| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Volume (2025) | 324.57 Million Liters |

| Market Volume (2030) | 420.19 Million Liters |

| CAGR | 5.30 % |

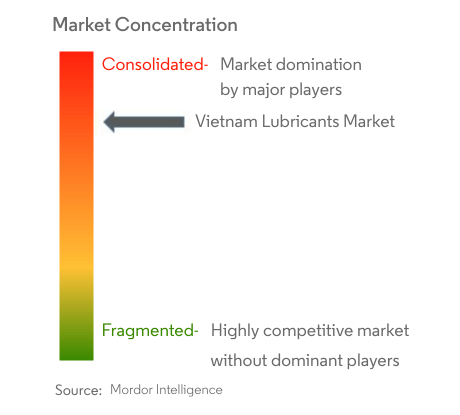

| Market Concentration | High |

Vietnam Lubricants Market Analysis

The Vietnam Lubricants Market size is estimated at 324.57 million liters in 2025, and is expected to reach 420.19 million liters by 2030, at a CAGR of 5.3% during the forecast period (2025-2030).

Vietnam's manufacturing sector has emerged as a key driver of industrial growth, with the manufacturing value added increasing by 8.59% in 2021, supported by significant foreign direct investment inflows. The country attracted USD 22.5 billion in FDI for its manufacturing sector in 2021, representing 57.9% of total investment, highlighting its growing prominence as a regional manufacturing hub. Major investments in 2022, including Lego A/S's USD 1.3 billion project and Trina Solar's USD 275 million facility, demonstrate continued investor confidence in Vietnam's industrial capabilities. This manufacturing expansion has created substantial opportunities for industrial lubricants across various applications, from machinery maintenance to production processes.

The power generation sector in Vietnam is undergoing significant transformation, with substantial capacity additions across both conventional and renewable energy sources. In 2021, the country expanded its power generation infrastructure by adding 2.96 GW of non-renewable energy capacity and 4.36 GW of renewable energy capacity. The government's commitment to energy diversification is evident in its power development plan, which aims to nearly double the total installed power generation capacity to 146,000 megawatts by 2030. This expansion has led to increased demand for specialized turbine oil and transformer oil used in power generation equipment, particularly in turbines and generators.

The metallurgical and metalworking sector has shown robust growth, with Vietnam's steel production reaching 26.15 million tons in 2021. The sector's expansion is further supported by major infrastructure projects and growing domestic demand for steel products. Companies like Hoa Phat are investing in capacity expansion, with the second phase of the Hoa Phat Dung Quat Iron and Steel Production Complex expected to increase total capacity to 11 million tonnes per year by 2024. This growth in metal processing activities has driven demand for metalworking fluids and specialized industrial lubricants.

The industrial infrastructure landscape is evolving with the development of new industrial zones and manufacturing facilities. Recent developments include the Deep C 2 Hai Phong Industrial Zone and various other infrastructure projects that are attracting both domestic and international investments. The chemical manufacturing sector has shown particular dynamism, with companies like Trina Solar establishing new production facilities. These developments have created new demand centers for industrial oil and process oil, particularly in hydraulic systems, machinery maintenance, and process applications, while also driving the need for more sophisticated lubricants solutions to meet evolving technological requirements.

Vietnam Lubricants Market Trends

Growing Automotive Industry and Vehicle Population

The robust growth in Vietnam's automotive sector is serving as a primary driver for the automotive lubricants market. The passenger vehicle segment has shown remarkable momentum, with sales surging by 49.12% in 2022, reflecting the country's improving economic performance and shifting consumer preferences from motorcycles to passenger vehicles. This transformation is further supported by Vietnam's liberalized economic environment, which has resulted in import tax reductions on various products, making cars more affordable for the growing middle-class population. The increasing disposable incomes and perception of cars as a safer and more convenient mode of transportation continue to fuel this transition.

The commercial vehicle sector's steady expansion, particularly in mini trucks, is creating sustained demand for engine oil and transmission fluid. Mini trucks have emerged as growth engines for the commercial vehicles segment, becoming the preferred choice for most commercial activities—from transporting commodities and agricultural produce between markets to moving industrial goods between factories, warehouses, and stores. The availability of easy financing plans and a steady stream of regular business across sectors has made mini trucks an attractive option for commercial operators, thereby driving the demand for various lubricant products including engine oils, transmission fluids, and greases.

Understand The Key Trends Shaping This Market

Download PDF

Industrial Manufacturing Expansion

Vietnam's manufacturing sector is experiencing substantial growth, supported by significant foreign direct investment and expansion of industrial facilities. In the first half of 2022, major investments such as Lego A/S's $1.3 billion project and Trina Solar's $275 million chemical production facility demonstrate the robust industrial growth trajectory. These investments are creating new demand channels for industrial lubricants, particularly in specialized applications such as hydraulic fluids, metalworking fluids, and industrial greases. The expansion of manufacturing capabilities across sectors including electronics, textiles, and automotive components is driving the need for high-performance lubricants that can ensure optimal equipment operation and maintenance.

The country's focus on developing high-value industrial sectors is reflected in the growth of basic metals production, motor vehicle manufacturing, and electronic components production. The industrial sector's advancement is particularly evident in the steel industry, where companies like Hoa Phat are expanding their production capabilities. The construction of the second phase of the Hoa Phat Dung Quat Iron and Steel Production Complex, which aims to increase total capacity to 11 million tonnes per year by 2024, exemplifies the scale of industrial expansion driving lubricant demand. This industrial growth is creating sustained demand for specialized lubricants designed for high-temperature operations, heavy-load applications, and precision manufacturing processes.

Power Generation Capacity Expansion

Vietnam's ambitious power sector development plans are creating significant opportunities for industrial lubricants. The country aims to nearly double its total installed power generation capacity to 146,000 megawatts by 2030, with a strong emphasis on renewable energy sources. This expansion includes comprehensive plans for both conventional and renewable energy facilities, each requiring specific types of lubricants for optimal operation. The development roadmap includes the construction of 11 new coal-fired power plants to raise coal-fired power capacity to 36 GW by 2030, alongside significant investments in renewable energy infrastructure.

The country's commitment to renewable energy, targeting 50% of power supply from solar and wind energy by 2045, is driving demand for specialized lubricants designed for wind turbines and solar power equipment. This transition is complemented by significant investments in the energy sector, with Vietnam allocating over $691 million in 2022 for energy development, including the construction of four hydropower plants scheduled for completion by 2025. The diverse power generation portfolio, ranging from conventional thermal plants to wind farms and solar installations, is creating sustained demand for various types of industrial lubricants, including turbine oils, hydraulic fluids, and high-performance greases designed for specific power generation applications.

Infrastructure Development Initiatives

Vietnam's comprehensive infrastructure development agenda, anchored by the Prime Minister-approved road development plan for 2021-2030, is creating substantial demand for construction lubricants and heavy equipment lubricants. The expansion of transportation infrastructure is driving the need for various types of construction machinery and equipment, each requiring specific lubricant solutions for optimal performance. This infrastructure push is complemented by the development of new industrial zones and urban development projects, creating a sustained demand for construction equipment and associated lubricant products.

The development of major infrastructure projects, including the Quang Tri Power Plant project and various industrial zones like Deep C 2 Hai Phong Industrial Zone and Core5 Hai Phong, is generating significant demand for heavy equipment lubricants. These projects require a wide range of construction machinery, from excavators and bulldozers to cranes and concrete pumps, each necessitating specific types of lubricants for their operation and maintenance. The continuous nature of these infrastructure developments, combined with the government's commitment to modernizing the country's infrastructure network, ensures a steady demand for construction equipment lubricants, including hydraulic fluids, gear oils, and heavy-duty greases.

Segment Analysis: By End-User Industry

Automotive Segment in Vietnam Lubricants Market

The automotive segment continues to dominate the Vietnam lubricants market, commanding approximately 71% of the total market share in 2024. This substantial market position is primarily driven by the high proportion of engine oil and transmission fluid usage in motor vehicles compared to any other application. The segment's dominance is reinforced by Vietnam's large motorcycle population, growing passenger vehicle sales, and expanding commercial vehicle fleet. The increasing preference for passenger vehicles among Vietnamese consumers, coupled with the country's improving economic performance, has significantly contributed to the high demand for automotive lubricants. Additionally, the strong recovery in sales of motor vehicles, particularly in the passenger vehicle segment, has further strengthened the automotive segment's position in the lubricants market.

Power Generation Segment in Vietnam Lubricants Market

The power generation segment is emerging as a key growth driver in Vietnam's lubricants market, with projections indicating robust expansion through 2024-2029. This growth is primarily fueled by Vietnam's ambitious plans to nearly double its total installed power generation capacity to 146,000 megawatts by 2030. The segment's expansion is further supported by the country's strategic focus on developing renewable energy sources, with targets to raise solar and wind energy contribution to 50% of Vietnam's power supply by 2045. The increasing investments in new power projects, including both conventional and renewable energy facilities, are creating substantial demand for specialized lubricants used in power generation equipment. The sector's growth is also bolstered by ongoing maintenance requirements of existing power infrastructure and the expansion of thermal power facilities across the country.

Remaining Segments in Vietnam Lubricants Market End-User Industry

The remaining segments in the Vietnam lubricants market include heavy equipment, metallurgy and metalworking, and other industrial applications, each serving distinct market needs. The heavy equipment segment plays a crucial role in supporting Vietnam's construction and infrastructure development projects, with demand driven by the country's ongoing urbanization and industrial expansion. The metallurgy and metalworking segment's consumption is closely tied to the nation's growing steel production and manufacturing activities, particularly in the automotive and construction sectors. Other industrial applications encompass various sectors such as textile manufacturing, food processing, and chemical production, contributing to the diverse application landscape of industrial lubricants in Vietnam.

Segment Analysis: By Product Type

Engine Oils Segment in Vietnam Lubricants Market

Engine oils dominate the Vietnam lubricants market, accounting for approximately 69% of the total market volume in 2024. This significant market share is primarily attributed to the high-volume requirements and low drain interval characteristics of engine oils, as they are extensively used in high-temperature and high-pressure applications. The segment's dominance is further strengthened by the robust automotive sector in Vietnam, particularly in the passenger vehicle segment which has shown strong growth in recent years. Engine oil consumption is mostly supported by the servicing requirements of the current on-road passengers and commercial vehicles, with the automotive segment holding nearly 89% of engine oil consumption, followed by the heavy equipment industry and power generation sectors.

Transmission & Gear Oils Segment in Vietnam Lubricants Market

The transmission and gear oils segment is projected to exhibit strong growth in the Vietnam lubricants market, with an expected growth rate of approximately 5% during 2024-2029. This growth is primarily driven by the increasing demand from the automotive sector, particularly from commercial vehicles which account for a significant portion of transmission fluid consumption. The segment's growth is further supported by the rising adoption of automatic transmission fluid over manual transmission fluid, which has increased oil change service intervals. The expansion in hybrid vehicle adoption, which requires both ATF and electric components, is also contributing to the segment's growth trajectory. Additionally, the power generation industry and other industrial sectors are creating substantial demand for gear oil.

Remaining Segments in Product Type Segmentation

The Vietnam lubricants market encompasses several other important segments including hydraulic fluids, metalworking fluids, and greases, each serving specific industrial and automotive applications. Hydraulic fluids play a crucial role in heavy equipment industries and manufacturing sectors, while metalworking fluids are essential in the growing metal manufacturing and processing industries. The greases segment maintains its significance in various applications ranging from automotive bearings to industrial machinery maintenance. These segments collectively contribute to the market's diversity and cater to the specific lubrication needs of Vietnam's expanding industrial base, with each segment showing steady growth patterns aligned with their respective end-user industries.

Vietnam Lubricants Industry Overview

Top Companies in Vietnam Lubricants Market

The Vietnam lubricants market is characterized by intense competition among both global and local players, with companies like BP Plc (Castrol), Petrolimex, Shell PLC, TotalEnergies, and Mekong Petrochemical JSC leading the market. Product innovation has emerged as a key strategic focus, with companies developing advanced synthetic lubricants, eco-friendly formulations, and specialized products for electric vehicles. Operational agility is demonstrated through extensive distribution networks, partnerships with automotive manufacturers, and strategic alliances with local distributors. Companies are actively expanding their presence through joint ventures, such as the partnership between Castrol and Petrolimex, while also investing in marketing initiatives and brand development. The market has witnessed significant strategic moves including manufacturing facility expansions, technology upgrades, and the establishment of research and development centers to enhance product quality and meet evolving customer demands.

Consolidated Market with Strong Global Presence

The Vietnam lubricants market exhibits a consolidated structure where multinational corporations maintain significant market control through their established brands and technological expertise. These global players leverage their international experience, research capabilities, and strong financial resources to maintain market leadership, while local companies compete through their deep understanding of regional preferences and established distribution networks. The market has witnessed several strategic partnerships and joint ventures between international and local players, enabling companies to combine global expertise with local market knowledge.

The competitive landscape is further shaped by vertical integration strategies, with many leading players maintaining control over their supply chains from base oil production to distribution. Market consolidation continues through strategic acquisitions and partnerships, particularly evident in deals like SK Lubricants' acquisition of a stake in Mekong Petrochemical JSC. Local players are increasingly focusing on specialized market segments and developing specialty lubricants to compete effectively against global giants, while also investing in manufacturing capabilities and distribution infrastructure to enhance their market presence.

Innovation and Distribution Drive Future Success

Success in the Vietnam lubricants market increasingly depends on companies' ability to innovate and adapt to changing market dynamics, particularly in response to the growing demand for high-performance and environmentally friendly products. Companies need to focus on developing advanced synthetic lubricants, expanding their product portfolios to include specialized solutions for emerging industries, and strengthening their distribution networks through strategic partnerships. The ability to provide comprehensive technical support, after-sales services, and maintain strong relationships with OEMs will be crucial for maintaining market position.

Market contenders can gain ground by focusing on underserved segments, developing specialized products for specific industries, and building strong local distribution networks. The increasing focus on environmental regulations and sustainability presents opportunities for companies to differentiate themselves through eco-friendly products and sustainable practices. Success will also depend on the ability to navigate potential regulatory changes, particularly regarding environmental standards and product quality requirements, while maintaining cost competitiveness in a price-sensitive market. Companies must also consider the growing influence of digital channels and e-commerce platforms in reaching end-users, while investing in brand building and customer education initiatives.

Vietnam Lubricants Market Leaders

-

BP Plc (Castrol)

-

MEKONG PETROCHEMICAL JSC

-

Petrolimex (PLX)

-

Royal Dutch Shell Plc

-

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Vietnam Lubricants Market News

- May 2022: TotalEnergies, NEXUS Automotive Extend Strategic Partnership for a period of five years. As part of this partnership, TotalEnergies Lubricants will be expanding its presence in the burgeoning N! community, which has seen rapid growth in sales from EUR 7.2 billion in 2015 to nearly EUR 35 billion by the end of 2021.

- January 2022: Effective January 21, 2022, Royal Dutch Shell plc changes its name to Shell plc.

- December 2021: The joint venture agreement between Castrol, BP, and the Vietnam National Petroleum Group (Petrolimex) has been extended for another 20 years, from 2022 to 2042. Castrol BP Petco Co. Ltd is the name of the joint venture company.

Vietnam Lubricants Market Report - Table of Contents

1. Executive Summary & Key Findings

2. Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3. Key Industry Trends

- 3.1 Automotive Industry Trends

- 3.2 Manufacturing Industry Trends

- 3.3 Power Generation Industry Trends

- 3.4 Regulatory Framework

- 3.5 Value Chain & Distribution Channel Analysis

4. Market Segmentation

-

4.1 By End User

- 4.1.1 Automotive

- 4.1.2 Heavy Equipment

- 4.1.3 Metallurgy & Metalworking

- 4.1.4 Power Generation

- 4.1.5 Other End-user Industries

-

4.2 By Product Type

- 4.2.1 Engine Oils

- 4.2.2 Greases

- 4.2.3 Hydraulic Fluids

- 4.2.4 Metalworking Fluids

- 4.2.5 Transmission & Gear Oils

- 4.2.6 Other Product Types

5. Competitive Landscape

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

-

5.3 Company Profiles

- 5.3.1 AP SAIGON PETRO JSC

- 5.3.2 BP Plc (Castrol)

- 5.3.3 Chevron Corporation

- 5.3.4 MEKONG PETROCHEMICAL JSC

- 5.3.5 Motul

- 5.3.6 NIKKO LUBRICANT VIETNAM

- 5.3.7 Petrolimex (PLX)

- 5.3.8 PVOIL

- 5.3.9 Royal Dutch Shell Plc

- 5.3.10 TotalEnergies

- *List Not Exhaustive

6. Appendix

- 6.1 Appendix-1 References

- 6.2 Appendix-2 List of Tables & Figures

7. Key Strategic Questions for Lubricants CEOs

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Vietnam Lubricants Industry Segmentation

| By End User | Automotive |

| Heavy Equipment | |

| Metallurgy & Metalworking | |

| Power Generation | |

| Other End-user Industries | |

| By Product Type | Engine Oils |

| Greases | |

| Hydraulic Fluids | |

| Metalworking Fluids | |

| Transmission & Gear Oils | |

| Other Product Types |

Need A Different Region or Segment?

Customize Now

Vietnam Lubricants Market Research FAQs

How big is the Vietnam Lubricants Market?

The Vietnam Lubricants Market size is expected to reach 324.57 million Liters in 2025 and grow at a CAGR of 5.30% to reach 420.19 million Liters by 2030.

What is the current Vietnam Lubricants Market size?

In 2025, the Vietnam Lubricants Market size is expected to reach 324.57 million Liters.

Who are the key players in Vietnam Lubricants Market?

BP Plc (Castrol), MEKONG PETROCHEMICAL JSC, Petrolimex (PLX), Royal Dutch Shell Plc and TotalEnergies are the major companies operating in the Vietnam Lubricants Market.

What years does this Vietnam Lubricants Market cover, and what was the market size in 2024?

In 2024, the Vietnam Lubricants Market size was estimated at 307.37 million Liters. The report covers the Vietnam Lubricants Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Vietnam Lubricants Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Vietnam Lubricants Market Research

Mordor Intelligence provides a comprehensive analysis of the Vietnam lubricants industry. This analysis covers everything from automotive lubricants to specialized industrial applications. Our extensive research includes industrial lubricants, marine lubricants, and aviation lubricants. It also examines essential products like engine oil, transmission fluid, and various types of grease. The analysis offers detailed segments on synthetic lubricants, mineral lubricants, and specialty lubricants. These insights are crucial for stakeholders looking to understand market dynamics and growth opportunities.

Our detailed report, available as an easy-to-download PDF, offers in-depth analysis of specific sectors. These sectors include metalworking fluid, cutting fluid, transformer oil, and hydraulic fluid applications. The research covers vital industrial components such as compressor oil, turbine oil, gear oil, and process oil markets. Stakeholders in construction lubricants, mining lubricants, and refrigeration oil segments will find valuable insights into market trends, competitive landscapes, and growth projections. The report also examines emerging opportunities in industrial oil applications, providing comprehensive data for informed decision-making across the value chain.