Xerostomia (Dry Mouth Disease) Therapeutics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Incidence Among Ageing & Polypharmacy Populations | +1.2% | Global focus in North America, Europe, Japan | Long term (≥ 4 years) |

| Expanding OTC Availability & E-Commerce Reach | +0.8% | North America and Europe lead, APAC emerging | Medium term (2-4 years) |

| Development of Innovative Mucoadhesive & Sustained-Release Formulations | +0.7% | Global R&D hubs in United States, Germany, South Korea | Medium term (2-4 years) |

| Emerging Regenerative & Cell-Based Salivary-Gland Therapies | +0.5% | Clinical trials centered in North America, Europe | Long term (≥ 4 years) |

| AI-Driven Personalized Saliva-Substitute Platforms | +0.4% | Early adoption in United States and select EU markets | Medium term (2-4 years) |

| Growing Awareness About Xerostomia-Related Products | +0.4% | Global, fastest in APAC and Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Incidence Among Ageing & Polypharmacy Populations

Polypharmacy prevalence climbed to 68% of seniors in OECD nations by 2025, and anticholinergics, antihypertensives, and antidepressants often combine to triple xerostomia risk.[1]World Health Organization, “Global Health Observatory,” who.int Only 18% of these patients receive preventive saliva substitutes during medication reviews, leaving a treatment gap that payers increasingly notice. Japan reported a 14% increase in hospital admissions for aspiration pneumonia associated with dry mouth in 2024, prompting mandatory oral assessments with anticholinergic therapy to be initiated at a specific point. Medicare spent USD 2.8 billion on xerostomia-related complications in 2025, strengthening reimbursement for substitutes and stimulants. Formulators have responded with low-preservative, once-daily gels tailored to cognitively impaired older adults.

Expanding OTC Availability & E-Commerce Reach

The FDA cleared three saliva sprays for OTC sale in March 2024, and the EMA granted a harmonized OTC path for carboxymethylcellulose gels in September 2024, eliminating physician visits for millions with mild symptoms.[2]U.S. Food and Drug Administration, “OTC Drug Monograph Updates,” fda.gov Amazon Pharmacy sales of dry-mouth products surged 127% between Q1 2024 and Q4 2025, with subscription refills indicating sticky demand. Telehealth platforms integrated xerostomia screening into diabetes programs, routing 220,000 U.S. users to product recommendations in 2025. Manufacturers enjoy higher direct-to-consumer margins, yet they must invest in digital content to boost brand recall. China remains the missing piece; its regulator has not yet approved OTC status, which is delaying e-commerce momentum in the world’s second-largest pharmaceutical market.

Development of Innovative Mucoadhesive & Sustained-Release Formulations

Conventional sprays relieve symptoms for 10-20 minutes, whereas new chitosan and polycarbophil blends adhere to the mucosa for over two hours, reducing daily dosing in half. A 2024 randomized trial confirmed that 120-minute contact times are effective with these polymers. GlaxoSmithKline’s Biotene Advanced Gel was launched in 2025 with a phase-change matrix that maintains hydration scores with four daily uses, compared to eight for legacy gels. Sun Pharmaceutical’s microencapsulated pilocarpine posted 12-hour stimulation in Phase II during 2025, potentially eliminating midday dosing. USPTO filings for xerostomia mucoadhesives almost doubled from 2022 to 2023, and then again from 2023 to 2024, signaling a tight race for intellectual property.

Emerging Regenerative & Cell-Based Salivary-Gland Therapies

Aquaporin-1 gene therapy raised unstimulated whole saliva flow 47% at six months in a 68-patient Phase IIb study completed in 2025. Autologous MSC injections improved flow and symptom scores in Sjögren’s patients in a 2024 trial, with no serious safety issues reported. Two cell therapies received RMAT designation in 2025, accelerating pathways but bringing reimbursement uncertainty due to the expected costs of USD 75,000 per patient. In 2024, bioprinted organoids produced functional saliva in mice for 90 days, attracting USD 18 million for translation. High cost and invasive procedures confine adoption to tertiary centers this decade, limiting immediate disruption to the broader xerostomia therapeutics market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Prescription Sialogogues | –0.6% | Global, hardest in emerging markets | Medium term (2-4 years) |

| Stringent Regulatory Hurdles for Novel Formulations | –0.5% | FDA and EMA jurisdictions | Medium term (2-4 years) |

| Limited Long-Term Efficacy of Existing Substitutes | –0.4% | Global | Long term (≥ 4 years) |

| Raw-Material Price Volatility | –0.3% | Global with Asian supply dependence | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Prescription Sialogogues

Branded pilocarpine costs USD 450 for 30 days in the United States, and generics still average USD 180, spurring a 31% abandonment rate among new Sjögren’s patients. Cevimeline’s branded version commands USD 620 monthly, an out-of-reach figure for many Medicare beneficiaries.[3]Journal of Managed Care & Specialty Pharmacy, “Prescription Abandonment,” jmcp.org Indian generics cost approximately INR 3,200 per month, which is approximately 12% of the median household income, limiting uptake to affluent urban users. Generic competition has not typically resulted in price declines of 60-80% because active ingredient synthesis remains complex and supply is concentrated. Prior authorization requirements by 43% of U.S. plans add administrative friction that delays the start of therapy by up to two weeks.

Stringent Regulatory Hurdles for Novel Formulations

In 2024, FDA guidance mandated extensive usability and human-factors testing for oral delivery devices, which elongated development cycles by nearly one year and added approximately USD 2.5 million in costs per product. The EMA required twelve-month mucosal irritation studies in 2025, which delayed two mucoadhesive gels by 18 months. Dual drug-device products must satisfy both pathways, creating 47-month approval times in one recent case. Japan’s PMDA added five-year real-world evidence mandates for sustained-relief labels, deterring small entrants. These hurdles concentrate innovation inside large firms that can shoulder longer timelines.

Segment Analysis

By Therapeutic Modality: Devices Challenge Substitute Dominance

Artificial saliva and substitutes held 62.21% of the xerostomia therapeutics market size in 2025, supported by entrenched first-line prescribing in oncology and rheumatology. Electro-stimulation devices are expected to expand at the fastest rate, with a 7.02% CAGR to 2031, aided by Medicare reimbursement codes added in late 2024 that reduced patient co-pays by approximately 40%. Salivary stimulants, both prescription and OTC, remain a mid-tier option because cholinergic side effects limit long-term compliance in roughly one-third of users. Other modalities, such as laser photobiomodulation, account for less than 5% of revenue but could gain traction if payer policies adapt.

Manufacturers are diverging in strategy. Substitute leaders push formulation upgrades, as evident in GlaxoSmithKline’s xylitol-enhanced gel, which now offers caries protection. Device newcomers embed Bluetooth modules that log usage, enabling clinicians to remotely tune pulse settings and increase adherence, while also generating data for payer contracting. The xerostomia therapeutics industry, therefore, crosses into connected-care territory, raising entry barriers for traditional consumer goods players.

Note: Segment shares of all individual segments available upon report purchase

By Product Form: Mouthwashes Gain on Convenience

Sprays commanded 46.73% of the xerostomia therapeutics market share in 2025, owing to their portability in community settings. Mouthwashes and rinses are expected to grow at a 7.48% CAGR through 2031, as mucoadhesive polymers extend relief beyond two hours, thereby halving the daily dosing frequency. Gels maintain traction in oncology wards because their higher viscosity shields the mucosa during radiotherapy; however, consumer surveys cite a sticky texture as a deterrent in everyday use. Lozenges remain a niche option for discreet use, working well only in mild cases where residual salivary flow persists.

Form differentiation aligns with demographic needs. Seniors with dexterity issues prefer redesigned spray actuators requiring less grip strength, while nursing homes adopt once-daily mouthwash rounds to streamline staff workloads. Single-dose spray vials, though 20-30% pricier, address infection-control needs in immunocompromised patients. Regulatory guidance on preservatives prompted several firms to adopt preservative-free packaging in 2025, a premium niche that is expected to grow as awareness increases. Overall, the product landscape is fragmenting, providing the xerostomia therapeutics market with ample room for targeted innovations.

By Distribution Channel: Online Gains as Telehealth Integrates

Hospital pharmacies accounted for 42.88% of revenue in 2025, reflecting their historical association with oncology and transplant centers. Online pharmacies are expected to post the swiftest gains, at a 6.13% CAGR from 2026 to 2031, as subscription programs and lower copays attract both seniors and busy professionals. Retail chains, which held about a 35% share in 2025, face margin compression yet experiment with in-store xerostomia consultations to differentiate themselves on service.

Payer decisions reinforce the tilt. A 2025 review found that 62% of Medicare Advantage plans set copays of USD 5-15 lower for 90-day online fills than for 30-day retail equivalents, driving older adults to internet channels. Hospital systems respond by creating xerostomia clinics offering product trials and compounded solutions, generating higher per-patient revenue but slower volume growth. Regulatory policing of unapproved claims in online stores remains a constraint, setting a compliance cost that favors larger platforms. The result is a channel mix in flux, with each route carving unique value propositions.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America accounted for 39.16% of global revenue in 2025, driven by high disease awareness, comprehensive insurance coverage, and aggressive direct-to-consumer advertising. The xerostomia therapeutics market size in the United States represents 85% of the regional total and is stable, as generic erosion and OTC competition offset unit growth. Canada lags due to strict formulary rules that cover only severe cases. At the same time, Mexico’s expanded Seguro Popular list is expected to add over one million treated patients by 2027, despite the implementation of tight price controls.

Germany leads per-capita consumption owing to statutory insurance coverage and a dense network of dental clinics. The United Kingdom faces dual regulatory filings post-Brexit, which add months to approval timelines, yet have allowed faster clearance for some niche formulations. France posts strong gel uptake in head-and-neck radiation centers, whereas Italy and Spain restrict OTC reimbursement, suppressing volume growth among price-sensitive seniors. Nordic markets excel online; Sweden sees 42% of xerostomia sales through e-pharmacies, contrasting with Eastern Europe where brick-and-mortar dominance persists.

The Asia-Pacific region is expected to grow at an 8.04% CAGR, the fastest worldwide. China’s diabetic population of 140 million drives huge latent demand, and inclusion of key substitutes on the 2024 national reimbursement list stimulated urban sales even at 40% co-pay levels. Japan boasts the world’s highest electro-stimulation penetration rate at 18% of domestic sales, reflecting a cultural preference for device solutions. India’s launch of ultra-low-cost pilocarpine in 2025 added millions of new users, but the uptake remains skewed towards urban areas. Mature markets, such as Australia and South Korea, favor premium, sustained-release gels backed by full insurance coverage. Southeast Asia began local manufacturing in 2024-2025, slicing import costs and accelerating volume in Indonesia and Thailand.

Competitive Landscape

The top five suppliers, GlaxoSmithKline, Colgate-Palmolive, 3M, Pfizer, and Sun Pharmaceutical, leave space for regional and technology-focused challengers. GlaxoSmithKline expanded Biotene into 15,000 new stores and introduced a mucoadhesive variant that provides relief for up to two hours, reinforcing its 18% global market share. Colgate-Palmolive invested capital in digital ads targeting hypertensive and diabetic groups, resulting in double-digit growth in online volume. Device specialists such as Saliwell and GenNarino employ Bluetooth telemetry and consumable electrodes to cultivate recurring revenue streams.

M&A activity accelerated. Pfizer spent USD 340 million in March 2025 on a gene-therapy start-up to secure a foothold in regenerative solutions, which are likely to enter Phase III by 2027. Patent filings for mucoadhesive and sustained-release systems increased to 37 in 2024-2025, with submissions from Colgate-Palmolive, GlaxoSmithKline, and Sun Pharmaceutical accounting for over half of the filings. Digital differentiation is emerging; data-rich devices and AI platforms enable value-based contracting with insurers, an edge that consumer product giants are only starting to build.

Regulatory expertise separates winners and laggards. Companies with seasoned compliance teams move through dual drug-device pathways more quickly, while small innovators exhaust their cash reserves during 12- to 18-month delays. Regional specialists often partner with global companies to achieve a larger distribution scale, as seen in BioXtra’s 2025 deal for a Japanese rollout. The result is a moderately concentrated yet rapidly evolving xerostomia therapeutics market that rewards scale, technology integration, and regulatory agility.

Xerostomia (Dry Mouth Disease) Therapeutics Industry Leaders

Parnell Pharmaceuticals Inc.

Quest Healthcare

GlaxoSmithKline plc

Synedgen Inc.

ADVANZ PHARMA Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Aquoral and Dentulu formed a partnership to deliver advanced xerostomia therapy through Dentulu’s telehealth network.

- October 2025: UCSF’s Hive Research initiative reported fresh progress on regenerative salivary treatments funded by SBIR grants.

- March 2025: University of South Australia researchers unveiled a citrus-oil mouthwash that relieved dry mouth in cancer patients undergoing radiation.

- March 2025: Ribox Therapeutics dosed the first patient in a Phase I/IIa study of RXRG001, the inaugural circular RNA therapy for radiation-induced xerostomia.

- February 2025: Saliwell highlighted three electro-stimulation innovations aimed at radiation-induced xerostomia at an international oral health forum.

Global Xerostomia (Dry Mouth Disease) Therapeutics Market Report Scope

As per the scope of the report, xerostomia is defined as a dry mouth, resulting from reduced or absent saliva flow. It is not a disease, but it could be a symptom of various medical conditions, a side effect of radiation to the head and neck, or a side effect caused by a wide variety of medications. The xerostomia (dry mouth disease) therapeutics market is segmented by type, product, distribution channel, and geography. By type, the market is segmented into artificial saliva/saliva substitutes, and salivary stimulants. By product, the market is segmented into drugs, salivary pens, and other products. The other product segment includes oral sprays and gels and ointments. By distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy. The report also covers the market size and forecasts for the xerostomia (dry mouth disease) therapeutics market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Artificial Saliva / Saliva Substitutes |

| Salivary Stimulants |

| Electro-stimulation Devices |

| Other Therapeutic Modalities |

| Sprays |

| Gels |

| Lozenges / Pastilles |

| Mouthwashes / Rinses |

| Other Product Forms |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapeutic Modality | Artificial Saliva / Saliva Substitutes | |

| Salivary Stimulants | ||

| Electro-stimulation Devices | ||

| Other Therapeutic Modalities | ||

| By Product Form | Sprays | |

| Gels | ||

| Lozenges / Pastilles | ||

| Mouthwashes / Rinses | ||

| Other Product Forms | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the xerostomia therapeutics market in 2026?

The market stands at USD 1.93 billion in 2026 and is projected to reach USD 2.35 billion by 2031.

Which therapeutic modality grows fastest through 2031?

Electro-stimulation devices grow at a 7.02% CAGR due to reimbursement support and clinical validation.

What region will show the highest growth rate?

Asia-Pacific posts the quickest regional expansion with an 8.04% CAGR driven by diabetes prevalence and aging populations.

Why are mouthwashes gaining preference over sprays?

Mucoadhesive polymers in new mouthwashes extend relief beyond two hours, reducing the need for daily applications and increasing satisfaction.

What is the main cost barrier facing patients?

Branded salivary stimulants such as pilocarpine and cevimeline cost USD 450-620 per month, leading to high abandonment rates.