| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 7.00 % |

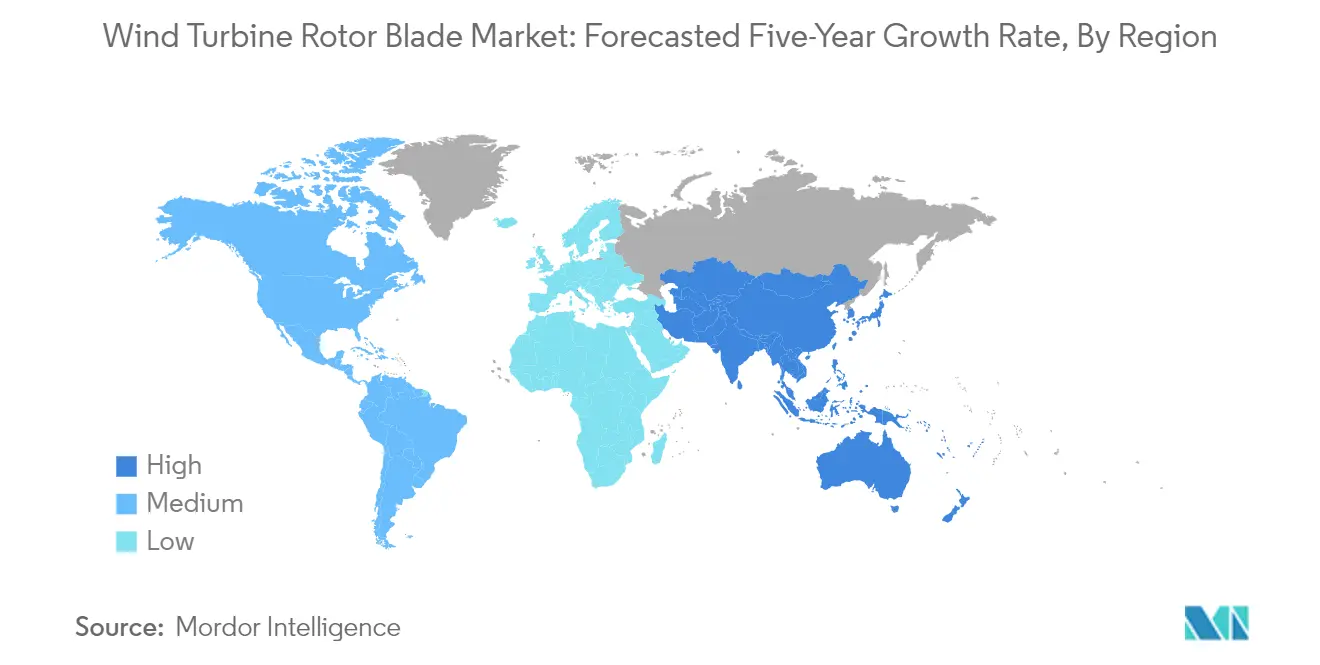

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Wind Turbine Rotor Blade Market Analysis

The Wind Turbine Rotor Blade Market is expected to register a CAGR of greater than 7% during the forecast period.

The wind turbine rotor blade industry is experiencing significant technological evolution, driven by the increasing demand for larger and more efficient turbines. Manufacturing competition has intensified globally, leading to innovations in wind turbine blade design and materials. A notable milestone was achieved in October 2022 when the world's largest rotor diameter of 252 meters was installed in an offshore wind turbine in China's Fujian Province, demonstrating the industry's push towards larger wind turbine blade size. This technological advancement enables single turbines to generate up to 63.5 million kWh annually, sufficient to power 30,000 households, showcasing the dramatic improvements in energy generation capacity.

The global manufacturing landscape is undergoing substantial transformation, with China emerging as the dominant hub for wind turbine components. Chinese manufacturers now account for approximately 60-65% of global production of turbines, nacelles, and key components including rotor blades. This manufacturing consolidation has intensified price competition, with turbine prices, including towers, dropping to record lows of USD 316/kW for onshore wind and USD 632/kW for offshore wind at the beginning of 2022. The industry is witnessing increased investment in automated wind blade manufacturing processes and advanced materials to improve blade quality while reducing production costs.

Cost efficiency improvements continue to drive market dynamics, with significant reductions in the Levelized Cost of Energy (LCOE). Industry projections indicate that wind energy LCOE is expected to decrease to 44.6 USD/MWh by 2025, making wind power increasingly competitive with traditional energy sources. This trend is accompanied by innovations in blade materials, including the integration of carbon fiber composites and hybrid materials, which enhance durability while reducing weight and maintenance requirements. Manufacturers are increasingly focusing on developing blades that optimize the balance between performance, cost, and reliability.

The industry is witnessing a marked shift towards sustainable manufacturing practices and circular economy principles. Wind turbine blade manufacturers are investing in recyclable materials and developing new manufacturing processes to address end-of-life concerns. Advanced materials such as thermoplastic resins and modular blade designs are being introduced to facilitate easier recycling and maintenance. This evolution in manufacturing approaches is complemented by the development of smart blade technologies incorporating sensors and monitoring systems, enabling predictive maintenance and optimal performance throughout the blade's lifecycle.

Wind Turbine Rotor Blade Market Trends

Declining Costs and Technological Advancements

The wind energy sector has witnessed significant cost reductions and technological improvements that are driving market growth. According to the International Renewable Energy Agency (IRENA), the levelized cost of energy (LCOE) has decreased substantially from 0.060 USD/kWh in 2016 to 0.039 USD/kWh in 2020, while the global weighted average total installed cost reduced from 1652 USD/kW to 1355 USD/kW during the same period. This declining cost trend is primarily attributed to reductions in capital costs, increased competition as the sector matures, and continuous technological improvements in wind turbine blades components, including rotor blades.

The wind energy power generation technology has evolved considerably over the last five years to maximize electricity production per megawatt capacity installed. Modern wind turbines have become larger with taller hub heights and broader diameters, necessitating longer and more efficient wind turbine blades designs. These technological advancements have enabled wind farms to operate efficiently even in areas with lower wind speeds, expanding the potential deployment locations. The industry has also made significant progress in materials technology, with wind blade manufacturers incorporating advanced materials like carbon fiber and innovative design features to enhance blade performance while reducing overall system costs.

Understand The Key Trends Shaping This Market

Download PDF

Supportive Government Policies and Environmental Regulations

Government support through policy reforms, dedicated R&D initiatives, and new financing mechanisms has emerged as a crucial driver for the wind turbine blade market. Countries worldwide are implementing ambitious renewable energy targets and supportive regulatory frameworks to accelerate the transition toward clean energy sources. For instance, several nations have introduced production tax credits, feed-in tariffs, and other financial incentives to promote wind energy development, directly benefiting the wind turbine blade manufacturers sector.

The global push toward achieving net-zero carbon emissions has resulted in stricter environmental regulations and the planned phase-out of conventional power systems. Many governments are implementing comprehensive plans to accelerate renewable energy development, including specific targets for wind energy capacity additions. These regulatory frameworks are complemented by increased public and private sector investments in wind energy infrastructure, creating a favorable environment for technological innovation and market expansion in the wind turbine rotor blade sector. The industry has also witnessed the emergence of new financing mechanisms and business models that help reduce project development risks and attract greater investment in wind energy projects.

Rising Energy Demand and Rural Electrification Needs

The growing global energy demand, particularly in developing regions, coupled with the need for rural electrification, is driving the expansion of wind energy infrastructure. Wind energy technology has proven to be an effective solution for providing electricity to rural and isolated areas, where traditional grid infrastructure may be challenging or cost-prohibitive to implement. The ability of wind power systems to operate independently or as part of microgrids makes them particularly suitable for addressing rural electrification needs while contributing to national renewable energy goals.

The increasing focus on sustainable development and energy security has led to greater emphasis on diversifying energy sources, with wind power emerging as a key component of the energy mix. Large-scale wind farms are being developed to meet the rising electricity demand in both urban and rural areas, while also addressing environmental concerns associated with conventional power generation. The industry has responded to this demand by developing more efficient and reliable wind turbine components, including advanced rotor blade designs that can maximize power generation across various wind conditions and geographical locations. Turbine blade manufacturing companies are at the forefront of this innovation, ensuring that the wind turbine blade market continues to evolve and meet the diverse needs of global energy consumers.

Segment Analysis: Location of Deployment

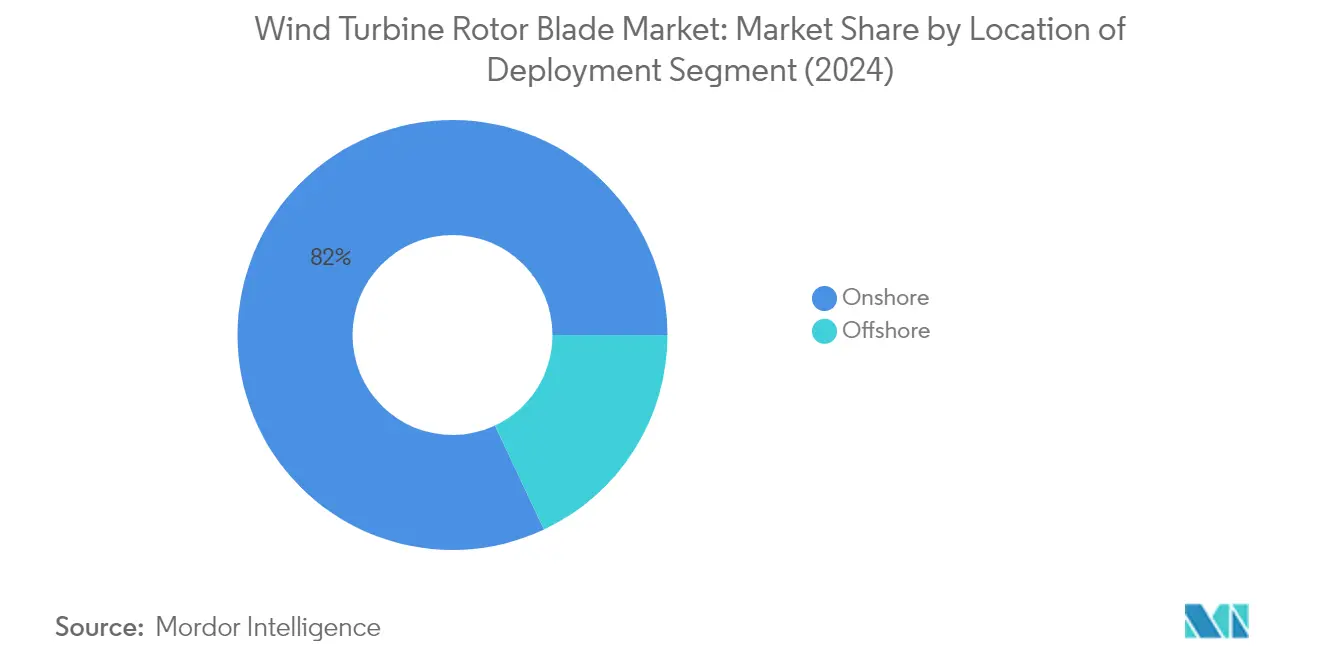

Onshore Segment in Wind Turbine Rotor Blade Market

The onshore segment dominates the wind turbine rotor blade market, commanding approximately 82% of the total market share in 2024. This dominance is primarily attributed to lower installation costs, easier maintenance access, and well-established infrastructure compared to offshore installations. Major markets like China, the United States, and India continue to drive substantial growth in the onshore segment through ambitious renewable energy targets and supportive government policies. The segment's strength is further reinforced by technological advancements in blade design and materials, allowing for larger rotor diameters and improved efficiency even in low wind speed conditions. Additionally, the increasing focus on repowering existing onshore wind farms with newer, more efficient turbines has created a steady demand for replacement wind turbine blades.

Offshore Segment in Wind Turbine Rotor Blade Market

The offshore segment is experiencing remarkable growth momentum in the wind turbine rotor blade market for the period 2024-2029. This accelerated growth is driven by massive investments in offshore wind projects, particularly in regions like Europe, China, and the United States. The segment's expansion is supported by technological innovations such as floating wind platforms, larger turbine capacities, and specialized blade designs optimized for marine environments. Countries like the UK, China, and the United States have announced ambitious offshore wind installation targets, with China leading the global offshore installations. The development of specialized port infrastructure, installation vessels, and maintenance capabilities is further facilitating the segment's growth. Additionally, the offshore segment benefits from higher wind speeds and more consistent wind conditions at sea, leading to greater power generation efficiency and attracting increased investment despite higher initial costs.

Segment Analysis: Blade Material

Carbon Fiber Segment in Wind Turbine Rotor Blade Market

Carbon fiber dominates the wind turbine blade material market, holding approximately 46% market share in 2024, due to its superior strength-to-weight ratio and exceptional performance characteristics. The material's properties make it particularly valuable for manufacturing longer and lighter rotor blades, as it is 70% lighter than steel and 40% lighter than aluminum while offering excellent fatigue resistance and corrosion protection. According to industry analysis, blades containing carbon fiber weigh approximately 25% less than conventional fiberglass materials, resulting in improved longevity and enhanced energy capture capabilities. The material's growing adoption is driven by the increasing demand for larger offshore wind turbines, where blade length and weight optimization are crucial factors for operational efficiency.

Glass Fiber Segment in Wind Turbine Rotor Blade Market

The glass fiber segment is experiencing rapid growth in the wind turbine blade market, driven by its cost-effectiveness and reliable performance characteristics. The material's popularity is particularly strong in onshore wind applications, where its combination of decent mechanical properties and lower cost compared to carbon fiber makes it an attractive choice for manufacturers. Glass fiber reinforced plastics (GRP) continue to be the preferred choice for many modern rotor blades, especially in regions where cost optimization is a priority. The segment's growth is further supported by ongoing technological improvements in glass fiber composites and their proven track record in the industry.

Remaining Segments in Blade Material Market

Other blade materials, including hybrid reinforcements, aramid fibers, and basalt fibers, play a specialized role in the wind turbine rotor blade market. These alternative materials often serve specific applications where unique properties are required, such as hybrid reinforcements combining E-glass/carbon and E-glass/aramid for optimized performance characteristics. Natural fibers, including bamboo-poplar epoxy laminates, are also emerging as sustainable alternatives, though their application remains limited to small wind turbine installations due to quality variations and thermal stability concerns.

Wind Turbine Rotor Blade Market Geography Segment Analysis

Wind Turbine Rotor Blade Market in North America

North America represents a mature wind turbine rotor blade market, characterized by significant technological advancement and robust infrastructure development. The region's market is primarily driven by increasing renewable energy targets, supportive government policies, and growing investments in both onshore and offshore wind projects. The United States dominates the regional landscape, followed by Canada, with both countries focusing on expanding their wind energy capacity through various initiatives and projects.

Wind Turbine Rotor Blade Market in United States

The United States maintains its position as the largest market for wind turbine blades in North America, commanding approximately 65% of the regional market share in 2024. The country's market is characterized by extensive onshore wind installations across multiple states, particularly in Texas, Iowa, and Oklahoma. The nation's commitment to wind energy is evident through its comprehensive infrastructure, established supply chains, and continuous technological innovations in blade design and manufacturing. The country's wind energy sector benefits from strong domestic manufacturing capabilities and a robust network of wind turbine blade manufacturers in the USA.

Wind Turbine Rotor Blade Market in Canada

Canada emerges as the fastest-growing market in North America, with an expected growth rate of approximately 8% during 2024-2029. The country's wind energy sector is experiencing rapid expansion, particularly in provinces like Ontario, Quebec, and Alberta. Canada's growth is supported by its vast wind resources, particularly in its northern and coastal regions, along with strong government support for renewable energy development. The country's commitment to reducing carbon emissions and transitioning to clean energy sources continues to drive investment in wind turbine blade infrastructure and technology.

Wind Turbine Rotor Blade Market in Europe

Europe maintains its position as a key turbine blade market, driven by ambitious renewable energy targets and strong regulatory support. The region's market is characterized by a mix of mature and emerging markets, with Germany, France, Spain, and the United Kingdom leading the development. The European market benefits from advanced manufacturing capabilities, strong research and development initiatives, and an increasing focus on offshore wind development.

Wind Turbine Rotor Blade Market in Germany

Germany continues to lead the European market, holding approximately 40% of the regional market share in 2024. The country's dominance is supported by its well-established wind energy infrastructure, strong domestic manufacturing capabilities, and comprehensive government support for renewable energy development. Germany's market is characterized by a balanced mix of onshore and offshore installations, with a particular focus on technological innovation and efficiency improvements in rotor blade design.

Wind Turbine Rotor Blade Market in United Kingdom

The United Kingdom demonstrates the highest growth potential in Europe, with an anticipated growth rate of approximately 12% during 2024-2029. The country's market is primarily driven by its ambitious offshore wind development plans and strong government support for renewable energy. The UK's strategic focus on developing its offshore wind capacity, particularly in the North Sea region, positions it as a key growth market for advanced wind turbine blade technologies.

Wind Turbine Rotor Blade Market in Asia-Pacific

The Asia-Pacific region represents a dynamic wind turbine rotor blade market, characterized by rapid industrialization, increasing energy demands, and strong government support for renewable energy development. The region encompasses diverse markets, including China, India, South Korea, and Japan, each with unique growth drivers and market characteristics. The market benefits from extensive manufacturing capabilities, competitive cost structures, and growing technological expertise.

Wind Turbine Rotor Blade Market in China

China maintains its position as the dominant force in the Asia-Pacific wind turbine blade market. The country's market leadership is driven by extensive manufacturing capabilities, strong domestic supply chains, and comprehensive government support for renewable energy development. China's market is characterized by continuous technological advancement, an increasing focus on offshore wind development, and strong integration of wind power into the national energy mix.

Wind Turbine Rotor Blade Market in India

India emerges as the fastest-growing market in the Asia-Pacific region. The country's growth is driven by ambitious renewable energy targets, favorable government policies, and increasing private sector investments in wind energy projects. India's market development is supported by improving infrastructure, growing domestic manufacturing capabilities, and a strategic focus on both onshore and offshore wind development. The presence of leading wind turbine blade manufacturers in India further strengthens the market's growth prospects.

Wind Turbine Rotor Blade Market in South America

The South American market for wind turbine rotor blades continues to evolve, with Brazil emerging as both the largest and fastest-growing market in the region. Other significant markets include Argentina and Chile, each contributing to the region's growing wind energy sector. The market is characterized by increasing investments in wind power infrastructure, improving regulatory frameworks, and a growing focus on renewable energy development. The region benefits from abundant wind resources, particularly along its coastal areas, and demonstrates strong potential for future growth in both onshore and offshore wind installations.

Wind Turbine Rotor Blade Market in Middle East & Africa

The Middle East and Africa region represents an emerging market for wind turbine rotor blades, with significant growth potential across various countries, including Morocco, Egypt, and South Africa. South Africa leads the regional market in terms of installed capacity, while Egypt demonstrates the fastest growth potential. The region's market is characterized by increasing investments in renewable energy infrastructure, growing government support for wind power development, and abundant wind resources, particularly in coastal and desert regions. The market benefits from improving regulatory frameworks and an increasing focus on diversifying energy sources away from traditional fossil fuels.

Get Analysis on Important Geographic Markets

Download PDF

Wind Turbine Rotor Blade Industry Overview

Top Companies in Wind Turbine Rotor Blade Market

The wind turbine blade market is characterized by companies focusing heavily on technological advancement and innovation, particularly in developing longer and more efficient blades for both onshore and offshore applications. Companies are investing substantially in research and development to create sustainable solutions, exemplified by initiatives like zero-waste blade manufacturing and the use of recyclable materials. Strategic partnerships and collaborations across the value chain have become increasingly common, especially between wind blade manufacturers and wind turbine OEMs, to optimize production capabilities and enhance market reach. Operational agility is demonstrated through the establishment of manufacturing facilities in strategic locations close to high-demand markets, while companies are also expanding their service offerings to include maintenance, repairs, and performance optimization solutions. Geographic expansion, particularly into emerging markets with strong wind energy potential, remains a key growth strategy for major players.

Market Structure Shows Mixed Global-Local Dynamic

The wind turbine rotor blade market exhibits a moderately fragmented structure with a mix of global conglomerates and specialized manufacturers. Large integrated companies like GE, Siemens Gamesa, and Vestas maintain significant market presence through vertical integration, controlling both turbine and blade manufacturing operations. Independent blade manufacturers like TPI Composites and LM Wind Power have established strong positions through specialized expertise and strategic partnerships with multiple turbine manufacturers. The market demonstrates regional variations in competitive dynamics, with local manufacturers holding strong positions in key markets like China and India, while global players dominate in Europe and North America.

The industry has witnessed significant consolidation through strategic acquisitions and partnerships, as exemplified by GE's acquisition of LM Wind Power and various collaborative agreements between blade manufacturers and turbine OEMs. Market entry barriers remain high due to substantial capital requirements, technical expertise needs, and the importance of established track records in blade design and manufacturing. The competitive landscape is further shaped by the increasing trend of backward integration by major wind turbine manufacturers, who are expanding their in-house blade manufacturing capabilities while maintaining relationships with independent suppliers.

Innovation and Sustainability Drive Future Success

Success in the wind turbine rotor blade market increasingly depends on companies' ability to innovate while maintaining cost competitiveness. Manufacturers must focus on developing advanced materials and manufacturing processes that enable longer, lighter, and more durable blades while reducing production costs. The ability to scale production efficiently while maintaining quality standards has become crucial, particularly as wind turbine sizes continue to increase. Companies must also demonstrate strong capabilities in sustainability and circular economy practices, as evidenced by the growing emphasis on recyclable blade materials and zero-waste manufacturing processes.

Market participants need to carefully balance their geographic presence and customer relationships, particularly given the high concentration of wind turbine blade manufacturers who represent the primary customer base. Success strategies for newer entrants include focusing on specific market segments or regions, developing innovative blade designs or materials, and establishing strong partnerships with established players. Regulatory support for wind energy development continues to shape market opportunities, while the increasing focus on offshore wind installations creates new demands for specialized blade designs and manufacturing capabilities. The relatively low threat of substitution products reinforces the importance of maintaining technological leadership and operational excellence in blade manufacturing.

Wind Turbine Rotor Blade Market Leaders

-

TPI Composites SA

-

Vestas Wind Systems A/S

-

Enercon GmbH

-

LM Wind Power (a GE Renewable Energy business)

-

Siemens Gamesa Renewable Energy, S.A.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Wind Turbine Rotor Blade Market News

- March 2022: The ZEBRA (Zero Waste Blade Research) consortium is a new step in the wind energy industry's transition to a circular economy with the production of its 100% recyclable wind turbine prototype blade. The 62-meter blade was made using Arkema's Elium resin, a thermoplastic resin well known for its recyclable properties, and the new high-performance Glass Fabrics from Owens Corning.

- March 2022: Hitachi Power Solutions will commence advanced services titled - Blade Total Service. It is expected to mitigate the risks of wind power facilities, including deterioration due to wear and tear of rotating blades, the stress imposed by violent winds during typhoons, and damage caused by lightning - by combining AI and other digital technologies with cutting-edge drone technology.

Wind Turbine Rotor Blade Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Wind Turbine Rotor Blades Price Analysis

- 4.4 Recent Trends and Developments

- 4.5 Government Policies, Regulations, and Targets

-

4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.2 Restraints

- 4.7 Supply Chain Analysis

-

4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

-

5.2 Blade Material

- 5.2.1 Carbon Fiber

- 5.2.2 Glass Fiber

- 5.2.3 Other Blade Materials

-

5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 TPI Composites Inc.

- 6.3.2 Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd

- 6.3.3 LM Wind Power (a GE Renewable Energy business)

- 6.3.4 Nordex SE

- 6.3.5 Siemens Gamesa Renewable Energy, S.A.

- 6.3.6 Vestas Wind Systems A/S

- 6.3.7 MFG Wind

- 6.3.8 Sinoma wind power blade Co. Ltd

- 6.3.9 Aeris Energy

- 6.3.10 Suzlon Energy Limited

- 6.3.11 Enercon GmbH

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Wind Turbine Rotor Blade Industry Segmentation

Wind turbine rotor blades are the key components of wind turbines, as they are in direct contact with high-speed winds. Rotor blades convert wind's kinetic energy into rotational energy, which is later converted into electrical energy. The global wind turbine rotor blade market is segmented by location of deployment, blade material, and geography. By location of deployment, the market is segmented into onshore and offshore. By blade material, the market is segmented by carbon fiber, glass fiber, and other blade materials. The report also covers the market size and forecasts for the wind turbine rotor blade market across major regions, namely North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion).

| Location of Deployment | Onshore |

| Offshore | |

| Blade Material | Carbon Fiber |

| Glass Fiber | |

| Other Blade Materials | |

| Geography | North America |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Wind Turbine Rotor Blade Market Research FAQs

What is the current Wind Turbine Rotor Blade Market size?

The Wind Turbine Rotor Blade Market is projected to register a CAGR of greater than 7% during the forecast period (2025-2030)

Who are the key players in Wind Turbine Rotor Blade Market?

TPI Composites SA, Vestas Wind Systems A/S, Enercon GmbH, LM Wind Power (a GE Renewable Energy business) and Siemens Gamesa Renewable Energy, S.A. are the major companies operating in the Wind Turbine Rotor Blade Market.

Which is the fastest growing region in Wind Turbine Rotor Blade Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Wind Turbine Rotor Blade Market?

In 2025, the Asia Pacific accounts for the largest market share in Wind Turbine Rotor Blade Market.

What years does this Wind Turbine Rotor Blade Market cover?

The report covers the Wind Turbine Rotor Blade Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Wind Turbine Rotor Blade Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Wind Turbine Rotor Blade Market Research

Mordor Intelligence provides a comprehensive analysis of the wind turbine rotor blade market, utilizing our extensive experience in renewable energy research. Our detailed report examines the evolving landscape of wind turbine blade technology. It includes crucial aspects such as wind turbine blade dimensions and manufacturing processes. The analysis covers various elements, from wind turbine blade size specifications—ranging from standard to offshore applications—to the latest developments in blade manufacturing techniques used by leading turbine blade manufacturers.

The report, available as an easy-to-download PDF, offers stakeholders crucial insights into wind turbine blade market growth trends and regional dynamics. It includes a detailed analysis of wind turbine blade manufacturers in India and wind turbine blade manufacturers USA. Our research encompasses a comprehensive evaluation of wind turbine rotor technology, blade repair market developments, and turbine blade cost considerations. The report also explores the expanding role of carbon fiber wind turbine blades and innovations in advanced wind turbine blade material. These insights are valuable for industry participants, investors, and decision-makers in the renewable energy sector.