| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 9.23 Billion |

| Market Size (2030) | USD 13.79 Billion |

| CAGR (2025 - 2030) | 8.36 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Wireless Connectivity Chipset Market Analysis

The Wireless Connectivity Chipset Market size is estimated at USD 9.23 billion in 2025, and is expected to reach USD 13.79 billion by 2030, at a CAGR of 8.36% during the forecast period (2025-2030).

The wireless connectivity chipset industry is experiencing transformative changes driven by rapid technological advancement and evolving consumer demands. The emergence of next-generation wireless technologies, particularly the transition from 5G to 6G, is reshaping the market landscape. According to GSMA, 5G networks are expected to cover one-third of the world's population by 2025, while countries like China are already laying the groundwork for 6G through initiatives like the IMT-2030 (6G) Promotion Group. This technological progression is creating new opportunities for chipset manufacturers to develop more sophisticated and efficient solutions that can support advanced wireless communications.

The integration of artificial intelligence and enhanced processing capabilities in wireless chipsets is becoming increasingly prevalent, as evidenced by recent industry developments. In May 2024, MediaTek's launch of the Kompanio 838 SoC for premium Chromebooks and the Pentonic 800 SoC for 4K premium smart TVs demonstrates the industry's push toward more powerful and versatile chipset solutions. These advancements are enabling manufacturers to address the growing demand for high-performance computing and connectivity in various consumer electronics applications, while simultaneously improving energy efficiency and reducing form factors. The introduction of Wi-Fi chipsets in these devices highlights the industry's focus on enhancing connectivity.

The market is witnessing a significant shift toward more sophisticated wireless connectivity solutions driven by the proliferation of mobile devices and digital transformation. According to We Are Social, global mobile users reached 5.34 billion by the start of Q3 2022, highlighting the massive scale of potential applications for wireless connectivity chipsets. This trend is complemented by MediaTek's November 2023 launch of the Filogic 860 and Filogic 360 chipsets, which are specifically designed to support next-generation Wi-Fi 7 connectivity across enterprise access points, service provider gateways, and consumer electronics. These Wi-Fi chipsets are crucial for meeting the demands of modern connectivity needs.

The industry is experiencing substantial growth in computer and smart device adoption, creating new opportunities for wireless chipset manufacturers. The OECD survey projects that the number of households with computers will reach 1,262.47 million by 2025, indicating a robust demand for wireless connectivity solutions. However, the market faces challenges related to cybersecurity concerns, as the increasing number of connected devices expands the potential attack surface for networks. This has led manufacturers to focus on developing more secure chipset solutions with enhanced protection features, while also addressing the high costs associated with advanced Wi-Fi chipset development and production. The inclusion of Bluetooth chipsets and wireless modules in these solutions further enhances device interoperability and connectivity.

Wireless Connectivity Chipset Market Trends

INCREASED DEMAND FOR CONNECTED HOMES THROUGH HOME AUTOMATION

The growing penetration of high-speed internet has significantly accelerated the adoption of connected devices and smart home applications, particularly focusing on voice assistants, smart thermostats, smart lighting, security cameras, and smart appliances. Products like Amazon Echo and Google Home have become central hubs for smart home gadgets, with their voice-activated assistants offering unprecedented convenience in home automation. The integration of these devices has created a robust ecosystem where automated HVAC control systems, smart thermostats, and security solutions like August Smart Lock are becoming standard features in modern homes, driving the demand for wireless modules and Bluetooth chipsets solutions that enable seamless communication between these devices.

Smart appliances are increasingly incorporating connected solutions that enhance user experience and operational efficiency. For instance, smart LG refrigerators now allow users to pre-order ice and check expiration dates on products, helping consumers optimize their shopping lists through wireless connectivity. The lighting solution segment has also witnessed significant innovation, with companies like Lifx Color 1000 and Phillips Hue Wireless Dimming Kit offering smart bulbs that can be controlled via smartphones and voice assistants. The Matter standard, scheduled for implementation, promises to ensure interoperability between smart home devices from different manufacturers, further driving the adoption of connected home solutions and consequently increasing the demand for WiFi chipset technology.

Understand The Key Trends Shaping This Market

Download PDF

INCREASING INTERNET PENETRATION INTO HOMES AND ENTERPRISES

According to the International Telecommunication Union, internet penetration has reached unprecedented levels with approximately 5.4 billion users worldwide in 2023, representing 67% of the global population. This massive increase in internet adoption has created a substantial demand for wireless communication IC solutions across homes and enterprises. The evolution of Wi-Fi network technology has enabled users to experience faster speeds and lower latency, prompting the rapidly increasing use of data-heavy services and applications. The significant rise in data volume carried by Wi-Fi networks has been primarily driven by consumer demand for video streaming, cloud services, and emerging technologies like augmented reality.

The deployment of advanced wireless infrastructure continues to accelerate, with countries making significant investments in connectivity solutions. For instance, in Japan, the government has granted permission to install 5G base stations on 208,000 traffic lights nationwide, with local administrations and operators sharing the costs to expedite network deployment. Additionally, the emergence of educational technology has further driven internet penetration, with companies providing tablets and digital learning solutions as part of their curriculum. According to Ericsson's Mobility Report, the monthly average usage of mobile data in North America is expected to reach 49GB per month for smartphones by 2026, driven by video-rich applications and large data plans, necessitating robust wireless transceivers solutions in both homes and enterprises.

Segment Analysis: By Type

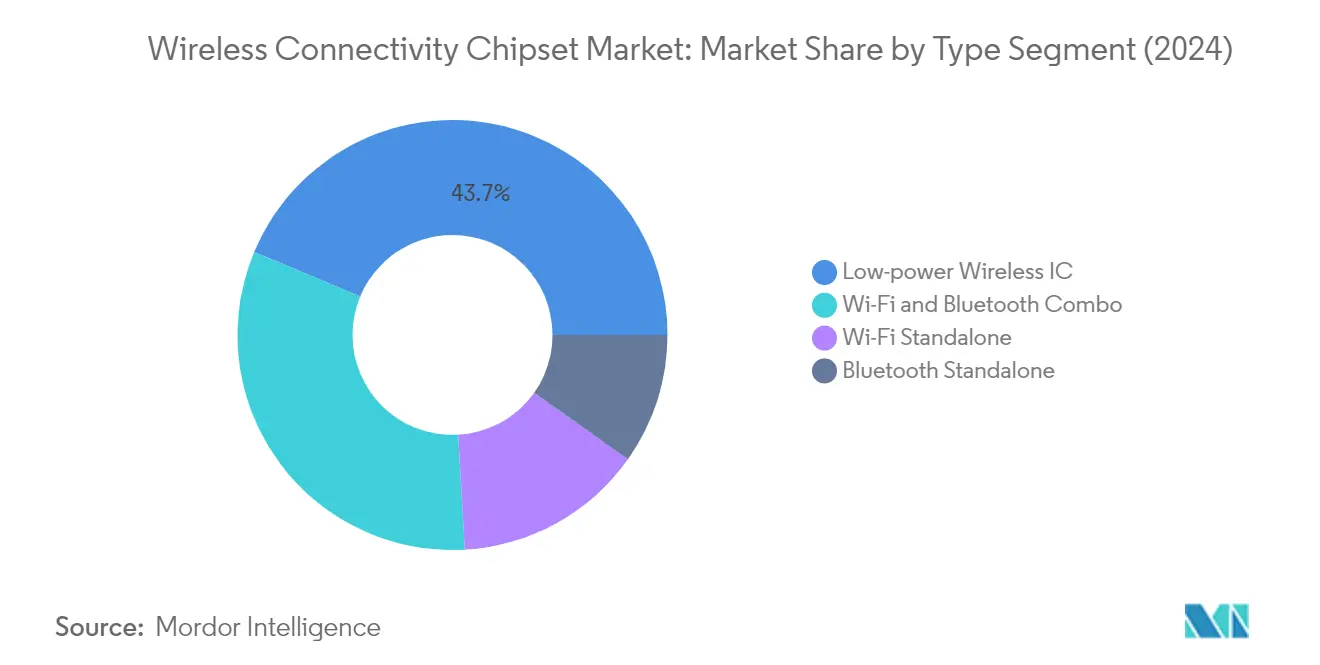

Low-power Wireless IC Segment in Wireless Connectivity Chipset Market

The low-power wireless IC segment dominates the wireless connectivity chipset market, commanding approximately 44% market share in 2024. This segment's leadership position is driven by the increasing adoption of IoT devices across consumer, industrial, and automotive applications that require energy-efficient wireless microcontroller solutions. The segment's growth is further accelerated by the rising demand for smart home devices, wearables, and industrial IoT applications that leverage technologies like Bluetooth Low Energy, Zigbee, and Thread protocols. Major semiconductor manufacturers are focusing on developing ultra-low power wireless microcontroller ICs with enhanced features like improved range, reliability, and security to cater to emerging IoT use cases. The integration of multiple wireless protocols in a single low-power IC is also gaining traction as it enables flexible connectivity options while maintaining minimal power consumption.

Remaining Segments in Wireless Connectivity Chipset Market

The Wi-Fi and Bluetooth combo segment represents the second-largest portion of the market, as these integrated solutions offer manufacturers cost and space advantages while supporting both short-range and wireless networking capabilities. The Wi-Fi standalone segment continues to serve applications requiring dedicated high-bandwidth Wi-Fi chipset connectivity, particularly in networking equipment and consumer electronics. Meanwhile, the Bluetooth standalone segment caters to specific use cases requiring only short-range wireless communication capabilities, utilizing specialized Bluetooth chipset solutions. Each of these segments plays a vital role in serving different market requirements—from high-performance networking to simple device-to-device connectivity. The ongoing evolution of wireless standards like Wi-Fi 6/6E/7 and Bluetooth 5.x is driving innovation across all these segments.

Segment Analysis: By End-User Application

Mobile Handsets Segment in Wireless Connectivity Chipset Market

The mobile handsets segment continues to dominate the wireless connectivity chipset market, commanding approximately 44% market share in 2024. This significant market position is driven by the increasing penetration of smartphones worldwide and the rising adoption of 5G technology. The segment's growth is further bolstered by the integration of advanced wireless module connectivity features in modern smartphones, including Wi-Fi 6/6E capabilities, Bluetooth 5.2 and above, and enhanced cellular connectivity options. The demand for high-performance Wi-Fi chipset solutions in mobile devices is also being fueled by the increasing consumption of data-intensive applications, cloud gaming, and augmented reality experiences on smartphones.

Automotive Segment in Wireless Connectivity Chipset Market

The automotive segment is emerging as the fastest-growing sector in the wireless connectivity chipset market, with a projected growth rate of approximately 11% during 2024-2029. This remarkable growth is primarily attributed to the increasing integration of advanced driver assistance systems (ADAS), connected car technologies, and the evolution towards autonomous vehicles. The automotive industry's shift towards electric vehicles and smart connectivity solutions is driving the demand for sophisticated wireless chipsets that enable vehicle-to-everything (V2X) communication, in-vehicle infotainment systems, and advanced telematics. The development of smart transportation infrastructure and the implementation of 5G technology in automotive applications are further accelerating the adoption of wireless connectivity chipsets in this segment.

Remaining Segments in Wireless Connectivity Chipset Market

The wireless connectivity chipset market encompasses several other significant segments, including consumer electronics, enterprise, industrial, and other end-user applications. The consumer segment is particularly noteworthy due to the growing adoption of smart home devices, wearables, and IoT applications. The enterprise segment focuses on networking infrastructure and business communication systems, while the industrial segment is driven by Industry 4.0 initiatives and industrial automation. These segments collectively contribute to the market's diversity and growth, with each serving unique applications ranging from smart city infrastructure to manufacturing automation and commercial networking solutions.

Wireless Connectivity Chipset Market Geography Segment Analysis

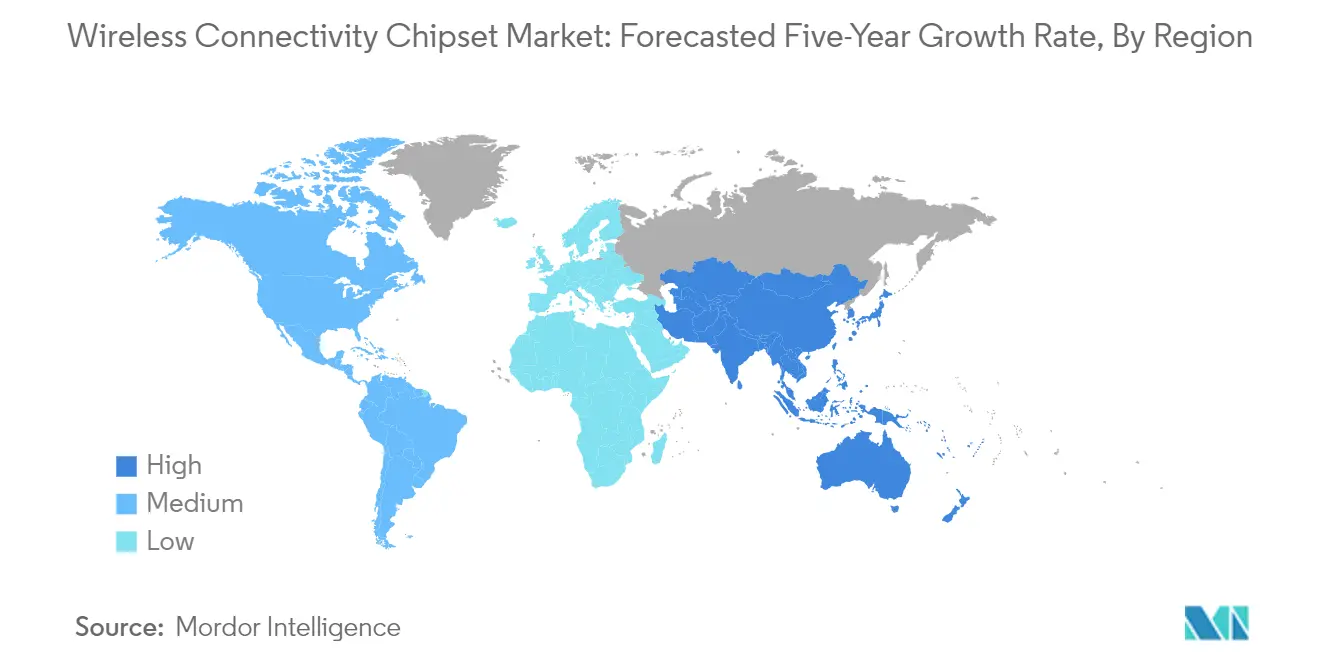

Wireless Connectivity Chipset Market in North America

The North American Wi-Fi chipset market maintains a significant position in the global landscape, commanding approximately 20% market share in 2024. The region's market is primarily driven by the rapid adoption of advanced wireless technologies across consumer electronics, automotive, and industrial sectors. The presence of major technology companies and semiconductor manufacturers has established a robust ecosystem for wireless connectivity solutions. The market is characterized by strong demand for Wi-Fi 6 and Bluetooth 5.2 technologies, particularly in smart home applications and enterprise networking solutions. The region's advanced telecommunications infrastructure and high consumer awareness of connected devices continue to fuel market growth. Additionally, the increasing integration of wireless connectivity in automotive applications, particularly in advanced driver assistance systems (ADAS) and in-vehicle entertainment systems, is creating new growth opportunities. The market also benefits from substantial investments in research and development, fostering innovation in low-power wireless technologies and IoT solutions.

Wireless Connectivity Chipset Market in Europe

The European wireless connectivity chipset market has demonstrated steady growth, with an approximate growth rate of 6% during the period 2019-2024. The market is characterized by strong adoption across automotive, industrial, and consumer electronics sectors, with particular emphasis on Industry 4.0 initiatives. The region's stringent regulatory framework regarding wireless communications and data security has shaped the development of specialized chipset solutions. European manufacturers are increasingly focusing on energy-efficient wireless connectivity solutions, driven by the region's strong commitment to sustainability and green technology. The market is witnessing significant developments in automotive applications, particularly in connected car technologies and electric vehicle infrastructure. The integration of wireless connectivity in industrial automation and smart manufacturing processes continues to drive market growth. Additionally, the region's focus on smart city initiatives and IoT applications has created sustained demand for advanced wireless connectivity solutions. The presence of established semiconductor manufacturers and research institutions continues to foster innovation in wireless technology development.

Wireless Connectivity Chipset Market in Asia-Pacific

The Asia-Pacific wireless connectivity chipset market is positioned for robust expansion, with an expected growth rate of approximately 10% during the period 2024-2029. The region represents the largest and most dynamic market for wireless connectivity chipsets, driven by rapid industrialization and digital transformation initiatives across major economies. The market is characterized by strong manufacturing capabilities, particularly in countries like China, Taiwan, and South Korea, which serve as global hubs for semiconductor production. The increasing adoption of smart devices, rising internet penetration, and growing middle-class population are creating substantial demand for wireless connectivity solutions. The region's automotive sector is experiencing significant growth in connected vehicle technologies, driving demand for automotive-grade wireless chipsets. The implementation of 5G networks and subsequent development of compatible devices is creating new opportunities for wireless connectivity solutions. Additionally, government initiatives supporting digital infrastructure development and smart city projects are fostering market growth. The region's competitive manufacturing landscape and cost advantages continue to attract investments in RF chipset production.

Wireless Connectivity Chipset Market in Rest of the World

The Rest of the World region, encompassing the Middle East and Africa, demonstrates growing potential in the wireless connectivity chipset market. The market is primarily driven by increasing digitalization efforts and the modernization of telecommunications infrastructure. Educational institutions in these regions are increasingly adopting digital learning tools, creating demand for wireless-enabled devices. The market is witnessing significant developments in smart city projects, particularly in the Middle East, driving demand for wireless connectivity solutions. The growing adoption of mobile devices and increasing internet penetration are creating new opportunities for wireless chipset manufacturers. The region's focus on industrial modernization and automation is driving demand for industrial IoT applications. Additionally, investments in telecommunications infrastructure and the rollout of advanced wireless networks are creating favorable conditions for market growth. The market also benefits from increasing adoption of connected devices in both consumer and enterprise segments, while government initiatives supporting digital transformation continue to drive market development.

Get Analysis on Important Geographic Markets

Download PDF

Wireless Connectivity Chipset Industry Overview

Top Companies in Wireless Connectivity Chipset Market

The wireless connectivity chipset market features prominent players like Broadcom, Qualcomm, MediaTek, Intel, and Texas Instruments, who lead innovation and market development. These companies are heavily investing in research and development to advance Wi-Fi technologies, particularly in the evolution from Wi-Fi 6 to Wi-Fi 7 capabilities. Strategic partnerships with device manufacturers and system integrators have become increasingly important for market expansion. Companies are focusing on developing integrated solutions that combine multiple wireless protocols like Wi-Fi, Bluetooth, and IoT connectivity standards. The industry witnesses continuous product launches targeting specific applications across automotive, consumer electronics, industrial automation, and smart home segments. Operational excellence is being achieved through a mix of in-house manufacturing capabilities and strategic outsourcing relationships with foundries and semiconductor fabrication partners.

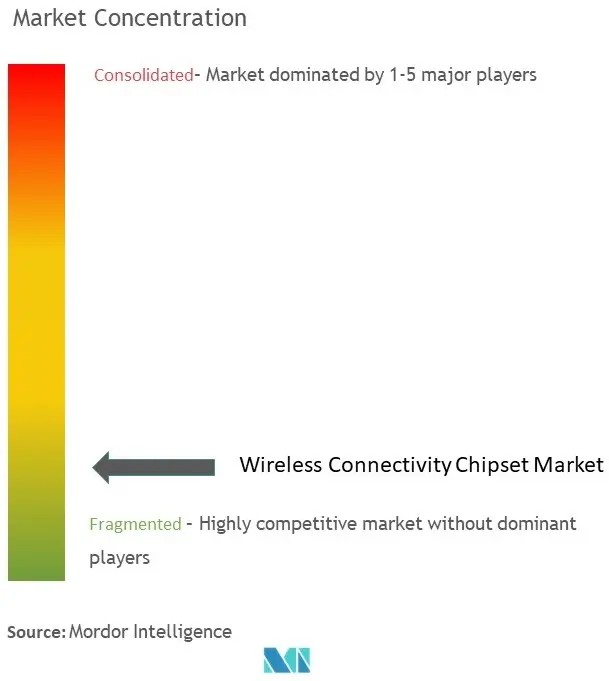

Consolidated Market with Strong Regional Players

The wireless connectivity chipset market demonstrates a relatively consolidated structure dominated by large multinational semiconductor companies with diverse product portfolios. These established players leverage their extensive research capabilities, patent portfolios, and long-standing relationships with device manufacturers to maintain their market positions. Regional players, particularly from Asia, are gaining prominence through focused innovation in specific application segments and cost-competitive offerings. The market has witnessed significant merger and acquisition activity, with larger players acquiring specialized technology companies to enhance their wireless semiconductor solutions portfolio and expand their technological capabilities.

The competitive dynamics are shaped by the increasing vertical integration trends, where some major players are developing end-to-end solutions from chip design to system integration. Market participants are establishing strategic partnerships with foundries and manufacturing partners to ensure supply chain resilience and production capacity. The industry also sees collaboration between chipset manufacturers and software developers to create comprehensive wireless processor solutions that address specific industry requirements and use cases.

Innovation and Adaptability Drive Market Success

Success in the wireless connectivity chipset market increasingly depends on companies' ability to innovate across multiple dimensions—from technical performance and power efficiency to integration capabilities and cost-effectiveness. Incumbent players must continue investing in next-generation wireless technologies while maintaining backward compatibility with existing standards. Companies need to develop specialized solutions for emerging applications like automotive connectivity, industrial IoT, and smart home devices while ensuring their products meet stringent regulatory requirements across different regions. Building strong relationships with device manufacturers and system integrators remains crucial for maintaining market share.

New entrants and challenger companies can gain ground by focusing on underserved market segments and developing specialized solutions for specific applications or regional markets. Success factors include the ability to offer differentiated features, competitive pricing, and robust technical support. Companies must also navigate the complex landscape of wireless standards and certifications while maintaining flexibility to adapt to evolving market requirements. The increasing focus on security and privacy in wireless communications presents both challenges and opportunities for market participants to differentiate their offerings. Additionally, the development of RF semiconductor technologies is pivotal for advancing wireless transceiver capabilities, further enhancing connectivity solutions.

Wireless Connectivity Chipset Market Leaders

-

Broadcom Inc.

-

Qualcomm Incorporated

-

Intel Corporation

-

Texas Instruments Incorporated

-

MediaTek Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Wireless Connectivity Chipset Market News

- April 2024: Ceva Inc., a licensor of silicon and software IP players, unveiled its latest offering, Ceva-Waves™ Links™. This new family of multi-protocol wireless platform IPs is designed to empower Smart Edge devices, enhancing their ability to connect, sense, and process data with heightened reliability and efficiency. The suite of integrated IPs not only complies with the most recent wireless standards but also caters to the escalating demand for connectivity-rich chips. These chips are specifically tailored for Smart Edge devices across diverse sectors, including consumer IoT, industrial applications, automotive, and personal computing. The standout feature of these IPs is their comprehensive support for a spectrum of wireless protocols, encompassing Wi-Fi, Bluetooth, Ultra-Wideband (UWB), and IEEE 802.15.4 (for Thread/Zigbee/Matter).

- March 2024: Murata, a leading electronics manufacturer, announced a collaboration with Infineon to develop a new IoT development solution. This comprehensive solution will facilitate Murata's Infineon-based Wi-Fi® and Bluetooth® modules' seamless integration with a wide range of STM32 Nucleo-144 boards to help reduce the time-to-market for many wireless-enabled applications. By leveraging each other's capabilities, it is engineered to provide hardware and software solutions that address several IoT development requirements. For its core competencies, the platform solution allows the STM32 microcontroller to connect Murata M.2 wireless modules featuring Infineon chipsets.

Wireless Connectivity Chipset Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Assessment of the Impact of Macroeconomic Trends on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increased Demand for Connected Homes Through Home Automation

- 5.1.2 Increasing Internet Penetration into Homes and Enterprises

-

5.2 Market Challenges

- 5.2.1 Issues Related to Security and Privacy of Data and Connectivity of Devices and Interoperability

- 5.2.2 Slow Demand for Some Mobile Handset Types

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Wi-Fi Standalone

- 6.1.2 Bluetooth Standalone

- 6.1.3 Wifi and Bluetooth Combo

- 6.1.4 Low-power Wireless IC

-

6.2 By End-user Application

- 6.2.1 Consumer

- 6.2.2 Enterprise

- 6.2.3 Mobile Handsets

- 6.2.4 Automotive

- 6.2.5 Industrial

- 6.2.6 Other End-user Applications

-

6.3 By Geography***

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Broadcom Inc.

- 7.1.2 Qualcomm Incorporated

- 7.1.3 Mediatek Inc.

- 7.1.4 Intel Corporation

- 7.1.5 Texas Instruments Incorporated

- 7.1.6 STMicroelectronics NV

- 7.1.7 NXP Semiconductors NV

- 7.1.8 On Semiconductor Corporation

- 7.1.9 Infineon Technologies AG

- 7.1.10 Microchip Technology Inc.

- 7.1.11 Qorvo Inc.

- 7.1.12 Skyworks Solutions Inc.

- 7.1.13 Hisilicon Technologies Co. Ltd

- 7.1.14 Tsinghua Unigroup Co. Ltd (unisoc (Shanghai) Technologies Co. Ltd

8. VENDOR MARKET SHARE ANALYSIS

9. INVESTMENT ANALYSIS

10. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'.

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Wireless Connectivity Chipset Industry Segmentation

A wireless chipset is designed to be a part of the internal hardware of wireless communication procedures to allow computers or systems to communicate with each other through wireless means, such as Wi-Fi, Bluetooth, or a combination of both.

The wireless connectivity chipset market is segmented by type (Wi-Fi standalone, Bluetooth standalone, Wi-Fi & Bluetooth combo, and low-power wireless IC), end-user applications (consumer, enterprise, mobile handsets, automotive, industrial, and other end-user applications), and geography (North America, Europe, Asia-Pacific, and the Rest of the World). The market sizes are provided in terms of value (USD) for all the above segments.

| By Type | Wi-Fi Standalone |

| Bluetooth Standalone | |

| Wifi and Bluetooth Combo | |

| Low-power Wireless IC | |

| By End-user Application | Consumer |

| Enterprise | |

| Mobile Handsets | |

| Automotive | |

| Industrial | |

| Other End-user Applications | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Wireless Connectivity Chipset Market Research FAQs

How big is the Wireless Connectivity Chipset Market?

The Wireless Connectivity Chipset Market size is expected to reach USD 9.23 billion in 2025 and grow at a CAGR of 8.36% to reach USD 13.79 billion by 2030.

What is the current Wireless Connectivity Chipset Market size?

In 2025, the Wireless Connectivity Chipset Market size is expected to reach USD 9.23 billion.

Who are the key players in Wireless Connectivity Chipset Market?

Broadcom Inc., Qualcomm Incorporated, Intel Corporation, Texas Instruments Incorporated and MediaTek Inc. are the major companies operating in the Wireless Connectivity Chipset Market.

Which is the fastest growing region in Wireless Connectivity Chipset Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Wireless Connectivity Chipset Market?

In 2025, the Asia-Pacific accounts for the largest market share in Wireless Connectivity Chipset Market.

What years does this Wireless Connectivity Chipset Market cover, and what was the market size in 2024?

In 2024, the Wireless Connectivity Chipset Market size was estimated at USD 8.46 billion. The report covers the Wireless Connectivity Chipset Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Wireless Connectivity Chipset Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Wireless Connectivity Chipset Market Research

Mordor Intelligence provides a comprehensive analysis of the wireless connectivity chipset industry. We leverage our extensive expertise in RF semiconductor and wireless technology research. Our detailed report explores the evolution of bluetooth chipset technology, wifi chipset innovations, and advanced wireless module solutions. The analysis covers the complete ecosystem, from wireless transceiver components to integrated wireless SOC platforms. Detailed insights are available in an easy-to-read report PDF format, ready for download.

This strategic report benefits stakeholders across the value chain. It offers deep insights into RF chipset developments and emerging wireless semiconductor technologies. Our analysis includes crucial components such as wireless microcontroller units, wireless processor architectures, and wireless communication IC developments. The report examines key applications of RF semiconductor technology and provides detailed forecasts for the wireless semiconductor market. This enables businesses to make informed decisions based on comprehensive market intelligence and technical expertise.