| Study Period | 2019 - 2030 |

| Market Volume (2025) | 3.42 Million tons |

| Market Volume (2030) | 4.07 Million tons |

| CAGR | 3.54 % |

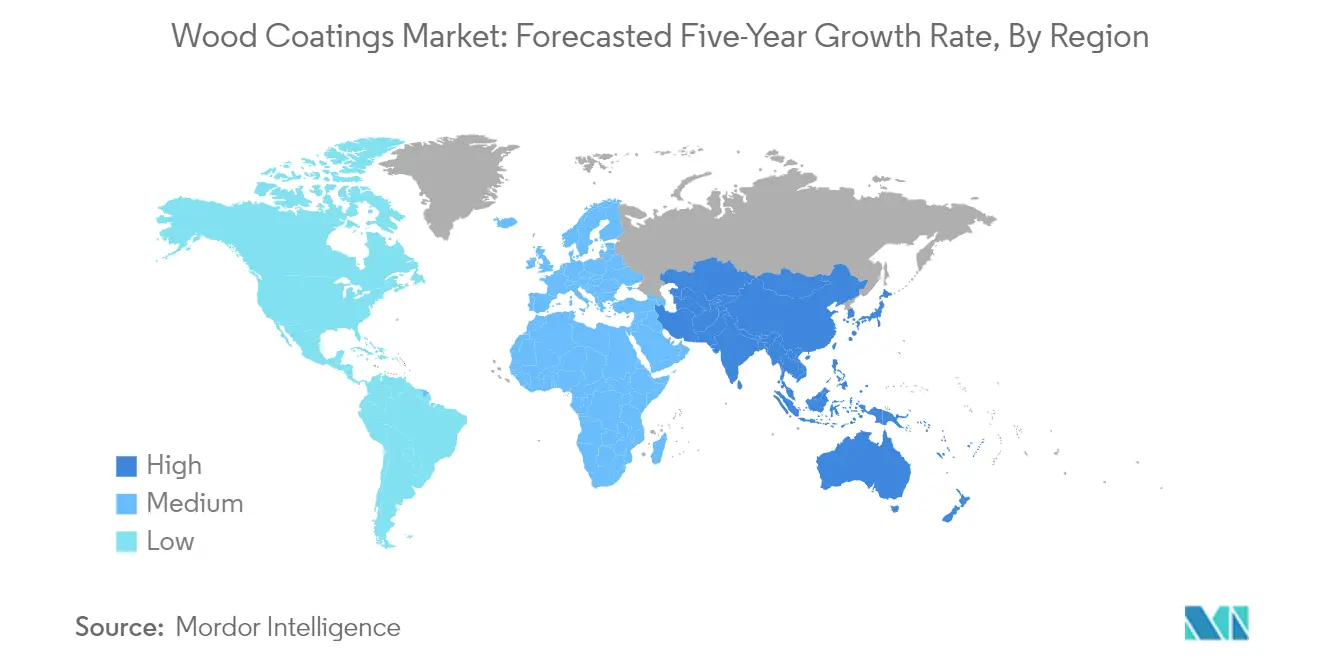

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

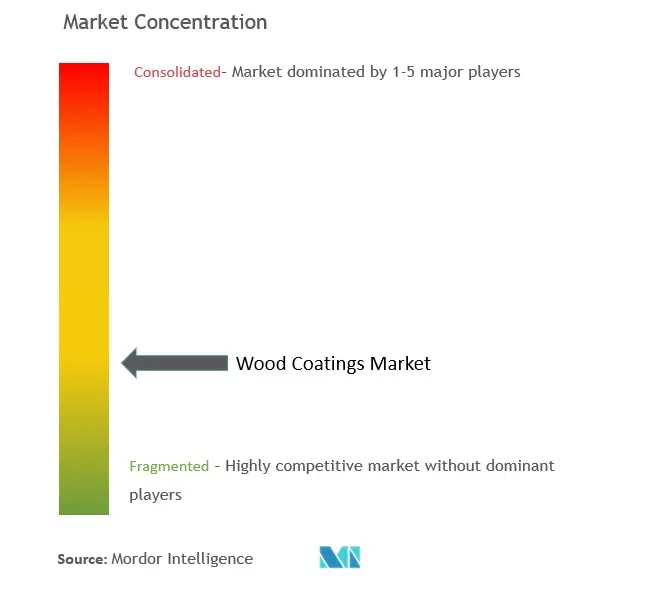

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Wood Coatings Market Analysis

The Wood Coatings Market size is estimated at 3.42 million tons in 2025, and is expected to reach 4.07 million tons by 2030, at a CAGR of greater than 3.54% during the forecast period (2025-2030).

The wood coatings industry is experiencing a significant shift toward sustainable and environmentally conscious solutions, driven by evolving regulatory frameworks and changing consumer preferences. Manufacturers are increasingly focusing on developing low-VOC and HAPs-free formulations to meet stringent environmental standards. The industry has witnessed a notable transition toward water-based and UV-cured coating technologies, which offer improved environmental performance while maintaining high-quality finishes. This transformation is particularly evident in the European market, where the furniture coatings sector sales grew by 22.2% in 2022 according to the FederlegnoArredo Study Center, despite the challenging regulatory environment.

The global wood coatings landscape is being reshaped by technological advancements and innovative application methods. UV-curable technologies are gaining prominence due to their fast curing times, reduced energy consumption, and superior performance characteristics. These advanced coating systems offer enhanced durability, scratch resistance, and chemical resistance while enabling manufacturers to achieve higher production efficiencies. The integration of smart coating technologies and automated application systems is revolutionizing the manufacturing process, leading to improved consistency and quality control in coating applications.

Consumer preferences are increasingly gravitating toward customized finishes and sustainable products, driving innovation in wood finishing products. The market is witnessing a growing demand for coatings that can provide unique aesthetic effects while maintaining environmental compliance. This trend is reflected in the success of major industry players, as evidenced by IKEA Group's performance in Korea, where it generated approximately USD 444 million in sales between September 2021 and August 2022. Manufacturers are responding by developing new color systems and finish options that cater to these evolving preferences while maintaining high performance standards.

The industry is experiencing significant supply chain transformations and manufacturing innovations to enhance operational efficiency and market responsiveness. Companies are investing in vertical integration and localized production capabilities to ensure supply chain resilience and reduce transportation costs. This trend is particularly notable in India, where furniture exports witnessed remarkable growth, increasing by over 220% from USD 810 million in 2018-19 to USD 2.6 billion in 2022-23. Manufacturers are also adopting advanced production technologies and automation solutions to improve product consistency and reduce waste, while simultaneously addressing labor challenges and increasing production efficiency. The adoption of wood protective coatings is also contributing to these advancements, ensuring longevity and durability in finished products.

Wood Coatings Market Trends

Increasing Furniture Production

The global demand for wood coatings is experiencing significant growth driven by expanding housing construction, population growth, and rising disposable incomes worldwide. The increased demand for furniture items such as chairs, tables, beds, sofas, shelves, and cupboards has become a key driver for market expansion. This trend is particularly evident in major markets where furniture production continues to rise to meet consumer demands. For instance, in China, there were 5,899 furniture stores as of 2022, showing a 0.1% increase from 2021, while retail furniture sales reached CNY 47.69 billion during the first four months of 2023. Major furniture manufacturers are also expanding their operations, with IKEA announcing its largest-ever investment in the American market in 2023 through the opening of eight new shops and expansion of its fulfillment network across its existing 51 stores in the United States.

The furniture industry is witnessing significant investments and expansions across various regions. In January 2022, WoodenStreet, a furniture startup, announced an investment of INR 50 crore to double its on-ground presence from 45 to 100 stores, while also introducing new products such as smart office furniture and modular kitchen solutions. The United States, which boasts the world's largest furniture market, recorded furniture and home furnishing store sales of approximately USD 141,261 million in 2022, representing an increase from 2021's sales of USD 140,586 million. The continuous evolution of interior design concepts for homes, offices, and apartments within the furniture industry is driving innovation and development, particularly in terms of designs, sizes, and colors, further stimulating the demand for wood paint and wood stain in furniture production.

Understand The Key Trends Shaping This Market

Download PDF

Growing Construction Industry in Asia-Pacific and Middle East & Africa

The construction industry across Asia-Pacific and the Middle East & Africa regions is witnessing substantial growth, creating increased demand for wooden products and consequently wood coatings. In Japan, the construction sector is projected to expand moderately over the next five years, driven by increasing investments in public and private infrastructure and commercial projects. According to Japan's Cabinet Office forecasts, the construction sector's GDP contribution is expected to reach JPY 30,973 billion in 2023 and JPY 31,500 billion in 2024. The region is also experiencing a boom in luxury residential projects, exemplified by Mitsubishi State's ongoing construction of Japan's tallest building, which will feature 50 luxury apartments generating monthly rents of USD 43,000 each, scheduled for completion by 2027.

The construction sector's growth is further supported by government initiatives and real estate development projects across the regions. In India, the real estate market is projected to reach USD 1 trillion by 2030, up from USD 200 billion in 2021, indicating substantial growth potential for home interior products and furniture. The Indian government has demonstrated its commitment to infrastructure development through initiatives such as the 'PM Aawas Yojana' scheme, allocating INR 48,000 crores in its Union Budget 2022-23 for the construction of 80,00,000 affordable homes for urban and rural populations. This extensive construction activity across residential, commercial, and infrastructure sectors is driving the demand for wooden products such as doors, windows, cabinets, and furniture, consequently boosting the wood coatings market in these regions. The demand for wood varnish and wood finish is also increasing, contributing to the growth of the wood coatings market.

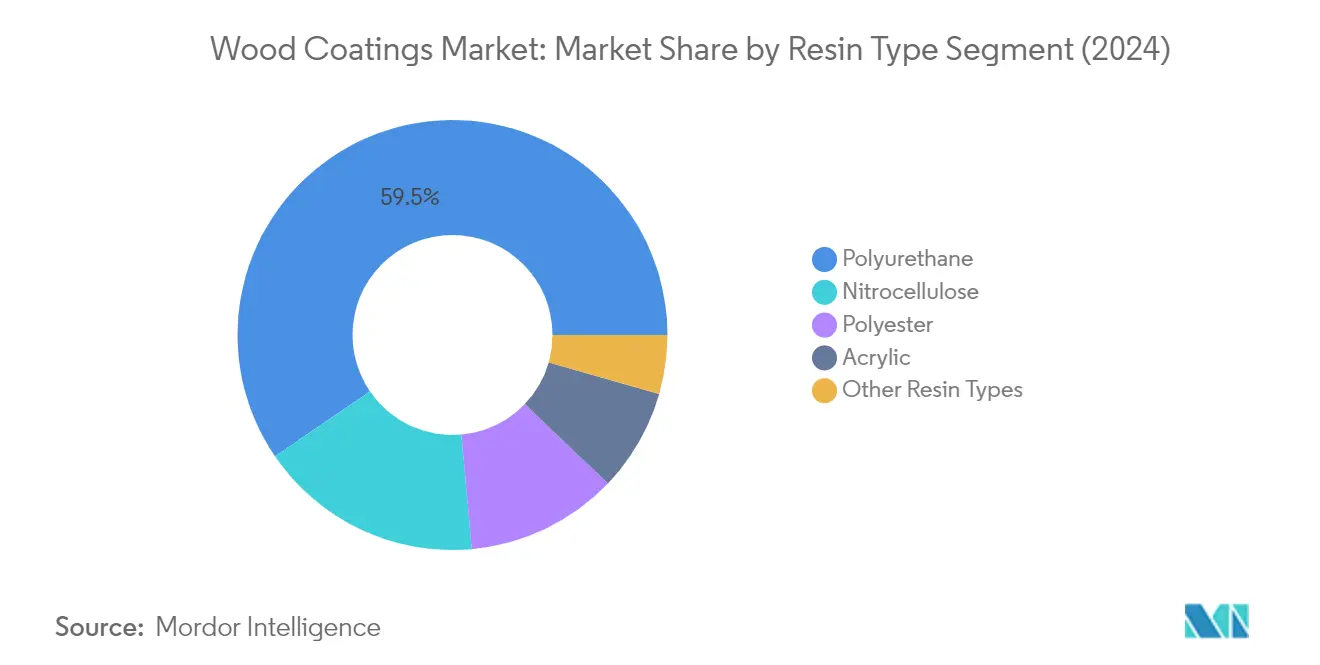

Segment Analysis: Resin Type

Polyurethane Segment in Wood Coatings Market

Polyurethane resin dominates the global wood coatings market, commanding approximately 60% of the market share in 2024. This significant market position is attributed to its exceptional versatility and superior performance characteristics in various wooden applications, particularly in furniture and fixtures. Polyurethane-based wood coatings are extensively preferred due to their outstanding durability, excellent chemical resistance, and superior protection against moisture and mechanical stress. These coatings are particularly suitable for wooden furniture subjected to rough usage, such as doors, windows, and counters, where they demonstrate remarkable resistance to moisture and provide strong chemical resistance against salt-laden air, making them ideal for furniture in coastal areas. The segment's dominance is further strengthened by its ability to form insoluble, extremely durable coating films when applied on wood, offering very good surface hardness and chemical resistance. Additionally, polyurethane is a key component in wood protective coatings, enhancing the longevity and aesthetic appeal of wooden surfaces.

Growth Trajectory of Polyurethane Segment

The polyurethane segment is projected to maintain its growth leadership in the wood coatings market during 2024-2029, with an expected growth rate of approximately 4%. This accelerated growth is driven by increasing adoption in high-end furniture applications and growing demand from the construction sector, particularly in the Asia-Pacific and Middle East regions. The segment's growth is further supported by technological advancements in polyurethane formulations, leading to enhanced performance characteristics and environmental compliance. Water-based polyurethane coatings are gaining significant traction due to their low VOC levels, minimal odor emissions, and quick-drying properties, while solvent-based polyurethane coatings continue to be preferred in applications requiring superior durability and faster drying times. These advancements are crucial in the development of wood floor coatings, which demand high durability and aesthetic appeal.

Remaining Segments in Resin Type

The wood coatings market encompasses several other significant resin types, including nitrocellulose, polyester, acrylic, and other specialized resins. Nitrocellulose coatings are particularly valued for their quick-drying properties and excellent polishing characteristics, making them ideal for furniture renovation and coating replicas. Polyester resins are preferred for their high filling power and shrinkage resistance, particularly in closed-pore topcoat applications. Acrylic resins have gained prominence due to their excellent resistance to weathering and UV radiation, making them suitable for exterior applications. Each of these segments serves specific market niches and contributes to the overall diversity of wood coating solutions available to manufacturers and end-users, including wood lacquer and wood sealers, which are essential for achieving desired finishes and protection levels.

Segment Analysis: Technology

Solvent-borne Segment in Wood Coatings Market

The solvent-borne coatings segment continues to dominate the global wood coatings market, holding approximately 67% market share in 2024. This significant market position is attributed to several key advantages these coatings offer, particularly in kitchen cabinet and furniture manufacturing where they are preferred for their fast-drying properties, easy repairability, and excellent ability to withstand climate fluctuations. Solvent-borne coatings encompass three main types widely used in wood applications: nitrocellulose lacquers primarily used in residential furniture, pre-catalyzed lacquers utilized in office and institutional furniture, and conversion varnishes commonly applied in kitchen cabinets. These coatings provide superior performance characteristics including excellent durability, high clarity, and exceptional resistance to various environmental factors, making them the preferred choice for many manufacturers despite their higher VOC content.

Water-borne Segment in Wood Coatings Market

The water-borne coatings segment is projected to experience the highest growth rate of approximately 4% during the forecast period 2024-2029, driven by increasing environmental regulations and growing consumer awareness about VOC emissions. These coatings are gaining significant traction in the market due to their eco-friendly nature and versatile properties, particularly in kitchen cabinets and furniture production where they demonstrate excellent resistance and mechanical capabilities. The segment's growth is further supported by the ongoing shift from solvent-based to water-based formulations, especially in regions with strict environmental regulations. Water-borne coatings offer additional advantages such as high elasticity, allowing the paint film to move with the wood without degradation, and thixotropic properties that enable thicker substance application while maintaining high relaxation and transparency levels. These properties are particularly beneficial for interior wood coatings, which require a balance of durability and aesthetic appeal.

Remaining Segments in Technology

The UV-cured and powder coatings segments complete the technology landscape in the wood coatings market, each offering unique advantages for specific applications. UV-cured coatings are particularly valued for their rapid curing speed, lower energy costs, and reduced atmospheric pollution, making them increasingly popular in high-volume door and panel finishing operations. Meanwhile, powder coatings, though representing a smaller market share, provide significant environmental benefits through their zero-VOC formulations and ability to be recycled, making them particularly suitable for heat-sensitive wood and wood composites in applications such as office furniture and cabinetry. Both segments continue to evolve with technological advancements, offering improved performance characteristics and environmental benefits. These advancements are crucial for developing exterior wood coatings, which must withstand harsh environmental conditions.

Segment Analysis: Application

Furniture and Fixtures Segment in Wood Coatings Market

The Furniture and Fixtures segment dominates the global wood coatings market, commanding approximately 69% of the total market share in 2024. This segment's prominence is primarily driven by the increasing demand for wooden furniture across residential and commercial sectors worldwide. The segment's growth is further bolstered by continuous innovations in interior design concepts for homes, offices, and hotels, which drives development in furniture designs, sizes, and colors. The rise in remote working opportunities has significantly increased the demand for office furniture, particularly in the Asia-Pacific region. The furniture market has been experiencing robust growth in emerging economies, with countries like India witnessing substantial expansion in their furniture industry. The segment's strong performance is also attributed to the growing middle-class population, combined with increased desire for home décor and furniture, supporting the demand for wooden chairs, tables, beds, sofas, shelves, and other items. Additionally, the segment benefits from the increasing trend of furniture customization and the growing preference for sustainable and eco-friendly furniture pieces, which require high-quality wood finish for protection and aesthetics.

Remaining Segments in Application Market

The wood coatings market encompasses several other significant application segments, including Doors and Windows, Cabinets, and Other Applications. The Doors and Windows segment plays a crucial role in both residential and commercial construction sectors, where wood coatings are essential for protecting these structures from weathering degradation and enhancing their aesthetic appeal. The Cabinets segment serves various applications, particularly in kitchen areas, beneath stairs, below windows, and other spaces where storage solutions are needed. These applications require specialized coatings that offer superior resistance to scratches, abrasion, and chemicals, especially in kitchen environments. The Other Applications segment includes diverse uses such as floors, decks, and molding products, where wood coatings provide essential protection against wear, mold, fungi, bacteria, and other environmental damages while maintaining the natural beauty of the wood. These applications often utilize wood sealers to enhance durability and longevity.

Wood Coatings Market Geography Segment Analysis

Wood Coatings Market in Asia-Pacific

The Asia-Pacific region represents the largest wood coatings market globally, driven by robust growth in construction activities and furniture manufacturing. Countries like China, India, Japan, and South Korea are key contributors to the regional wood coatings market, with significant investments in residential and commercial construction projects. The region's expanding middle class, rapid urbanization, and growing disposable incomes have led to increased demand for wooden furniture and fixtures, thereby driving the wood coatings industry.

Wood Coatings Market in China

China dominates the Asia-Pacific wood coatings market as the largest consumer, holding approximately 71% of the regional wood coatings market share. The country's construction sector is the largest globally, with significant investments in infrastructure and residential projects. The Chinese furniture market continues to expand, supported by major players like IKEA Group and domestic manufacturers. The government's focus on boosting investments across the construction sector and various infrastructure initiatives has created substantial demand for wood coatings in applications ranging from furniture to architectural woodwork.

Wood Coatings Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 4% during 2024-2029. The country's wood coatings market is experiencing rapid expansion driven by increasing investments in residential and commercial sectors, along with strategic government initiatives. The Indian furniture market's robust growth, coupled with the entry of international players and expansion of domestic manufacturers, has created significant opportunities. The government's focus on affordable housing schemes and infrastructure development continues to drive demand for wood coatings across various applications.

Wood Coatings Market in North America

The North American wood coatings market demonstrates strong growth potential, supported by robust construction activities and renovation projects across the United States, Canada, and Mexico. The region's market is characterized by high adoption of innovative coating technologies and an increasing focus on environmentally friendly products. The presence of major manufacturers and well-established distribution networks further strengthens the market dynamics.

Wood Coatings Market in United States

The United States leads the North American market, commanding approximately 62% of the regional wood coatings market share. The country's large construction sector, employing over 7.6 million workers, drives significant demand for wood coatings. The robust residential construction activity, coupled with extensive home renovation projects and a strong furniture manufacturing base, continues to fuel market growth. The presence of major office furniture manufacturing companies and increasing commercial construction projects further solidifies the country's dominant position.

Wood Coatings Market in United States - Growth Trends

As the fastest-growing market in North America, the United States is projected to expand at a rate of approximately 3% during 2024-2029. The growth is driven by increasing construction spending, particularly in residential and commercial sectors. The country's focus on sustainable building practices and growing demand for high-performance wood coatings in various applications continues to create new opportunities. The trend toward home renovation and remodeling, supported by various government initiatives and loans, further strengthens market growth prospects.

Wood Coatings Market in Europe

The European wood coatings market showcases strong development, supported by technological advancements and increasing demand for eco-friendly coating solutions. The region benefits from a well-established furniture manufacturing industry and stringent quality standards. Germany leads the market with its robust industrial base and strong construction sector, while Italy demonstrates the highest growth potential among European countries. The market is characterized by increasing adoption of innovative coating technologies and a growing focus on sustainable products.

Wood Coatings Market in Germany

Germany maintains its position as the largest market for wood coatings in Europe, supported by its position as the largest construction industry in the region. The country's strong focus on residential construction activities and increasing commercial projects drives substantial demand for wood coatings. The remarkable rise in the residential sector, attributed to growing public expenditure on housing and government initiatives for speeding up construction of residential units, continues to fuel market growth.

Wood Coatings Market in Italy

Italy emerges as the fastest-growing market in Europe, driven by its well-established furniture manufacturing industry and growing construction activities. The country's renowned position in high-quality furniture manufacturing creates substantial demand for furniture coatings. Despite economic challenges, the furniture sector's strong performance and growing export activities continue to drive market growth, particularly in premium wood coatings segments.

Wood Coatings Market in South America

The South American wood coatings market demonstrates steady growth potential, with Brazil, Argentina, and other countries contributing to regional development. Brazil emerges as both the largest and fastest-growing market in the region, supported by its extensive furniture industry and construction sector. The region's market is characterized by increasing investments in residential construction and growing demand for wooden furniture and fixtures.

Wood Coatings Market in Middle East & Africa

The Middle East & Africa wood coatings market shows promising growth prospects, driven by increasing construction activities and growing furniture demand. Saudi Arabia leads the regional market, while South Africa demonstrates significant growth potential. The region's market benefits from large-scale construction projects, particularly in Saudi Arabia, and increasing investments in residential and commercial developments across various countries.

Get Analysis on Important Geographic Markets

Download PDF

Wood Coatings Industry Segmentation

Top Companies in Wood Coatings Market

The global wood coatings market features prominent wood coating companies like The Sherwin-Williams Company, PPG Industries, AkzoNobel, RPM International, and Asian Paints leading the industry through continuous innovation and strategic expansion. Companies are increasingly focusing on developing environmentally sustainable coating technologies, particularly low-VOC and water-based formulations, to meet evolving regulatory requirements and consumer preferences. The industry witnesses regular product launches targeting specific applications like furniture, flooring, and architectural woodwork, while manufacturers are strengthening their distribution networks through both traditional and digital channels. Major players are expanding their geographical presence through strategic acquisitions and partnerships, particularly in emerging markets across the Asia-Pacific and Middle East regions. Research and development investments are primarily directed towards improving coating performance characteristics, durability, and aesthetic appeal while reducing environmental impact.

Fragmented Market with Strong Regional Players

The wood coatings market exhibits a partially fragmented structure, with the top five players accounting for approximately one-third of the global production volumes, while the top ten manufacturers represent about forty percent of the market share. The competitive landscape is characterized by a mix of global conglomerates offering comprehensive coating solutions and regional specialists focusing on specific market segments or geographical areas. The market structure encourages healthy competition while maintaining sufficient room for regional players to establish a strong local presence through specialized product offerings and intimate customer relationships.

The industry has witnessed significant consolidation through mergers and acquisitions, exemplified by Sherwin-Williams' acquisition of ICA Group and AkzoNobel's purchase of Kansai Paint's African operations. These strategic moves are driven by the desire to expand product portfolios, enhance manufacturing capabilities, and strengthen regional market positions. Companies are increasingly focusing on vertical integration strategies, with some major players producing their own raw materials like resins and solvents to better control supply chains and maintain competitive advantages in terms of cost and quality control.

Innovation and Sustainability Drive Future Success

Success in the wood coatings industry increasingly depends on companies' ability to balance environmental compliance with performance requirements while maintaining cost competitiveness. Market leaders are investing in research and development to create innovative solutions that address both regulatory requirements and customer demands for improved functionality. Companies are also strengthening their position through enhanced technical support services, custom formulation capabilities, and integrated solutions that help customers optimize their coating processes and reduce overall operational costs.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized products or focusing on specific geographical regions where they can build strong customer relationships. The industry's future will be shaped by factors such as increasing environmental regulations, growing demand for sustainable products, and the need for improved coating performance characteristics. Companies that can effectively navigate these challenges while maintaining operational efficiency and customer focus will be better positioned to capture market opportunities and maintain competitive advantages in the evolving marketplace.

Wood Coatings Market Leaders

-

The Sherwin-Williams Company

-

Akzo Nobel N.V.

-

PPG Industries, Inc.

-

RPM International Inc.

-

Asian Paints

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Wood Coatings Market News

- April 2024: Axalta Building Products, a division of the globally renowned Axalta Coating Systems, unveiled its innovative Zenamel range of wood coating solutions tailored for cabinet manufacturers. With this launch, Axalta Building Products seeks to empower its wood finishing industry clients to create top-tier, sustainable, eco-friendly products that align with tightening regulatory standards and evolving consumer preferences.

- April 2023: Benjamin Moore & Co. unveiled Element Guard, a new exterior paint tailored for diverse substrates, wood included. With the launch of Element Guard, Benjamin Moore & Co. seeks to empower painting professionals, ensuring its exterior projects endure the elements and satisfy client expectations.

- January 2023: Asian Paints planned to invest in a new manufacturing facility dedicated to water-borne paints, boasting an annual capacity of 4 lakh kl. This facility will also produce water-borne wood coatings, with operations slated to begin in 2026. Through this expansion, Asian Paints seeks to bolster its production capacity, aligning with the projected surge in demand for water-borne wood coatings in India.

- December 2022: Sherwin-Williams Company announced the successful completion of its acquisition of the ICA Group. By acquiring the ICA Group, Sherwin-Williams aimed to create a more diversified and competitive wood coatings company with a stronger presence in the European market and a broader range of products and technologies to offer its customers.

Wood Coatings Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Increasing Furniture Production

- 4.1.2 Escalating Demand for Interior Design and Decoration

- 4.1.3 Other Drivers

-

4.2 Restraints

- 4.2.1 Stringent Environmental Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Nitrocellulose

- 5.1.3 Polyester

- 5.1.4 Polyurethane

- 5.1.5 Other Resin Types

-

5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solven-borne

- 5.2.3 UV-cured

- 5.2.4 Powder Coatings

-

5.3 By Application

- 5.3.1 Furniture and Fixtures

- 5.3.2 Doors and Windows

- 5.3.3 Cabinets

- 5.3.4 Other Applications (including Floors, Decks, and Molding Products)

-

5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Akzo Nobel NV

- 6.4.2 Asian Paints

- 6.4.3 Axalta Coating Systems

- 6.4.4 Benjamin Moore & Co.

- 6.4.5 Ceramic Industrial Coatings

- 6.4.6 Hempel AS

- 6.4.7 Jotun

- 6.4.8 Kansai Paint Co. Ltd

- 6.4.9 KAPCI Coating

- 6.4.10 MAS Paints

- 6.4.11 National Paints Factories Co. Ltd

- 6.4.12 Nippon Paint Holdings Co. Ltd

- 6.4.13 PPG Industries Inc.

- 6.4.14 Ritver

- 6.4.15 RPM International Inc.

- 6.4.16 Teknos Group

- 6.4.17 Sherwin-Williams Company

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for UV-cured Coatings

- 7.2 Other Opportunities

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Wood Coatings Industry Segmentation

Wood coatings are applied to wood surfaces to protect, enhance, and decorate them. They can be used on various wood products, including furniture, flooring, and cabinets.

The wood coatings market is segmented based on resin type, technology, application, and geography. By resin type, the market is segmented into acrylic, nitrocellulose, polyester, polyurethane, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, UV-cured, and powder coatings. By application, the market is segmented into furniture and fixtures, doors and windows, cabinets, and other applications. The report also covers the market size and forecasts for the wood coatings market in 27 countries across major regions. For each segment, the market sizing and forecasts are provided in terms of volume in kilotons.

| By Resin Type | Acrylic | ||

| Nitrocellulose | |||

| Polyester | |||

| Polyurethane | |||

| Other Resin Types | |||

| By Technology | Water-borne | ||

| Solven-borne | |||

| UV-cured | |||

| Powder Coatings | |||

| By Application | Furniture and Fixtures | ||

| Doors and Windows | |||

| Cabinets | |||

| Other Applications (including Floors, Decks, and Molding Products) | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Thailand | |||

| Indonesia | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| NORDIC Countries | |||

| Turkey | |||

| Russia | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| Qatar | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Wood Coatings Market Research FAQs

How big is the Wood Coatings Market?

The Wood Coatings Market size is expected to reach 3.42 million tons in 2025 and grow at a CAGR of greater than 3.54% to reach 4.07 million tons by 2030.

What is the current Wood Coatings Market size?

In 2025, the Wood Coatings Market size is expected to reach 3.42 million tons.

Who are the key players in Wood Coatings Market?

The Sherwin-Williams Company, Akzo Nobel N.V., PPG Industries, Inc., RPM International Inc. and Asian Paints are the major companies operating in the Wood Coatings Market.

Which is the fastest growing region in Wood Coatings Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Wood Coatings Market?

In 2025, the Asia Pacific accounts for the largest market share in Wood Coatings Market.

What years does this Wood Coatings Market cover, and what was the market size in 2024?

In 2024, the Wood Coatings Market size was estimated at 3.30 million tons. The report covers the Wood Coatings Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Wood Coatings Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Wood Coatings Market Research

Mordor Intelligence provides a comprehensive analysis of the wood coatings industry. We leverage our extensive experience in market research and consulting. Our latest report examines the dynamic market for timber coatings. It encompasses various segments, including wood stain, wood paint, wood varnish, and wood lacquer products. The analysis covers crucial segments such as furniture coatings, wood floor coatings, and wood protective coatings. Detailed insights are available in an easy-to-download report PDF format.

Our research benefits stakeholders across the value chain. This includes manufacturers of wood finishing products and suppliers of wood sealers and exterior wood coatings. The report thoroughly examines interior wood coatings applications and the industrial wood coatings market. It also analyzes the wood preservative coatings market. Stakeholders gain access to detailed analysis of wood deck coatings trends and market dynamics. This is supported by our expert consultation services. The comprehensive coverage includes both current market assessment and future growth projections. It is an essential tool for strategic decision-making in the wood coatings industry.