Market Overview

| Study Period | 2020 - 2030 |

|---|---|

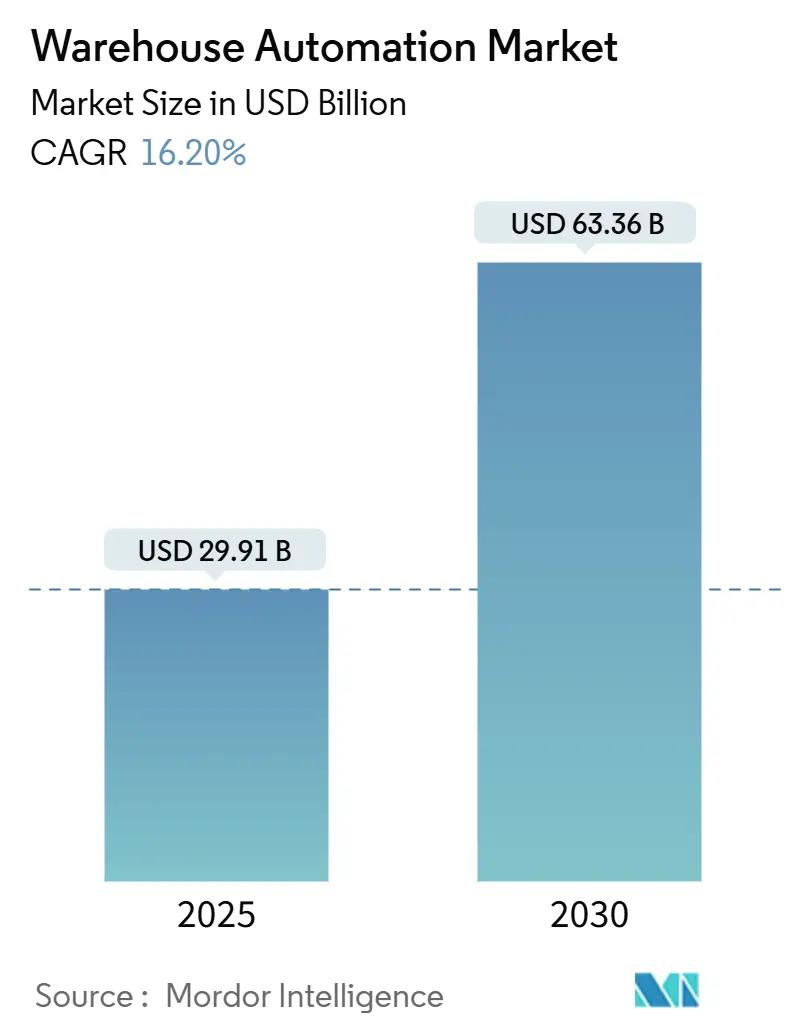

| Market Size (2025) | USD 29.91 Billion |

| Market Size (2030) | USD 63.36 Billion |

| Growth Rate (2025 - 2030) | 16.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Warehouse Automation Market Analysis by Mordor Intelligence

The warehouse automation market size is estimated at USD 29.91 billion in 2025 and is projected to advance to USD 63.36 billion by 2030, reflecting a robust 16.20% CAGR. Growth rides on three converging currents: sustained e-commerce volume, persistent labor scarcity, and subscription-based robotics services that lower capital barriers. Hardware—particularly AS/RS installations and conveyor infrastructure—still accounts for most spending, yet software layers that synchronize people, robots, and inventory are scaling faster as fulfillment centers move toward data-driven orchestration. North America keeps its lead position by pairing mega-warehouse construction with reshoring incentives, while the Asia–Pacific region is accelerating on the back of urban consumption and policy support despite a cyclical slowdown in China. Autonomous mobile robots (AMRs) illustrate the sector’s shifting economics, delivering payback in under 24 months and ROI above 250% in live deployments.[1]MHL News, "How to Automate Diverse AMR and AGV Fleets for Efficiency", mhlnews.com

Key Report Takeaways

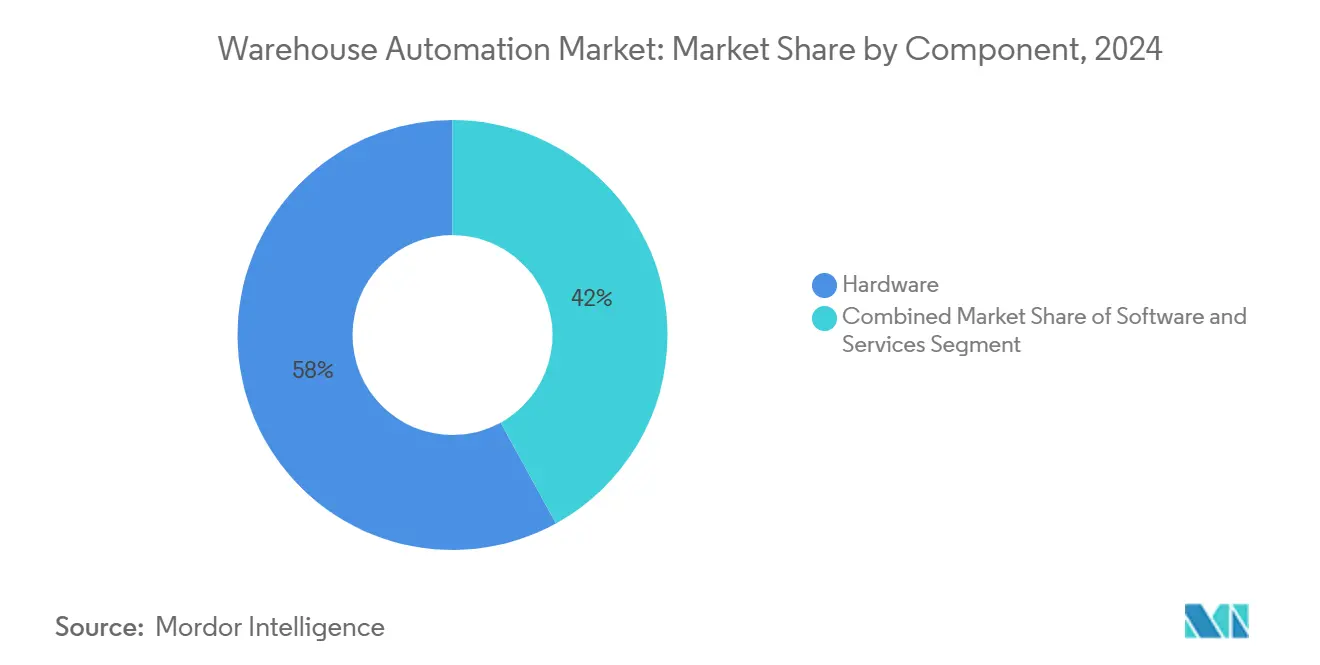

- By component, hardware captured 58% of the warehouse automation market share in 2024, whereas software is set to post the highest 17% CAGR through 2030.

- By technology, AS/RS led with 30.5% of warehouse automation market share in 2024; mobile robots are forecast to expand at a 20.5% CAGR to 2030.

- By end-user industry, retail & e-commerce held 28% revenue share in 2024, while e-grocery is projected to grow at 18.3% CAGR through 2030.

- By warehouse size, medium facilities (50–200 k sq ft) commanded 37% of the warehouse automation market size in 2024; mega sites (>500 k sq ft) are advancing at a 17.2% CAGR to 2030.

- By ownership, company-owned sites represented 52% of the 2024 warehouse automation market size, but 3PL facilities are expected to record a 16.4% CAGR to 2030.

- KION Group, Daifuku, and Symbotic collectively controlled ~22% of global revenue in 2024, underscoring a moderately consolidated field.

Global Warehouse Automation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom & last-mile expectations | +4.2% | North America, APAC | Medium term (2-4 years) |

| Labour shortages & wage inflation | +3.8% | North America, EU; spreading to APAC | Short term (≤ 2 years) |

| Rapid ROI from plug-and-play AMR/AGV fleets | +2.9% | Global | Short term (≤ 2 years) |

| Robotics-as-a-Service (RaaS) lowering cap-ex | +2.1% | North America, EU | Medium term (2-4 years) |

| ESG-linked energy-efficiency mandates | +1.7% | EU lead; NA follow | Long term (≥ 4 years) |

| Reshoring-driven mega hubs | +1.5% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

E-commerce boom & last-mile expectations

Order volumes have tripled since 2020 in flagship omnichannel facilities, forcing operators to engineer dense micro-fulfillment outposts that handle 300,000+ orders per year while keeping promise windows under two hours.[2]Honeywell, “Honeywell Announces Intent to Separate Automation and Aerospace,” honeywell.com Retailers now prioritize orchestration layers that can throttle capacity up or down without a physical re-layout. Honeywell’s Momentum WES is emblematic, dynamically batching waves and interleaving replenishment and returns to maintain 99.9999% accuracy and a 25% cycle-time reduction.

Labour shortages & rising wage inflation

More than half of warehouse operators cite unfilled headcount as the top automation catalyst, and recent regulatory caps on overtime—for example, Japan’s 960-hour annual limit for truck drivers—intensify the squeeze. Wage bills climbed 7–9 % YoY in 2024 for U.S. general warehouse labor, reinforcing ROI math that favors collaborative robotics. Employers respond by funding upskilling programs; 46% now subsidize robotics certificates to enhance human-machine teaming.

Rapid ROI from plug-and-play AMR/AGV fleets

Modern AMRs deploy in weeks, not quarters, because they require no fixed guide-path infrastructure. Case studies show a 42% five-year OPEX reduction relative to manual processes and an eight-month payback where four operators were redeployed to value-added tasks.

Robotics-as-a-Service lowering cap-ex hurdles

Seventy-two percent of logistics firms plan to adopt RaaS contracts that swap multi-million-dollar cap-ex for usage-based OPEX, unlocking automation for mid-tier shippers previously priced out of the market. Toyota Industries earmarked JPY 1.5 trillion (USD 10.2 billion) for flexible services to ride this payment-model pivot.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cap-ex & long payback for fixed systems | -2.8% | Global; hits SMEs hardest | Medium term (2-4 years) |

| Legacy IT & WMS integration complexity | -1.9% | North America, EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High upfront cap-ex & long pay-back for fixed systems

Traditional AS/RS lanes cost USD 50,000–80,000 per unit and often tie up capital for 30 months before breakeven. SMEs mitigate by retrofitting existing racking or buying refurbished equipment to sidestep greenfield costs.

Legacy IT & WMS integration complexity

Aging host systems hamper real-time data exchange with robotics fleets. Operators face downtime risk during cut-over, and 61% cite change-management—not hardware—as the single biggest upgrade obstacle. Cyber-risk amplifies concerns as every robot, scanner, and gateway enlarges the attack surface.

Segment Analysis

By Component: Hardware Dominance Amid Software Acceleration

Hardware still anchors 58% of the warehouse automation market in 2024, reflecting sunk investments in conveyors, shuttles, and gantry pick systems that form the physical core of modern fulfillment. The segment is forecast to trail overall growth, however, as the intelligence layer outpaces mechanics. Software revenues are growing at a 17% CAGR, with warehouse execution systems assuming the role of traffic cop for multi-vendor robotic fleets. Services contribute the balance, driven by predictive maintenance and continuous improvement consulting for brownfield sites. AutoStore’s CarouselAI shows that coding, not iron, increasingly differentiates value propositions.

The pivot to code-centric differentiation indicates that future winners will monetize optimization algorithms rather than hardware margins. The global WMS software pool reached USD 11.6 billion in 2024 and remains on a low double-digit growth trajectory, underscoring the appetite for orchestration that spans inbound, outbound, and returns. As subscription models proliferate, vendors that bundle analytics, cybersecurity, and uptime guarantees into service-level agreements position themselves for stickier recurring revenue.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: AS/RS Leadership Challenged by Mobile Robot Surge

AS/RS maintained a 30.5% warehouse automation market share in 2024, favored in high-throughput environments that prize cube utilization. Yet the momentum baton is shifting: mobile robots are penciled in for a 20.5% CAGR through 2030, driven by flexible layout and lower integration cost. Conveyor and sortation, palletizing robotics, piece-picking arms, and bar-coding systems fill out the technology stack, each optimizing a specific flow node.

Projects pairing goods-to-person robots with AI routing logic now rival AS/RS on cycle time while sidestepping civil works lead times. Itochu Logistics’ Tianjin site, housing 120 AMRs across 30,000 bins, ships 3,000 orders per hour, and can scale capacity by adding bots, not steel.[3]HAI Robotics, "ITOCHU Logistics and Hi-Robotics to Build New Infrastructure for Warehouse Automation in Tianjin" , hairobotics.comPiece-picking arms equipped with vision analytics lift accuracy above 99.5% across diverse SKUs, eroding the perception that full-case environments alone justify automation.

By End-User Industry: Retail Dominance with E-Grocery Acceleration

Retail and e-commerce account for 28% of current spend as omnichannel order complexity mandates high pick rates and near-instant cut-off times. The subsector’s next inflection is e-grocery, slated to outpace the aggregate warehouse automation market at an 18.3% CAGR. Kroger and Ocado’s continued rollout of regional fulfillment centers reflects a data-backed conviction that robotics can contain perishables’ razor-thin margins.

Beyond retail, healthcare, and pharma, automate for traceability, while industrial manufacturers use automation to rebalance global footprints under reshoring policies. 3PLs, traditionally late adopters of capital-heavy infrastructure, are flipping course as 74% of shippers threaten to switch providers if AI capability lags. The path forward points to differentiated service bundles—returns processing, late-stage customization, cold-chain kitting—enabled by modular robot fleets.

By Warehouse Size: Medium Facilities Lead, Mega Sites Accelerate

Medium warehouses (50–200 k sq ft) make up 37% of the warehouse automation market size because they hit the sweet spot of justifiable automation without megaproject complexity. Yet the fastest trajectory belongs to mega sites, where the 17.2% CAGR reflects scale economics and regional hub strategies. Amazon’s 3 million sq ft Shreveport plant, staffed by 2,500 associates and 750,000 robots, signals how hyperscale sites combine high-density storage, robotic sortation, and yard automation to orchestrate national last-mile networks.

The cap-ex envelope for mega builds is shrinking as vertical-lift access vehicles and mezzanine conveyors allow higher throughput per square foot. Developers are also experimenting with four-story designs near urban cores to reconcile land scarcity with delivery promises.

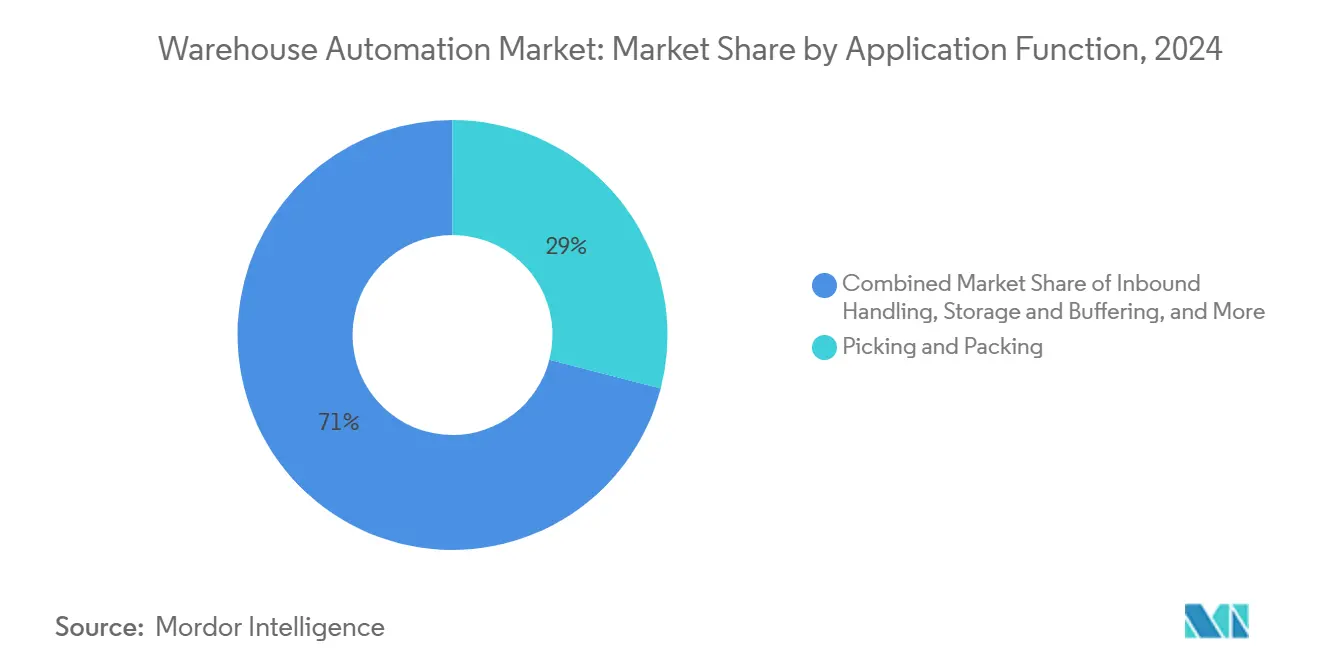

By Application Function: Picking Dominance with Returns Processing Surge

Picking & packing governs 29% of 2024 spend because it touches every order line and still leans on manual labor in many legacy operations. However, the highest growth node is returns processing at 18.8% CAGR. The U.S. retail sector alone wrestles with USD 890 billion in annual returns, pushing retailers to deploy sort-to-light and vision-guided reverse logistics cells that triage items for resale, refurbishment, or recycling.[4]DC Velocity, "Rethinking reverse logistics", dcvelocity.com

Unified execution platforms now interleave forward and reverse flows, deriving capacity that shortens dwell times. Almost 90% of store associates report that mobile workflow tools boost customer satisfaction, further validating the ROI case for integrated returns modules.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Ownership Model: Company-Owned Leadership with 3PL Acceleration

In 2024, company-owned operations account for 52% of the warehouse automation market size. Direct control appeals to firms whose brand promise hinges on fulfillment speed, data ownership, and continuous process improvement. The 3PL cohort is catching up fast: a 16.4% CAGR reflects mounting pressure to differentiate beyond price. 3PLs embed RaaS and AI analytics to lock in long-term contracts, while shippers hedge risk by splitting volumes across automated and conventional nodes.

As the outsourcing trend deepens, technology credentials rival geographic footprint in contract awards. Providers that package analytics dashboards, ESG reporting, and dynamic labor planning into a single SLA gain share, especially among mid-market customers seeking turnkey modernization.

Geography Analysis

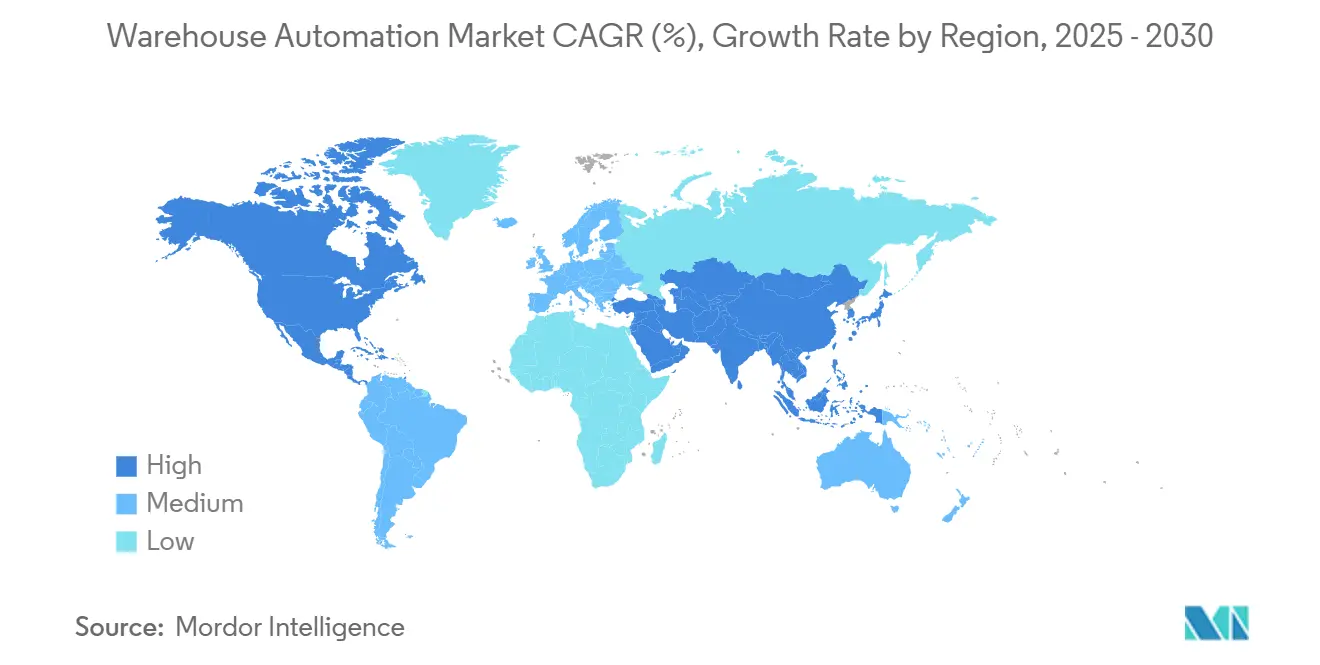

North America, with 35.6% of 2024 global revenue, remains the bellwether for the warehouse automation market. The U.S. continues to commission mega-centers exceeding 1 million sq ft, supported by a USD 44.2 billion industrial build-out pipeline and reshoring tax incentives. Yet headline vacancy reached 6.9% in 2025 as supply briefly outstripped demand, prompting developers to add flexible robotics infrastructure to futureproof assets for multi-tenant scenarios.

Asia–Pacific is the growth pacesetter, marked by an 18.6% CAGR outlook through 2030. While China’s near-term capital spend moderated, India, Southeast Asia, and Australia are filling the gap as consumer digital adoption rises. Japanese importers source cost-competitive Chinese robotics to address the 2024 driver-hour cap, illustrating cross-border technology flows. Cold-chain investments widen APAC’s addressable base; China’s refrigerated logistics value chain surpassed CNY 5.17 trillion (USD 711 billion) in 2023 and is projected to almost double by 2026.

Europe shows measured expansion underpinned by ESG regulation and automation subsidies. Western markets confront softer economic sentiment, but Eastern Europe attracts fresh capital as manufacturers diversify supply chains. DHL’s pledge for net-zero carbon warehouses by 2025 has catalyzed the procurement of energy-efficient AS/RS cranes and AMRs that run on renewable electricity. Germany’s KION Group is trimming fixed costs by EUR 160 million (USD 174 million) annually to fight margin erosion under intensifying price pressure from Asian entrants.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Global leadership remains concentrated in a handful of integrated solution vendors, yet competitive lines blur as software-native disruptors partner with hardware OEMs. KION Group and Daifuku retain scale advantages in multi-technology bids, buoyed by established service networks. Symbotic’s USD 22.4 billion backlog underscores the value of proprietary AI and high-velocity pallet shuttle systems, further fortified by its USD 200 million pickup of Walmart’s robotics assets.[5]SEC Filings, “Symbotic FY 2024 10-K,” sec.govVenture funding exceeding USD 20 billion in 2023 armed start-ups with capital to chase niche opportunities in returns automation and AI scheduling.

M&A momentum reflects a quest for end-to-end platforms: Rockwell Automation’s minority stake in RightHand Robotics aligns perception-driven picking with OTTO Motors’ AMRs, creating a hybrid execution stack that systems integrators can bolt onto legacy lines. Chinese manufacturers exploit lower bill-of-materials costs to penetrate price-sensitive segments, forcing incumbents to sharpen service differentiation rather than match headline equipment pricing. Emerging themes—zero-carbon operations, RaaS, and edge analytics—shape the next wave of value propositions.

Warehouse Automation Industry Leaders

-

Dematic Group (Kion Group AG)

-

Daifuku Co. Limited

-

Swisslog Holding AG (KUKA AG)

-

Jungheinrich AG

-

Honeywell Intelligrated

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: DPD partnered with Deus Robotics to equip its Docklands hub with AI-enabled robots that move 660 kg racks, aligning with the parcel carrier’s EcoLaunchpad sustainability roadmap.

- March 2025: Rockwell Automation invested in RightHand Robotics, integrating piece-picking with AutoStore AS/RS and OTTO Motors AMRs to simplify brownfield upgrades.

- March 2025: AutoStore introduced CarouselAI and VersaPort to widen addressable sites, particularly smaller footprints, and deepen AI-driven decision loops.

- February 2025: Itochu Logistics and HAI Robotics launched a Tianjin warehouse featuring 120 AMRs handling 30,000 stock locations, showcasing scalable goods-to-person throughput.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the warehouse automation market as all equipment, control systems, and integrated software that automate the physical flow of inventory into, within, and out of warehouses and distribution centers. This spans mobile robots (AGV, AMR), AS/RS, conveyors and sorters, palletizing and depalletizing robotics, AIDC devices, and the supervisory WMS and WES layers bundled with those assets.

Scope exclusion: Stand-alone WMS software sold without associated material-handling hardware and construction-related civil works are outside our numbers.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Technology

- Mobile Robots (AGV, AMR)

- Automated Storage and Retrieval Systems (AS/RS)

- Conveyor and Sortation Systems

- Palletizing / Depalletizing Robotics

- Piece-Picking Robots

- Automatic Identification and Data Collection (AIDC)

- By End-User Industry

- Food and Beverage

- Post and Parcel

- Retail and E-commerce

- Apparel and Footwear

- Manufacturing (Durable and Non-Durable)

- Pharmaceuticals and Healthcare

- 3PL / Contract Logistics

- Other Industries

- By Warehouse Size

- Small (<50 k sq ft)

- Medium (50-200 k sq ft)

- Large (200-500 k sq ft)

- Mega (>500 k sq ft)

- By Application Function

- Inbound Handling

- Storage and Buffering

- Picking and Packing

- Sorting and Consolidation

- Outbound Loading

- Returns Processing

- By Ownership Model

- Company-Owned Warehouses

- 3PL / Contract Warehouses

- E-commerce Pure-plays

- Government / Defence

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Australia

- New Zealand

- Rest of APAC

- Middle East

- GCC

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and pulse surveys with logistics managers, 3PL operators, systems integrators, and component suppliers across North America, Europe, and Asia helped validate equipment utilization rates, discount ladders, and deployment hurdles that rarely surface in documents. Insights from these discussions refined our input values and stress-tested scenario ranges.

Desk Research

Analysts first mapped global installed warehouse space, e-commerce parcel volumes, and robot shipments using public sources such as UN Comtrade customs data, the US Census Bureau's County Business Patterns, Eurostat structural business statistics, and industry white papers from MHI and Interact Analysis. Company 10-K filings, investor day decks, and patent databases (Questel, USPTO) supplied vendor revenue splits, ASP shifts, and pipeline innovations. Paid access to D&B Hoovers enriched private-player financials, while Dow Jones Factiva kept the team current on project announcements. The sources listed here illustrate, not exhaust, the corpus referenced during desk work.

Market-Sizing and Forecasting

A top-down model begins with warehouse floor area by region, applies automation penetration ratios by size tier, and multiplies by representative hardware-plus-software CAPEX per square foot. Results are then cross-checked against a selective bottom-up roll-up of leading vendors' automation revenue and sampled deal ASP multiplied by unit volumes gleaned from channel checks. Key variables like e-commerce order growth, regional logistics wages, median robot ASP, capital payback expectations, and industrial construction starts underpin the model. Multivariate regression, benchmarked with primary-expert consensus, generates the 2025-2030 forecast and flags inflection scenarios. Any data gaps in vendor splits are bridged with blended averages derived from peer disclosures and normalized where variance exceeds five percentage points.

Data Validation and Update Cycle

Outputs pass anomaly checks, senior analyst review, and variance reconciliation against independent indicators such as Interact Analysis robot shipments and Bureau of Labor Statistics logistics wage indices. Reports refresh annually; material events trigger interim snapshots, ensuring clients receive the most current view.

Credibility Anchor - Why Mordor's Warehouse Automation Baseline Stands Up

Published estimates differ because studies choose divergent asset scopes, discount curves, and refresh cadences.

Key gap drivers include whether research counts in-house built systems, how aggressively future ASP erosion is modeled, and the cadence at which macro variables are refreshed.

Mordor Intelligence fixes its scope around off-the-shelf hardware plus integrated software, updates inputs yearly, and tempers ASP decline assumptions with live integrator feedback, yielding a balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 29.9 B (2025) | Mordor Intelligence | - |

| USD 42.8 B (2025) | Global Consultancy A | Includes facility construction costs and stand-alone WMS licenses |

| USD 21.3 B (2024) | Trade Journal B | Excludes mobile robot fleets under RaaS contracts |

| USD 26.5 B (2024) | Regional Study C | Uses conservative penetration rates and 2020 exchange rates without annual recalibration |

Taken together, the comparison shows that Mordor's disciplined scope selection, annually refreshed variables, and dual-path validation provide a dependable mid-point that decision-makers can track and replicate with confidence.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the warehouse automation market?

It stands at USD 29.9 billion in 2025 and is on track to reach USD 63.4 billion by 2030.

Which region is growing fastest for warehouse automation investments?

Asia–Pacific is projected to post the quickest expansion at an 18.6% CAGR through 2030, buoyed by e-commerce penetration and urban logistics demand.

Why are AMRs considered a game changer in warehouse automation?

They deploy quickly, need no fixed guidance infrastructure, and typically deliver payback in under two years while cutting five-year operating costs by about 40%.

How does Robotics-as-a-Service affect adoption?

RaaS converts large capital outlays into usage-based fees, making advanced automation accessible to mid-size warehouses and accelerating overall market uptake.

Which application is expanding fastest within warehouse automation?

Returns processing automation leads with an 18.8% CAGR, reflecting the USD 890 billion retail returns challenge that firms must address to protect margins.

What role do ESG goals play in warehouse automation decisions?

Energy efficiency and carbon neutrality targets push European and global operators toward green robotics and smart energy management, influencing technology choice and supplier selection.

Page last updated on: