Vietnam Plastic Packaging Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

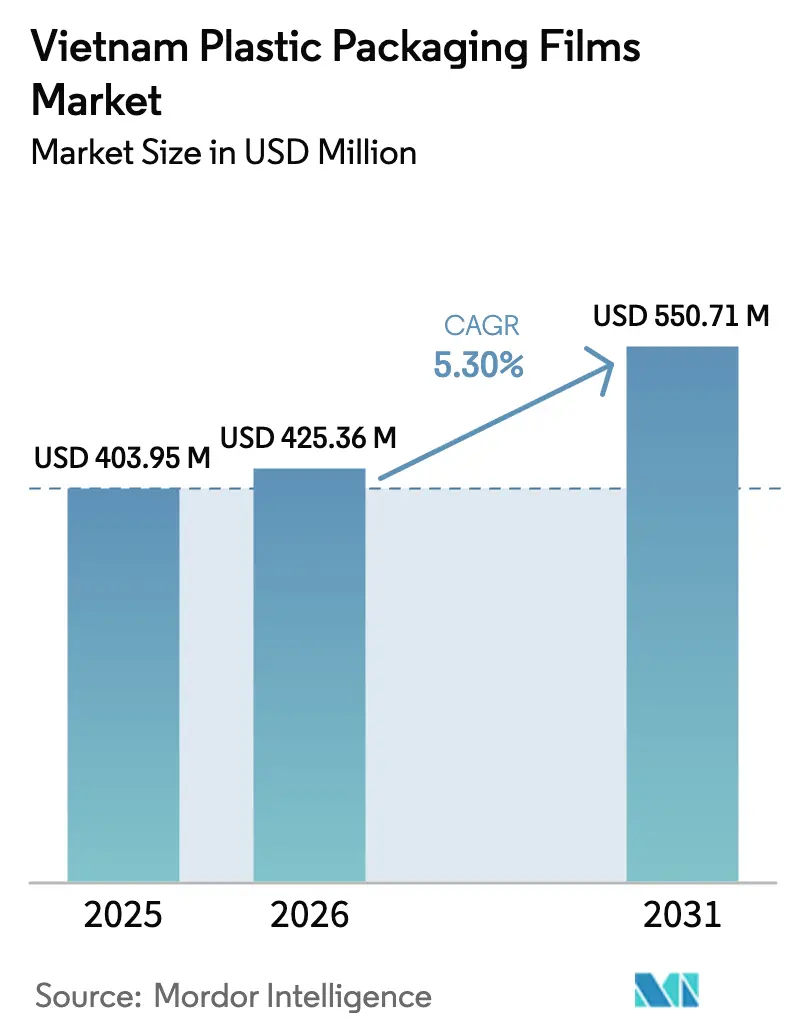

| Base Year Market Size (2025) | USD 403.95 Million |

| Market Size (2026) | USD 425.36 Million |

| Market Size (2031) | USD 550.71 Million |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Plastic Packaging Films Market Analysis by Mordor Intelligence

Vietnam plastic packaging films market size in 2026 is estimated at USD 425.36 million, growing from 2025 value of USD 403.95 million with 2031 projections showing USD 550.71 million, growing at 5.30% CAGR over 2026-2031. Growth reflects Vietnam’s position as a manufacturing hub where an expanding FMCG base intersects with stricter environmental rules that push converters toward thinner, more recyclable structures. Government eco-plastic mandates enacted in 2024 accelerate thin-gauge polyethylene adoption, even as foreign direct investment (FDI) of USD 1.25 billion from South Korea in January 2025 signals continued capacity expansion Seafood exports, modern retail proliferation and e-commerce logistics multiply demand for diverse barrier profiles, while resin price swings and fragmented recycling infrastructure compress converter margins.[1]“SK's billion-dollar investment marks a strong return of Korean investors to Việt Nam,” Vietnam News, vietnamnews.vn

Key Report Takeaways

- By end-use industry, food packaging led with 55.20% of Vietnam plastic packaging films market share in 2025; healthcare and pharmaceuticals are projected to grow at a 7.52% CAGR through 2031.

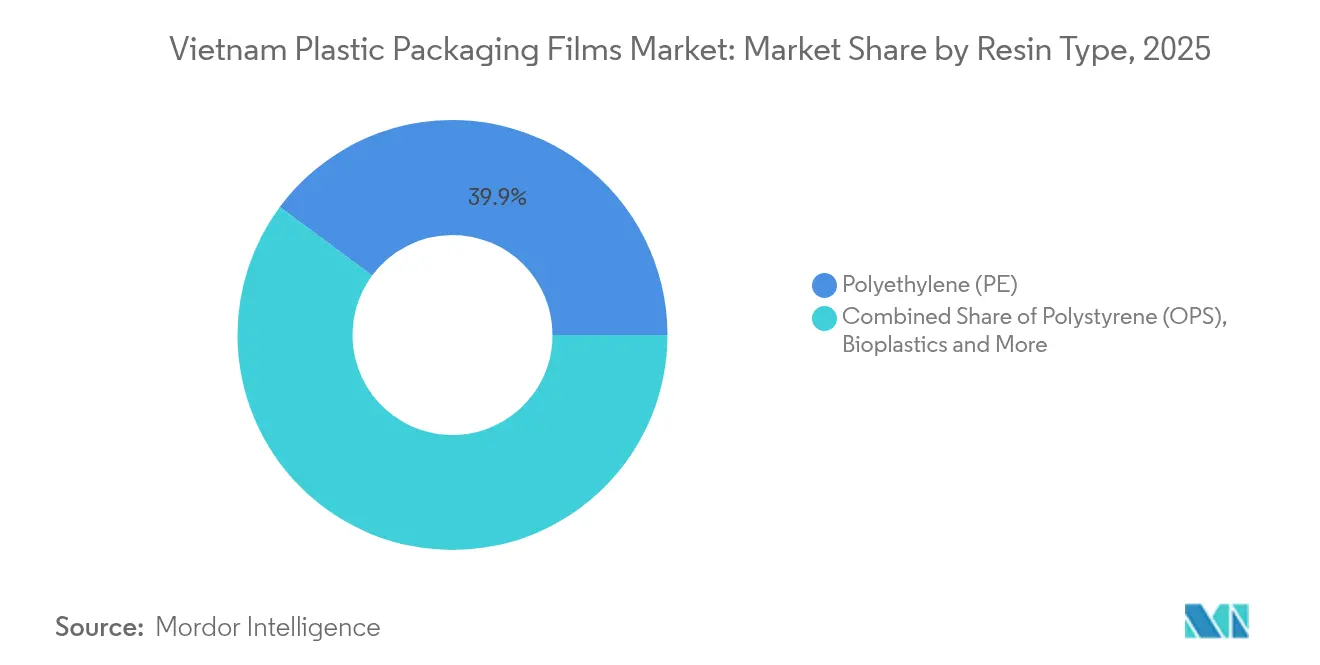

- By resin type, polyethylene retained 39.85% of the Vietnam plastic packaging films market share in 2025, whereas bioplastics are set to expand at an 8.21% CAGR to 2031.

- By film functionality, low-barrier mono-material films captured 60.70% of the Vietnam plastic packaging films market size in 2025; high-barrier multilayer films are advancing at a 6.55% CAGR to 2031.

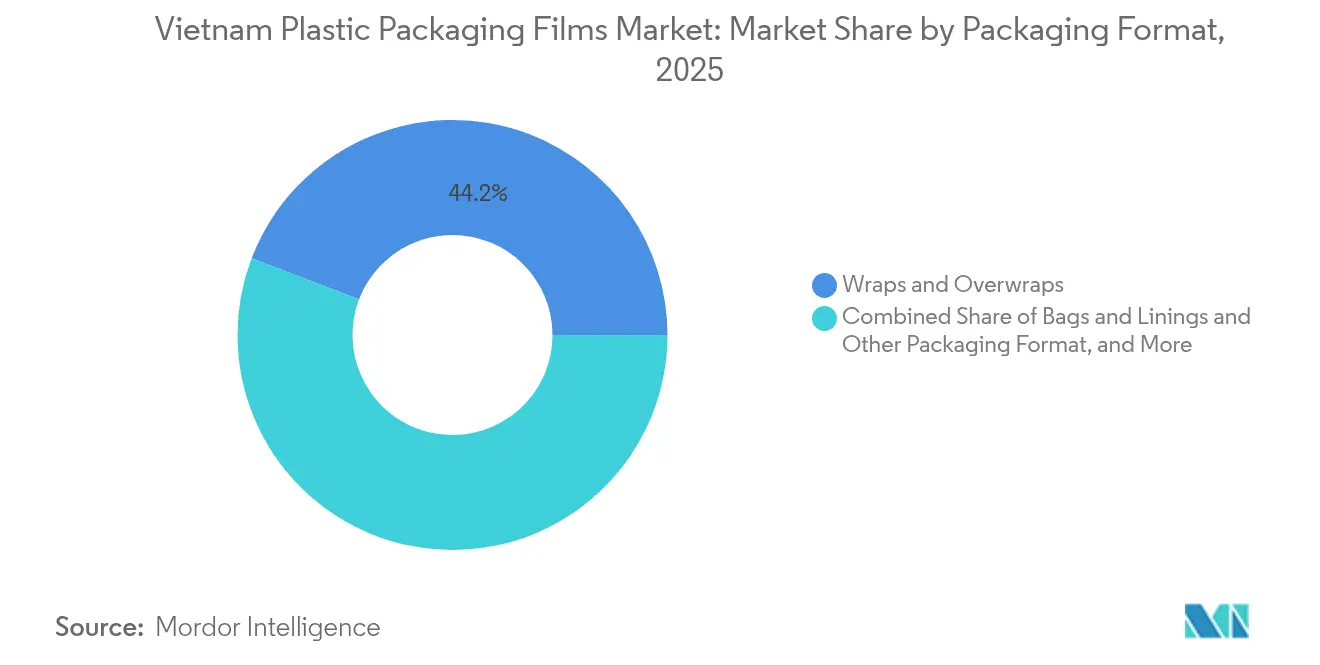

- By packaging format, wraps and overwraps held 44.20% revenue share in 2025, but pouches are expected to post the fastest 8.72% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Plastic Packaging Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming domestic FMCG production accelerating flexible-film demand | +1.2% | National, concentrated in Ho Chi Minh City and Hanoi industrial zones | Medium term (2-4 years) |

| Government eco-plastic mandates driving thin-gauge PE film adoption | +0.8% | National, with stricter enforcement in major cities | Long term (≥ 4 years) |

| Expansion of modern retail chains boosting shelf-ready film needs | +0.7% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Seafood-export growth requiring high-barrier multilayer films | +0.6% | Coastal provinces, Mekong Delta region | Short term (≤ 2 years) |

| E-commerce logistics surge increasing secondary film usage | +0.9% | National, with concentration in major urban centers | Short term (≤ 2 years) |

| FDI in food plants localising PET/BOPP film sourcing | +0.5% | Industrial parks nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Domestic FMCG Production Accelerating Flexible-Film Demand

Vietnam’s FMCG producers keep scaling output for domestic and export sales, pushing converters to deliver short-lead custom films. Unilever Vietnam’s planned USD 125 million upgrade of its Cu Chi site illustrates how multinationals are localising inputs, thereby lifting orders for specialty films.[2]“Unilever Việt Nam 'chơi lớn': Tăng vốn nhà máy Củ Chi lên gần 3.000 tỷ, muốn tự sản xuất Sorbitol,” Cafef, cafef.vnNew fruit-processing capacity in Tra Vinh follows the same path, widening opportunities for mid-tier converters that promise rapid turnaround. A 32% year-on-year jump in plastic exports in H1 2024 underlines the sector’s momentum.

Government Eco-Plastic Mandates Driving Thin-Gauge PE Film Adoption

Extended Producer Responsibility (EPR) rules, effective January 2024, impose minimum recycling rates and steer buyers toward mono-material structures. Thin-gauge polyethylene thus gains preference because it meets recyclability targets without compromising seal performance. Retailers such as AEON target 85% eco-friendly packaging by 2025, compelling suppliers to shift portfolios.

Expansion of Modern Retail Chains Boosting Shelf-Ready Film Needs

Chains penetrating secondary cities demand shelf-ready packs that tolerate automated handling and longer display cycles. Services contributed 43.44% of Vietnam’s Q1 2025 GDP, spotlighting retail as a rising force in pack specification. Converters equipped with puncture-resistant, high-clarity films gain an edge as retailers standardise formats and require global-grade certifications.

Seafood-Export Growth Requiring High-Barrier Multilayer Films

A spike in shrimp and fish processing, typified by a new 15,000-ton Dong Thap plant, drives usage of multilayer films that hold oxygen and moisture at bay over long export legs. Suppliers offering vacuum or modified-atmosphere packaging can lock in higher margins because compliance with international food-safety codes narrows the field.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented recycling ecosystem limiting PCR resin supply | -0.9% | National, more acute in rural areas | Long term (≥ 4 years) |

| City-level single-use plastic bans shifting demand to paper | -0.6% | Major urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Imported resin-price volatility compressing converter margins | -1.1% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Shortage of skilled orientation technicians constraining scale-up | -0.4% | Industrial zones nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Recycling Ecosystem Limiting PCR Resin Supply

Recycling rates hover near 25%, leaving converters short of post-consumer resin needed for EPR compliance. Duy Tân’s 100,000-ton plant in Long An is world-class, yet national capacity still trails demand, pushing firms back to virgin resin and raising costs.[3]“Vietnam PET Recycling: Accelerating post-consumer PET recycling in Vietnam,” FiinGroup, fiingroup.vn

Imported Resin-Price Volatility Compressing Converter Margins

Vietnam imports up to 80% of its resin, so price gyrations in global polypropylene cut directly into thin converter margins. PP landed in August 2024 at USD 950-990 per ton, then rebounded, complicating stock planning. Domestic producer Long Son Petrochemicals even idled operations amid poor spreads in late 2024, keeping the market exposed to foreign pricing cycles.[4]Unknown, “PP prices fall to year-to-date lows in Vietnam,” ChemOrbis, chemorbis.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Bioplastics Drive Innovation Despite PE Dominance

Polyethylene held 39.85% of the Vietnam plastic packaging films market share in 2025. Bioplastics, while smaller in volume, expand at an 8.21% CAGR as brands chase compostable labels. An Phat’s AnEco line and EuroPlas’s BiONext compounds highlight the shift toward plant-based feedstocks. Polypropylene remains vital for clarity and heat resistance, whereas BOPET satisfies high-barrier niches. Recent customs approvals for recycled PP homopolymers indicate state backing for circular feedstocks.

Bioplastics’ premium pricing still limits widespread uptake, yet new capacity plus tightening EPR targets are expected to carve larger slices of the Vietnam plastic packaging films market size through 2031. Commercial trials in mono-material pouch laminates reveal that converters can balance functionality with compostability, easing brand migration.

By Film Functionality: Multilayer Films Gain Traction

Low-barrier mono-material films led with 60.70% revenue in 2025, prized for recyclability under EPR. High-barrier multilayer formats, however, post 6.55% CAGR as seafood and processed foods need longer shelf life. Metallised medium-barrier films serve snack and instant-noodle packs, combining shelf appeal with moderate protection. Active and antimicrobial coatings are surfacing to curtail mold in Vietnam’s humid climate.

Converters investing in triple-bubble or MDO technology can supply thinner yet tougher laminates, aligning with both cost and sustainability targets. This capability strengthens export competitiveness because global buyers increasingly specify downgauged but high-performance structures.

By Packaging Format: Pouches Capitalize on Convenience Trends

Wraps and overwraps controlled 44.20% sales in 2025. Pouches, especially stand-up variants, expand 8.72% annually as consumers' priorities and portion control. Spouted pouches for liquid condiments and baby food are gaining traction in urban areas. Industrial sacks retain relevance for rice, fertilizer, and resin transport.

E-commerce adds weight to puncture-resistant courier bags and bubble mailer films. Converters that tailor tear-notch, laser-score, and zipper features secure contracts with leading online retailers seeking differentiation and minimal leakage risk.

By End-use Industry: Healthcare Emerges as Growth Driver

Food retained a 55.20% share of the Vietnam plastic packaging films market size during 2025. Pharmaceutical and healthcare usage accelerates at 7.52% CAGR, owing to projects such as Bidiphar’s USD 35 million sterile drugs facility. Personal care films also build on the back of Unilever’s localisation push. Industrial segments rely on heavy-duty wraps for exports. Rising pet ownership in urban hubs is spawning demand for high-barrier pet-food pouches.

Enhanced infection-control rules introduced in 2025 spur multilayer medical film sales. Hospitals request gamma-sterilisable, puncture-proof bags, providing a high-margin outlet that buffers converters from commodity price swings.

Geography Analysis

Southern Vietnam, anchored by Ho Chi Minh City, generated the highest regional revenue on the back of dense industrial estates, proximity to ports, and established resin distribution. Northern clusters around Hanoi log the fastest CAGR as electronics, textiles, and automotive plants emerge with FDI support. A USD 1.25 billion Korean package announced in early 2025 pushes additional demand for protective films across assembly lines.

The Mekong Delta stimulates orders for high-barrier seafood films and moisture-control wraps for fruit exports. Coastal provinces ship frozen shrimp worldwide, requiring oxygen-proof laminates. Central Vietnam, aided by new highway links, shifts from agriculture toward light industry, creating fresh demand pockets.

Urban plastic bans in Hanoi and Ho Chi Minh City redirect some orders toward coated paper, trimming plastic film volumes locally. Yet rural and peri-urban markets continue to prefer cost-effective polyethylene sacks. Collectively, these regional dynamics foster a diversified Vietnam plastic packaging films market, reducing over-dependence on any one customer base.

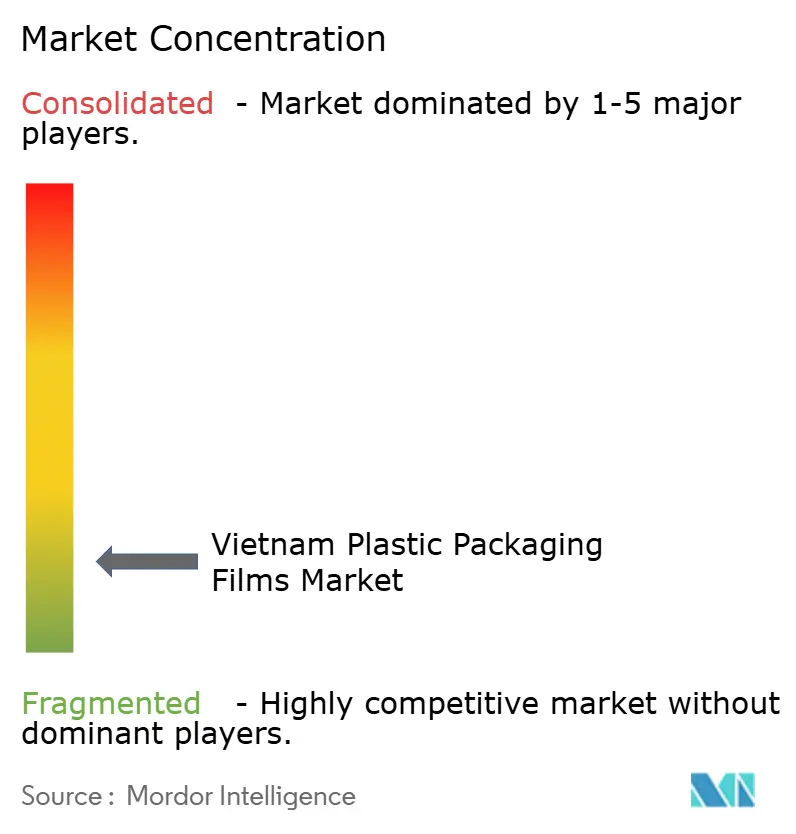

Competitive Landscape

The Vietnam plastic packaging films market remains fragmented. Local firms include An Phat Holdings, Duy Tân Plastics, and EuroPlas, competing against Japan’s Nitto Denko and Thailand’s SCG Chemicals. Price competition prevails in commodity grades, but specialty segments reward technical investment. An Phat’s cautious 2025 revenue target of VND 9.179 trillion reflects trade uncertainty, yet its eco-film focus positions it for future regulatory benefits.[5]“ĐHĐCĐ thường niên APH 2025: Kế hoạch kinh doanh thận trọng giữa 'bão' thương mại,” Cafef, cafef.vn

Vertical integration appears as a key strategy. Duy Tân operates both recycling and converting lines, ensuring a PCR supply. Foreign players introduce multilayer extrusion and in-line MDO to raise gauge control and optical clarity. Joint ventures with resin suppliers help manage volatility. Firms investing in ISO 13485, BRC, or FSSC 22000 certification win export-oriented food and pharma contracts, where compliance hurdles deter smaller rivals.

Vietnam Plastic Packaging Films Industry Leaders

Rang Dong Long An Plastic JSC

Polifilm Vietnam Co. Ltd.

IFC Plastic Co., Ltd.

Feliz Plastic Vietnam Co., Ltd.

Vietnam Packing Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SYRE Impact AB received investment certification for a USD 1 billion PET textile-to-resin recycling complex in Bình Định province, creating Vietnam’s largest polyester circular‐economy facility with 250,000 tons annual capacity expected to start up in 2029.

- March 2025: An Phat Holdings broke ground on a USD 67 million PBAT resin plant in Hải Dương to secure feedstock for its AnEco compostable films line, targeting commercial output by 2026.

- November 2024: SCG Chemicals earmarked USD 700 million to upgrade feedstock flexibility at Long Son Petrochemicals, completion by 2027.

- September 2024: CCL Label opened a USD 20 million sleeve-label and specialty-film converting facility in Ho Chi Minh City, lifting regional capacity to 300 million meters per year.

Vietnam Plastic Packaging Films Market Report Scope

Plastic film packaging refers to various thin plastic materials that wrap or protect products. These films are commonly used in the food, pharmaceutical, and other industries. The report tracks the demand for converted packaging films across major resin and application types. This encompasses a range of materials and uses, reflecting the market's varied requirements and the evolving preferences of consumers and businesses.

The Vietnamese plastic packaging films market is segmented by type (polypropylene (biaxially oriented polypropylene (BOPP) and cast polypropylene (CPP)), polyethylene (low-density polyethylene (LDPE) and linear low-density polyethylene (LLDPE)), polyethylene terephthalate (biaxially oriented polyethylene terephthalate (BOPET)), polystyrene, bio-based, and PVC, EVOH, PETG, and other film types) and by end-user industry (food [candy and confectionery, frozen foods, fresh produce, dairy products, dry foods, meat, poultry, and seafood, pet food, and other food products (seasonings and spices, spreadable, sauces, condiments, etc.)], healthcare, personal care and home care, industrial packaging, and other end-user industry applications). The report offers market forecasts and size in volume (tonnes) for all the above segments.

| Polypropylene (PP) |

| Polyethylene (PE) |

| Polyethylene-terephthalate (BOPET) |

| Polystyrene (OPS) |

| Bioplastics |

| Other Material Types |

| Wraps and Overwraps |

| Bags and Linings |

| Pouches (stand-up, spouted) |

| Other Packging Format |

| Low-Barrier Mono-material Films |

| Medium-Barrier Metallised Films |

| High-Barrier Multilayer Films |

| Specialty Active and Antimicrobial Films |

| Food | Candy and Confectionery |

| Frozen Foods | |

| Fresh Produce | |

| Dairy Products | |

| Dry Foods | |

| Meat, Poultry and Seafood | |

| Pet Food | |

| Other Food Products | |

| Healthcare and Pharmaceutical | |

| Personal Care and Home Care | |

| Industrial Packaging | |

| Other End-use Industry |

| By Resin Type | Polypropylene (PP) | |

| Polyethylene (PE) | ||

| Polyethylene-terephthalate (BOPET) | ||

| Polystyrene (OPS) | ||

| Bioplastics | ||

| Other Material Types | ||

| By Packaging Format | Wraps and Overwraps | |

| Bags and Linings | ||

| Pouches (stand-up, spouted) | ||

| Other Packging Format | ||

| By Film Functionality | Low-Barrier Mono-material Films | |

| Medium-Barrier Metallised Films | ||

| High-Barrier Multilayer Films | ||

| Specialty Active and Antimicrobial Films | ||

| By End-use Industry | Food | Candy and Confectionery |

| Frozen Foods | ||

| Fresh Produce | ||

| Dairy Products | ||

| Dry Foods | ||

| Meat, Poultry and Seafood | ||

| Pet Food | ||

| Other Food Products | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Home Care | ||

| Industrial Packaging | ||

| Other End-use Industry | ||

Key Questions Answered in the Report

What is the current size of the Vietnam plastic packaging films market?

The market is valued at USD 425.36 million in 2026.

How fast is the Vietnam plastic packaging films market expected to grow?

It is projected to advance at a 5.30% CAGR, reaching USD 550.71 million by 2031.

Which end-use industry represents the largest demand?

Food packaging leads with 55.20% of market share in 2025.

Which resin type is growing the quickest?

Bioplastics expand at an 8.21% CAGR, the fastest among all resin categories.

What regional area in Vietnam shows the highest growth potential?

Northern Vietnam, driven by new FDI-backed electronics and automotive facilities, records the highest forecast CAGR.

How are eco-plastic regulations affecting converters?

Extended Producer Responsibility rules compel adoption of thin, mono-material polyethylene and incentivise investment in recycling-compatible technologies.

Page last updated on: