Market Overview

| Study Period | 2020 - 2031 |

|---|---|

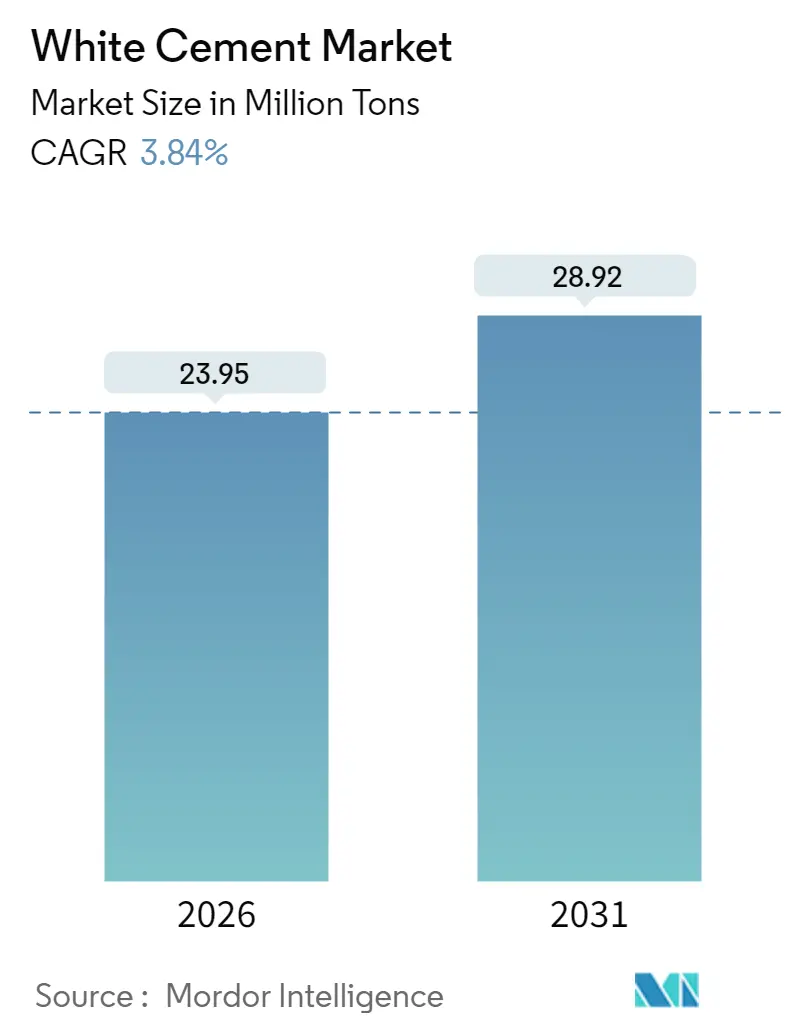

| Market Volume (2026) | 23.95 Million tons |

| Market Volume (2031) | 28.92 Million tons |

| Growth Rate (2026 - 2031) | 3.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

White Cement Market Analysis by Mordor Intelligence

The White Cement market is expected to grow from 23.06 million tons in 2025 to 23.95 million tons in 2026 and is forecast to reach 28.92 million tons by 2031 at 3.84% CAGR over 2026-2031. Demand acceleration flows from premium architectural finishes, heat-reflective roofing systems, and a steady pipeline of infrastructure mega-projects across Asia-Pacific and the Middle East. High urbanization rates, rising disposable incomes, and stricter green-building codes collectively reinforce the growth path of the white cement market. Producers with dedicated white cement kilns enjoy pricing power because the product requires low-iron raw materials and operates under energy-intensive conditions that restrict supply. Competitive differentiation centers on capacity optimization, supply-chain control of suitable limestone, and formulation innovation aimed at meeting heritage-restoration and high-performance structural requirements.

Key Report Takeaways

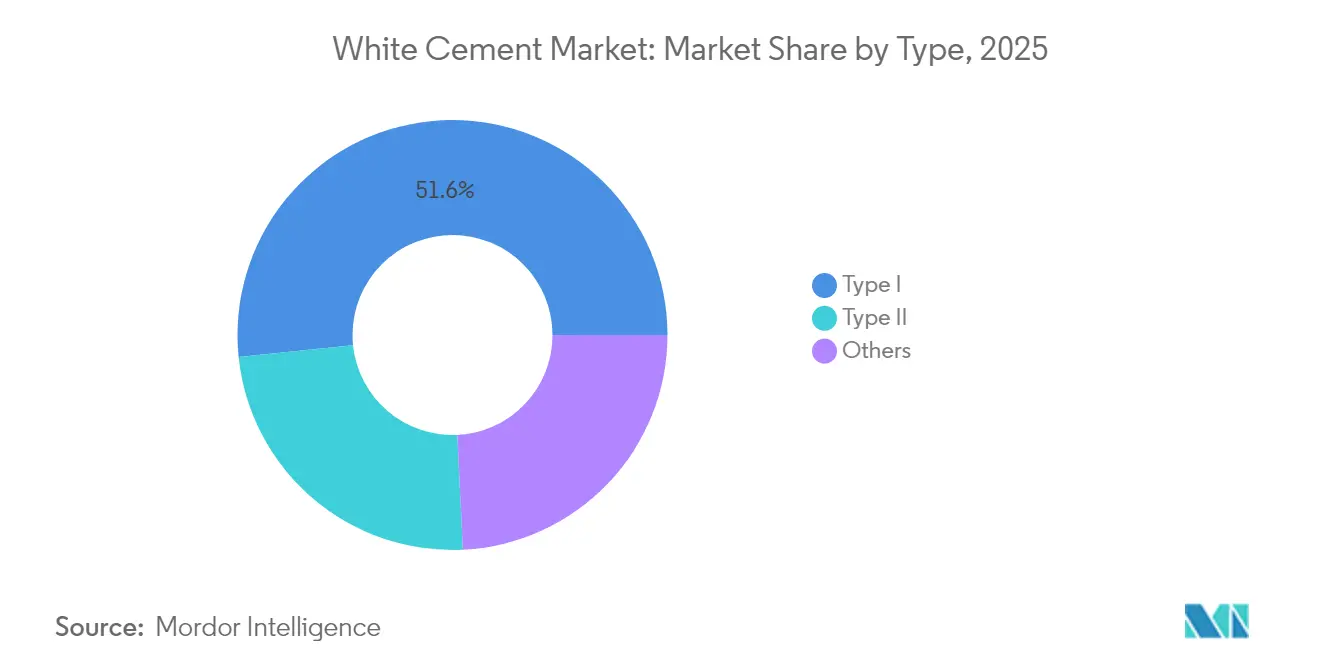

- By type, Type I accounted for 51.63% of white cement market share in 2025 and carries the fastest expansion pace at a 3.96% CAGR to 2031.

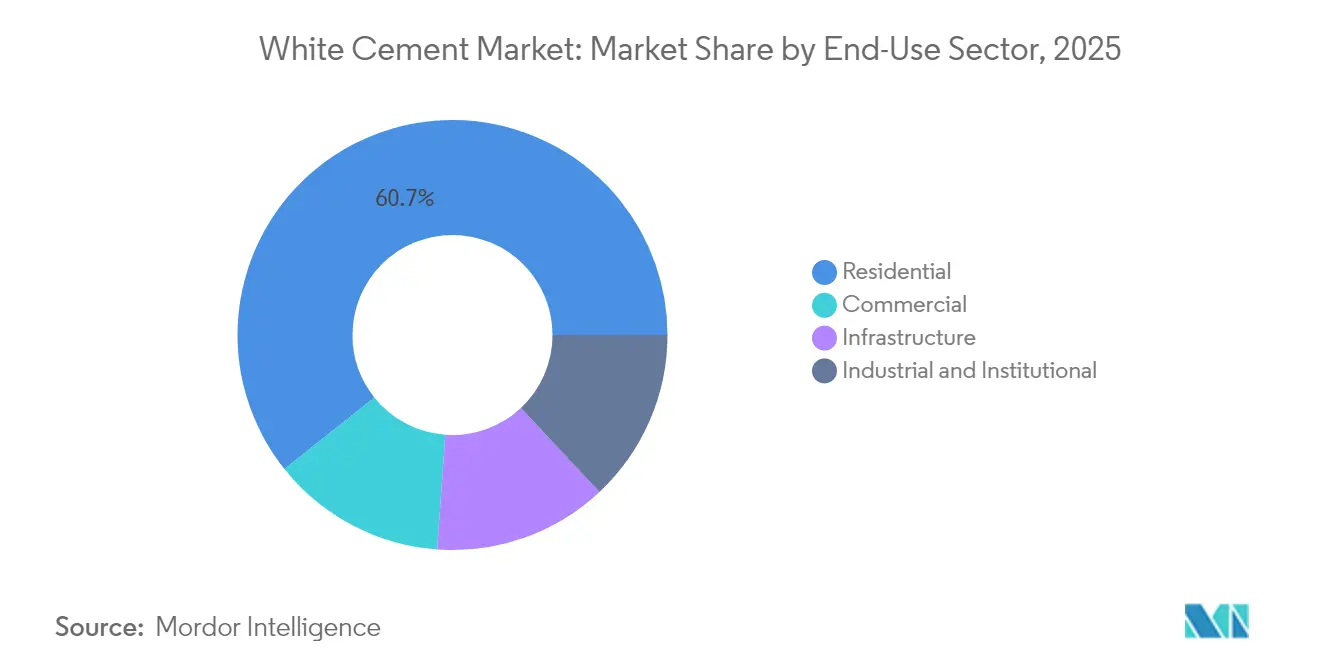

- By end-use, the residential sector generated 60.72% of demand in 2025 while leading growth at a 4.03% CAGR across the forecast horizon.

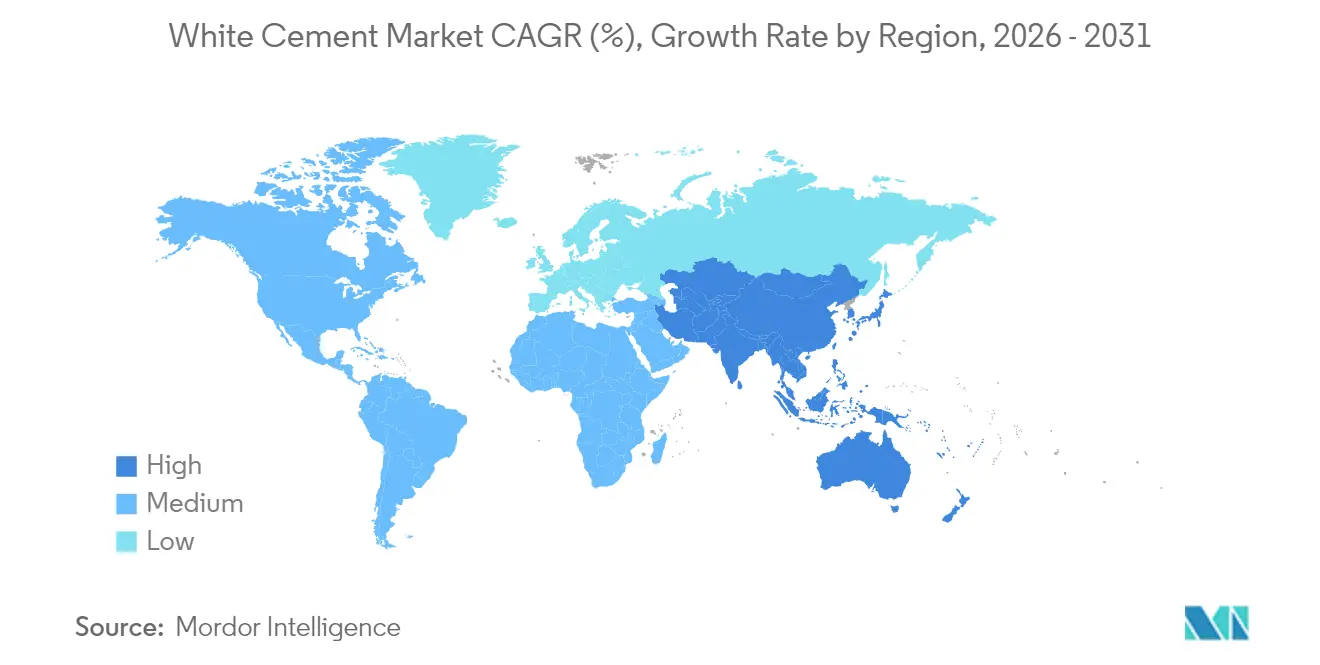

- By geography, Asia-Pacific held 47.55% of 2025 volume and is projected to log the highest regional CAGR of 4.33% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global White Cement Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decorative and architectural construction surge | +1.2% | Global, with concentration in APAC and MEA | Medium term (2-4 years) |

| Infrastructure mega-projects in Asia-Pacific and Middle East | +0.9% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Heat-reflective roofing demand in hot climates | +0.7% | MEA, South Asia, Australia | Medium term (2-4 years) |

| Heritage restoration premiumization | +0.4% | Europe, North America | Long term (≥ 4 years) |

| Low-carbon white PLC adoption | +0.3% | Europe, North America, with expansion to APAC | Long term (≥ 4 years) |

| E-commerce penetration in DIY segment | +0.2% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Decorative and Architectural Construction Surge

Architects specify white cement to create uniform, light-toned façades that differentiate high-rise residential towers and experiential retail complexes in densely populated cities. Rising urban land prices intensify the need for visually distinctive buildings, pushing contractors toward exposed white concrete that eliminates cladding costs. Decorative interior elements such as terrazzo floors and GRC panels further magnify volume uptake, as homeowners pursue premium materials that elevate property value. JK Cement recorded a jump in decorative-grade sales in 2024, fueled by metropolitan India’s luxury housing projects. Municipal regulations that promote higher solar-reflectance surfaces dovetail with private-sector aesthetic goals, making decorative usage a resilient demand pillar for the white cement market.

Infrastructure Mega-Projects in Asia-Pacific and Middle East

Flagship undertakings such as Saudi Arabia’s NEOM city, India’s Smart Cities Mission, and Belt and Road showcase projects specify white cement for stations, terminals, bridges, and cultural landmarks. Design guidelines emphasize glare reduction, thermal comfort, and enduring color stability—attributes amplified in white cement formulations. The UAE allocated USD 15.2 billion to public-sector infrastructure in 2024, channeling a sizable share toward airport concourses and metro systems that require bright, stain-resistant finishes[1]UAE Ministry of Infrastructure, “Infrastructure Investment Report 2024,” MOID.GOV.AE. Contractors favor long-term supply agreements with regional producers to mitigate import bottlenecks, extending the visibility of the white cement market pipeline well beyond typical building cycles. These mega-projects also set quality benchmarks that govern subsequent provincial and municipal developments, multiplying forward demand.

Heat-Reflective Roofing Demand in Hot Climates

Temperatures above 40 °C have become recurring across parts of South Asia, the Middle East, and northern Australia, prompting regulatory bodies to mandate cool-roof standards. White cement coatings offer solar-reflectance index values that lower roof surface temperatures by 15-25%, translating into double-digit reductions in energy bills for commercial facilities. Asian Paints augmented its coatings catalog with white cement-based reflectives in 2024, citing rapid uptake from industrial warehouses and school facilities. Policy incentives that couple building-permit approvals with energy-saving metrics embed heat-reflective roofing into mainstream construction, cementing another growth lever for the white cement market.

Heritage Restoration Premiumization

UNESCO guidelines require material compatibility and long-term durability when restoring historically significant masonry. Research conducted for lime-white cement blends demonstrates a 30% rise in service life over conventional restoration mixes. European conservators willingly pay 40-60% price premiums for bespoke white cement compositions that replicate the visual character of original stonework. Specialized artisans deploy micro-lime particles within white cement mortars to match century-old textures on cathedrals and museums. Although restoration volumes remain modest, margins are the highest across end-use categories, defending profitability even when energy prices spike. Consequently, producers invest in ISO-accredited laboratories to refine color consistency and pore-structure properties specific to cultural-heritage mandates.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and energy costs compared to grey cement | -1.1% | Global, particularly Europe and North America | Short term (≤ 2 years) |

| Scarcity of low-iron raw materials | -0.8% | Europe, North America | Medium term (2-4 years) |

| Colour constraints on alternative fuels and SCMs | -0.5% | Global, most acute in regions with strict environmental regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production and Energy Costs Compared with Grey Cement

Specialized kilns for white cement maintain higher firing temperatures and reject cost-saving alternative fuels that might contaminate color. Cementir Group disclosed that energy accounted for 35% of its white cement production expenditure in 2024, compared to 28% for grey cement. Carbon-pricing schemes compound the disadvantage in Europe, pushing operating margins downward during periods of electricity inflation. Public procurement for large-scale infrastructure often awards contracts to the lowest bidder, limiting the adoption of white cement unless thermal or visual criteria require it. Short-term profitability, therefore, hinges on hedging energy exposure and optimizing waste-heat recovery systems.

Scarcity of Low-Iron Raw Materials

White cement specifications cap the total iron oxide content below 0.3%, yet most limestone deposits exceed this threshold, forcing European producers to source from Morocco and Tunisia. Buzzi Unicem’s approval of an Italian kiln expansion in 2024 was contingent upon securing a dedicated North African quarry, illustrating how raw material logistics govern capacity decisions. Transporting high-purity limestone incurs additional freight costs, widening the price gap compared to regionally mined grey cement. New entrants face formidable expenses for geological exploration and environmental permitting hurdles, which protect incumbent market positions while also constraining aggregate volume growth within the white cement market.

Segment Analysis

By Type: Versatile Formulations Keep Type I at the Forefront

Type I generated 51.63% of 2025 output and is forecast to accelerate at a 3.96% CAGR, underscoring its role as the baseline grade across ornamental façades, terrazzo, and architectural precast elements. High workability and balanced compressive-strength trajectories simplify contractor logistics, allowing a single inventory item to span structural columns, wall panels, and interior plasters. Upgrading mixes with polymeric additives has expanded their applicability to medium-load bridge decks, encroaching on the territory once held by Type II. Manufacturers such as JK Cement introduced a new Type I blend in 2024, demonstrating higher early strength without sacrificing flow properties, marking an iterative progression that maintains market leadership. Continuous performance gains reinforce specifier confidence and discourage substitution, cementing Type I’s franchise in the white cement market.

Type II addresses aggressive environments where sulfate resistance, chloride permeability, or elevated compressive strength surpass Type I thresholds. Though representing a smaller slice of the white cement market, Type II secures premium pricing from coastal industrial plants, petrochemical docks, and desalination infrastructure. Pipeline documents for Saudi Arabia’s NEOM include tailored Type II mixes for power-block foundations, indicating niche but sticky demand. The “Others” category, encompassing restoration-grade, ultra-high-performance, and 3D-printing formulations, logged the fastest percentage growth in 2024. Nevertheless, patent activity surged 25% year-over-year, suggesting a long runway for specialized applications that could incrementally reshape type segmentation over the next decade.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-Use Sector: Residential Premiumization Dominates Consumption

Residential construction accounted for 60.72% of the 2025 tonnage, with 4.03% growth, as homeowners sought light-colored façades, polished concrete countertops, and low-maintenance exterior walls. Online DIY tutorials and e-commerce availability of 25 kg bags have democratized access, evidenced by an upswing in consumer-channel sales reported by Asian Paints. Higher disposable incomes in Tier-2 Chinese and Indian cities unlock new demand layers, while renovation cycles in North America enlarge replacements for weathered siding and stucco.

Commercial spaces—such as corporate campuses, shopping malls, and hospitality venues—rank as the second-largest end-use. Architects exploit white cement to align branding aesthetics with minimalist interiors and daylight-optimized lobbies. In 2024, multiple airport terminal upgrades in the UAE integrated exposed-aggregate white concrete to improve interior luminosity and passenger well-being. Industrial and institutional segments rely on antimicrobial coatings and reflective floors that facilitate sanitation, particularly in food-processing and healthcare facilities. Infrastructure uptake lags, confined mainly to heat-reflective pavements and utility rooftops in tropical zones. Still, pilot road segments in western India achieved surface-temperature gains of 8 °C over conventional asphalt, suggesting latent growth for the white cement market once cost hurdles are moderated.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Asia-Pacific region anchors nearly half of the global volume, reflecting a 47.55% share in 2025 and delivering the top regional CAGR of 4.33% through 2031. China's consumption is driven by continuous high-rise construction and provincial mandates on cool roofing. India trails but grows faster due to smart city investments and federal housing programs; Southeast Asian markets, such as Vietnam and Thailand, ride the upcycle in hospitality and retail capital expenditures, aided by favorable logistics costs for intra-ASEAN cement flows.

North America contributes steady, if less spectacular, gains, concentrated in renovation and heritage-preservation activities. U.S. building codes referencing cool-roof standards bolster demand for white cement in southern states, while Canadian commercial developers adopt light-colored façades for energy code compliance. Mexico taps cross-border supply chains to fuel industrial parks near the U.S. Sun Belt, ensuring stable inflows despite currency volatility.

Europe emphasizes conservation and premium architectural veneers. Energy costs and carbon trading pinch margins, yet policy incentives for recyclable, high-albedo materials provide partial offsets. The Middle East and Africa, though smaller in absolute tonnage, display robust momentum linked to flagship projects such as NEOM, Riyadh metro extensions, and South African warehouse hubs. Extreme climate amplifies thermal-reflectance advantages, nudging government specifications toward white cement for public-domain assets. South America remains nascent but promising, especially in Brazil where sustainability criteria in real-estate financing encourage the adoption of high-reflectance façades. Argentina’s commercial-office refurbishments also integrate white cement cladding to modernize 1970s-era buildings, highlighting a continental shift toward premium materials even amid macroeconomic flux.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The white cement market comprises a moderate concentration of regionally anchored champions, underpinned by proximity to raw materials. UltraTech’s acquisition of Wonder Cement’s 0.6 million-ton Rajasthan plant in April 2025 epitomizes inorganic expansion that consolidates feedstock control while enhancing downstream wall-putty integration[2]UltraTech Cement, “Annual Report 2024,” ULTRATECHCEMENT.COM. European multinationals allocate research and development spending to enhance energy efficiency and expand specialized capabilities, such as 3D printing cement. Patent filings for admixture compatibility and nano-pigment dispersion increased by 25% year-on-year, signaling a competitive shift toward formulation science. Import dependencies emerge in geographies lacking low-iron limestone, presenting export opportunities for North African and Middle Eastern players seeking to monetize their quarry holdings. Supply-chain disruptions, notably maritime freight spikes, thus reshape trade flows and occasionally allow spot-pricing surges that benefit integrated exporters.

White Cement Industry Leaders

Cementir Holding N.V.

JK Cement Ltd.

Çimsa Çimento

CEMEX S.A.B. de C.V.

HOLCIM

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: JK Cement approved an INR 4,805 crore plan to add 7 MTPA capacity, including a 4 MTPA clinker line in Jaisalmer and split grinding in Rajasthan and Punjab. This strategic expansion strengthens JK Cement’s position in the grey cement segment and supports its leadership in white cement and wall putty, with capacities of 1.12 million tonnes per annum and 1.33 million tonnes per annum, respectively.

- April 2025: UltraTech Cement Ltd. agreed to acquire Wonder Cement’s 0.6 MTPA white cement unit in Rajasthan for INR 235 crore to fortify raw-material proximity.

Global White Cement Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Type I, Type III are covered as segments by Sub Product. Asia-Pacific, Europe, Middle East and Africa, North America, South America are covered as segments by Region.By Type

| Type I |

| Type II |

| Others |

By End-Use Sector

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| Italy | |

| Spain | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Type | Type I | |

| Type II | ||

| Others | ||

| By End-Use Sector | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| Residential | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Spain | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- END-USE SECTOR - White cement consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of white cement including type I and type II, among others is considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF