Market Overview

| Study Period | 2020 - 2030 |

|---|---|

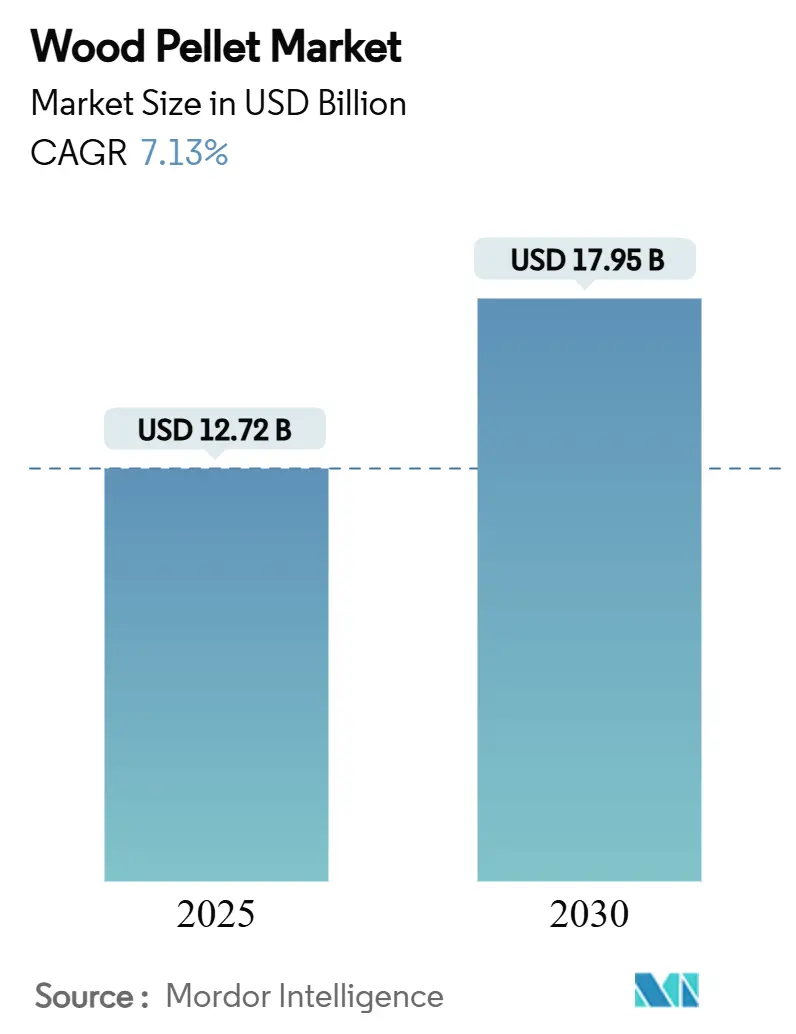

| Market Size (2025) | USD 12.72 Billion |

| Market Size (2030) | USD 17.95 Billion |

| Growth Rate (2025 - 2030) | 7.13% CAGR |

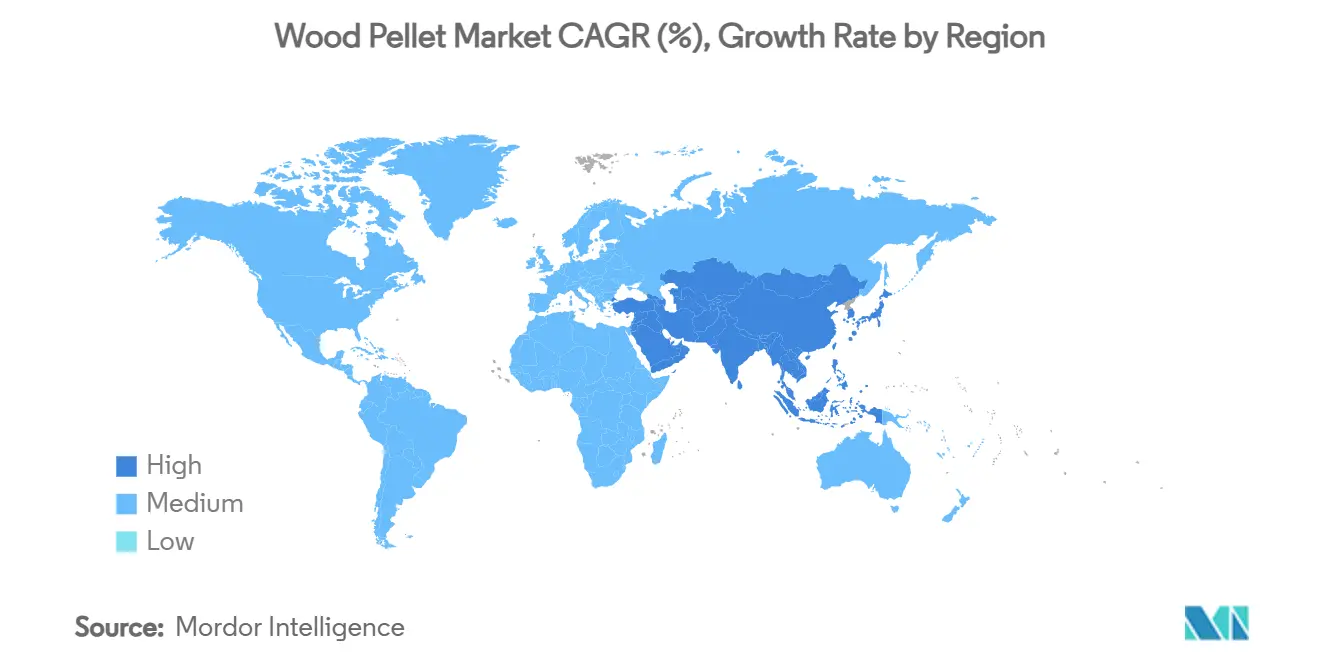

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wood Pellet Market Analysis by Mordor Intelligence

The Wood Pellet Market size is estimated at USD 12.72 billion in 2025, and is expected to reach USD 17.95 billion by 2030, at a CAGR of 7.13% during the forecast period (2025-2030).

Rapid corporate adoption of net-zero procurement contracts has moved demand beyond the traditional policy-led cycle, with long-term offtake agreements now shaping plant-level investment decisions across North America, Europe, and Asia. Heating remains the largest use case, yet power generators ramp up purchases to support coal-to-biomass conversions, extending asset life while meeting climate targets. Producers are diversifying feedstock portfolios—shifting from forest residue toward agriculture-based inputs—to avoid sustainability bottlenecks and satisfy new certification regimes. Geographic supply chains are in flux as South American capacity gains momentum, eroding Europe’s historical dominance and challenging North American exporters to defend their share through higher-grade products and traceable forestry practices. Consolidation among incumbents continues, but rising regional challengers and premium-grade innovators are gradually diluting their influence in the wood pellet market.

Key Report Takeaways

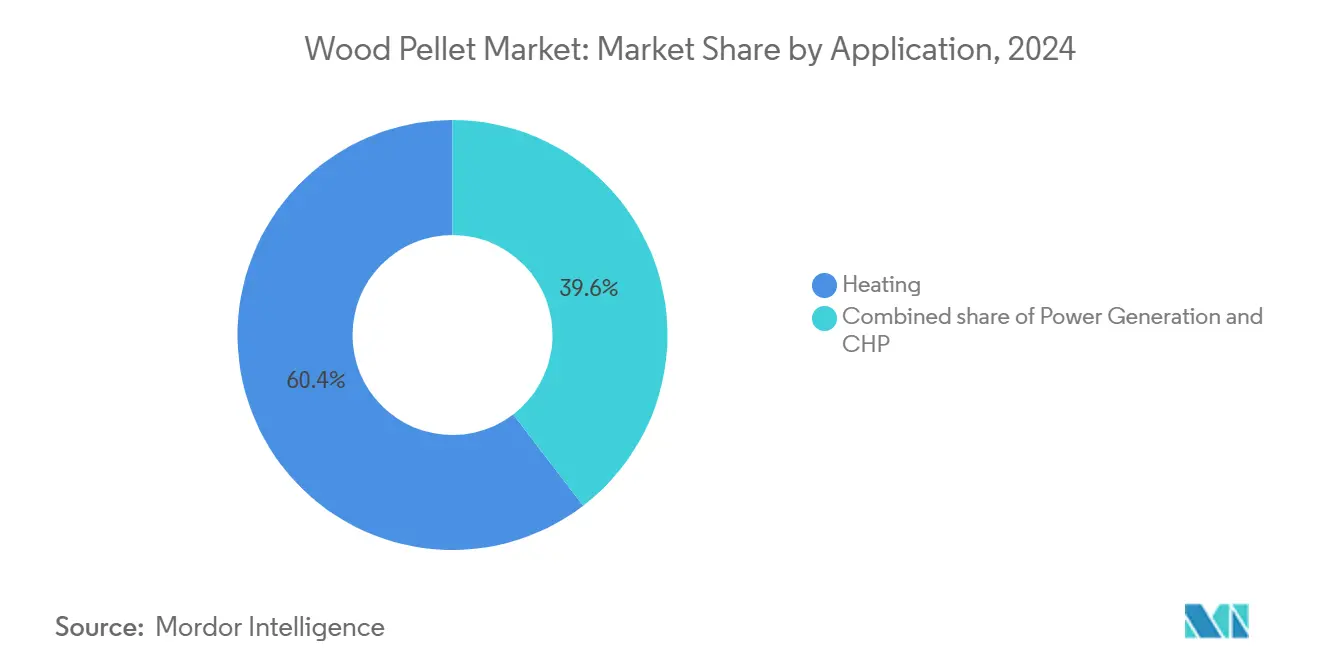

- By application, heating captured 60.4% of the wood pellet market share in 2024, while power generation is projected to advance at a 7.22% CAGR to 2030.

- By end-user, industrial and utility buyers held 47.5% share of the wood pellet market size in 2024; commercial demand is rising fastest at an 8% CAGR through 2030.

- By feedstock, forest and wood residue accounted for 57.5% of the wood pellet market size in 2024, whereas agricultural residue will expand at a 7.25% CAGR during the same horizon.

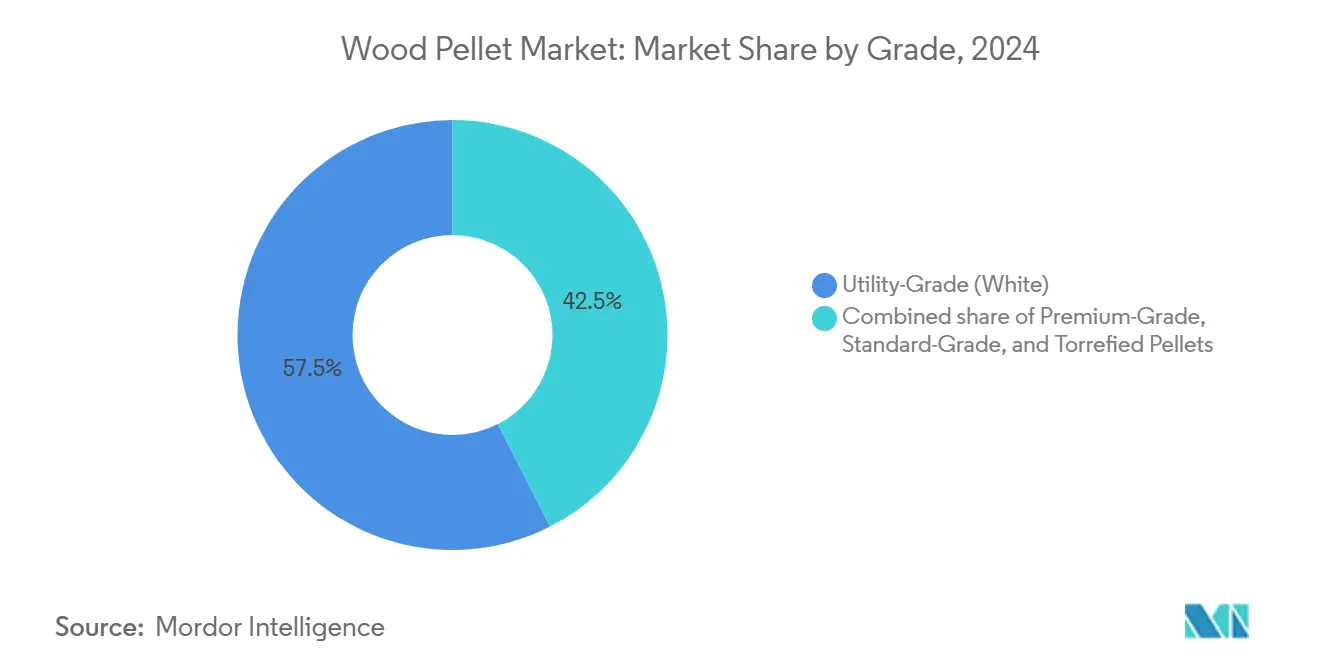

- By grade, utility-grade pellets led with 57.5% revenue share in 2024; torrefied pellets record the highest outlook at a 9.25% CAGR through 2030.

- By region, Europe dominated with 66.5% of the wood pellet market share in 2024, but Asia-Pacific is forecast to climb at a 14.55% CAGR to 2030.

Global Wood Pellet Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Japan-South Korea Biomass Co-Firing Mandates Accelerating Industrial Pellet Imports | +1.2% | Asia-Pacific, with spillover to North America exports | Medium term (2-4 years) |

| EU REDIII Sustainability Criteria Fueling Demand for Certified Premium Pellets | +0.8% | Europe & Global supply chains | Long term (≥ 4 years) |

| Corporate Net-Zero Contracts Boosting U.S. Export-Grade Production | +1.5% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| District-Heating Build-out in Nordics Propelling Pellet Boiler Adoption | +0.6% | Northern Europe, with expansion to Central Europe | Long term (≥ 4 years) |

| Volatile European Gas Prices Driving Residential Stove Conversions | +0.9% | Europe, with indirect effects on global pricing | Short term (≤ 2 years) |

| Emergence of Torrefied “Black Pellets” for Coal-Plant Retrofits | +0.7% | Global, concentrated in coal-dependent regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Japan–South Korea Biomass Co-Firing Mandates Accelerating Industrial Pellet Imports

Asian energy policies are tilting decisively toward co-firing, with Japan’s feed-in tariff and South Korea’s renewable portfolio standard pushing combined industrial pellet imports past 8 million t by 2026 [1]Argus Media, “Vietnam pellet exports hit record 5.3 mn t,” argusmedia.com. South Korean utilities are locked in long-term deals before the 2025 subsidy reset, ensuring supply continuity even as incentives decline. Japan requires strict certification under sustainability schemes, splitting the wood pellet market into premium and standard layers that command distinct price levels. Vietnamese exports surged to 5.3 million tons in the first eleven months of 2024, underscoring Southeast Asia’s pivot to serve this certified demand. Co-firing rules also spur torrefaction investments because high-energy-density pellets lower shipping costs and integrate seamlessly into existing pulverized coal systems. These mandates are underwriting next-generation biomass technology while gifting producers predictable revenue streams.

EU REDIII Sustainability Criteria Fueling Demand for Certified Premium Pellets

The Renewables Directive III is reshaping European procurement, as non-certified material risks outright exclusion [2]European Commission, “Directive (EU) 2018/2001 on the promotion of the use of energy from renewable sources,” europa.eu. Certification schemes such as ENplus® and the Sustainable Biomass Program handled a record 15.6 million t in 2024, of which 12.45 million t were pellets. Utilities are now signing take-or-pay contracts that cover full lifecycle traceability, enabling producers to secure financing for vertically integrated forestry assets and digital monitoring systems. Price premiums of 15-20% for certified products have quickly become normalized, reallocating capital toward chain-of-custody technology and pushing uncertified suppliers toward lower-value markets. With cascading-use rules prioritizing higher-value wood before energy recovery, producers are re-engineering feedstock plans to remain compliant, cementing certification as a competitive requirement rather than a differentiator within the wood pellet market.

Corporate Net-Zero Contracts Boosting U.S. Export-Grade Production

Large technology firms now commit to biomass supply agreements that outlast political cycles, anchoring several U.S. greenfield mills. Enviva’s Alabama complex will ship 1 million tons annually under such contracts when it enters service in 2025. These contracts embed stricter criteria than most government rules, covering carbon intensity, forest management, and shipping emissions. Producers benefit from indexed escalation tied to carbon prices, improving margins and derisking leverage. Financial partners, meanwhile, treat these offtakes as quasi-utility PPAs, lowering interest spreads for capacity expansions. As a result, private procurement is emerging as a stronger growth pillar than policy incentives, buffering the wood pellet market against regulatory volatility.

District-Heating Build-Out in Nordics Propelling Pellet Boiler Adoption

Northern Europe’s district-energy renaissance favors pellet-fired systems that couple heat and seasonal thermal storage. Denmark diversified wood-chip imports from North America in 2025 to secure low-moisture material for combined heat-and-cool plants [3]. Austria’s 75% capex subsidy program catalyzed 19,181 residential boiler installations in early 2024, reinforcing mass-market momentum. Sweden’s 100% fossil-free power goal by 2040 underpins investment in biomass plants that stabilize grids during wind lulls. This Nordic blueprint blends policy support, grid services, and high-grade fuel demand, offering producers a resilient channel that prioritizes quality and local air-emission compliance.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy Rollbacks in U.K./NL over Lifecycle-Emission Concerns | -0.7% | Europe, with policy spillover effects globally | Medium term (2-4 years) |

| Sustainable Feedstock Bottlenecks in U.S. Southeast | -1.1% | North America, affecting global export supply | Long term (≥ 4 years) |

| Competition from Palm-Kernel-Shell Biomass in ASEAN Power Mix | -0.4% | Asia-Pacific, primarily Japan and South Korea | Short term (≤ 2 years) |

| High-Interest-Rate Capex Burden for New Pellet Mills | -0.6% | Global, concentrated in capital-intensive regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Subsidy Rollbacks in U.K./NL Over Lifecycle-Emission Concerns

The United Kingdom’s Clean Power 2030 plan imposes tighter rules on large biomass plants, threatening a 2 million t annual import decline for the wood pellet market. The Netherlands is following with tougher feedstock restrictions that exclude certain forest residues, raising compliance costs. Academic studies questioning biomass carbon neutrality are gaining traction, fueling protest campaigns and political pressure across Europe that could reverberate into other consuming nations. Investors demand higher risk premiums for new capacity tied to EU utilities, nudging producers to diversify contract portfolios toward Asia and corporate buyers.

Sustainable Feedstock Bottlenecks in U.S. Southeast

Despite a large theoretical biomass supply, practical availability is tightening in the Southeast due to competing lumber demand and stricter harvest guidelines. Logistics now account for up to 30% of pellet cost as diesel prices and driver shortages pinch margins. Environmental NGOs are litigating harvest permits, prompting regulators to review clear-cutting practices. Climate-induced storms and droughts further reduce forest productivity, pushing mills to trial agricultural residues and energy crops that require new preprocessing lines. Until those alternatives scale, feedstock scarcity will cap expansion plans and could slow overall growth in the wood pellet market.

Segment Analysis

By Application: Power Generation Drives Industrial Transformation

Power generation’s share of the wood pellet market is expanding at a 7.22% CAGR through 2030. Utilities retrofit coal boilers for 5-20% co-firing ratios, avoiding capital-intensive replacements and cutting SO₂ and CO₂ emissions simultaneously. India’s Talwandi Sabo plant illustrates this trend, building a 500 t-per-day torrefaction facility that consumes agricultural stubble and trims daily coal use by 5%. Co-firing also anchors the business case for torrefied products that cost more but deliver higher calorific value and better grindability. Meanwhile, combined heat and power systems are gaining favor in pulp, food, and chemical complexes because they generate process heat while selling surplus electricity into deregulated markets.

Heating retains 60.4% of demand today, yet its growth moderates as legacy European installations mature. Nonetheless, district-energy networks continue to roll out high-efficiency condensing boilers that can accept premium residential pellets, lifting average selling prices. The interplay between these segments blurs as utilities test CHP-capable retrofits, creating a fluid opportunity set for producers that can tailor products to industrial and community energy schemes within the wood pellet market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-user: Commercial Sector Emerges as Growth Engine

Industrial and utility customers anchored 47.5% of 2024 revenue through multi-year, vessel-scale purchase agreements. These large buyers require consistent ISO-compliant products delivered to deep-water ports, favoring players with integrated port storage and loading assets. Conversely, commercial applications—retail chains, office parks, and educational campuses—are accelerating at 8% CAGR as developers roll out low-carbon building portfolios. Government incentives such as the U.S. 30% biomass tax credit permit each installation to receive up to USD 2,000 annually, narrowing the payback gap with natural-gas alternatives.

The residential niche is stable but competitive. Heat-pump adoption in Germany, France, and Italy limits new pellet boiler sales, yet existing homeowners still consume significant volumes for backup heat during winter price spikes. Animal bedding remains a specialized outlet that absorbs lower-grade pellets, supporting sawmill waste utilization without cannibalizing premium heating markets. Diversified buyer profiles insulate the wood pellet market from single-sector downturns and incentivize product segmentation by grade, ash content, and durability.

By Feedstock: Agricultural Residue Gains Momentum Amid Forest Constraints

Forest and wood residue supplied 57.5% of inputs in 2024, benefiting from mature collection networks and equipment. Yet, tight land-use regulations and competing sawlog demand are capping incremental growth. Agricultural residue, notably rice straw and corn stover, now advances at 7.25% CAGR, attracting policy support in India, where utilities must purchase 96,000 t daily for co-firing programs. Producers invest in torrefaction and pelletizing lines capable of handling higher silica and alkali contents without compromising boiler tubes to unlock this feedstock.

Emerging work on energy crops—miscanthus, switchgrass—promises consistent yields but needs multi-year planting cycles and contracts with growers. Sawdust blends still serve the mid-grade pellet segment, but rising construction lumber demand limits excess availability. The feedstock reshuffle, therefore, hinges on preprocessing innovation and logistics hubs that can seasonally stockpile agricultural residue, reducing moisture to below 12% for stable pellet quality. These adaptations safeguard raw-material security and expand product options within the wood pellet market.

By Grade: Torrefied Pellets Lead Premium Market Evolution

Utility-grade pellets captured 57.5% revenue during 2024 due to cost competitiveness in large-scale power plants. However, torrefied black pellets, processed at roughly 275 °C, grow at 9.25% CAGR because they handle like coal, resist water absorption, and cut milling power by half. Producers see margin upside as these pellets often sell at USD 30-40 t over standard industrial product, justifying higher capex for rotary kilns and inert-atmosphere reactors.

Premium residential-grade pellets, meanwhile, serve Nordic and Central European markets that mandate low ash and sulfur. Standard-grade sits in between, balancing price and performance for smaller commercial boilers. Segment stratification is deepening: utilities that retrofit coal assets increasingly demand torrefied grades, while district energy schemes favor premium A1 pellets that minimize particulate emissions. The evolving grade mix diversifies revenue and cushions the wood pellet market from price swings in any category.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

European consumption dominated with a 66.5% wood pellet market share in 2024, as the region produced 20.7 million t but burned 21.9 million t, relying on imports for 95% of power-plant feedstock [3]Bioenergy Europe, “Statistical Report Pellets 2024,” bioenergyeurope.org. War-related gas disruptions refocused policymakers on supply security, bolstering residential demand yet clouding industrial outlooks amid subsidy rollbacks. Brussels launched incentives for domestic capacity to mitigate exposure, including grants for small-scale pellet mills in drought-resilient Mediterranean forests.

North America remains the export backbone, supplying roughly three-quarters of U.K. imports in 2024, leveraging FSC-certified southern pine forests and rail-port networks. Canadian output benefits from beetle-killed pine salvage, although freight costs to Asian buyers rise with canal toll hikes. Currency exchange trends added volatility, pressuring Canadian margins when the USD weakens. Producers answer with debottlenecking projects and port partnerships to safeguard their foothold in the wood pellet market.

Asia-Pacific is the fastest-growing node, clocking 14.55% CAGR to 2030. Countries such as Japan, South Korea, and China rapidly expand imports to meet renewable energy targets, with supportive subsidies and feed-in-tariff schemes accelerating market uptake. Japan eyes 15 million t annual demand, and South Korea tweaks subsidies but still needs biomass for baseload balance. In other parts of the world, Brazil tapped eucalyptus plantations to ship 24,000 t to Denmark in September 2024. Investors backed Colombia’s Bioena plant to diversify sourcing for Dutch residential retailers. In the Middle East and Africa, pilot projects for cement kilns and off-grid power reveal nascent uptake, awaiting policy clarity and logistics improvements.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Market concentration is moderate. Enviva, Drax, and Graanul Invest control a sizeable slice through long-term contracts and vertically integrated forestry assets, yet new entrants in Vietnam, Brazil, and Malaysia trim their dominance. Drax’s 2021 acquisition of Pinnacle added Canadian output that pushes its total production above 4 million t, supporting co-firing at its U.K. power station. Graanul Invest’s 2024 Texas facility signals Baltic players’ global ambitions.

Technology is the new battleground. Torrefaction reactors, real-time moisture sensors, and blockchain traceability deliver tangible pricing premiums. NYK Line partnered with Drax to trial ammonia-ready, biomass-fueled bulk carriers, lowering well-to-wake emissions on trans-Atlantic routes [4]NYK Line, “Bulk Carrier Biofuel Trial Press Release,” nyk.com. Financial restructuring also reshapes competition: Enviva shed USD 1 billion of debt in February 2025, freeing capital for its eleventh Alabama mill that targets corporate clients. Smaller specialists differentiate via feedstock—rice-husk pellets in Indonesia—or by powering their plants with biomass-generated steam, shrinking lifecycle emissions.

The competitive web, therefore, hinges on cost, carbon intensity, and reliability. Buyers increasingly bundle fuel and carbon-credit attributes, rewarding firms demonstrating audited sequestration and ship-route emissions. As premium-grade penetration deepens and regional supply rises, incumbents need additional efficiency gains and strategic alliances to maintain influence within the wood pellet market.

Wood Pellet Industry Leaders

-

Enviva Inc.

-

Drax Group PLC

-

AS Graanul Invest

-

Lignetics Inc.

-

Segezha Group JSC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Drax Group posted record 4 million t pellet output for 2024 and signaled USD 250 million recurring EBITDA from biomass production after 2027.

- April 2025: India’s Talwandi Sabo Power commissioned a 500 t-day torrefied pellet plant using crop residue.

- December 2024: South Korea cut biomass renewable-credit rates for new projects, gradually phasing down incentives for existing plants.

- November 2024: Vietnam exported 5.3 million t of pellets during Jan-Nov 2024, on track for 5.8 million t for the year.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the wood pellet market as all revenues generated from the sale of densified biomass pellets manufactured from forestry residues, sawmill by-products, or purpose-grown energy crops and consumed for heating, power generation, or combined heat and power across residential, commercial, industrial, and utility settings worldwide.

Scope exclusion: pellets produced purely for animal bedding or barbecue applications are not counted.

Segmentation Overview

- By Application

- Heating

- Power Generation

- Combined Heat and Power (CHP)

- By End-user

- Residential

- Commercial

- Industrial and Utility

- Animal Bedding

- By Feedstock

- Forest/Wood Residue

- Agricultural Residue

- Energy-Crop and Sawdust Mix

- By Grade

- Utility-Grade (White)

- Premium-Grade

- Standard-Grade

- Torrefied “Black” Pellets

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- Nordic Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview pellet producers, traders, power plant fuel managers, boiler OEMs, and regional bioenergy associations across Europe, North America, and Asia-Pacific. Insights on spot pricing spreads, feedstock cost inflation, and plant utilization rates validate desk estimates and close data gaps identified in early drafts.

Desk Research

We begin by mapping supply and demand fundamentals through open datasets such as FAO forestry statistics, Eurostat trade flows, U.S. EIA biomass inventories, and Bioenergy Europe capacity reports. Policy documents, including EU RED III, Japan FIT tariffs, and U.S. Renewable Heat Incentive updates, clarify regulatory drivers. Company filings and investor decks reveal contract volumes and average selling prices. When regional volumes are unclear, paid repositories like D&B Hoovers and Dow Jones Factiva help triangulate producer shipments. This list is illustrative; many further public and subscription sources inform our desk work.

Market-Sizing and Forecasting

A top-down reconstruction starts with national production, import, and inventory balances, which are then reconciled with consumption by end use. Select bottom-up checks, sampled mill output, distributor channel checks, and premium-grade ASP times export volume calibrate totals. Key variables include residential heating degree days, announced coal-to-biomass retrofit capacity, certified sustainable forest residue availability, average industrial pellet price, and shipping costs to Europe and Northeast Asia. Multivariate regression links these drivers to historical revenue, while scenario analysis stresses policy or weather shocks before extending forecasts to 2030.

Data Validation and Update Cycle

Every draft undergoes anomaly checks versus independent indicators, followed by analyst peer review. We refresh models annually and issue interim updates whenever material events, such as policy shifts, large-scale plant outages, or significant currency swings, alter market trajectories.

Why Our Wood Pellet Baseline Commands Reliability

Published figures often diverge because firms choose different feedstock boundaries, price assumptions, and refresh rhythms.

Key gap drivers arise when other studies merge animal-bedding grades, rely on single-region ASPs, or freeze policy scenarios for multiple years, whereas Mordor updates tariffs and exchange rates each cycle and keeps non-energy pellet demand outside the core scope.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.72 bn (2025) | Mordor Intelligence | - |

| USD 19.48 bn (2024) | Global Consultancy A | Includes barbecue and bedding pellets; uses uniform global price |

| USD 13.60 bn (2024) | Industry Journal B | Applies aggressive 16 percent CAGR without recent policy moderation |

| USD 9.32 bn (2024) | Regional Consultancy C | Excludes Asia-Pacific industrial demand and counts only heating use |

Taken together, the comparison shows that Mordor's disciplined scope, live policy tracking, and dual validation steps deliver a balanced, transparent baseline that decision-makers can retrace and update with confidence.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the wood pellet market?

The wood pellet market stands at USD 12.72 billion in 2025 and is projected to reach USD 17.95 billion by 2030 on a 7.13% CAGR.

Which region leads consumption of wood pellets?

Europe dominates with 66.5% of global demand in 2024, though its growth rate is slowing due to subsidy revisions and stricter sustainability rules.

Why are torrefied pellets gaining popularity?

Torrefied pellets offer higher energy density, better moisture resistance, and can be co-milled with coal, making them ideal for retrofitting existing power plants; they are growing at a 9.25% CAGR.

How are corporate net-zero goals influencing the wood pellet industry?

Tech majors and other corporates now sign long-term biomass supply contracts that exceed regulatory sustainability standards, giving producers price stability and funding for capacity expansion.

What are the main challenges facing pellet producers in the U.S. Southeast?

Feedstock competition, higher logistics costs, and environmental scrutiny are tightening sustainable wood supply, potentially slowing new capacity additions.

Which end-user segment is expanding fastest?

Commercial users—especially district-heating networks and corporate campuses—are the fastest-growing, advancing at an 8% CAGR through 2030 as they deploy pellet boilers to meet decarbonization targets.

Page last updated on: