Global Virtual Care Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

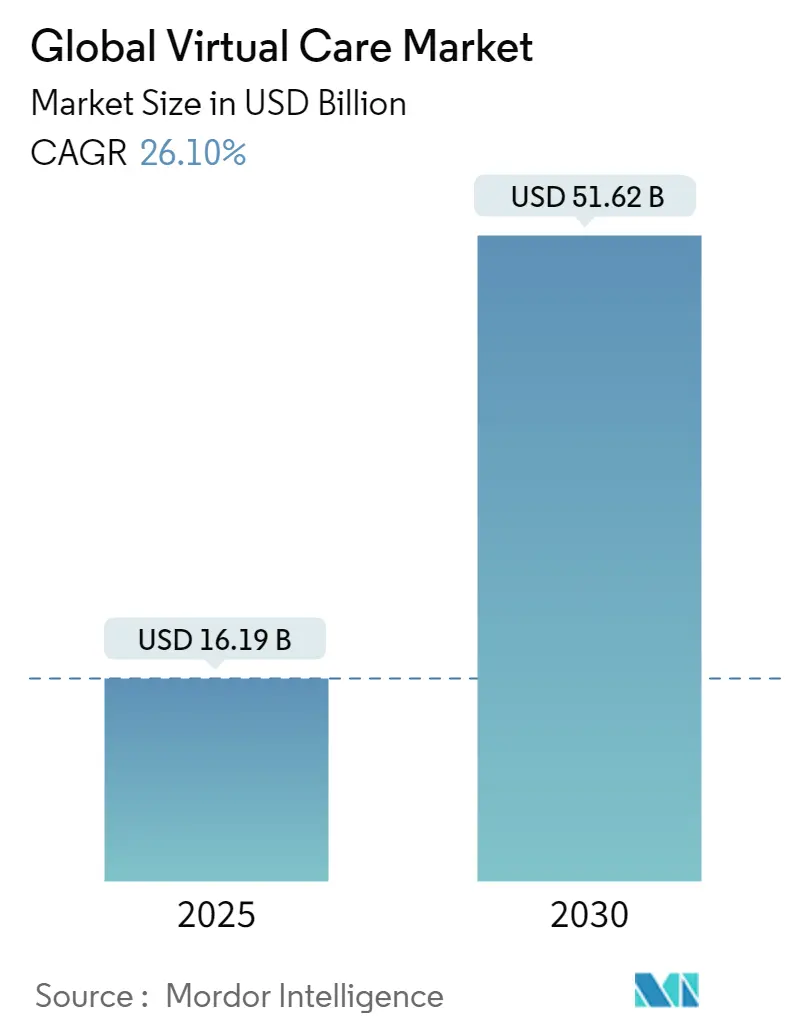

| Market Size (2025) | USD 16.19 Billion |

| Market Size (2030) | USD 51.62 Billion |

| Growth Rate (2025 - 2030) | 26.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

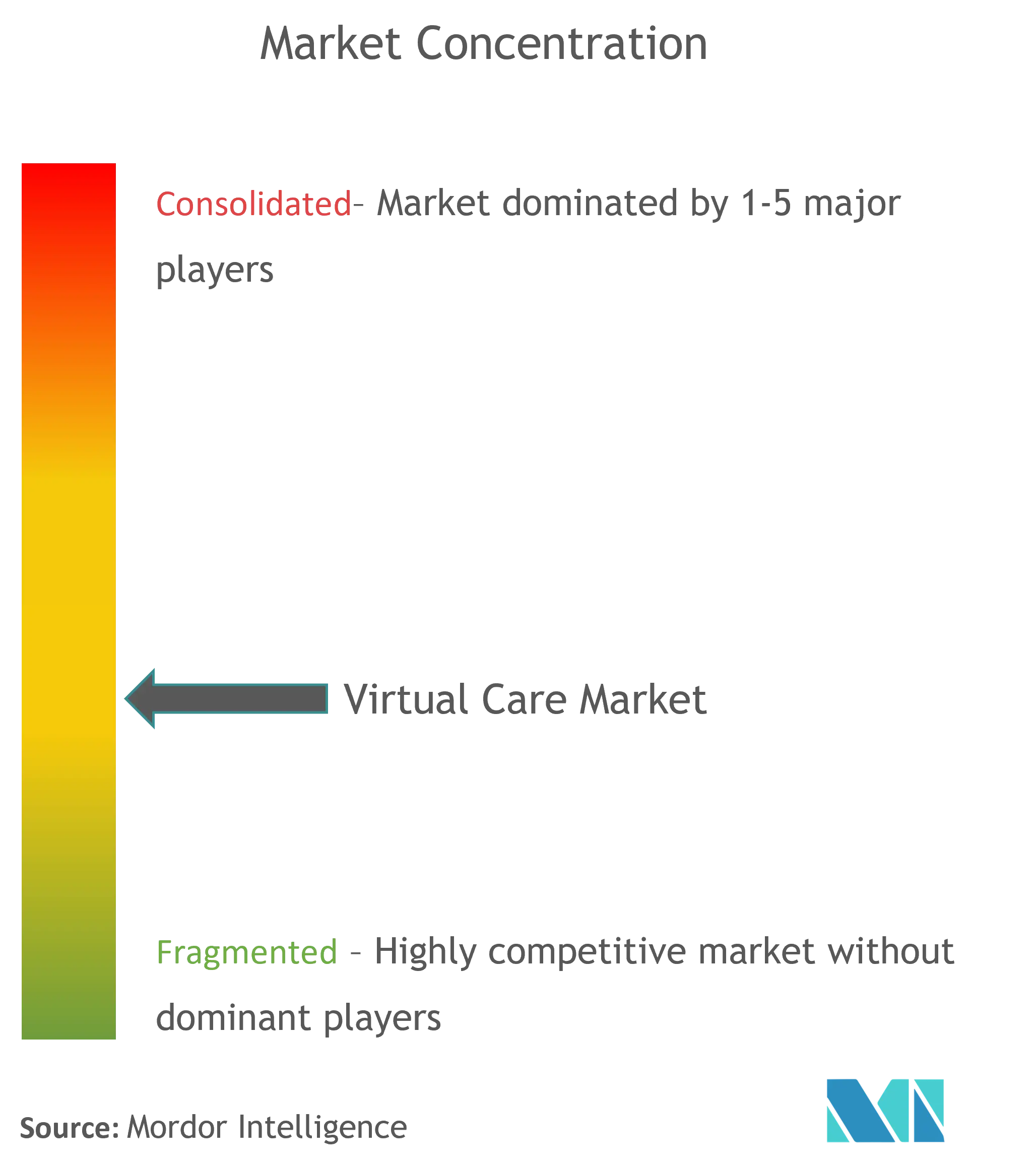

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Virtual Care Market Analysis by Mordor Intelligence

The virtual care market size is valued at USD 16.19 billion in 2025 and is forecast to reach USD 51.62 billion in 2030, reflecting a 26.1% CAGR over the period. The expansion stems from permanent reimbursement parity, sustained venture funding in AI-enabled platforms, a rapidly aging population seeking home-based chronic‐care models, and widening rural clinician shortage[1]Source: Centers for Medicare & Medicaid Services, “Calendar Year 2025 Medicare Physician Fee Schedule Final Rule,” cms.gov . New federal parity laws in 43 states and Washington D.C. anchor sustainable payment models, while satellite-enabled broadband pilots begin to close rural connectivity gaps[2]Source: National Conference of State Legislatures, “Telehealth Private Insurance Laws,” ncsl.org . Chronic-care programs that document 30% cost savings through hospital-at-home models and remote patient monitoring reinforce the business case for integrated virtual primary care. Concurrently, employers embrace enterprise-wide virtual benefits to curb long-term costs, and AI-powered triage platforms attract record capital, accelerating consolidation across fragmented service providers. Yet the market navigates uneven broadband penetration in emerging economies, tightening data-privacy mandates, and cybersecurity fatigue among health systems, each tempering near-term growth trajectories.

Key Report Takeaways

By component, services held 54.35% of virtual care market share in 2024, while software is projected to record the fastest 27.92% CAGR to 2030.

By delivery mode, video consultation retained 61.02% share of the virtual care market in 2024; VR/AR-enabled care is expected to expand at a 28.49% CAGR through 2030.

By application, chronic disease management commanded 28.72% of the virtual care market size in 2024, whereas mental health services are forecast to rise at a 29.07% CAGR over the outlook period.

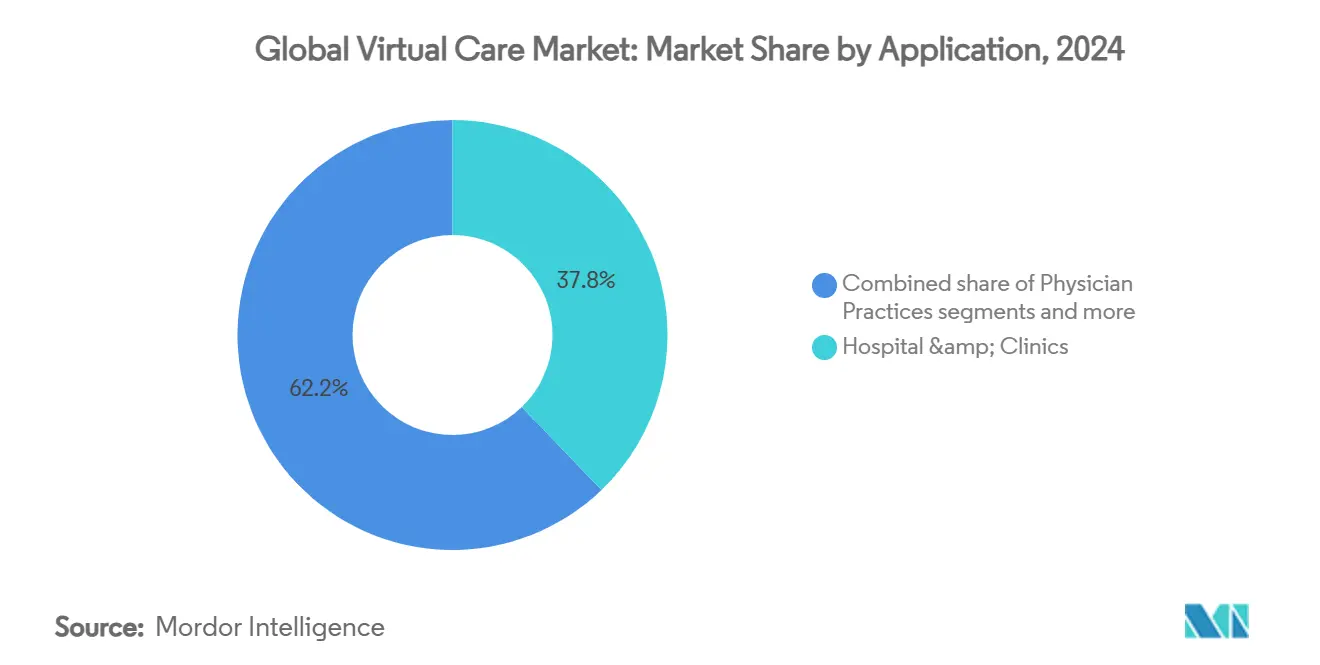

By end user, hospitals and clinics generated 37.82% of 2024 revenue, but home-care settings are projected to advance at a 29.66% CAGR by 2030.

Geographically, North America led with a 42.23% revenue share in 2024; Asia-Pacific is positioned for a 30.27% CAGR to 2030.

Global Virtual Care Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement parity laws expanding post-pandemic | +4.2% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Aging population driving home-based chronic-care models | +6.8% | Global, with concentration in developed markets | Long term (≥ 4 years) |

| Clinician shortages in rural regions | +3.9% | North America rural, APAC emerging markets | Medium term (2-4 years) |

| Venture funding into AI-powered virtual triage | +5.1% | Global, with early gains in North America, Europe | Short term (≤ 2 years) |

| Employer demand for integrated virtual primary care | +3.7% | North America & EU corporate markets | Medium term (2-4 years) |

| Satellite-enabled connectivity in low-bandwidth areas | +2.3% | Rural regions globally, priority in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Parity Laws Expanding Post-Pandemic

Permanent payment parity statutes have doubled to 33 U.S. states since 2019, and the Telehealth Modernization Act of 2024 extends Medicare waivers through 2026, eliminating geographic restrictions and broadening provider eligibility. CMS’s 2025 Physician Fee Schedule adds bundled Advanced Primary Care Management Services, creating predictable revenue streams for virtual providers. Commercial insurers follow suit, with parity clauses included in 87% of large-group contracts filed in 2025. These mechanisms institutionalize virtual care as a standard benefit rather than an emergency workaround. As payer confidence grows, venture investors channel fresh capital into platform scalability, and hospital systems embed virtual pathways across inpatient and ambulatory settings.

Aging Population Driving Home-Based Chronic-Care Models

By 2030, the global population aged 65 and above will surpass 1 billion, while chronic disease prevalence continues to climb. Remote patient monitoring programs record 1.68% fasting-glucose reductions and 0.45% HbA1c drops among diabetics, validating clinical effectiveness. Hospital-at-home pilots deliver 30% lower care costs and up to 83% fewer readmissions, stimulating payer interest in value-based virtual bundles. McKinsey projects USD 265 billion of U.S. health services can shift to the home, realigning facilities planning and clinician workflows. As demographic pressures intensify, health systems treat home-centric virtual pathways as essential to workforce sustainability.

Clinician Shortages in Rural Regions

Rural communities account for under 25% of U.S. physicians, yet serve 60 million residents; shortages are projected to reach 68,020 primary-care doctors by 2036. Virtual hubs such as Guthrie Clinic’s model reduced nursing turnover from 25% to 13%, saving USD 7 million in annual labor expense. Tele-neurology and tele-cardiology programs shorten time-to-treatment for stroke and STEMI cases, enhancing outcomes despite geographical isolation. Because rural recruitment pipelines remain thin, telehealth substitutes become permanent rather than stopgap measures. State licensure compacts expand multistate practice privileges, but administrative friction persists, heightening demand for turnkey credentialing services.

Venture Funding Into AI-Powered Virtual Triage

Global consumer health-tech funding rose 37% year-on-year to USD 6.3 billion in 2024, with AI-driven triage platforms capturing the largest share. K Health’s USD 50 million extension underscored investor confidence in models that reduce avoidable ED use. Peer-review research shows AI recommendations outperform physician decisions in identifying antibiotic-resistant infections during virtual urgent care, driving payer endorsements. Private-equity-led roll-ups increased 63% in 2024, signaling a consolidation phase that favors platforms with embedded AI. Enhanced acuity alignment improves clinical outcomes and optimizes network cost structures, persuading large employers to broaden virtual benefit coverage.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy litigation risk under evolving regulations | -2.8% | Global, with heightened focus in EU & North America | Short term (≤ 2 years) |

| Unequal broadband penetration in emerging economies | -3.4% | APAC emerging markets, rural regions globally | Long term (≥ 4 years) |

| Physician licensure barriers across state borders | -1.9% | North America interstate practice | Medium term (2-4 years) |

| Cyber-security fatigue among health systems | -2.1% | Global, with concentration in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Litigation Risk Under Evolving Regulations

HHS plans to mandate encryption, multifactor authentication, and formal asset management in proposed HIPAA rule revisions slated for 2025, imposing steep compliance spending. The FTC expands enforcement on consumer health-data breaches, heightening litigation exposure for virtual platforms. Divergent state privacy acts, notably California’s CPRA and Virginia’s CDPA, layer additional requirements, complicating multistate rollouts. European operators contend with GDPR harmonization and cross-border data-transfer restrictions. These overlapping regimes slow product cycles and increase vendor-due-diligence timelines, nudging smaller entrants toward partnership or acquisition.

Unequal Broadband Penetration in Emerging Economies

Smartphone ownership averages 78% in rural APAC, while laptop access sits at 56%, constraining high-fidelity video care. The U.S. Broadband Equity, Access, and Deployment Act injects USD 42 billion into infrastructure, yet project delays and legal challenges threaten completion targets. Satellite solutions alleviate gaps but remain cost-intensive for community clinics. In India, national telehealth efforts reach thousands of villages, but bandwidth variance undermines consistent service levels. Consequently, audio-only and asynchronous modes retain relevance, but limited bandwidth restricts advanced VR/AR therapies, capping total addressable demand for the virtual care market.

Segment Analysis

By Component: Services Sustain Leadership Amid Software Acceleration

Services captured 54.35% of virtual care market share in 2024 as multidisciplinary clinical teams remained vital for diagnosis, triage, and longitudinal monitoring. The segment’s resilience is reinforced by bundled reimbursement codes that prize care coordination and value-based outcomes. Software, however, advances at a 27.92% CAGR through 2030, propelled by scalable AI algorithms that automate symptom checking, risk stratification, and documentation. This dual trajectory enables platforms to layer high-margin SaaS fees atop labor-intensive service lines, blending predictable subscription revenue with encounter-based billing. Hardware lags in growth because device standardization and patient usability hurdles limit rapid refresh cycles, yet connected-sensor adoption still supports continuous data capture for chronic-care pathways.

Software’s momentum also emanates from hospital demand for virtual sitter dashboards that allow a single nurse to oversee multiple beds, reducing fall incidents and saving USD 1.2 million per facility annually. Payer credentialing APIs, integrated within EHRs, shave minutes off call times and tighten denial rates. As predictive analytics mature, software modules increasingly deliver automated plan-of-care recommendations, shifting clinical staff to higher-acuity tasks. With enterprise buyers negotiating multi-year licenses, software revenue visibility improves, drawing institutional investors who value recurring income streams inside the virtual care market.

Note: Segment shares of all individual segments available upon report purchase

By Delivery Mode: Video Still Dominant as Immersive Tech Gains Ground

Video consultation accounted for 61.02% of 2024 revenue, offering clinicians real-time visual cues essential for acute assessments. States have codified coverage for audio-only visits in 18 jurisdictions, ensuring continuity for bandwidth-limited patients, yet reimbursement remains lower than video in most commercial contracts. VR/AR-enabled care, though nascent, accelerates at a 28.49% CAGR as evidence mounts for pain distraction, exposure therapy, and physical-rehab applications. Holographic pilots in Texas reported higher patient-engagement scores relative to standard video, hinting at future competitive differentiation. Asynchronous (store-and-forward) modalities support dermatology and ophthalmology where high-resolution imaging replaces synchronous dialog.

In rural broadband deserts, satellite backhaul stabilizes video quality, but latency occasionally disrupts neuro-rehab sessions, sustaining demand for hybrid audio-plus-text workflows. Platform roadmaps increasingly integrate mixed-reality toolkits using consumer headsets, yet reimbursement policy still lags technological capability. Providers therefore adopt phased rollouts, initially deploying VR for in-clinic behavioral health before expanding to at-home kits as payer codes solidify. The convergence of unlimited-reality technologies is poised to widen therapeutic scope, though cost and accessibility must improve before immersive delivery modes erode video’s commanding virtual care market share.

By Application: Mental Health Services Outpace Chronic Disease Management

Chronic disease programs retained 28.72% of 2024 revenue as validated RPM protocols tracked daily vitals for diabetes, hypertension, and heart-failure cohorts. Nonetheless, mental health services are forecast to grow 29.07% annually as post-pandemic behavioral-health demand persists, with 38.3% of 2023 encounters conducted virtually. Telepsychiatry lowers wait times by 35 days on average, improving clinical outcomes and adherence. Primary care remains foundational, yet faces commoditization, sparking vertical integration into wellness and disease-prevention add-ons. Specialty consultation leverages national panels of subspecialists to support community hospitals lacking onsite expertise.

Digital cognitive-behavioral therapy modules complement synchronous sessions, extending clinician reach without compromising effectiveness. Integrated cardiometabolic pipelines combine lifestyle coaching with mental-health screening to capture comorbidity synergies. Meanwhile, post-acute rehab leverages gamified VR exercises that shorten recovery by 17% for knee-replacement patients, though widespread payer recognition is pending. The marriage of mental health and chronic-care management under unified platforms positions vendors to unlock cross-selling opportunities and defend against point-solution competitors.

Note: Segment shares of all individual segments available upon report purchase

By End User: Home-Care Settings Redefine Continuum of Care

Hospitals and clinics contributed 37.82% of 2024 revenue as inpatient teleconsultations, virtual nursing, and remote specialist access extended capacity amid staffing constraints. Yet home-care settings are slated for a 29.66% CAGR, reflecting the financial appeal of hospital-at-home programs that generate 30% savings and materially lower readmissions. Physician practices embed virtual check-ins to preserve panel size, while employers and payers leverage integrated platforms to shrink total cost of care. Government and defense facilities deploy secure telemedicine channels for dispersed populations, and direct-to-consumer offerings entice digitally savvy patients.

Advances in 5G and edge computing enable near-real-time remote vital-sign streaming, meeting clinical thresholds for early intervention. Portable diagnostic kits equip visiting nurses with lab-quality imaging, shrinking dependency on brick-and-mortar sites. Reimbursement alignment under the CMS Acute Hospital Care at Home waiver through 2029 further de-risks provider investment, anchoring long-term expansion in domiciliary models. As trust in at-home modalities grows, payers develop risk-sharing contracts that reward vendors for avoiding unnecessary emergency visits, reinforcing home settings as a strategic growth engine within the virtual care market.

Geography Analysis

North America led the virtual care market with 42.23% revenue in 2024, buoyed by mature reimbursement and early technology adoption. The American Relief Act of 2025 extends Medicare telehealth coverage through March 2025, but permanent legislation remains pending, injecting regulatory uncertainty. State parity momentum persists, yet upcoming DEA controlled-substance rules create new compliance layers. Rural broadband pilots featuring Starlink have begun closing access gaps, lifting encounter volumes 12% in participating clinics. Persistent clinician shortages drive cross-state networks, although full licensure reciprocity is still incomplete.

Asia-Pacific is projected to achieve a 30.27% CAGR to 2030, propelled by government funding and large-scale platform rollouts in China, India, and Indonesia. India’s E-Sanjeevni network has already facilitated 130 million consultations, illustrating the scalability of hub-and-spoke virtual models. Venture funding remains robust, targeting AI analytics and remote diagnostics attuned to local affordability thresholds. Infrastructure disparities persist, with rural regions dependent on mobile-first strategies and asynchronous messaging. Policy heterogeneity across markets demands country-specific go-to-market tactics, yet collective momentum positions the region as the fastest-growing node in the virtual care market.

Europe records steady adoption, underpinned by 40 nations formalizing telemedicine frameworks. EU cross-border health initiatives aim to harmonize reimbursement, but data privacy directives present compliance complexity. Telepsychiatry solutions proliferate as mental-health waitlists lengthen. Satellite-enabled trials in the UK extend connectivity to remote GP practices, while Nordic countries pioneer national tele-monitoring registries that integrate with electronic health cards. Consolidation accelerates as valuations normalize post-pandemic, with acquirers prioritizing AI-enhanced triage capabilities to counter margin compression.

Competitive Landscape

Market fragmentation persists, yet 2024 M&A activity rose 63% as private equity and strategic buyers sought scale and differentiated technology. Teladoc Health completed 18.4 million visits in 2023 and deepened vertical integration by acquiring Catapult Health (at-home diagnostics) and UpLift (mental health) for a combined USD 95 million in 2025. Transcarent’s merger with Accolade couples advocacy with provider navigation, illustrating convergence between care delivery and benefits management. AI differentiation remains paramount, with K Health’s chatbot outperforming physicians on antibiotic stewardship in clinical trials, prompting regional payers to subsidize its deployment.

White-space opportunities center on immersive therapies and satellite-connected rural outreach. Fabric’s four-acquisition spree expanded coverage to 100 million lives and built a national virtual urgent-care backbone. Specialist segments such as tele-cardiology attract new entrants leveraging FDA-cleared connected stethoscopes that synchronize with EHRs. Competitive pressure intensifies in primary care where commoditization depresses margins; hence multi-service ecosystems and employer channels increasingly determine defensibility. Vendors that package chronic-care, mental-health, and preventive bundles under one contract appeal to payers aiming to simplify vendor ecosystems.

The power balance also shifts as large health systems build proprietary platforms, sometimes white-labeling technology from established vendors but retaining branding and data ownership. Start-ups without clear differentiation face rising customer-acquisition costs and stricter hospital procurement standards that favor cybersecurity-certified suppliers. Over the forecast horizon, winners will combine AI-driven clinical pathways, robust payer contracts, and proven enterprise security postures to consolidate a greater slice of the virtual care market.

Global Virtual Care Industry Leaders

-

Teladoc Health, Inc.

-

CVS Health

-

American Well Corporation

-

MDLIVE

-

Oracle Corporation (Cerner)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Teladoc Health acquired UpLift for USD 30 million, adding 1,500 clinicians to its BetterHelp platform and seeking a 30% increase in engagement duration

- April 2025: Transcarent finalized its merger with Accolade, creating an end-to-end virtual care and advocacy platform

Global Virtual Care Market Report Scope

Per the report's scope, virtual care generally enables patients to undergo online consultation with doctors from anywhere. Virtual care generally includes consultation through live audio, video, and instant messaging as a mode of communication with the patients remotely. The virtual care market is segmented by mode of delivery (video, audio, and messaging), component (solutions and services), end user (home healthcare, hospitals, and others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Hardware |

| Software |

| Services |

| Video Consultation |

| Audio Consultation |

| Messaging |

| Asynchronous (Store-and-Forward) |

| VR / AR-Enabled Care |

| Others |

| Primary Care |

| Specialty Consultation |

| Chronic Disease Management |

| Mental Health Services |

| Post-Acute & Rehabilitation |

| Wellness & Preventive Care |

| Hospitals & Clinics |

| Physician Practices |

| Home-Care Settings |

| Employers & Payers |

| Government & Defense Facilities |

| Patients |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Component (Value) | Hardware | |

| Software | ||

| Services | ||

| By Delivery Mode (Value) | Video Consultation | |

| Audio Consultation | ||

| Messaging | ||

| Asynchronous (Store-and-Forward) | ||

| VR / AR-Enabled Care | ||

| Others | ||

| By Application (Value) | Primary Care | |

| Specialty Consultation | ||

| Chronic Disease Management | ||

| Mental Health Services | ||

| Post-Acute & Rehabilitation | ||

| Wellness & Preventive Care | ||

| By End User (Value) | Hospitals & Clinics | |

| Physician Practices | ||

| Home-Care Settings | ||

| Employers & Payers | ||

| Government & Defense Facilities | ||

| Patients | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

1. What is the current virtual care market size and projected growth?

The virtual care market size stands at USD 16.19 billion in 2025 and is projected to reach USD 51.62 billion by 2030, growing at a 26.1% CAGR.

2. Which component leads the virtual care market share today?

Services lead with 54.35% of revenue in 2024, reflecting the labor intensity of clinical delivery.

3. Why is Asia-Pacific the fastest-growing regional market?

Asia-Pacific benefits from government investment, rapid digital adoption, and large underserved populations, driving a 30.27% CAGR forecast through 2030.

4. How are reimbursement changes affecting market expansion?

Permanent payment-parity laws and extended Medicare waivers guarantee sustainable revenue streams and encourage provider investment in virtual models.

5. Which application segment is expanding the quickest?

Mental health services are advancing at a 29.07% CAGR, propelled by ongoing demand for telepsychiatry and digital behavioral-health tools.

6. What restrains faster global adoption of virtual care?

Key barriers include uneven broadband access, evolving privacy regulations, interstate licensure constraints, and escalating cybersecurity threats.

Page last updated on: