Wooden Decking Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

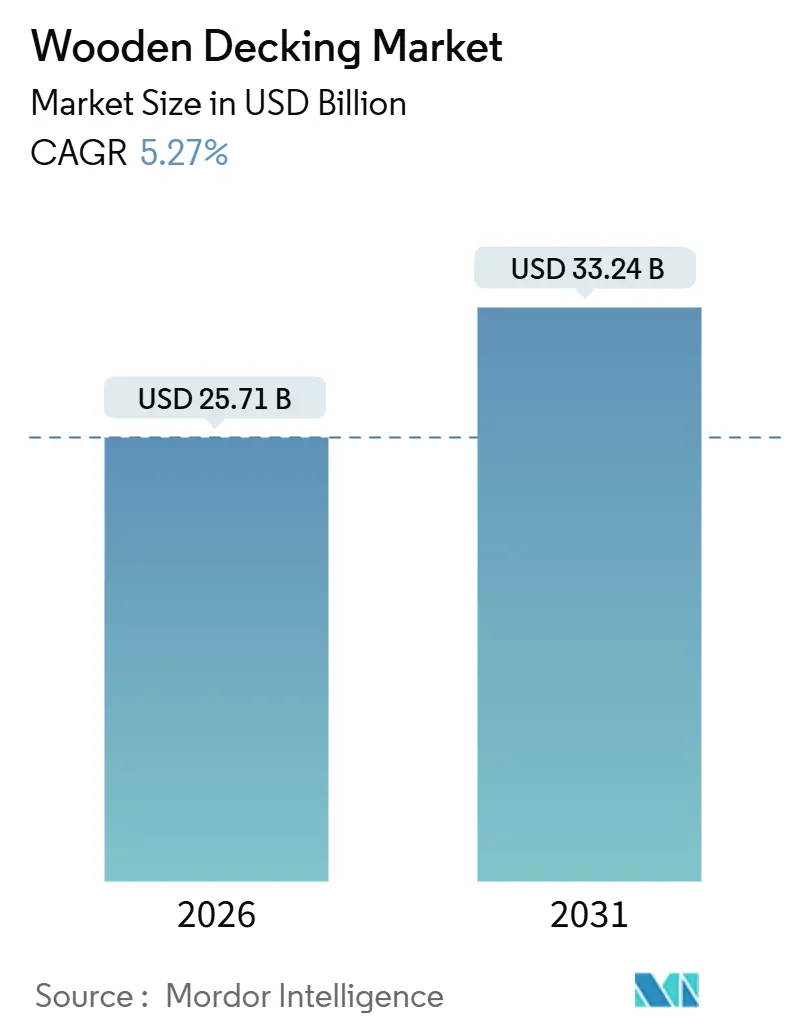

| Market Size (2026) | USD 25.71 Billion |

| Market Size (2031) | USD 33.24 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

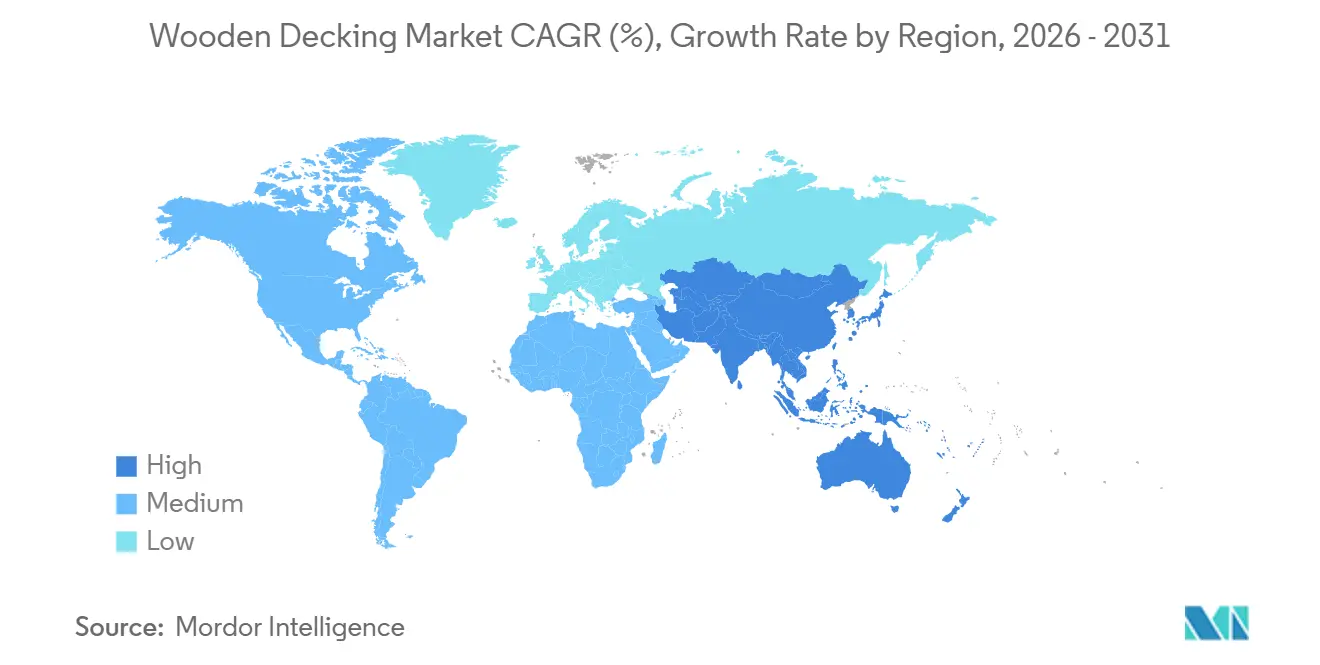

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wooden Decking Market Analysis by Mordor Intelligence

The Wooden Decking Market size is estimated at USD 25.71 billion in 2026, and is expected to reach USD 33.24 billion by 2031, at a CAGR of 5.27% during the forecast period (2026-2031). This growth path reflects resilient residential remodeling demand, expanding green-building mandates, and rapid innovation in modified-wood technologies that together buoy the wooden decking market even as composite substitution intensifies. Pressure-treated pine retains price leadership, yet consumers continue to favor materials that promise longer service life, lighter maintenance, and verified sustainability credentials. Regional dynamics remain diverse: North America benefits from an aging housing stock and a strong DIY culture, while Asia-Pacific delivers the fastest incremental volume thanks to ongoing urbanization and a growing middle-class homeowner base. Over the next five years, suppliers that align product portfolios with fire-safety codes, eco-certification requirements, and modular installation systems are expected to capture outsized gains within the wooden decking market.

Key Report Takeaways

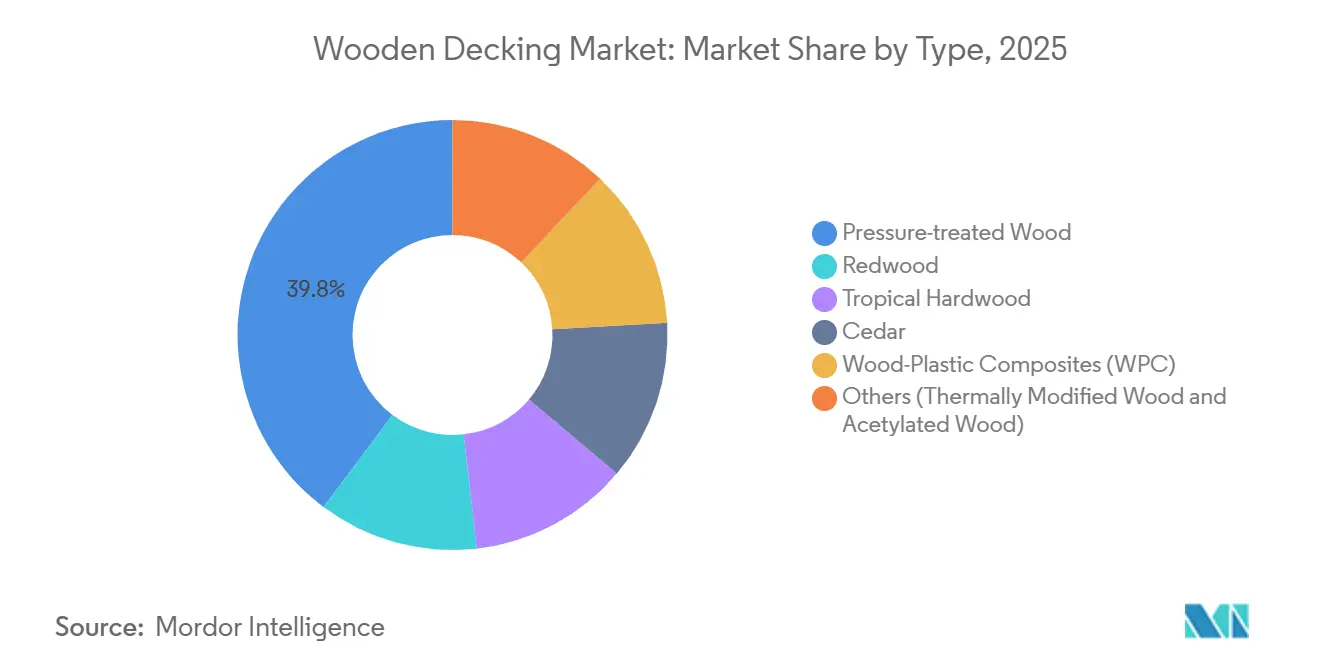

- By material type, pressure-treated wood held 39.75% of the Wooden Decking market share in 2025, while wood-plastic composites are forecast to expand at an 8.67% CAGR from 2026 to 2031.

- By application, floor installations accounted for 46.91% of the Wooden Decking market size in 2025 and will advance at a 5.42% CAGR through 2031.

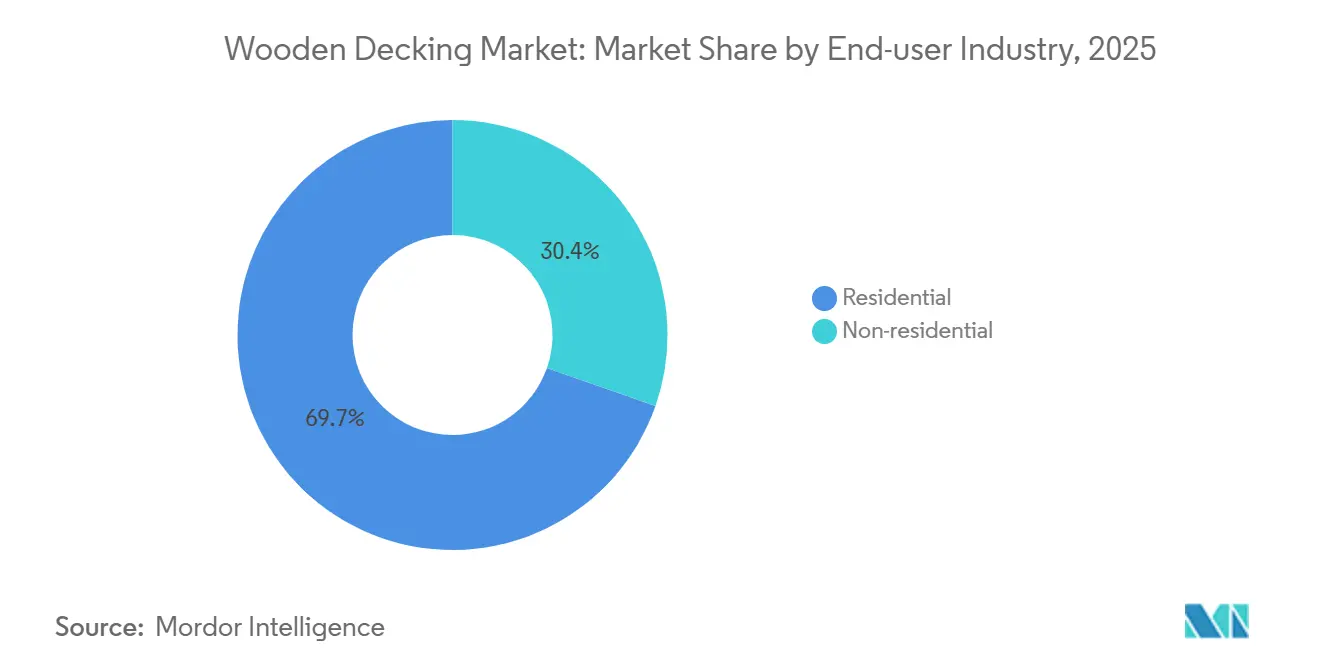

- By end user, residential projects represented 69.65% of demand in 2025; the segment is projected to grow at a 5.37% CAGR between 2026 and 2031.

- By region, North America commanded 36.77% of the Wooden Decking market share in 2025, while Asia-Pacific is poised for the fastest regional CAGR of 5.37% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wooden Decking Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remodeling and refurbishment activities | +0.8% | United States, United Kingdom, Germany, France | Medium term (2-4 years) |

| Residential outdoor-living and DIY culture | +1.2% | Global focus on United States and Australia | Short term (≤ 2 years) |

| Eco-certified wood under green-building codes | +0.9% | Europe, California, Singapore | Long term (≥ 4 years) |

| Advances in thermally modified and acetylated wood technologies | +0.7% | Nordic producers and premium segments in North America | Long term (≥ 4 years) |

| Municipal mass-timber procurement | +0.4% | United Kingdom, France, Canada, Oregon, Washington | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increase in Remodeling and Refurbishment Activities

Residential remodeling expenditure in the United States reached USD 485 billion in 2024, with outdoor-living upgrades such as deck replacement representing 12% of spend[1]Joint Center for Housing Studies, “Improving America’s Housing 2025,” jchs.harvard.edu. The median US home age exceeded 40 years in 2024, and decks built during the 1980s-1990s have reached end-of-life, prompting widespread replacement. Mortgage-rate pressure is discouraging home sales, so owners invest in improving existing properties, placing decking high on the project list. In Europe, the United Kingdom’s Timber in Construction Roadmap targets 300,000 cubic meters of additional timber usage each year by 2030, much of it tied to garden-decking and balcony upgrades. Bundling of energy-efficiency retrofits with outdoor-space enhancements further lifts volume. As a result, the wooden decking market gains predictable replacement demand that moderates cyclicality.

Surge in Residential Outdoor-Living and DIY Culture

Sixty-eight percent of US homeowners plan an outdoor project in 2025, up from 52% in 2019, underlining durable lifestyle shifts toward at-home leisure. Sales of decking materials to DIY customers at big-box retailers expanded at double-digit rates in 2024. Easy-to-assemble kits, hidden-fastener systems, and ubiquitous online tutorials have lowered the perceived difficulty of installing a deck, broadening the addressable buyer pool. Comparable momentum appears in Australia, where composite and timber decking volumes rose 15% year over year in 2024. The wooden decking market, therefore, benefits from both discretionary lifestyle spending and the democratization of installation skills.

Demand for Eco-Certified Wood Under Green-Building Codes

LEED v4.1 awards credits for FSC-certified wood, while LEED v5 extends recognition to PEFC and SFI certifications. California’s Title 24 update in 2025 requires environmental product declarations for all wood decking used in public projects, favoring suppliers with chain-of-custody documentation. The share of certified lumber in global industrial roundwood rose from 38% in 2020 to an estimated 48% in 2025. Extended service life from acetylated and thermally modified woods further strengthens lifecycle sustainability profiles, making eco-certified options commercially attractive. These rules anchor long-run demand within the wooden decking market instead of creating transient spikes.

Advances in Thermally Modified and Acetylated Wood Technologies

Thermal modification reduces hygroscopicity, delivering decking that resists warping in humid climates, while acetylation replaces hydroxyl groups to extend service life beyond 30 years. Accoya wood now carries a 50-year above-ground warranty and meets Class 1 durability under EN 350. Accsys doubled acetylation capacity to 80,000 cubic meters in 2024, lowering unit cost by 18%, and Kebony opened distribution channels in Japan and South Korea the following year. These innovations combine premium performance with non-toxic profiles, gradually converting design-conscious buyers and institutional specifiers, and thereby lifting the wooden decking market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution by composite and PVC decking | -1.1% | Coastal United States, United Kingdom, Netherlands, Australia | Short term (≤ 2 years) |

| Volatile lumber prices and supply-chain shocks | -0.8% | Global, with acute swings in North America and Europe | Short term (≤ 2 years) |

| Stringent fire-safety rules on untreated softwoods | -0.6% | California, Oregon, Colorado, Australia bushfire zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Substitution by Composite and PVC Decking

Wood-plastic composites captured 28% of U.S. decking demand in 2025, gaining six percentage points in five years[2]Trex Company, “Q3 2024 Earnings Release,” trex.com. Homeowners in high-moisture or salt-air regions favor maintenance-free surfaces, and national builders increasingly specify composites to cut warranty risk. Regulatory support compounds the shift: California’s 2025 Chapter 7A update requires Class A-rated decking in wildland-urban interface areas, a threshold that most untreated softwoods fail to meet. As composites replicate exotic-wood aesthetics and widen color choices, the wooden decking market confronts ongoing share dilution in coastal geographies.

Volatile Lumber Prices and Supply-Chain Shocks

Random Lengths framing-lumber prices swung between USD 430 and USD 475 per thousand board feet during 2024-2025, compressing contractor margins and delaying projects. Reduced North American sawmill capacity, wildfire-damaged timber, and export tariffs compound supply tightness. Similar pressures are seen in Europe, where bioenergy demand diverts logs away from lumber production. Unpredictable raw-material costs erode buyer confidence, nudging some toward composites that carry more stable pricing owing to integrated resin and fiber sourcing. Such volatility dampens near-term growth in the wooden decking market.

Segment Analysis

By Type: Composites Challenge Pressure-Treated Dominance

Pressure-treated wood retained a 39.75% share of the wooden decking market in 2025, thanks to its USD 1.50-2.00 per linear-foot price point and established retail networks. The segment still benefits from the AWPA 2024 updated Use Category system that reduced copper-azole loading by 12% without undercutting durability. Despite this base, composites are projected to log an 8.67% CAGR during 2026-2031, the quickest among all materials. Their encapsulated-shell designs prevent moisture ingress and carry warranties up to 50 years, narrowing long-term cost differentials. Thermally modified and acetylated woods, grouped under Others, were helped by capacity expansion at Accsys and distribution partnerships forged by Kebony and Thermory. As a result, the wooden decking market continues to bifurcate between value-driven pressure-treated lumber and performance-driven alternatives that command premium pricing.

Pressure-treated pine still satisfies budget buyers and large-volume DIY projects, while composites seize coastal share where humidity, salt spray, and fire codes accelerate lifecycle replacements. Tropical hardwoods remain a niche, concentrated in luxury hospitality and high-end residential settings that demand natural aesthetics and extreme density. Redwood and cedar supply constraints, triggered by lower federal timber sales in California, sustain pricing premiums that edge some specifiers toward thermally modified substitutes. Collectively, these dynamics underpin an evolving material mix that keeps innovation at the core of the wooden decking market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Flooring Anchors Demand, Railings Gain Share

Floor installations represented 46.91% of the wooden decking market size in 2025 and are expected to advance at a 5.42% CAGR through 2031. Growth stems from modular fastener systems that cut labor requirements by as much as 25%, encouraging wider DIY uptake and faster turnarounds for professional contractors. Railings captured nearly 30% share in 2025 and benefit from International Residential Code changes that now call for taller, more robust guardrails on elevated decks, increasing linear footage per project. This regulatory shift raises bill-of-materials value even when overall square footage remains stable.

Wall-cladding demand resides mainly in commercial segments; European architects frequently pair vertical wood elements with cross-laminated timber structures to achieve biophilic design goals and consistent material palettes. Other uses, including pergolas, privacy screens, and built-in furniture, absorb the balance of volume and enjoy strong price realization because homeowners treat these items as aesthetic upgrades. As multi-level outdoor rooms become common, accessories such as lighting channels and integrated seating drive incremental board-foot consumption, reinforcing positive mix dynamics within the wooden decking market.

By End-User Industry: Residential Dominance, Non-Residential Upside

Residential customers commanded 69.65% of total volume in 2025 and are forecast to grow at a 5.37% CAGR during 2026-2031, mirroring housing-stock age profiles and a persistent stay-at-home lifestyle bias. Remodeling Magazine reported that wood-deck additions recoup 63% of cost at resale, boosting homeowner confidence in project payback. DIY channels continue to expand; individual consumers formed major decking sales at leading home-improvement chains in 2024. This deep, steady demand base underpins the wooden decking market even when new-build housing cycles pause.

Non-residential demand is projected to rise due to hotels, retail centers, and institutional builds that specify premium materials for high-traffic areas. Public-sector mass-timber schemes in Europe and Canada further enlarge institutional appetite for engineered-wood decking that shares aesthetics and structural coherence with primary CLT or glulam elements. Warranty requirements of 25 years or more and mandatory Class A fire ratings drive specifiers toward composites and modified woods, supporting revenue-per-foot growth across the wooden decking market.

Geography Analysis

North America controlled 36.77% of the wooden decking market in 2025, anchored by USD 485 billion in US remodeling spend that funnels 12% toward outdoor projects. Replacement cycles remain active because most decks installed before 2000 have reached the typical 20-25-year service limit. Canada’s updated 2025 building code, permitting 18-story mass-timber structures, adds public-plaza decking demand, and Mexico’s year-over-year rise in cement consumption during Q3 2024 indicates broader construction momentum that also lifts decking volumes. Fire-safety regulations in western US states accelerate composite penetration, while lumber-price volatility complicates planning for smaller contractors, nudging some to lock in composite supply contracts to avoid price swings.

Asia-Pacific delivers the fastest CAGR at 5.37% through 2031. China’s focus on quality-of-life improvements in existing urban housing, despite wider real-estate cooling, favors balcony and terrace refurbishments that require decking. India’s 11% increase in 2024 housing starts boosts pressure-treated lumber shipments into tier-2 cities. Japan and South Korea gravitate toward premium acetylated or thermally modified species for high-rise balconies, a niche Kebony has targeted since expanding local distribution in 2025. ASEAN tourism rebounded in 2024, and hospitality chains in Thailand and Indonesia refurbished pool decks and beachfront walkways, thereby lifting composite and hardwood consumption.

Europe remains a pivotal technology and policy leader within the wooden decking industry. The United Kingdom aims to inject 300,000 cubic meters of timber into construction annually by 2030, a figure that includes residential garden decking. Germany and France have begun adopting LEED v5 alongside DGNB standards, spurring uptake of FSC-certified lumber and boosting demand for product-specific environmental declarations. Nordic producers Thermory and Metsa Wood enjoy proximity to spruce and ash resources suitable for thermal modification, enabling competitive exports across Europe and into North America. Bioenergy competition for sawlogs, however, tightens supply and supports hardwood and composite pricing across the continent.

South America and the Middle East & Africa remain smaller contributors. Brazilian resort developments continue specifying tropical hardwoods despite a 2.1% contraction in domestic construction in 2024. Saudi Arabia’s Vision 2030 projects incorporate promenade decks, yet high reliance on imports inflates costs by nearly 30% compared with North American supply chains. While their combined volume remains modest, strategic vendors view these regions as future growth pockets once local standards evolve to prioritize sustainability and fire performance.

Competitive Landscape

The Wooden Decking market is fragmented. Composite leaders Trex and AZEK benefit from vertically integrated extrusion lines and extensive dealer networks that standardize training and after-sales support. AZEK’s 2024 purchase of StruXure extends its reach into pergolas and complements railing lines, enabling packaged outdoor-structure deals that raise share of wallet. Given scale advantages in resin procurement and nationwide distribution, incremental consolidation is likely. Nonetheless, regional sawmills and specialty modifiers will stay relevant by offering localized species and fast turnarounds that large multinationals cannot match.

Wooden Decking Industry Leaders

Trex Company, Inc

The AZEK Company LLC

Fiberon

UFP Industries, Inc.

West Fraser Timber Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: SRS Distribution Inc. announced its acquisition of Specialty Wood Products, Inc., a distributor specializing in premium wooden decking, siding, heavy timber products, and other architectural-grade building materials.

- March 2025: UFP Industries, Inc. acquired a 30-acre site in Lackawanna, a suburb of Buffalo, New York. This site will be developed into a state-of-the-art facility, set to double the production capacity for the company's Deckorator brand's Surestone composite-decking product.

Global Wooden Decking Market Report Scope

A deck is an elevated surface usually constructed outdoors, elevated from the ground, and connected to the buildings. A wooden deck gives a functional outdoor living space. A railing mainly encloses it for safety purposes. Wooden deck rails are composed of an assembly of parts. There are different methods for building guardrails with various materials for decks, but most rails made from wood share a common set of components. The wooden decking market is segmented by type, application, end-user industry, and geography. The market is segmented by pressure-treated wood, redwood, tropical hardwood, cedar, wood-plastic composites, and other types. By application, the market is segmented into the railing, floor, wall, and other applications. By end-user industry, the market is segmented into residential and non-residential. The report also covers the market size and forecasts for the wooden decking market in 11 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Pressure-treated Wood |

| Redwood |

| Tropical Hardwood |

| Cedar |

| Wood-Plastic Composites (WPC) |

| Others (Thermally Modified Wood, Acetylated Wood) |

| Railing |

| Floor |

| Wall |

| Other Applications |

| Residential |

| Non-residential |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Pressure-treated Wood | |

| Redwood | ||

| Tropical Hardwood | ||

| Cedar | ||

| Wood-Plastic Composites (WPC) | ||

| Others (Thermally Modified Wood, Acetylated Wood) | ||

| By Application | Railing | |

| Floor | ||

| Wall | ||

| Other Applications | ||

| By End-user Industry | Residential | |

| Non-residential | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the wooden decking market?

The wooden decking market size is USD 25.71 billion in 2026 and is set to reach USD 33.24 billion by 2031.

Which region is growing the fastest for wooden decking?

Asia-Pacific holds the highest forecast CAGR at 5.37% between 2026 and 2031 due to rapid urbanization and expanding middle-class homeownership.

Why are composites gaining share against traditional wood?

Composites offer low maintenance, Class A fire ratings, and warranties up to 50 years, making them attractive in coastal and wildfire-prone areas.

How do fire-safety codes affect material choice?

Updated codes in California, Colorado, and Australia require Class A decking in high-risk zones, effectively shifting demand toward composites or modified hardwoods.

Which application dominates wooden decking demand?

Floor installations represent 46.91% of 2025 volume and will remain the largest application as decks continue to serve as primary outdoor living surfaces.