Wind Turbine Maintenance, Repair, And Overhaul (MRO) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

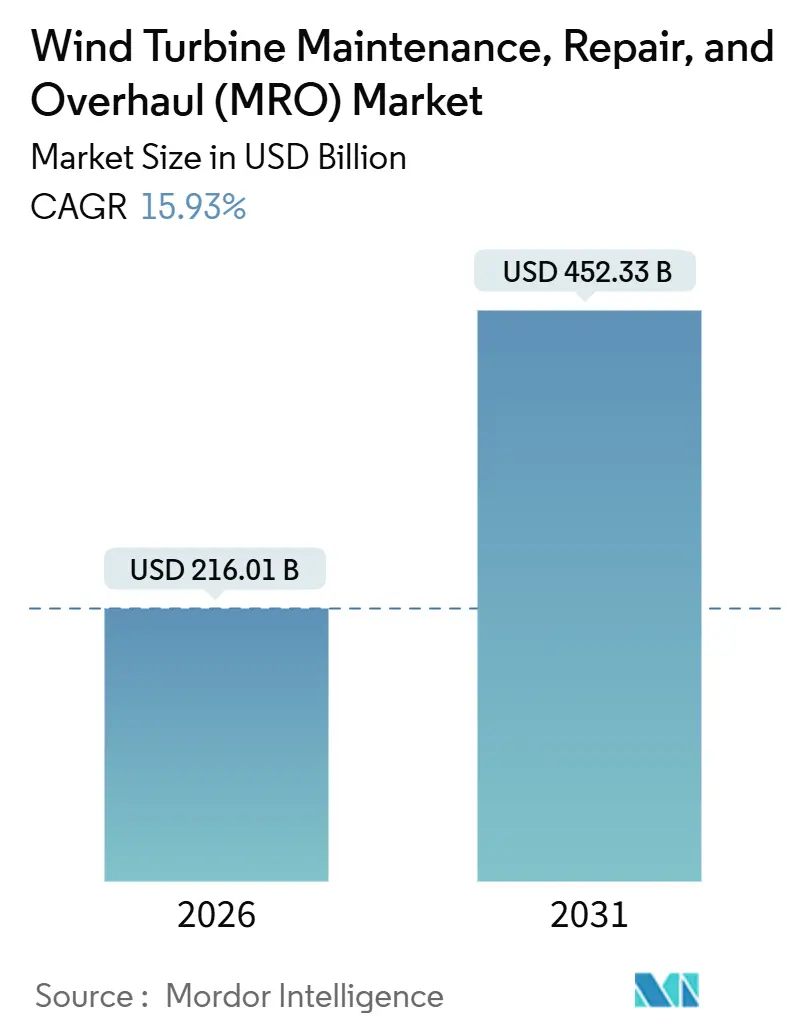

| Market Size (2026) | USD 216.01 Billion |

| Market Size (2031) | USD 452.33 Billion |

| Growth Rate (2026 - 2031) | 15.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wind Turbine Maintenance, Repair, And Overhaul (MRO) Market Analysis by Mordor Intelligence

The Wind Turbine Maintenance, Repair, And Overhaul Market size is estimated at USD 216.01 billion in 2026, and is expected to reach USD 452.33 billion by 2031, at a CAGR of 15.93% during the forecast period (2026-2031).

Growth is fueled by an aging installed base that has now passed 1 terawatt, an upshift in OEM business models toward long-term availability contracts, and tightening grid-code mandates that push owners to retrofit power electronics, blades, and gearboxes. Asia-Pacific remains the revenue anchor, led by China’s directive to upgrade more than 50 GW of pre-2015 onshore capacity, while Europe drives complexity through expanding offshore fleets, especially floating platforms that require specialized vessels and real-time condition monitoring. Intensifying competition between OEMs and independent service providers (ISPs) is lowering transactional repair prices yet broadening the menu of risk-sharing contracts. Digital twins and AI-enabled predictive analytics are cutting unplanned downtime, but the market still contends with gearbox reliability issues in the >5 MW class, heavy-lift vessel shortages, and a global lack of certified blade-repair technicians.

Key Report Takeaways

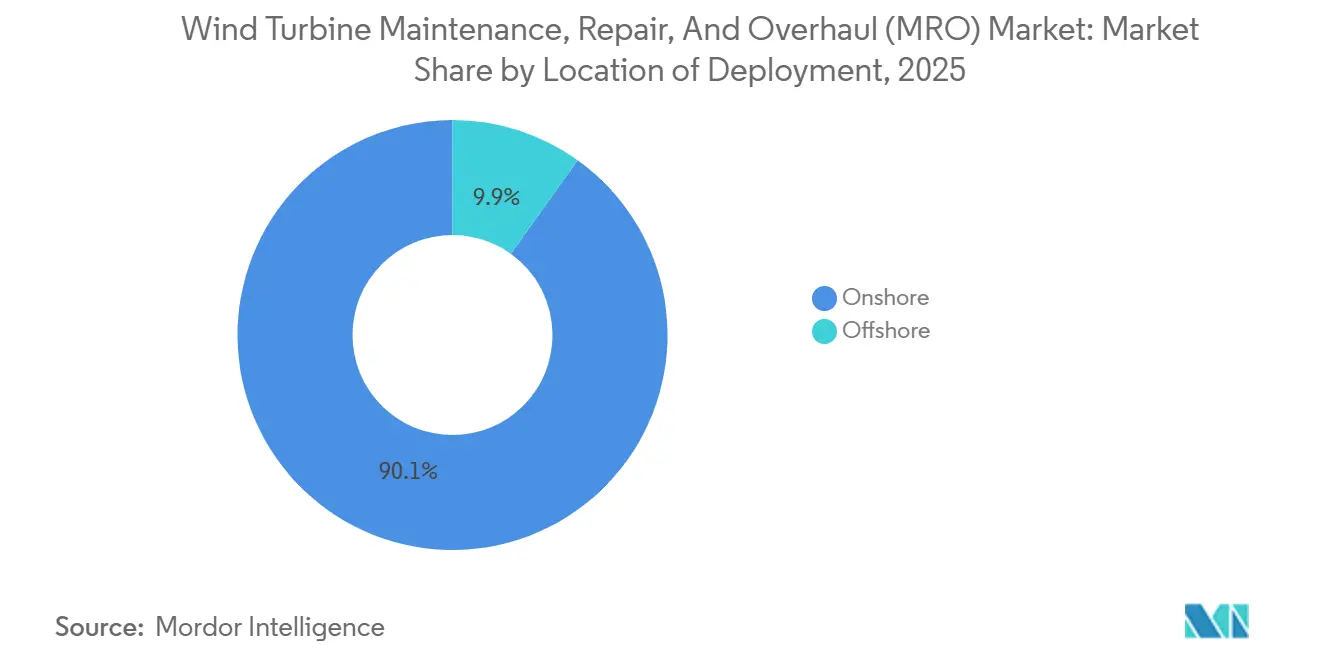

- By location of deployment, onshore sites captured 90.1% of 2025 revenue; offshore work is advancing at 28.3% CAGR on the back of larger >15 MW turbines and floating-wind rollouts.

- By service type, overhaul activities led with 46.4% of wind turbine maintenance, repair & overhaul (MRO) market share in 2025; the category is forecast to expand at a 20.4% CAGR through 2031.

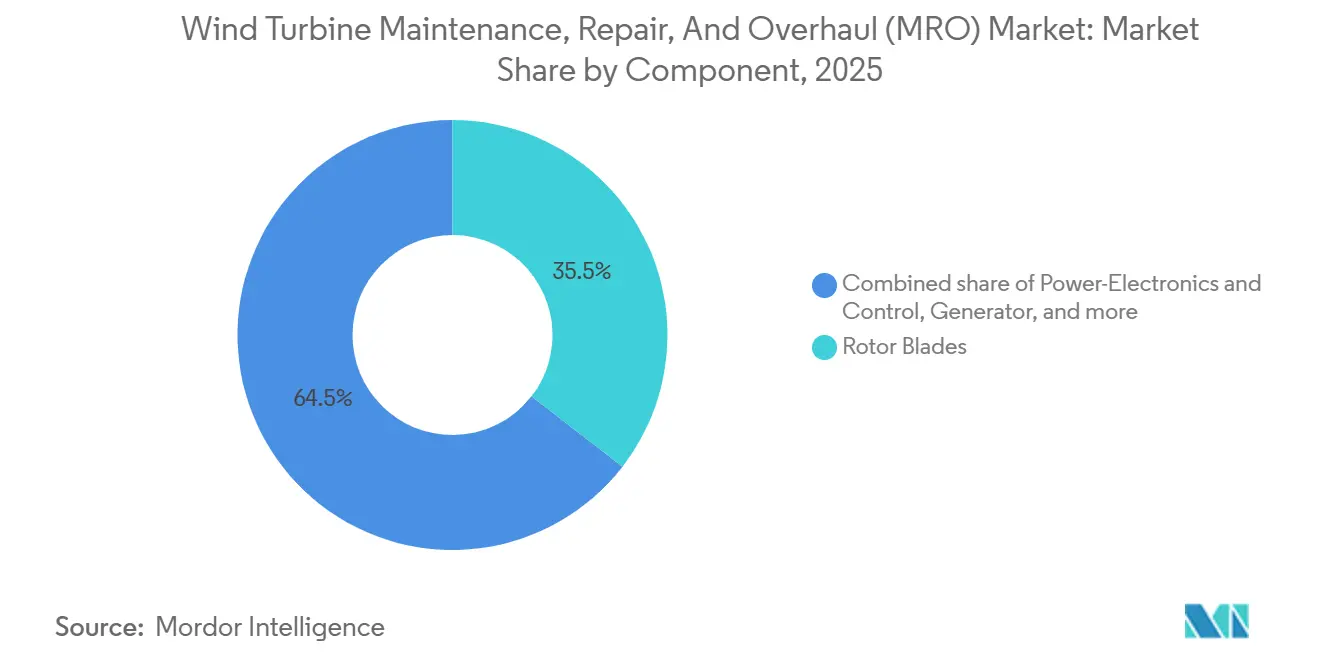

- By component, rotor blades accounted for 35.5% of spending in 2025, while power-electronics upgrades are projected to grow at 22.5% CAGR to 2031.

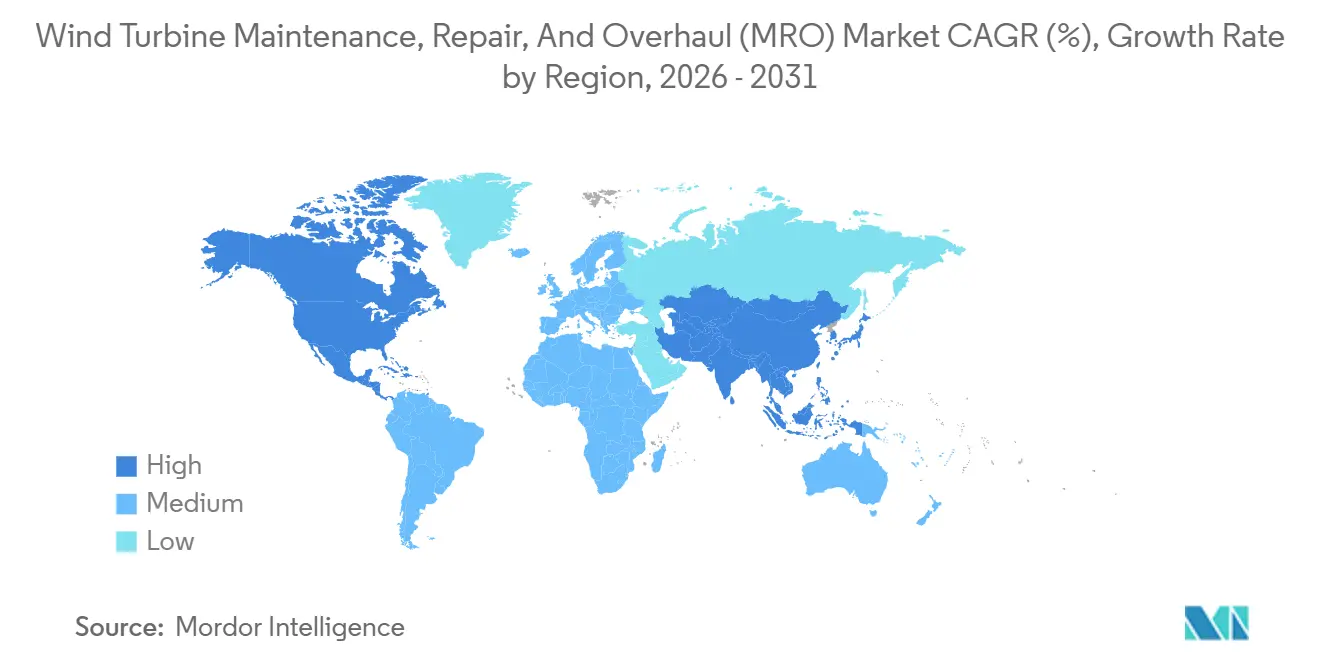

- By geography, Asia-Pacific commanded 53.9% of the 2025 total, driven by China’s retrofit mandate and India’s production-linked incentives; the region is forecast to post a 17.6% CAGR to 2031.

- Vestas, Siemens Gamesa, and GE Renewable Energy controlled close to 60% of the global service backlog in 2025, yet regional specialists such as Global Wind Service and B9 Energy are gaining share through multi-brand technician pools and faster mobilization.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wind Turbine Maintenance, Repair, And Overhaul (MRO) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended turbine lifespans through life-extension retrofits | +3.2% | Global, concentrated in Europe & North America | Medium term (2-4 years) |

| AI-driven predictive analytics reduce unplanned downtime | +2.8% | Asia-Pacific core; spill-over to Europe & North America | Short term (≤2 years) |

| Service-oriented OEM business models (power-by-the-hour) | +2.5% | Global, led by Europe & North America | Medium term (2-4 years) |

| National repowering incentives for >10-yr-old fleets | +3.1% | North America & Europe, emerging in Asia-Pacific | Long term (≥4 years) |

| Floating-wind rollout creates specialized MRO demand | +1.9% | Europe (North Sea, Atlantic) & Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Extended Turbine Lifespans Through Life-Extension Retrofits

Operators are increasingly choosing retrofit programs that add 5–10 additional operating years at one-quarter the capital outlay of full repowering. Germany alone has extended more than 4 GW of pre-2005 capacity by reinforcing blade spars and replacing main bearings, circumventing the 24–36-month permitting cycle tied to new foundations. Project costs typically fall between USD 150,000 and USD 400,000 per turbine, compared with USD 1.2 million to USD 1.8 million for a complete replacement. Vestas reported that life-extension contracts reached 18% of its 2025 service revenue, up from 11% in 2023.[1]Vestas Wind Systems, “Annual Report 2025,” vestas.com The trend is accelerating in the United States because the Inflation Reduction Act’s production tax credit rewards incremental output from existing assets. Publication of DNV GL’s updated IEC 61400 lifetime-extension guidelines in 2024 has lowered certification risk and opened the door for ISPs to compete aggressively for retrofit work.

AI-Driven Predictive Analytics Reduce Unplanned Downtime

Machine-learning algorithms that parse SCADA streams, vibration data, and thermal imagery are detecting failures 4–8 weeks in advance, turning reactive work orders into condition-based tasks. Siemens Gamesa’s Digital Services platform, deployed across 25 GW by mid-2025, lowered unplanned downtime by 22% and trimmed emergency call-out costs by USD 35,000 per turbine per year.[2]Siemens Gamesa Renewable Energy, “Digital Services Expansion,” siemensgamesa.com GE’s Digital Wind Farm suite delivered a 15% availability gain across 18 GW of installations. Offshore owners value the technology most, using early alerts to cluster interventions into single campaigns and shave vessel charter budgets by up to 40%. Retrofits are limited by sparse sensor coverage on turbines built before 2018, creating an aftermarket for instrumentation upgrades.

Service-Oriented OEM Business Models (Power-by-the-Hour)

OEMs are migrating from transactional part sales to availability-based pricing that shifts performance risk onto the supplier and stabilizes cash flow. Under Active Output Management contracts, operators pay per megawatt-hour generated, while Vestas assumes full responsibility for spares, labor, and optimization. The firm covered 32 GW under these deals in 2025, generating USD 1.8 billion in service revenue and achieving a 68% renewal rate. Nordex mirrored the model by layering dynamic power-curve tuning and real-time yaw alignment into its Premium Service tier. Financial investors prefer the arrangement because it converts variable O&M cost into a fixed-fee profile, although it concentrates market power with OEMs that can hedge component-failure volatility.

National Repowering Incentives for >10-Year-Old Fleets

The U.S. Inflation Reduction Act extends a 30% investment tax credit for projects that raise capacity at least 20%, making it financially appealing to swap 2 MW machines from the early 2010s with 4–5 MW models. Germany earmarked EUR 1.2 billion in 2024 tenders for onshore repowering, while Spain trimmed permitting to six months for projects that keep grid-connection points. These carrots are driving demand for decommissioning, foundation diagnostics, and blade recycling, yet landfill bans across the EU underscore the urgency of scalable composite-recycling solutions.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent gearbox reliability issues in >5 MW class | –2.1% | Global; acute offshore Europe & Asia-Pacific | Short term (≤2 years) |

| Scarcity of blade-repair technicians & composite materials | –1.8% | Global; most severe in Asia-Pacific & North America | Medium term (2-4 years) |

| Revenue squeeze from expiring 20-year service contracts | –1.4% | Europe & North America | Medium term (2-4 years) |

| Logistics bottlenecks for offshore heavy-lift vessels | –1.6% | Europe (North Sea) & Asia-Pacific (Taiwan, Japan) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Persistent Gearbox Reliability Issues in >5 MW Class

Bearing micropitting, gear-tooth spalling, and lubrication contamination keep gearbox failures the largest single cause of downtime in the 6–8 MW fleet, driving emergency repairs that can reach USD 1.2 million when offshore crane mobilization and lost generation are counted. A 2024 peer-reviewed study covering 1,200 turbines found gearbox outages at 38% of total downtime hours despite representing only 12% of the component count. Siemens Gamesa increased warranty provisions by EUR 180 million after higher-than-expected bearing failures on its 8 MW platform. While ZF’s 2025 modular gearbox allows in-situ bearing swaps and trims intervention time by 40%, retrofitting legacy units remains uneconomical for most owners.

Scarcity of Blade-Repair Technicians & Composite Materials

Fewer than 8,000 technicians globally hold both rope-access and composite-layup credentials necessary for 70 m+ blade repairs, with vacancy rates at 18% in Europe and North America. Certification programs take 12–18 months, and turnover exceeds 25% as aerospace firms poach talent. Material shortages add another hurdle: Hexcel reported carbon-fiber lead times of 20 weeks in Q3 2025, up from 12 weeks a year earlier, because aerospace demand rebounded faster than production capacity. These twin constraints inflate repair costs by more than 30% and stretch maintenance backlogs.

Segment Analysis

By Location of Deployment: Offshore Complexity Drives Premium Pricing

Onshore installations represented 90.1% of wind turbine maintenance, repair & overhaul (MRO) market revenue in 2025, reflecting easier road access and lower labor rates. The segment’s average annual spend per turbine hovers near USD 35,000, with two scheduled maintenance visits each year and minimal vessel costs. In contrast, the offshore share of the wind turbine maintenance, repair & overhaul (MRO) market size is rising quickly, advancing at 28.3% CAGR through 2031 as developers install >15 MW turbines farther from shore. A single offshore turbine typically consumes USD 95,000 annually in MRO outlays, with vessel logistics absorbing almost half of that bill.[3]Ørsted, “Hornsea 2 Operational Update,” orsted.com

Floating-wind adds yet another cost layer. Dynamic mooring systems, pitch-roll platform motion, and scarcer weather windows require motion-compensated gangways and autonomous inspection drones. Japan’s JPY 12 billion program to build robotic blade-repair tools underscores industry recognition that conventional rope-access methods will not suffice offshore. As offshore work claims a larger slice of global capacity, specialized marine contractors are expected to capture outsized margins and consolidate a young supply chain still short on vessels and certified technicians.

Note: Segment shares of all individual segments available upon report purchase

By Service Type: Overhaul Dominance Reflects Fleet Aging

Overhaul work led 2025 spend with 46.4% of wind turbine maintenance, repair & overhaul (MRO) market share and is projected to record a 20.4% CAGR to 2031. Gearbox rebuilds alone can cost USD 300,000–700,000 per machine; generator rewinds add another USD 150,000–350,000. As fleets installed from 2010-2015 enter their second decade, operators accept those costs to avoid multi-million-dollar repowering budgets, driving the wind turbine maintenance, repair & overhaul (MRO) market size for overhaul services sharply upward. Maintenance tasks, such as scheduled inspections and consumable swaps, remain mandatory for warranty compliance but face stiff price competition from ISPs that underbid on labor-intensive work. Repair services stay episodic, triggered by lightning strikes or control-system faults, prompting OEMs to wrap them into availability guarantees that flatten revenue volatility.[4]Vestas Wind Systems, “Annual Report 2025,” vestas.com

OEMs fine-tune service tiers to capture value: Vestas’ 2025 menu offers quarterly oil analysis and annual blade borescope inspections within a premium plan that fetches 10–15% higher fees. ISPs counter by pooling spare-part inventories across multiple brands, lowering cycle times by 30–50% and winning multiyear contracts once thought impenetrable.

By Component: Power Electronics Surge on Grid-Code Mandates

Rotor blades absorbed 35.5% of 2025 component spend, reflecting frequent leading-edge erosion fixes and lightning-protection upgrades. Automated repair rigs like LM Wind Power’s UV-cured system cut labor hours by 60% and shrink repair windows to two days, valuable when turbines stand idle at USD 30,000-plus per day revenue loss. Nonetheless, power electronics and control systems will be the fastest-growing slice, expanding at a 22.5% CAGR as grid operators worldwide impose voltage-ride-through and reactive power rules. Germany’s updated technical guidelines oblige inverter retrofits on 18 GW of legacy turbines by 2027. Each upgrade costs USD 120,000–280,000 but opens access to ancillary service revenues that can repay half the investment within five years. The wind turbine maintenance, repair & overhaul (MRO) market size for power electronics thus exhibits outsized momentum versus mechanical components like towers or yaw systems.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific retained 53.9% of 2025 global revenue and is expected to clock a 17.6% CAGR through 2031. China’s 14th Five-Year Plan mandates controller upgrades and blade extensions across 50 GW of pre-2015 assets, lifting retrofit outlays and enlarging the wind turbine maintenance, repair & overhaul (MRO) market size in the region. Goldwind’s Inner Mongolia service hub, opened in October 2025, halves lead times for gearboxes and spares. India’s production-linked incentive grants INR 15 per kWh for overhauled turbines, encouraging owners to invest in multi-component rebuilds rather than decommission.

Europe remains a high-value arena owing to its 30 GW offshore fleet and strict operating codes. The UK’s Round 4 seabed awards compel developers to use domestic vessels for 60% of maintenance activity, spurring local supply-chain build-out. Germany and the Netherlands anchor demand for heavy-lift campaigns, while Spain accelerates onshore repowering with six-month permitting cycles.

North America benefits from the Inflation Reduction Act’s extended production tax credit, which keeps older turbines profitably spinning after gearbox, blade, and inverter upgrades. GE’s USD 320 million Indian onshore MRO contract in November 2025 illustrates OEM appetite for long-dated agreements that blend retrofit, overhaul, and analytics.

South America and the Middle East & Africa remain emerging contributors. Brazil’s ANEEL now enforces annual blade inspections and biennial oil analysis, spawning new ISP entrants. Morocco and South Africa are the first African markets to confront large-scale overhauls as 2017-2019 turbines approach mid-life.

Competitive Landscape

The wind turbine maintenance, repair & overhaul (MRO) market exhibits moderate concentration. The top five OEMs, Vestas, Siemens Gamesa, GE Renewable Energy, Goldwind, and Nordex, manage roughly 60% of global service backlogs via bundled contracts tied to equipment sales. Yet the expiration of 20-year agreements is loosening OEM grip, allowing ISPs such as Global Wind Service to win multibrand deals by fielding cross-trained technicians and stocking regional warehouses that cut part delivery by up to 50%.

Digitalization is the new battleground. Vestas’ 2024 purchase of Utopus Insights gave it proprietary analytics that integrate weather, price signals, and component health, optimizing maintenance for revenue yield rather than pure availability. Siemens Gamesa followed by buying a majority stake in Offshore Wind Services GmbH, securing scarce heavy-lift vessel capacity and marine expertise. GE and Envision push cloud-native digital twins that promise 18% reductions in unplanned downtime.

Barriers to entry are lower in niches such as blade recycling, gearbox oil analytics, and drone-based tower inspection. Venture-backed specialists leverage technology to offer risk-sharing contracts that guarantee sub-5-day response times. Yet skills deficits, especially in composite repairs, restrain market fragmentation by keeping high-complexity tasks with OEMs and large ISPs.

Wind Turbine Maintenance, Repair, And Overhaul (MRO) Industry Leaders

Vestas Wind Systems A/S

Siemens Gamesa Renewable Energy SA

General Electric Company

Suzlon Energy Ltd

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Andhra Pradesh Chief Minister N. Chandrababu Naidu secured a ₹20,000 crore investment from the Hinduja Group during a UK visit. The funds will support power expansion, renewable energy, EV manufacturing, and charging infrastructure, aligning with green energy goals and industrial growth.

- September 2025: Umiya Buildcon has introduced fully indigenous MRO-TEK CORNUS networking switches, contributing to India's self-reliant technology ecosystem. These switches can indirectly support wind turbine MRO operations by providing reliable digital infrastructure for monitoring and control systems in wind farms

- August 2025: Ocean Power Technologies expanded its UAE partnership with Unique Group to accelerate WAM-V uncrewed surface vehicle deployment across the Gulf. Unique Group will lease a WAM-V 22 and collaborate on fleet growth, with plans to establish a Maintenance, Repair, and Overhaul (MRO) hub in the UAE for offshore and subsea operations.

- March 2025: SANY Heavy Industry launched the ST230V skid steer loader in Canada, offering 360° steering, quick attachment changes, and strong performance for urban, municipal, and construction tasks. Its versatility and regulatory compliance enhance fleet efficiency, meeting the demand for service-friendly heavy machinery in maintenance and repair operations.

Global Wind Turbine Maintenance, Repair, And Overhaul (MRO) Market Report Scope

The Wind Turbine Maintenance, Repair, and Overhaul (MRO) Market involves inspection, servicing, repair, component replacement, and life-extension solutions for onshore and offshore wind turbines. Key activities include routine maintenance, predictive monitoring, gearbox and blade repairs, generator refurbishment, and major overhauls to ensure turbine performance and reliability throughout their operational lifecycle.

The global wind turbine maintenance, repair & overhaul (MRO) market is segmented by location of deployment, service type, component, and geography. By location of deployment, the market is segmented into onshore and offshore. By service type, the market is divided into maintenance, repair, and overhaul. By component, the market is segmented into rotor blades, nacelle & drivetrain, generator, and others. The report also covers the market size and forecasts for the market across major regions. Market sizing and forecasts have been done for each segment based on revenue (USD billion).

| Onshore |

| Offshore |

| Maintenance |

| Repair |

| Overhaul |

| Rotor Blades |

| Nacelle and Drivetrain |

| Generator |

| Tower |

| Power-Electronics and Control |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Finland | |

| Sweden | |

| Tukey | |

| Netherlands | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Vietnam | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Service Type | Maintenance | |

| Repair | ||

| Overhaul | ||

| By Component | Rotor Blades | |

| Nacelle and Drivetrain | ||

| Generator | ||

| Tower | ||

| Power-Electronics and Control | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Finland | ||

| Sweden | ||

| Tukey | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Vietnam | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the wind turbine maintenance, repair & overhaul (MRO) market today?

The market generated USD 216.03 billion in 2026 and is forecast to reach USD 452.33 billion by 2031, reflecting a 15.93% CAGR.

Which segment grows fastest within wind turbine MRO?

Overhaul services, covering gearboxes, generators, and blades, are projected to expand at 20.4% CAGR as turbines commissioned between 2010-2015 enter major-repair cycles.

Why is Asia-Pacific the leading region?

China's mandate to retrofit over 50 GW of pre-2015 turbines and India's incentive program for life-extension projects together account for 53.9% of 2025 global revenue and drive a regional CAGR of 17.6%.

What is the main technical challenge facing offshore MRO?

A shortage of heavy-lift vessels and motion-compensated cranes pushes day rates above USD 150,000 and can delay blade or nacelle interventions by up to six months.

How are OEMs adapting their business models?

They are shifting toward availability-based 'power-by-the-hour' contracts that bundle spares, labor, and digital monitoring, offering predictable fees while taking on performance risk.

Which new technology delivers the biggest maintenance savings?

AI-enabled predictive analytics integrated with digital twins can cut unplanned downtime by 15-22%, saving roughly USD 35,000 per turbine each year on emergency call-outs.