Vietnam Plastic Market Size

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Volume (2025) | 11.84 Million tons |

| Market Volume (2030) | 17.76 Million tons |

| CAGR | 8.44 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Vietnam Plastic Market Analysis

The Vietnam Plastics Market size is estimated at 11.84 million tons in 2025, and is expected to reach 17.76 million tons by 2030, at a CAGR of 8.44% during the forecast period (2025-2030).

Vietnam's plastics industry is experiencing significant transformation driven by technological advancement and sustainability initiatives. The country's rapid urbanization, projected to reach 51.2% by 2040, is reshaping the industry landscape by creating increased demand for plastic products across various sectors. The government's commitment to environmental sustainability is evident through recent initiatives, particularly in Ho Chi Minh City, where authorities launched comprehensive plans in June 2022 to reduce plastic waste pollution and treatment costs, focusing on eliminating single-use plastics and non-biodegradable plastics bags.

The electronics sector has emerged as a crucial driver for the plastics industry, with hardware and electronics export earnings reaching USD 57 billion in 2022, marking a 16.4% increase. This growth is complemented by significant investments in manufacturing capabilities, particularly in high-tech polymer components for electronic applications. The sector's expansion is further supported by the relocation of major manufacturing facilities from other Asian countries to Vietnam, creating new opportunities for specialized plastic materials and components.

The industry is witnessing a notable shift towards sustainable and bioplastics alternatives, with projections indicating a demand for biodegradable plastics reaching 80,000 tonnes annually by 2025. This transition is exemplified by recent developments such as AnEco compostable bags being awarded the "Vietnam National Brand" in November 2022, marking a significant milestone in the country's sustainable plastics segment. Major manufacturers are actively investing in eco-friendly solutions, with companies like SCG Chemicals announcing in August 2022 their plans to invest USD 22.7 million in a BOPET manufacturing project.

The market is experiencing substantial industrial expansion through strategic investments and technological upgrades. In September 2022, Billion Industrial Holdings announced plans to establish a PET plant with an annual production capacity of approximately 300,000 tons, demonstrating the industry's commitment to expanding domestic plastic manufacturing capabilities. The kitchenware segment alone generated revenue of USD 24.5 million in 2022, indicating robust demand in consumer applications. These developments are accompanied by increasing foreign direct investment and technological transfers, positioning Vietnam as an emerging hub for advanced plastic manufacturing in Southeast Asia.

Vietnam Plastic Market Trends

Growing Demand from the Construction Sector

The construction sector has emerged as a significant driver for the Vietnamese plastics market, contributing approximately 5.97% to the country's total GDP in 2021. The sector's robust growth is supported by massive infrastructure development initiatives, including the government's ambitious plan to construct one million low-cost houses for workers, particularly internal migrants in Ho Chi Minh City by 2025. This extensive construction activity has created substantial demand for various plastic products, including PVC pipes, window frames, insulation materials, waterproofing membranes, and other construction-related plastic components that offer durability, cost-effectiveness, and superior performance characteristics.

The construction industry's growth trajectory is further reinforced by Vietnam's accelerating urbanization rate, which is projected to reach 51.2% by 2040 from 38.05% in 2021. This urban expansion is complemented by significant infrastructure investments, with the transport ministry planning to invest between USD 43-65 billion in transportation infrastructure development between 2021 and 2030. Several major projects initiated in 2022 demonstrate this momentum, including the USD 320 million Cadia Qui Nhon Mixed-use Development project, the USD 317 million Mau Son Ecotourism Complex, and the USD 302 million Sapa Domestic Airport Development project, all of which require substantial quantities of construction-grade industrial plastics for their completion.

Other Drivers

The plastic packaging industry has emerged as another crucial driver for the Vietnamese plastics market, with over 900 factories currently operational in the sector, approximately 70% of which are concentrated in the Southern region, primarily in Ho Chi Minh City, Binh Duong, and Dong Nai. Major investments in this sector, such as Tetra Pak's additional USD 5.9 million investment in its Binh Duong packaging material factory in March 2022, demonstrate the industry's growth potential. The facility's expansion from 11.5 billion to 16.5 billion packages annually reflects the robust demand for plastic packaging materials across various end-use industries, particularly in food and beverage, healthcare, and consumer goods sectors.

The electronics manufacturing sector represents another significant driver, with Vietnam positioning itself as one of the top-five fastest-growing technology equipment markets globally. The industry's evolution is marked by substantial foreign investments and manufacturing relocations to Vietnam, exemplified by major international electronics companies establishing production facilities in the country. This trend is further supported by the government's initiatives to strengthen domestic manufacturing capabilities, with the production index of electronic, computer, and optical products showing significant growth. The increasing demand for plastic components in electronic products, from casings to internal components, continues to drive innovation and consumption in the plastics industry. Moreover, advancements in plastic processing techniques are enhancing the quality and application range of these components.

Segment Analysis: Type

Traditional Plastics Segment in Vietnam Plastics Market

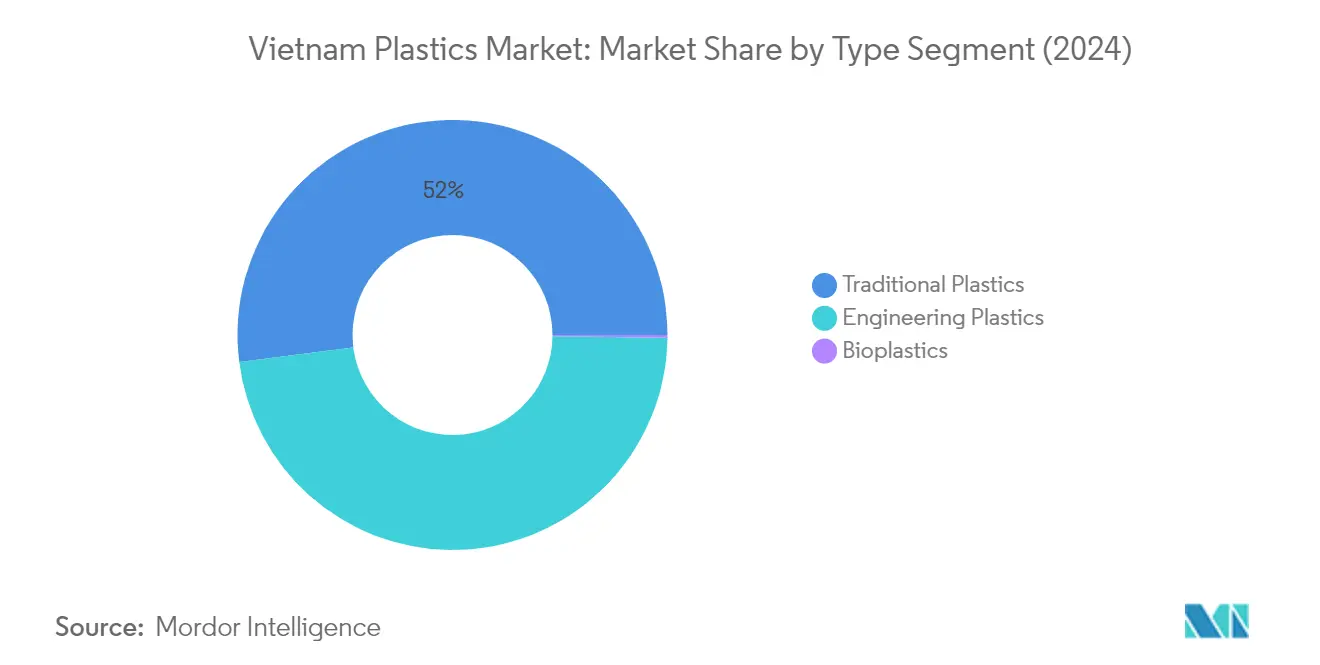

Traditional plastics continue to dominate the Vietnam plastics market, holding approximately 52% market share in 2024. This segment includes key materials like polyethylene, polypropylene, polystyrene, and polyvinyl chloride that are extensively used across various industries. The segment's dominance is primarily driven by the growing demand from the construction sector, where these materials are used in pipes, fittings, window frames, and various building components. Additionally, the increasing usage in plastic packaging applications, particularly in food and beverage packaging, consumer goods, and retail sectors, further strengthens its market position. The segment's growth is also supported by Vietnam's expanding manufacturing sector and the country's position as a major export hub for plastic products in Southeast Asia.

Bioplastics Segment in Vietnam Plastics Market

The bioplastics segment is emerging as the fastest-growing category in Vietnam's plastics market, projected to grow at approximately 13% during 2024-2029. This remarkable growth is driven by increasing environmental awareness and the government's ambitious initiatives to reduce plastic waste. Vietnam's commitment to stop using disposable plastic in stores, markets, and supermarkets by 2030 has created strong momentum for bioplastics adoption. Major retail chains like Big C, Mega Market, Co.opmart, Vinmart, and Lotte are actively transitioning towards environmentally-friendly packaging solutions. The segment is further boosted by innovations in biodegradable materials and the emergence of local manufacturers like An Phat Bioplastics and Biostarch, who are developing advanced biodegradable products ranging from shopping bags to food packaging materials.

Remaining Segments in Type

Engineering plastics represent a significant segment in Vietnam's plastics market, offering high-performance materials for specialized applications. This segment includes materials like polyurethanes, fluoropolymers, polyamides, polycarbonates, and various other engineering plastics that cater to demanding applications in the automotive, electronics, and industrial sectors. The segment's growth is supported by Vietnam's expanding electronics manufacturing sector and increasing foreign investments in high-tech industries. The versatility of engineering plastics in providing superior mechanical properties, heat resistance, and chemical resistance makes them indispensable in manufacturing sophisticated components for various end-use industries.

Segment Analysis: Technology

Extrusion Segment in Vietnam Plastics Market

The plastic extrusion segment dominates the Vietnam plastics market, commanding approximately 57% of the total market share in 2024. This technology is extensively utilized in the production of various construction and technical plastic materials, with more than 1,000 extruders currently operating across Vietnam. The segment's prominence is particularly evident in the manufacturing of PVC, HDPE, PPR pipes, profile bars, plastic doors and windows, panels, and furniture. Leading companies like Tien Phong Plastic JSC and Binh Minh Plastic JSC have established strong market positions, with the former controlling around 60% of the northern market and the latter dominating 40% of the southern market. The segment's growth is primarily driven by Vietnam's robust construction sector development and increasing urbanization rate, which is expected to reach 51.2% by 2040. Additionally, the government's initiative to build affordable housing in more than 350 industrial zones has significantly boosted the demand for construction and technical plastics, further solidifying the plastic extrusion segment's market leadership.

Remaining Segments in Technology

The remaining segments in the Vietnam plastics market technology landscape include blow molding, plastic injection molding, and other technologies. Blow molding technology plays a crucial role in the packaging sector, particularly in the production of PET bottles, kegs, and various plastic packaging products. The plastic injection molding segment serves the growing electrical and electronics industry, with applications in manufacturing complex components for smartphones, tablet PCs, and other electronic devices. Other technologies, including structural foaming, thermoforming, and GRP molding, cater to specific applications such as large trash containers, freeway safety containers, in-ground housing water systems, and various automotive components. These technologies complement each other in meeting the diverse needs of Vietnam's expanding plastics industry, particularly in sectors such as packaging, electronics, automotive, and construction.

Segment Analysis: Application

Packaging Segment in Vietnam Plastics Market

The plastic packaging segment dominates the Vietnam plastics market, commanding approximately 50% of the total market share in 2024. This significant market position is driven by the rapid growth of Vietnam's packaging industry, which is one of the country's fastest-growing sectors with over 900 factories currently in operation, with approximately 70% concentrated in the Southern region, primarily in Ho Chi Minh City, Binh Duong, and Dong Nai. The segment's prominence is further reinforced by increasing demand across various end-user industries, with the food sector accounting for 30-50% of demand, while pharmaceutical, healthcare, and electronics sectors each contribute 5-10%. The versatility of plastic packaging materials, including polyethylene terephthalate (PET), high-density polyethylene (HDPE), polyvinyl chloride (PVC), and polypropylene (PP), makes them ideal for applications ranging from food and beverage packaging to consumer goods and healthcare packaging. The growth is also supported by Vietnam's expanding export market and various free trade agreements, such as the Vietnam-EU FTA, which continue to drive demand for packaging products.

Building and Construction Segment in Vietnam Plastics Market

The building and construction segment represents a significant growth opportunity in the Vietnam plastics market, with robust expansion projected for 2024-2029. This growth is primarily driven by Vietnam's position as the fourth-fastest construction growth rate holder in East Asia, supported by ambitious government initiatives to develop infrastructure and attract foreign investment. The segment's expansion is further fueled by the country's rapid urbanization trajectory, with urban development expected to reach 51.2% by 2040. The construction sector's development is evidenced by major ongoing projects such as the Cadia Qui Nhon Mixed-use Development, Mau Son Ecotourism Complex, and various infrastructure initiatives. The government's commitment to improving transportation infrastructure, with planned investments between USD 43 billion and USD 65 billion, along with the target to construct more than 5,000 kilometers of expressways by 2030, continues to drive demand for construction plastics. Additionally, the focus on affordable housing development, with plans to build one million affordable houses in more than 350 industrial zones, further strengthens the segment's growth prospects.

Remaining Segments in Application

The Vietnam plastics market encompasses several other significant segments including electrical and electronics, automotive and transportation, housewares, and furniture and bedding. The electrical and electronics segment benefits from Vietnam's position as one of the top-five fastest-growing technology equipment markets globally, with substantial growth in production of electronic components and communication equipment. The automotive and transportation segment is driven by increasing vehicle production and the growing adoption of electric vehicles. The housewares segment maintains steady growth through rising domestic consumption and expanding retail networks, while the furniture and bedding segment capitalizes on Vietnam's strong position as the largest furniture exporter in Southeast Asia. Each of these segments contributes uniquely to the market's diversity and overall growth, supported by ongoing industrialization, increasing consumer spending, and government initiatives promoting domestic manufacturing capabilities.

Vietnam Plastic Industry Overview

Top Companies in Vietnam Plastics Market

The Vietnamese plastics market features a mix of domestic and international players focusing on continuous innovation and strategic expansion. Companies are increasingly investing in research and development to create sustainable plastic solutions and enhance their product portfolios, particularly in packaging and construction applications. Market leaders are strengthening their positions through capacity expansions, with several players establishing new manufacturing facilities and upgrading existing ones to meet growing demand. Strategic partnerships and collaborations are becoming more prevalent, especially in technology transfer and distribution networks. Companies are also emphasizing operational efficiency through vertical integration and automation of plastic manufacturing processes, while simultaneously developing eco-friendly alternatives to address environmental concerns.

Market Dominated by International Strategic Players

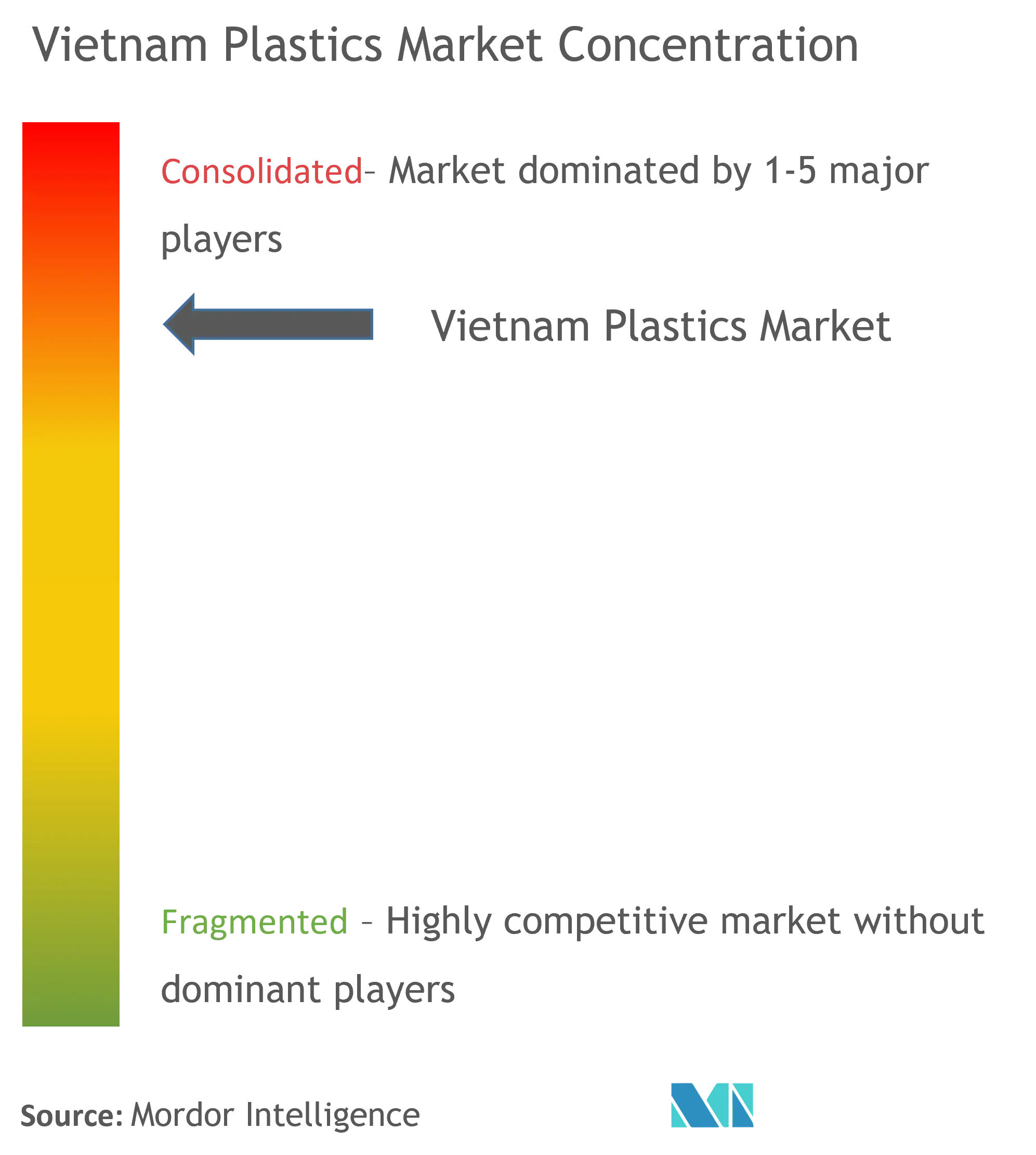

The Vietnamese plastics market structure is characterized by the strong presence of international conglomerates that have established significant manufacturing bases in the country. These global players, particularly from Japan, South Korea, and Thailand, leverage their advanced technological capabilities and extensive distribution networks to maintain market leadership. The market shows moderate consolidation, with major players like Far Eastern New Century, Hyosung Chemical, and SCG Chemicals holding substantial market shares through their local manufacturing facilities and strategic partnerships with domestic distributors.

The market is witnessing increased merger and acquisition activities as international players seek to strengthen their foothold in Vietnam's growing plastics industry. Companies are particularly focused on acquiring local manufacturing capabilities and distribution networks to enhance their market presence. The domestic players, though fewer in number, are gradually strengthening their positions through joint ventures and technical collaborations with international companies, helping them access advanced technologies and expand their product portfolios. This dynamic is creating a more competitive landscape where both global and local players are continuously evolving their strategies to maintain market relevance.

Innovation and Sustainability Drive Future Success

Success in the Vietnamese plastics market increasingly depends on companies' ability to balance innovation with sustainability requirements. Market incumbents are focusing on developing value-added products and expanding their production capabilities while simultaneously investing in eco-friendly solutions. The ability to offer customized solutions for specific industry applications, particularly in the packaging and construction sectors, while maintaining cost competitiveness, has become crucial for maintaining market share. Companies are also strengthening their backward integration to reduce dependence on plastic raw materials imports and improve operational efficiency.

For new entrants and smaller players, the path to market success lies in identifying and serving niche segments while building strong relationships with end-users. The market presents opportunities for companies that can offer innovative solutions in specialized applications or eco-friendly alternatives. However, success also depends on managing the challenges of raw material price volatility and increasing environmental regulations. Companies need to focus on developing strong supply chain networks and maintaining product quality while adapting to evolving environmental standards and changing consumer preferences towards sustainable products. The ability to form strategic partnerships and access advanced technologies will continue to be critical factors for success in this dynamic market.

Vietnam Plastic Market Leaders

-

Far Eastern New Century

-

Hyosung Chemicals

-

Nghi Son Refinery and Petrochemical (NSRP)

-

Billion Industrial Holdings Limited

-

SCG Chemicals Public Company Limited (TPC VINA)

*Disclaimer: Major Players sorted in no particular order

Vietnam Plastic Market News

- In September 2022, Billion Industrial Holdings Limited announced the expansion of the manufacturing facilities for polyester bottle chips in Vietnam. This manufacturing facility will have a production capacity of 300,000 tons of polyethylene terephthalate resin.

- In August 2022, SCG Chemicals Co. Ltd announced an investment of USD 22.7 million in the AJ Plastproject to produce biaxially oriented polyethylene terephthalate (BOPET) in Vietnam. The BOPET project will boost the company's product portfolio with a value-added product designed to meet the growing consumer demand.

Vietnam Plastic Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand from the Construction Sector

4.1.2 Other Drivers

4.2 Restraints

4.2.1 Over-reliance on Imports of Raw Materials and Finished Plastics

4.2.2 Environmental Concerns of Plastics and the Availability of New Substitutes

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Raw Material Analysis

5. MARKET SEGMENTATION (Market Size in Volume)

5.1 Type

5.1.1 Traditional Plastics

5.1.1.1 Polyethylene

5.1.1.2 Polypropylene

5.1.1.3 Polystyrene

5.1.1.4 Polyvinyl Chloride

5.1.2 Engineering Plastics

5.1.2.1 Polyurethanes

5.1.2.2 Fluoropolymers

5.1.2.3 Polyamides

5.1.2.4 Polycarbonates

5.1.2.5 Styrene Copolymers (ABS and SAN)

5.1.2.6 Thermoplastic Polyesters

5.1.2.7 Other Engineering Plastics

5.1.3 Bioplastics

5.2 Technology

5.2.1 Blow Molding

5.2.2 Extrusion

5.2.3 Injection Molding

5.2.4 Other Technologies

5.3 Application

5.3.1 Packaging

5.3.2 Electrical and Electronics

5.3.3 Building and Construction

5.3.4 Automotive and Transportation

5.3.5 Housewares

5.3.6 Furniture and Bedding

5.3.7 Other Applications

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis**

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Agc Inc.

6.4.2 Billion Industrial Holdings Limited

6.4.3 Far Eastern New Century Corporation

6.4.4 Hyosung Chemical

6.4.5 Lyondellbasell Industries Holdings Bv

6.4.6 Nan Ya Plastics Corporation

6.4.7 Nsrp Llc

6.4.8 Scg Chemicals Public Company Limited

6.4.9 Toray Industries Inc.

6.4.10 Vietnam Oil And Gas Group

6.4.11 Vietnam Polystyrene Co. Ltd

6.4.12 Vinaplast

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increase in Foreign Investments

7.2 Other Opportunities

Vietnam Plastic Industry Segmentation

Plastics are a broad category of synthetic or semi-synthetic materials that contain polymers as a primary component. Plastics can be molded, extruded, or pressed into solid objects of various shapes due to their plasticity. This adaptability, along with a variety of other properties, such as being lightweight, durable, flexible, and low cost of production, led to their widespread use. The Vietnamese plastics market is segmented by type, technology, and application. By type, the market is segmented into traditional plastics, engineering plastics, and bioplastics. By technology, the market is segmented into blow molding, extrusion, injection molding, and other technologies. By application, the market is segmented into packaging, electrical and electronics, building and construction, automotive and transportation, housewares, furniture and bedding, and other applications. For each segment, the market sizing and forecasts have been done on the basis of volume (kilo tons).

| Type | |||||||||

| |||||||||

| |||||||||

| Bioplastics |

| Technology | |

| Blow Molding | |

| Extrusion | |

| Injection Molding | |

| Other Technologies |

| Application | |

| Packaging | |

| Electrical and Electronics | |

| Building and Construction | |

| Automotive and Transportation | |

| Housewares | |

| Furniture and Bedding | |

| Other Applications |

Vietnam Plastic Market Research FAQs

How big is the Vietnam Plastics Market?

The Vietnam Plastics Market size is expected to reach 11.84 million tons in 2025 and grow at a CAGR of 8.44% to reach 17.76 million tons by 2030.

What is the current Vietnam Plastics Market size?

In 2025, the Vietnam Plastics Market size is expected to reach 11.84 million tons.

Who are the key players in Vietnam Plastics Market?

Far Eastern New Century, Hyosung Chemicals, Nghi Son Refinery and Petrochemical (NSRP), Billion Industrial Holdings Limited and SCG Chemicals Public Company Limited (TPC VINA) are the major companies operating in the Vietnam Plastics Market.

What years does this Vietnam Plastics Market cover, and what was the market size in 2024?

In 2024, the Vietnam Plastics Market size was estimated at 10.84 million tons. The report covers the Vietnam Plastics Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Vietnam Plastics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Vietnam Plastics Market Research

Mordor Intelligence provides a comprehensive analysis of the plastics industry in Vietnam. The research covers everything from plastic manufacturing processes to end-user applications. Our extensive study includes thermoplastics, thermoset plastics, and emerging bioplastics technologies. The report offers detailed insights into the production of plastic materials, such as plastic resins, plastic compounds, and engineering plastics. It also analyzes key processes like plastic molding, plastic extrusion, and plastic injection techniques.

Stakeholders gain valuable insights into plastic packaging trends, industrial plastics applications, and the increasing demand for sustainable plastics. The report examines the evolution of recyclable plastics and biodegradable plastics, alongside traditional synthetic plastics and specialty plastics. Our analysis covers the entire value chain, from plastic raw materials to finished plastic products, including plastic components and plastic films. The comprehensive report PDF is available for download, featuring detailed analysis of plastic processing technologies, plastic additives, and emerging plastic composites applications in the Vietnamese market.