| Study Period | 2019 - 2030 |

| Market Volume (2025) | 141.39 Million units |

| Market Volume (2030) | 179.42 Million units |

| CAGR | 4.88 % |

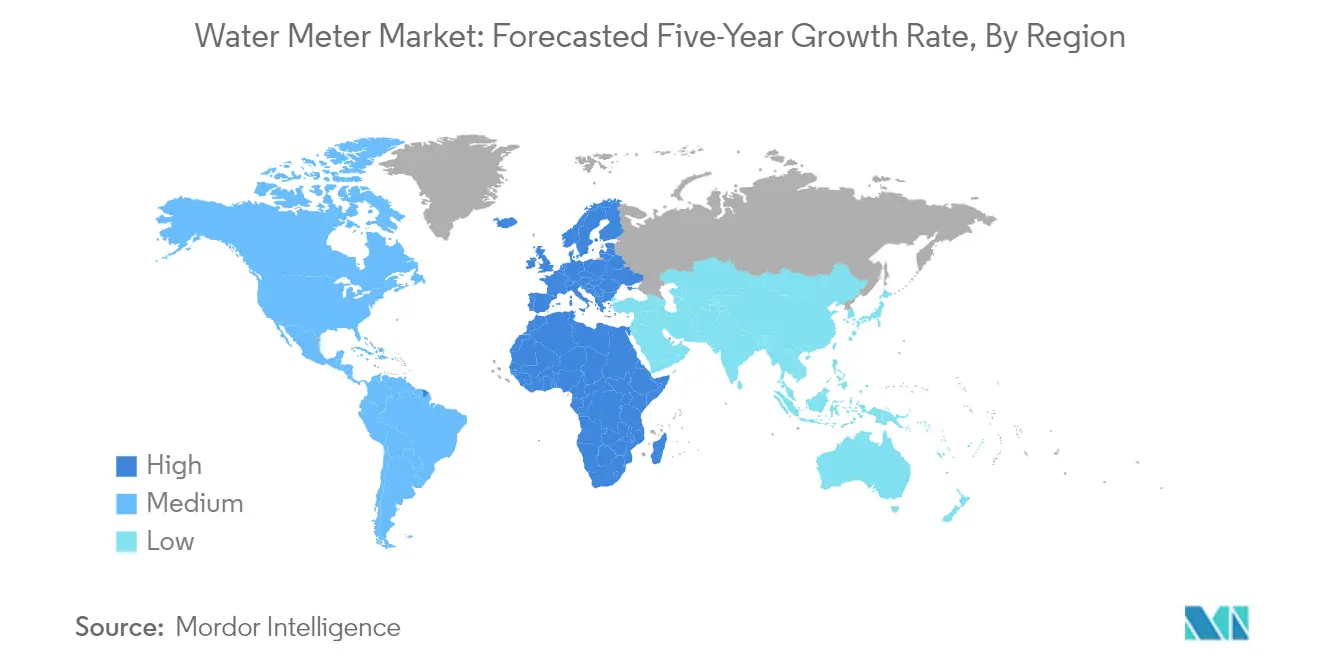

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

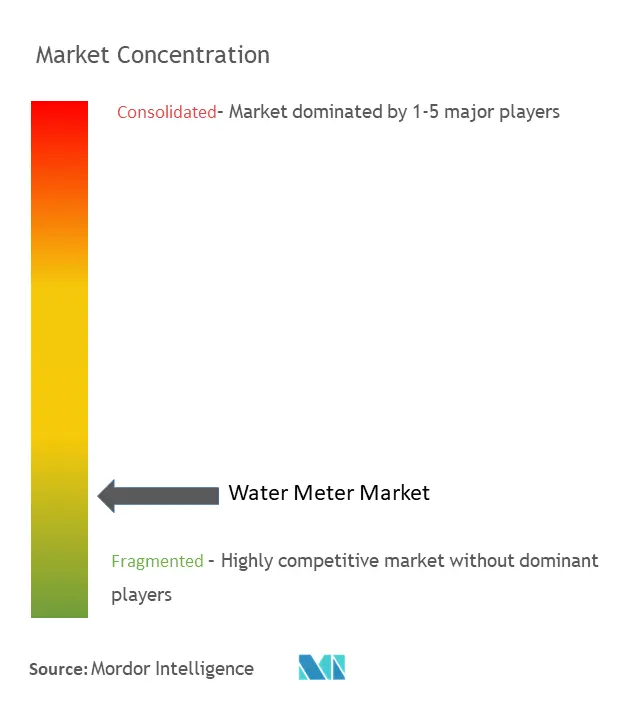

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Water Meter Industry Analysis

The Water Meter Industry in terms of shipment volume is expected to grow from 141.39 million units in 2025 to 179.42 million units by 2030, at a CAGR of 4.88% during the forecast period (2025-2030).

The water meter industry is experiencing significant transformation driven by escalating global water consumption patterns and resource scarcity concerns. According to LawnStarter's 2022 data, the United States leads global per-capita water consumption measurement at 2,842 cubic meters, followed by Canada, New Zealand, and Costa Rica, highlighting the critical need for effective water management system solutions. The increasing urbanization rates, industrial development, and changing consumption patterns have led to widespread water stress, with the United Nations projecting that approximately 1.8 billion people will be living in water-scarce regions by 2025. This evolving landscape has catalyzed the development of more sophisticated water metering device technologies and management approaches.

The technological evolution of water meters has progressed significantly, moving from basic mechanical devices to advanced smart water meter solutions incorporating IoT capabilities and real-time monitoring features. Various surveys indicate that smart water meter installations can achieve consumption reductions ranging from 20% to 50% within facilities, demonstrating the tangible impact of these technological advancements. The integration of technologies such as Silicon Labs' Low Duty Cycle optimization and ultra-low power SoC design has enhanced operational efficiency, enabling digital water meter solutions to function for up to ten years on a single battery while providing continuous monitoring capabilities.

The industry is witnessing a notable shift in material selection and manufacturing processes, with an increasing preference for specialty polymers over traditional metals like copper and brass. These advanced materials offer superior benefits, including better corrosion resistance, enhanced strength at higher temperatures, and elimination of heavy metal contamination risks in tap water. Recent innovations in network-enabled ultrasonic water flow meter technology, miniaturization of electronics, and sensor technology have enabled the integration of additional functionalities such as temperature monitoring, leak detection, and water quality assessment, significantly expanding the application scope of water meters.

Success stories from utility providers demonstrate the transformative impact of advanced water metering device solutions. For instance, Manila Water in the East Zone of Metro Manila achieved one of Asia's lowest non-revenue water rates, reducing it from 63% to 12.69% through the implementation of proactive technical solutions, including network reconfiguration and comprehensive meter management programs. In Europe, Germany has emerged as a leading market with approximately 45 million installed water meters representing a production value of nearly EUR 1 billion, while Spain faces critical challenges with around 27% of its regions experiencing drought classified as "alert" or "emergency" in 2023, driving urgent adoption of advanced metering solutions.

Water Meter Industry Trends

Growing Investment in Water Infrastructure Upgradation Activities

The global water infrastructure sector is witnessing unprecedented investment levels as governments and utilities address growing water management challenges. In March 2023, India's Jal Shakti Ministry announced plans to invest more than USD 240 billion in the country's water sector, focusing on partnerships with start-ups, private innovators, and water-user associations to ensure universal drinking and sanitation water access. Similarly, in March 2023, Germany and the Netherlands launched the Urban Water Catalyst Initiative, with Germany providing EUR 32 million and the Netherlands contributing EUR 10 million to support wastewater utilities and municipal water management system improvements in Global South cities.

China has significantly accelerated its investment in water conservation projects, with a total investment of CNY 921.1 billion (~USD 130 billion) announced in late 2022. The country initiated work on 45 major projects with a total investment of CNY 424.9 billion, demonstrating a strong commitment to infrastructure modernization. In the United States, the government announced over USD 140 million for water conservation and efficiency projects in April 2023, supporting 84 projects across 15 western states that are expected to conserve over 230,000 acre-feet of water annually.

Understand The Key Trends Shaping This Market

Download PDF

Growth in Adoption Rate of Second-Generation Water Meters

The water meter industry is experiencing rapid technological transformation with the increasing adoption of second-generation advanced metering infrastructure featuring advanced capabilities. These modern devices incorporate sophisticated communication modules and IoT-enabled advanced metering infrastructure (AMI), offering enhanced capabilities in leak detection, real-time visualization, and machine-to-machine communications. Utility providers are actively exploring and implementing low-power, wide-area network cellular communication technologies like narrowband (NB) and long-range (LoRa)-IoT to optimize efficiency and extend the battery life of smart water meter devices.

Recent developments showcase the industry's innovation trajectory, with companies launching breakthrough solutions. In May 2023, Honeywell introduced its Next Generation Cellular Module (NXCM), enabling the upgrade of legacy water meters into smart meters without additional infrastructure investment. Similarly, in June 2023, Xylem Inc. launched Cordonel, an innovative ultrasonic C&I water flow meter featuring patented technology with three measurement channels that seamlessly integrate with the FlexNet communication network, providing real-time accurate readings to customers and utility providers. These advancements are complemented by the growing availability of supporting infrastructure, with GSMA projecting 5G networks to cover one-third of the global population by 2025.

Segment Analysis: By Type

Basic Water Meter Segment in Water Meter Market

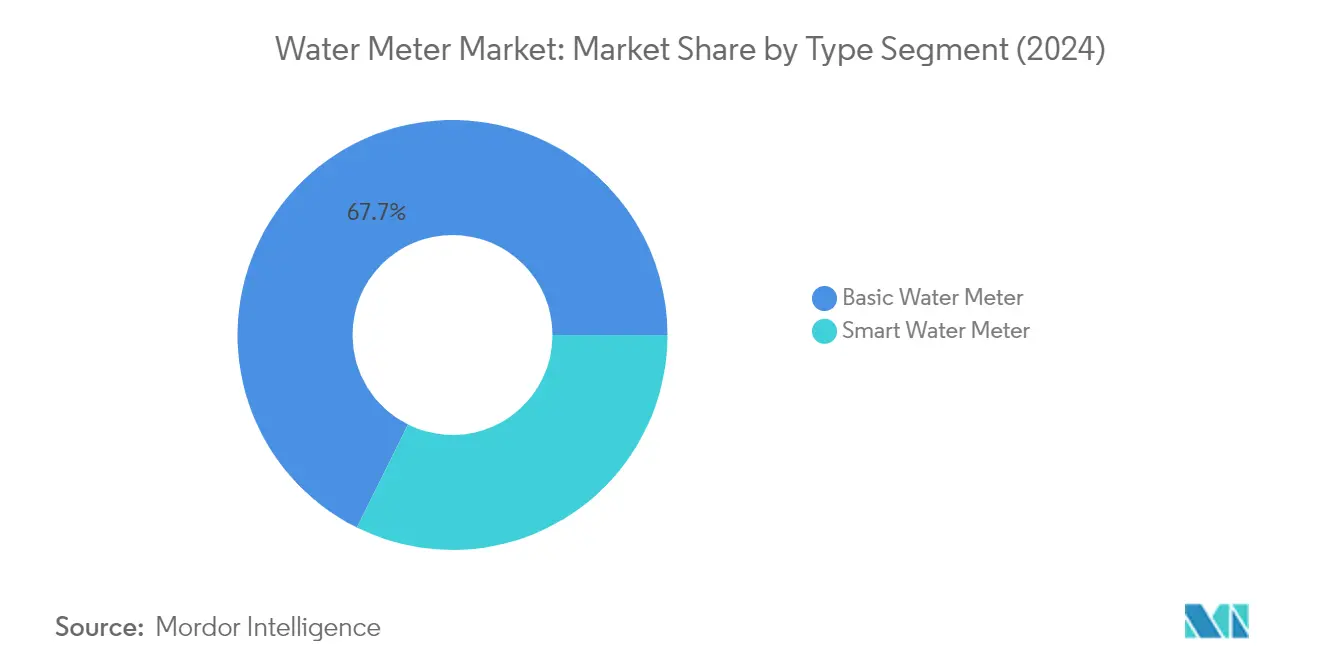

The Basic water meter segment continues to dominate the global water meter market, holding approximately 68% market share in 2024. This significant market position is primarily attributed to the segment's widespread adoption across developing economies where price sensitivity is relatively higher. Basic water meters maintain their strong presence due to their easy integration capabilities with legacy infrastructure and lower initial costs compared to smart water meters. These meters are particularly prevalent in regions where traditional infrastructure still forms the backbone of water management systems. The segment's dominance is also supported by the practical impossibility of completely eliminating basic water meters from the ecosystem, as they serve as reliable solutions for areas where advanced technological infrastructure is not yet feasible or necessary.

Smart Water Meter Segment in Water Meter Market

The smart water meter segment is experiencing remarkable growth, projected to expand at approximately 11% during the forecast period 2024-2029. This accelerated growth is driven by the increasing adoption of IoT-enabled advanced metering infrastructure (AMI) and enhanced capabilities in leak detection and real-time visualization. The segment's growth is further propelled by technological advancements in communication modules, with utilities exploring and adopting low-power, wide-area network cellular communication technologies like narrowband (NB) and long-range (LoRa)-IoT to enhance efficiency and battery life. Smart water meters are gaining traction due to their ability to provide dynamic water billing, eliminate manual supervision, and support real-time, web-based metering that helps utility providers automatically generate and share bills with consumers efficiently. Additionally, the integration of automatic meter reading systems in smart water meters enhances operational efficiency.

Water Meter Market Geography Segment Analysis

Water Meter Market in North America

North America represents a mature water meter market, characterized by advanced infrastructure and high adoption rates of smart metering technologies. The region's water meter industry is driven by factors such as aging water infrastructure, an increasing focus on water conservation, and growing investments in smart city initiatives. The United States and Canada are the key markets in this region, with both countries showing a strong commitment to modernizing their water management systems through the implementation of advanced metering solutions.

Water Meter Market in United States

The United States dominates the North American water meter market, accounting for approximately 88% of the regional market in 2024. The country's market is primarily driven by stringent regulations pertaining to water conservation and increasing government initiatives toward adopting smart meters. Several states within the region have started facing issues related to water availability, drawing increased attention from consumers, utility suppliers, and government organizations. The presence of major water meter manufacturers and strong technological infrastructure further strengthens the country's position in the market.

Water Meter Market in Canada

Canada represents the fastest-growing market in North America, with a projected growth rate of approximately 6% during 2024-2029. The country's growth is fueled by increasing urbanization and the growing need for efficient water management systems. Despite having abundant freshwater resources, only a smaller percentage is considered renewable, pushing utilities to focus on the efficient management of water consumption. The country has witnessed several smart meter implementation projects across major cities, including Ottawa, Toronto, and Quebec, with newer cities joining the trend to upgrade their residential water meter management infrastructure.

Water Meter Market in Europe

Europe represents a significant water meter market, with countries across the region showing a strong commitment to water conservation and management. The region's market is characterized by high technological adoption rates and the presence of several leading water meter manufacturers. The United Kingdom, France, Spain, and Italy are the key markets in this region, each contributing significantly to the regional market dynamics with their unique water management initiatives and infrastructure development programs.

Water Meter Market in United Kingdom

The United Kingdom leads the European water meter market, holding approximately 25% of the regional market share in 2024. The country's dominant position is supported by several initiatives from the government and utility suppliers to drive efficiency and bring sustainability to the water supply industry. The UK's water utilities are actively working on replacing traditional meters with smart meters, particularly as the country faces an increased risk of drought and the need for better water management becomes more critical.

Water Meter Market in France

France emerges as the fastest-growing market in Europe, with a projected growth rate of approximately 6% during 2024-2029. The country's growth is driven by increasing water conservation needs and government initiatives such as the Water Conservation Plan announced to reduce water consumption across all sectors. The presence of established water meter manufacturers and early adoption of smart metering technologies has created a strong foundation for market growth. The country has also witnessed significant developments in supporting infrastructure for smart residential water meter systems.

Water Meter Market in Asia-Pacific

The Asia-Pacific region represents a dynamic water meter market, characterized by rapid urbanization, a growing population, and an increasing focus on water conservation. The region encompasses diverse markets, including China, Japan, and New Zealand, each with its unique water management challenges and solutions. The market is witnessing significant developments in smart metering technologies and supporting infrastructure, particularly in urban areas where water management has become a critical concern.

Water Meter Market in China

China dominates the Asia-Pacific water meter market, holding a strong presence in the global water meter industry value chain. The country's market is driven by its large population, growing urbanization rate, and significant investments in water supply infrastructure. China has recently strengthened its approach to the comprehensive utilization and protection of water resources, with an increased focus on water consumption management and leakage reduction. The presence of numerous local manufacturers and strong manufacturing capabilities further reinforces China's position in the market.

Water Meter Market in New Zealand

New Zealand, despite being a smaller market, demonstrates significant potential in the water meter industry. The country's market is characterized by high urbanization rates and growing awareness about water conservation. Several cities are undertaking water meter implementation projects, with Auckland leading the way in smart meter adoption. The country's utilities are increasingly focusing on modernizing their water management systems through the adoption of smart metering technologies and advanced data analytics solutions.

Water Meter Market in Rest of the World

The Rest of the World region, encompassing the Middle East, Africa, and Latin America, presents significant opportunities in the water meter market. These regions are characterized by growing water scarcity concerns and increasing investments in water infrastructure modernization. In the Middle East, countries are focusing on efficient water management due to limited freshwater resources, while African nations are working on improving their water supply infrastructure. Latin America is witnessing growing adoption of smart municipal water meter systems, particularly in urban areas. Saudi Arabia emerges as the largest market in this region, while Mexico shows the fastest growth potential, driven by various smart meter deployment initiatives and water conservation programs.

Get Analysis on Important Geographic Markets

Download PDF

Water Meter Industry Overview

Top Companies in Water Meter Market

The water meter companies market features established players like Badger Meter, Diehl Metering, Honeywell, Sensus (Xylem), Neptune Technology, and Landis+Gyr leading innovation and market development. These companies are increasingly focusing on developing smart water metering solutions incorporating IoT connectivity, advanced sensors, and data analytics capabilities to address growing water conservation needs. Strategic partnerships with technology providers and utilities are becoming commonplace to enhance product capabilities and expand market reach. Companies are investing significantly in R&D to develop ultrasonic measurement technologies, leak detection features, and communication protocols like NB-IoT and LoRa. Manufacturing facilities are being modernized with Industry 4.0 concepts to improve operational efficiency and product quality. Geographic expansion, particularly in the emerging markets of Asia-Pacific and the Middle East, remains a key growth strategy alongside the development of comprehensive end-to-end water management solutions.

Market Dominated by Diversified Technology Leaders

The competitive landscape is characterized by a mix of large diversified technology conglomerates like Honeywell and specialized water technology companies like Badger Meter and Neptune Technology. These established players leverage their strong R&D capabilities, extensive distribution networks, and long-standing relationships with utilities to maintain market share in water meters. The market shows moderate consolidation with major players actively pursuing strategic acquisitions to expand their technological capabilities and geographic presence. Regional players, particularly in Asia-Pacific, maintain strong positions in their local markets through cost advantages and established customer relationships.

The industry is witnessing increased merger and acquisition activity as companies seek to enhance their smart metering capabilities and expand their geographic footprint. Large players are acquiring specialized technology companies to strengthen their IoT and analytics capabilities, while also pursuing regional players to gain market access. Strategic partnerships between meter manufacturers, communication technology providers, and software companies are becoming increasingly common to develop integrated smart metering solutions. The market is also seeing new entrants, particularly in the smart water meter market segment, bringing innovative technologies and business models.

Innovation and Integration Drive Market Success

For incumbent players to maintain and expand their market share, continuous investment in R&D and product innovation remains crucial, particularly in developing smart metering solutions with advanced connectivity and analytics capabilities. Building comprehensive end-to-end solutions that integrate hardware, software, and services is becoming increasingly important. Companies need to strengthen their relationships with utilities through enhanced after-sales support and service capabilities while also developing flexible business models to address varying customer needs. Geographic expansion through strategic partnerships and localization of products for specific market requirements is essential for growth.

New entrants and challenger companies can gain ground by focusing on niche market segments or specific technological innovations, particularly in the growing smart meter segment. Developing cost-effective solutions for emerging markets while maintaining quality standards presents a significant opportunity. The regulatory environment, particularly regarding water conservation and smart city initiatives, continues to favor advanced metering solutions, though companies must ensure compliance with evolving standards. While the risk of substitution is relatively low due to the essential nature of water metering, companies must continue to innovate to address changing customer needs and technological advancement. The concentrated nature of the utility customer base necessitates strong relationship management and customized solution development capabilities.

Water Meter Industry Leaders

-

Badger Meter Inc.

-

Diehl Metering GMBH (Diehl Stiftung & Co. KG)

-

Ningbo Water Meter (Group) Co. Ltd

-

Honeywell International Inc.

-

BM Water Meters

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Water Meter Industry News

- September 2023 - Honeywell announced the integration of quantum computing hardware encryption Keys on smart utility meters to protect the end user's data from increasing cyber threats. To help strengthen reliability and trust in a digitalized energy sector, Honeywell will use the Quantum Origin technology of Quantinuum. To ensure that natural gas, water, and electricity infrastructures are maintained for residential and commercial purposes, the enhanced security utility meter establishes a new benchmark that protects against data breaches.

- June 2023 - Xylem officially announced the opening of its new testing facility for bulk water meters in Laatzen, Germany. The new facility is a significant investment in its metrology branch, Sensus, and a dedicated commitment to the success of the latest ultrasonic bulk water meter, Cordonel.

- Cordonel and other bulk water meters in this new test bench may be tested in accurate installation and extreme environmental conditions due to its U0D0 section and integrated climate chamber.

Water Meter Industry Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Technology Evolution

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macro Trends on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Growing Investment in Water Infrastructure Upgradation Activities

- 5.1.2 Growth in Adoption Rate of Second-generation Water Meters

-

5.2 Market Challenges/Restraints

- 5.2.1 High Installation Cost and Longer ROI Period

- 5.2.2 Longer Replacement Cycle of Water Meters

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Smart Water Meter

- 6.1.2 Basic Water Meter

-

6.2 By Geography***

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada and Central America

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 France

- 6.2.2.3 Spain

- 6.2.2.4 Italy

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 Australia and New Zealand

- 6.2.3.3 Japan

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Badger Meter Inc.

- 7.1.2 Diehl Metering GMBH (Diehl Stiftung & Co. KG)

- 7.1.3 BM Water Meters

- 7.1.4 Ningbo Water Meter (Group) Co. Ltd

- 7.1.5 Honeywell International Inc.

- 7.1.6 Sensus USA Inc. (Xylem Inc.)

- 7.1.7 Master Meter Inc. (ARAD Group)

- 7.1.8 Neptune Technology Group Inc.

- 7.1.9 Tongtuo Water Meter Factory

- 7.1.10 Suntront Tech Co. Ltd

- 7.1.11 Azbil Kimmon Co., Ltd.

- 7.1.12 Itron Inc.

- 7.1.13 Kamstrup As

- 7.1.14 Landis+GYR Group AG

- *List Not Exhaustive

8. FUTURE OUTLOOK OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Water Meter Industry Industry Segmentation

Water meters are devices used to measure the quantity/volume of water passing through a supply pipeline/outlet, which may include the primary water supply pipeline for an entire facility or a sub-zone. Measurements can be done in units, including cubic feet or gallons, among others.

The scope of the study focuses on the market analysis of water meters across the world, and market sizing encompasses the unit shipment of both smart and basic types of water meters. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period. The study also analyzes the overall impact of macro trends on the ecosystem. The scope of the report encompasses market sizing and forecast for segmentation by type and geography.

The water meter market is segmented by type (smart water meter, basic water meter) and by geography (North America (United States, Canada and Central America), Europe (United Kingdom, France, Spain, Italy, Rest of Europe), Asia-Pacific (New Zealand, China, Japan, Rest of Asia-Pacific), and Rest of the World). The market sizes and forecasts are provided in terms of shipment volume (shipment units) for all the above segments.

| By Type | Smart Water Meter | ||

| Basic Water Meter | |||

| By Geography*** | North America | United States | |

| Canada and Central America | |||

| Europe | United Kingdom | ||

| France | |||

| Spain | |||

| Italy | |||

| Asia | China | ||

| Australia and New Zealand | |||

| Japan | |||

| Latin America | |||

| Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Water Meter Industry Research FAQs

How big is the Water Meter Market?

The Water Meter Market size is expected to reach 141.39 million units in 2025 and grow at a CAGR of 4.88% to reach 179.42 million units by 2030.

What is the current Water Meter Market size?

In 2025, the Water Meter Market size is expected to reach 141.39 million units.

Who are the key players in Water Meter Market?

Badger Meter Inc., Diehl Metering GMBH (Diehl Stiftung & Co. KG), Ningbo Water Meter (Group) Co. Ltd, Honeywell International Inc. and BM Water Meters are the major companies operating in the Water Meter Market.

Which is the fastest growing region in Water Meter Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Water Meter Market?

In 2025, the Asia Pacific accounts for the largest market share in Water Meter Market.

What years does this Water Meter Market cover, and what was the market size in 2024?

In 2024, the Water Meter Market size was estimated at 134.49 million units. The report covers the Water Meter Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Water Meter Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Water Meter Industry Research

Mordor Intelligence provides comprehensive industry analysis and market research solutions for the water meter market, covering various segments like smart water meters, digital water meters, and advanced metering infrastructure. Our detailed market outlook encompasses industry size, growth trends, and competitive landscape analysis of leading water meter companies across residential, commercial, and industrial applications. The report offers invaluable insights into emerging technologies like ultrasonic water meters and water management systems, along with detailed market segmentation and forecast data, all conveniently accessible in an easy-to-read report PDF format.

Beyond market research, our consulting expertise extends to strategic areas crucial for stakeholders in the water meter industry. We assist clients with technology scouting for innovative metering solutions, regulatory assessment of water measurement standards, and comprehensive analysis of water monitoring systems implementation strategies. Our services include customer need analysis for different meter types, from mechanical water meters to electromagnetic water meters, product positioning assessments for new smart metering solutions, and evaluation of potential partners and distributors in target markets. Through B2B surveys and data analytics, we help clients understand evolving market dynamics and optimize their competitive positioning in the global water metering landscape.