Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

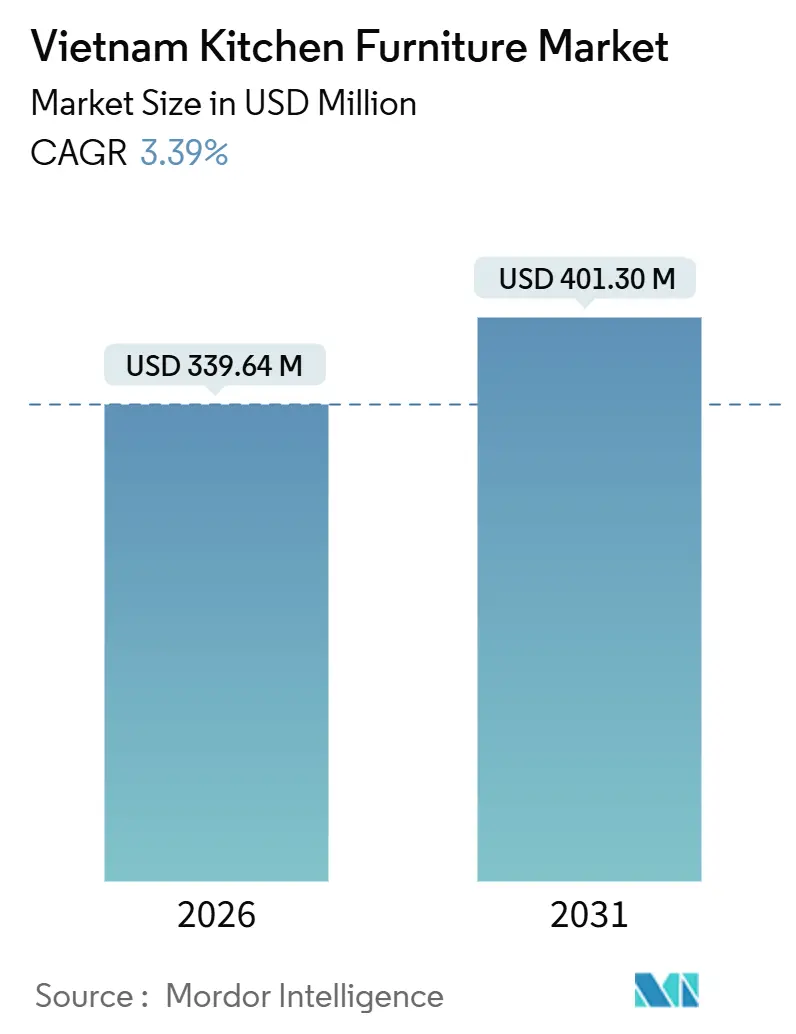

| Market Size (2026) | USD 339.64 Million |

| Market Size (2031) | USD 401.30 Million |

| Growth Rate (2026 - 2031) | 3.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Kitchen Furniture Market Analysis by Mordor Intelligence

The Vietnam Kitchen Furniture market size is USD 339.64 million in 2026 and is projected to reach USD 401.30 million by 2031 at a 3.39% CAGR, reflecting steady expansion in value despite shifting channel dynamics. Growth in the Vietnam Kitchen Furniture Market is driven by the pivot toward developer-bundled turnkey packages in high-rise projects, which concentrate specification power with project distributors and shorten sales cycles for scaled suppliers. This channel-led structure sits alongside a mature retail base where showroom experiences still matter for premium wood and custom finishes, although digital catalogs and remote advisory tools are improving buyer confidence for online purchases. The B2B/Project route, while a smaller slice today, is the fastest-growing pathway as developers standardize kitchens to support unit pre-sales and coordinated interior fit-outs. Policy reform that cuts construction-permit steps for projects with 1/500 planning approval, reducing timelines by three to six months and costs by 5%, reinforces the early-lock-in advantage for bulk kitchen orders.

Key Report Takeaways

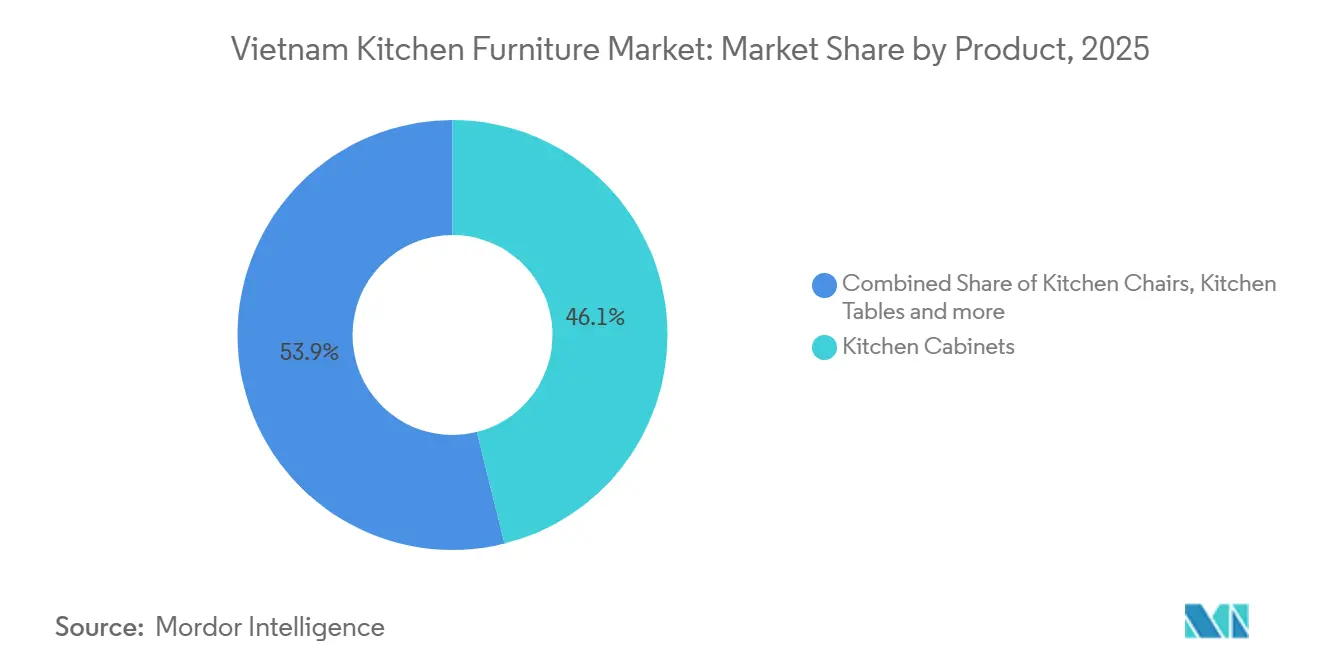

- By product, kitchen cabinets command 46.11% of the Vietnam kitchen furniture market share in 2025, while kitchen chairs post the fastest growth at a 3.91% CAGR through 2031.

- By material, wood accounts for 71.42% of the Vietnam kitchen furniture market share in 2025, while metal is advancing at a 4.17% CAGR through 2031.

- By end-user, residential represents 71.82% of the Vietnam kitchen furniture market share in 2025, while commercial is the fastest growing at a 4.76% CAGR through 2031.

- By distribution channel, B2C/retail holds 70.41% of the Vietnam kitchen furniture market share in 2025, while B2B/project is the fastest growing at a 4.28% CAGR through 2031.

- By geography, Ho Chi Minh City Metropolitan Area leads with 36.56% of the Vietnam kitchen furniture market share in 2025, while the Central Key Economic Region records the highest projected CAGR at 3.83% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Kitchen Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Developer-bundled turnkey kitchen packages in new condominium launches | +1.2% | Concentrated in HCMC MA and Hanoi & Red River Delta, expanding to Central KER. | Medium term (2–4 years) |

| National "Make-in-Vietnam Kitchen" branding campaign boosting local brand preference | +0.4% | National, strongest in HCMC MA & Hanoi, expanding to tier-2 cities via retail associations. | Medium term (2–4 years) |

| Expansion of modern retail & e-commerce channels | +0.8% | Strongest in HCMC & Hanoi urban cores, spill-over to tier-2 cities. | Short term (≤ 2 years) |

| Government incentives for wood processing & FDI | +0.7% | National, concentrated in Binh Duong, Dong Nai, and Binh Phuoc wood-processing zones. | Long term (≥ 4 years) |

| Surge in smart-home adoption | +0.6% | HCMC MA and Hanoi affluent districts, early gains in Da Nang premium developments. | Medium term (2–4 years) |

| Accelerated demand for green-certified materials | +0.5% | HCMC & Central KER (LOTUS-certified projects), expanding nationally under EUDR compliance. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Developer-Bundled Turnkey Kitchen Packages in New Condominium Launches

Developer-integrated kitchen offerings shift specification power from individual buyers to project merchandisers, which changes who decides materials, hardware, and appliance integration for entire towers. In Hanoi, 30,000 new apartments were launched in H1 2025, the highest half-year supply in five years, and this pipeline helps normalize turnkey kitchen suites as standard or optional upgrades in the mid to premium brackets[1]Source: “Hanoi Leads Nation in Apartment Price Growth,” VietnamPlus, en.vietnamplus.vn. Portfolio breadth underpins this model at scale, illustrated by Casta’s long-running focus on residential projects with extensive developer partnerships across the country. ALC Corp’s role in supplying large developers such as Vinhomes, Masterise Homes, and Gamuda Land further shows how project-based relationships embed kitchen specifications upstream in the construction cycle. Permit streamlining for projects with 1/500 planning approval shortens development timelines by three to six months and trims costs by 5%, allowing earlier commitments on bulk kitchen packages that secure volume visibility for manufacturers. Suppliers without sufficient throughput capacity and logistics coordination risk exclusion from tier-one towers as developers prioritize partners that can meet consistent monthly shipment schedules and installation milestones across multiple sites.

Expansion of Modern Retail & E-commerce Channels

Kitchen furniture has been showroom-led for years because buyers want to see fit, finish, and color under live lighting, yet omnichannel upgrades are reshaping the discovery and purchase journey. Hafele Vietnam’s roll-out of 33 new dealer locations in 2024, alongside comprehensive digital catalogs, signals a hybrid approach that keeps physical touchpoints while enabling remote consideration and post-visit configuration. Payments are less of a barrier than before, as 87.08% of adults hold bank accounts, which reduces friction for large-ticket online transactions that involve deposits and milestone-based invoicing for built-in cabinetry[2]Source: Ministry of Information and Communications, “Report on National Digital Transformation: July 2024,” MIC Vietnam, mic.gov.vn. An Cuong’s Creative Hub format expands access in tier-two cities by pairing physical product libraries with QR-linked e-catalogs, letting customers complete selections without traveling to Ho Chi Minh City. This omnichannel shift benefits modular cabinetry brands that can standardize finishes and modules for faster lead times, while still offering configurability that mirrors in-store advisory experiences. The Vietnam Kitchen Furniture Market, therefore, sees digital tools used to reduce indecision and accelerate order conversion, particularly in the Rest of Vietnam geographies, where independent showrooms historically dominated local demand.

Surge in Smart-Home Adoption

Smart-home adoption is reshaping expectations for kitchen fit-outs as buyers look for motion, sensors, and app-based controls that integrate with lighting, ventilation, and appliances. Kitchen-specific applications, IoT-enabled induction cooktops, sensor-activated faucets, and app-controlled cabinet lighting are moving beyond novelty to functional necessity as dual-income households seek time-saving automation. Apple and BYD's October 2024 announcement of a USD 413 million smart home device production facility in Phu Tho signals multinational confidence in local manufacturing ecosystems, which will likely reduce device costs and hasten integration with domestic furniture brands. Hoa Phat’s recent investment ramp in cooking appliances is one example of vertical expansion aligned with integrated kitchen packages, which are becoming more common in mid-range and premium projects. These trends are most visible in affluent urban districts and selecting coastal projects where buyer expectations for connected living are highest, and budgets can accommodate technology upgrades. As integration deepens, the Vietnam Kitchen Furniture Market favors suppliers that can pair cabinetry with reliable hardware and appliance partners to deliver cohesive smart-ready solutions in a single package.

Accelerated Demand for Green-Certified Materials

LOTUS, Vietnam’s green-building standard for new construction and interiors, places strict emphasis on low-VOC materials and lifecycle efficiency, which elevates the role of certified boards, adhesives, and finishes in kitchen projects. An Cuong’s portfolio includes GREENGUARD and Singapore Green Label certifications that can streamline material approvals on LOTUS-registered projects, which reduces testing overhead and accelerates submittals for project installers. FSC-certified forestry is expanding, with 520,000 hectares certified and a government target of one million hectares by 2030, which supports both export compliance and domestic green-building objectives for kitchen fit-outs. Rising alignment with international traceability regimes shapes procurement policies for large developers and hospitality chains that specify kitchen packages as part of broader sustainability goals. Vina Cabinetry’s long-standing emphasis on clean-air standards, including zero-VOC finishes and solvent-recycling processes, shows how sustainability credentials can differentiate suppliers in project tenders and premium retail.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in timber & input prices | -0.7% | Global, particularly affecting HCMC MA & Binh Duong production clusters reliant on imported timber. | Short term (≤ 2 years) |

| Fragmented supply chain & SME scale limits | -0.4% | Rest of Vietnam and tier-2 cities, where SME workshops dominate; minimal impact in HCMC/Hanoi project channels. | Medium term (2–4 years) |

| Competition from imported premium brands | -0.5% | HCMC MA & Hanoi high-rise developments; Central KER hospitality projects specifying European brands. | Medium term (2–4 years) |

| Skilled-labour shortages in cabinetry | -0.8% | Binh Duong & HCMC industrial zones; Rest of Vietnam struggling with retention amid electronics/textile sector competition. | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatility in Timber & Input Prices

Vietnam’s wood processing base relies heavily on imported materials, which exposes kitchen-furniture producers to exchange-rate swings and global commodity cycles that pass through to panel, veneer, and hardware costs. Integrated manufacturers can buffer these shocks through in-house production of boards and finishes, disciplined procurement, and long-term supplier contracts that smooth pricing across quarters. An Cuong reported a five-year high gross margin in 2024 while keeping volume growth conservative, which reflects a strategic focus on value engineering and controlled input exposure in a volatile materials environment. Smaller workshops that lack scale and working-capital buffers are more likely to absorb cost spikes or increase consumer prices, which can weaken competitiveness against fixed-price developer packages that are locked earlier in the construction cycle. Until forward purchasing and risk-sharing mechanisms become standard for SMEs, input volatility will remain a near-term drag on margins and investment appetite, particularly outside the largest production clusters.

Fragmented Supply Chain & SME Scale Limits

The Vietnam Kitchen Furniture Market includes hundreds of SMEs that operate with limited container throughput, constrained access to testing and certification, and uneven adoption of automation, which together limit their ability to meet large project timelines. Truong Thang’s 20,000-square-meter factory footprint is one example of the scale required to amortize investments in CNC and edge-banding lines that support consistent finishes across large orders[4]Source: Truong Thang Furniture, “Natural Wood Interiors,” Truong Thang, truongthang.vn. Casta’s production and logistics infrastructure demonstrates the throughput and coordination required for developer-bundled volume, including standardized models and shipment planning across many active projects. Industry bodies in Ho Chi Minh City and Binh Duong are working more closely to accelerate green and digital transitions, with targets for higher compliance with green standards by 2035, which could support pooled certification and shared service models over time. Foreign hardware brands are deepening local presence, with Hettich establishing a joint subsidiary in 2025 to localize supply and shorten lead times for drawer systems and fittings used in contemporary kitchens. Without policy levers that encourage technology transfer and cooperative procurement, however, scale disparities will continue to shape margins and segment positioning in the Vietnam Kitchen Furniture Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cabinets Anchor Share While Seating Accelerates

Kitchen Cabinets represent 46.11% of value in 2025, establishing the category as the largest product line anchored by both developer turnkey packages and retrofit projects, while Kitchen Chairs post the fastest growth at a 3.91% CAGR through 2031 in the Vietnam Kitchen Furniture Market. The Vietnam Kitchen Furniture market size for cabinets is reinforced by the emphasis on standardized modules that allow developers to scale installations across towers while maintaining finish consistency. In parallel, seating gains momentum as open plan living extends kitchen aesthetics into dining spaces, which boosts attachment rates for chairs and stools that match cabinet finishes and hardware tones. Tables benefit from compact extension mechanisms suited to apartment footprints where adaptable layouts matter for multi-use spaces that blend cooking, dining, and work zones. As catalogs widen, the Vietnam Kitchen Furniture Market rewards full-line suppliers that can raise order value by bundling seating and tables with cabinetry, lighting, and hardware in single, coordinated packages.

Cabinet growth continues to be volume-led by developer projects, but margin expansion depends on accessory and hardware attachment, where soft-close runners, organizers, and integrated lighting elevate price realization. Truong Thang’s use of sustainably sourced species and engineered woods in premium offerings supports durable finishes and aesthetic variety for upmarket buyers who want natural textures balanced with modern geometry. Hardware and appliance linkages create upsell pathways, as seen in Hafele’s dishwashers and sink-faucet lines that complement cabinet layouts and drive packaged sales. Chairs and other movable items allow quicker refresh cycles compared with built-ins, which helps brands maintain engagement with past buyers and address wear-and-tear replacements over shorter intervals. The Vietnam Kitchen Furniture industry also benefits from design convergence where finish palettes and hardware tones align across cabinets, seating, and tables, creating consistent visual stories that enhance perceived value in showroom and online experiences.

By Material: Wood Dominance Meets Metal Innovation

Wood holds 71.42% share in 2025, while Metal is the fastest-growing material at a 4.17% CAGR through 2031, as stainless-steel Inox 304 systems gain traction for durability and hygiene in humid kitchens within the Vietnam Kitchen Furniture Market. The Vietnam Kitchen Furniture market size dynamics reflect the balance of wood’s broad appeal and the niche but rising adoption of metal for commercial-grade and coastal applications, where corrosion resistance is a priority. FSC-certified supply supports wood’s incumbency in both export-facing and domestic projects, as developers and hospitality chains require documented traceability and low emissions in interior fit-outs. LOTUS green-building requirements keep low-VOC materials front and center for interior credits, which shape adhesive and surface selection in kitchen environments. The Vietnam Kitchen Furniture Market, therefore, sees a two-track material story, with engineered wood broadening style and price points while metal lines carve out growth in moisture-heavy or commercial applications.

Material innovation is a core differentiator as suppliers expand codes in melamine-faced chipboard, laminates, acrylics, and 3D surfaces to deliver premium looks with predictable performance. An Cuong’s expanding catalog shows how engineered solutions can reduce solid-timber dependency while meeting design briefs that demand realistic textures and durable finishes for heavy-use kitchens. Metal adoption rides on rising hygiene awareness and the desire for easy-to-clean surfaces, especially in coastal provinces and hospitality venues that emphasize maintenance efficiency. Plastic and polymer options fill entry-level price points and align with low-VOC requirements in budget-sensitive towers, where project specifications prioritize compliance and lifespan over bespoke finishes. As compliance frameworks converge, the Vietnam Kitchen Furniture Market sees certified materials and documented processes become prerequisites for large project bids and high-visibility commercial installations.

By End-User: Residential Stability Versus Commercial Momentum

The Residential segment accounts for 71.82% in 2025 as urbanization, condominium launches, and turnkey interior packages sustain steady demand within the Vietnam Kitchen Furniture Market. The Commercial segment is the fastest-growing at a 4.76% CAGR through 2031 as hotels, restaurants, and managed apartments upgrade or expand their kitchen infrastructure to serve renewed travel and food-service flows. Residential demand is concentrated in high-rise developments where developers specify standardized kitchens to enhance pre-sales and deliver move-in-ready units that reduce post-handover fit-out delays for buyers. At the same time, retrofit opportunities persist in premium segments where buyers commission custom finishes, imported hardware, and unique layouts that require specialized workshops and longer installation windows.

Commercial demand benefits from the hospitality rebound and the continued build-out of F&B ecosystems in fast-growing corridors, supported by specifications that emphasize stainless steel, ventilation integration, and heavy-duty hardware. The Central Key Economic Region, with Da Nang at its core, illustrates how resort pipelines and serviced apartments pull through commercial-grade kitchen packages while also shaping adjacent retail demand for vacation homes and rentals. Export-oriented producers that specialize in ready-to-assemble cabinets with container-based minimums demonstrate how standardized manufacturing can serve both international channels and local projects that favor consistent quality. In denser urban settings, residential buyers are more likely to take advantage of showroom networks and omnichannel advisory services to select materials that fit budget and sustainability preferences. As these end-user dynamics evolve, the Vietnam Kitchen Furniture industry prioritizes capacity planning and differentiated catalogs to meet the distinct needs of residential scale and commercial durability.

By Distribution Channel: Project Volume Gains on Retail Maturity

B2C/Retail channels represent 70.41% of value in 2025, reflecting long-established showroom habits and a dense ecosystem of dealers, while B2B/Project is growing faster at a 4.28% CAGR through 2031 as developers bundle kitchens to standardize fit-outs at scale in the Vietnam Kitchen Furniture Market. Retail remains the most diverse route with home centers, specialty stores, and brand-led showrooms, supported by digital catalogs and virtual advisory tools that convert research into orders even in tier-two cities. High banking penetration reduces payment friction for online purchases, which helps larger retailers and brands deploy e-commerce and hybrid models for big-ticket items. An Cuong’s investment in Creative Hubs underscores how brands bring material libraries closer to customers while maintaining centralized production and delivery scheduling. The Vietnam Kitchen Furniture Market therefore sustains a balanced channel mix, with retail delivering breadth and projects consolidating depth.

Project channels concentrate influence among manufacturers that can meet consistent monthly shipping plans, align with developer design guidelines, and coordinate on-site installation across multiple towers. Casta’s large project portfolio highlights these capabilities and provides a path to recurring volume with national developers. Relationships with leading developers such as Vinhomes, Masterise Homes, and Gamuda Land also demonstrate the strategic importance of exclusive or preferred partnerships that secure early specification lock-ins. Permit simplification for projects with 1/500 planning approval reduces overall project durations and supports earlier procurement milestones, which favors organized suppliers that can commit to volume and lead times with fewer contingencies. As project pipelines spread into new corridors, the Vietnam Kitchen Furniture Market will see more regional distributors align with developer networks while retail continues to serve bespoke buyers and post-handover upgrades.

Geography Analysis

Ho Chi Minh City Metropolitan Area holds 36.56% share in 2025, reflecting a combination of scale in residential launches and proximity to production clusters that enable shorter lead times and efficient installation schedules in the Vietnam Kitchen Furniture Market. Local presence of leading kitchen and interior suppliers strengthens logistics and service coverage for large project developers in this region, which supports the growth of B2B/Project channels and consistent product standards. As land scarcity lifts average prices in core districts, developers increasingly rely on turnkey kitchens as value enhancements that support faster sales and more predictable handovers. Streamlined procedures for construction approvals aim to reduce delays and lower costs, reinforcing early procurement and specification cycles for interior packages, including kitchens. Compliance and sustainability considerations influence material choices, with documented low-VOC finishes and traceable wood supply becoming baseline requirements for large developments.

The Central Key Economic Region, anchored by Da Nang, records the fastest growth at a 3.83% CAGR through 2031, supported by hospitality recovery and mixed-use projects that specify commercial-grade kitchens for hotels and serviced apartments within the Vietnam Kitchen Furniture Market. Coastal exposure and humid conditions favor metal systems in select applications, while premium residential projects blend engineered wood with higher-spec hardware and integrated lighting for aesthetic and functional balance. Permit reforms that shorten project cycles enable earlier lock-ins for kitchen packages, which support better factory scheduling and inventory planning for regional distributors. As resort and convention pipelines expand, the pull-through of kitchen installations extends to adjacent retail and rental markets that benefit from standardized components and reliable after-sales service. Compliance with green-building frameworks, particularly LOTUS, continues to shape material and adhesive choices in both residential and commercial kitchens, reinforcing demand for certified inputs.

Hanoi & Red River Delta delivered 30,000 new apartments in H1 2025, the highest half-year supply in five years, but kitchen-furniture uptake is affected by the prevalence of bare-shell units at the top end, where buyers often commission bespoke interiors post-handover in the Vietnam Kitchen Furniture Market. This creates a split where project channels focus on mid-tier turnkey volumes while high-income buyers pursue custom designs through specialty retailers and workshops. The climate profile supports wood’s dominance in material choices, with fewer stainless-steel-heavy specifications compared to southern provinces, where humidity and coastal conditions encourage metal adoption in select zones. The rest of Vietnam, including cities such as Can Tho and Hai Phong, presents white space for modular cabinetry as brands invest in showrooms and distributor partnerships to standardize quality in markets long served by local carpenters. High banking penetration reduces thresholds for e-commerce and hybrid purchases in these cities, which supports wider adoption of catalog-driven modules and remote advisory workflows that suit distributed demand.

Regulatory Landscape

Vietnam kitchen furniture compliance is shaped by the Law on Standards and Technical Regulations (2006, amended by Law No. 70/2025/QH15), which takes effect on January 1, 2026 and reinforces the framework where national standards (TCVN) are generally voluntary while technical regulations (QCVN) are mandatory. For product performance and safety alignment, TCVN 5373:2020 sets technical requirements for indoor wooden furniture, while TCVN 5372:2023 provides test methods for appearance and physical-mechanical properties used in quality verification.

On market surveillance, Circular No. 01/2024/TT-BKHCN (effective March 3, 2024) strengthens state inspection of quality for goods circulating on the market, which raises the value of documented quality control for cabinets and other high-value kitchen items sold via retail and project channels. Imports and trading compliance also center on customs procedures and labeling rules (notably Decree No. 43/2017/NĐ-CP on goods labeling), affecting finished kitchen furniture as well as key inputs such as panels, hardware, and fittings moving through distributor networks.

Value Chain Analysis

The value chain starts with timber and engineered wood panels (plus adhesives, laminates, and finishes), supported by Vietnam’s legality framework for timber sourcing through the Vietnam Timber Legality Assurance System (VNTLAS) under Decree 102/ND-CP, and extends to metal hardware systems that increasingly localize supply to shorten lead times. Manufacturing is concentrated in southern industrial clusters such as Binh Duong and Dong Nai, where producers combine CNC-based cutting, edge-banding, and finishing with more labor-intensive custom work for premium projects. Scale advantages help suppliers meet developer-bundled tower schedules that depend on consistent monthly deliveries and coordinated installation.

Downstream, distribution splits between (i) B2B/project routes where developers and project distributors specify standardized kitchen packages early in the construction cycle, and (ii) B2C/retail networks of showrooms, dealers, and online catalogs that drive upgrades and post-handover customization. Logistics and throughput are anchored by proximity to major gateways including Cat Lai and Cai Mep, supporting both domestic replenishment and export-linked production runs that share capacity with local kitchen cabinet lines. Industry associations such as HAWA, Viforest, BIFA, and DOWA coordinate capability building and compliance readiness, while recurring bottlenecks for smaller workshops center on certification access, skilled cabinetry labor, and working-capital demands tied to large project orders.

Competitive Landscape

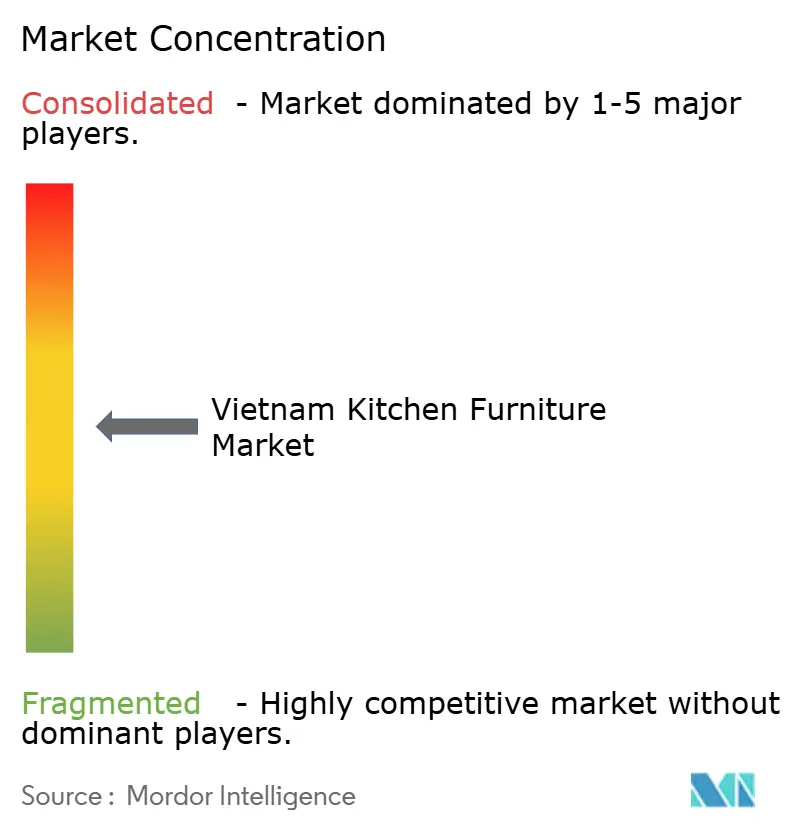

The Vietnam Kitchen Furniture Market shows moderate concentration, with the top five suppliers accounting for about 52% of the 2025 value, leaving significant scope for regional and specialist players to compete for the remaining share. Competitive positioning follows channel lines, where developer-aligned incumbents emphasize early specification lock-ins and project servicing capabilities, and export-leaning firms optimize for container-level throughput and certification compliance. An Cuong’s 2024 performance illustrates margin defense through value engineering and integrated material production, with profitability at a multi-year high even as revenue growth remained measured in a volatile input environment. Component leaders such as Hettich and Hafele focus on hardware and appliance ecosystems, partnering with local cabinet makers to embed higher-spec fittings that command price premiums while elevating user experience in drawers, hinges, and integrated lighting. The Vietnam Kitchen Furniture Market, therefore, rewards suppliers that can match developer timelines, maintain consistent quality at scale, and differentiate through sustainable materials and hardware integration.

White-space opportunities are most visible in tier-two urban centers where modular cabinetry penetration is still being built, and local workshops have limited capacity to meet green standards and test requirements for large projects. Industry associations in Ho Chi Minh City and Binh Duong are pushing for greener and more digital operations with future targets that encourage broader compliance across producers, which could shift procurement toward certified suppliers as those targets approach. Larger OEMs and international brands invest in automated lines and logistics that reduce lead times and enable reliable product flows for both project and retail channels, which smaller firms struggle to replicate. Hardware joint ventures also gain traction as global firms localize production to simplify distribution and tailor systems to Vietnamese dimensions and design preferences. As capabilities shift, the Vietnam Kitchen Furniture Market will continue to see channel consolidation around suppliers with integrated catalogs and service coverage that extends from specification to installation and after-sales support.

Long-term collaboration with leading developers anchors share for incumbents that provide proven throughput and standardized installation protocols across multi-phase projects. Casta’s project portfolio and alignment with major developers highlight how supplier-developer collaboration transforms into recurring volume that smooths factory utilization and procurement. ALC Corp’s partnerships in high-profile residential projects demonstrate the strategic value of co-developing specifications and ensuring on-site coordination that keeps interior schedules on track. Retail-led expansion by materials and finished goods brands continues in parallel, as seen in An Cuong’s Creative Hubs that bring catalogs closer to customer clusters beyond the largest cities. As hardware leaders deepen their Vietnam presence and local manufacturers broaden certified offerings, competitive differentiation will center on material traceability, VOC compliance, and the ability to deliver coherent, smart-ready kitchen packages at scale.

Vietnam Kitchen Furniture Industry Leaders

Vibuma

Pacific Craftworks

Ikea

Ixina

Star Marine Furniture Company Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Mid-tier modular cabinetry expansion in tier-2 cities remains a clear whitespace, supported by omnichannel formats that reduce the need for full-scale flagship showrooms while still enabling configuration-driven sales. This is reinforced by supplier moves that combine physical touchpoints with digital selection tools (for example, dealer-network rollouts and QR-linked e-catalog approaches referenced across the market), which support standardized finishes, shorter lead times, and higher buyer confidence for built-in orders outside Ho Chi Minh City and Hanoi.

A second opportunity is in higher-compliance and higher-spec projects that require traceability and low-emission materials, where LOTUS-aligned interior specifications and broader standards enforcement raise the bar for certified boards, finishes, and documented processes during bid evaluation. Industry-wide capability building is also becoming more visible through platforms and associations: in March 2026, HAWA taking chairmanship of the ASEAN Furniture Industries Council (2026-2027 term) and the scale of HawaExpo 2026 (700 exhibitors in a single-venue strategy) point to stronger regional market access and more productization momentum for Vietnam-based manufacturers and suppliers. On the component side, localization of hardware supply and smart-home-ready fittings expand the bundling options for cabinet makers selling into developer turnkey packages, particularly where installation and after-sales service coverage matter for project buyers.

Recent Industry Developments

- June 2026: Pacific Craftworks published updated manufacturing and process documentation highlighting in-house lumber kilning and integrated production at its Binh Duong facility. The disclosure signals continued focus on controllable wood stability and finish consistency, which supports premium custom cabinetry specifications for high-end residential and hospitality kitchens.

- January 2026: Hettich opened its first joint subsidiary in Vietnam with FGV to establish local manufacturing and distribution for kitchen hardware systems, including drawer systems and fittings. Localized supply shortens lead times for cabinet makers and installers, supporting the delivery of developer-bundled kitchen packages on fixed site schedules.

- June 2025: Woodsland JSC obtained a Factory Production Control Conformity Certificate for plywood products, reinforcing CE-mark-aligned compliance for certified panel supply. This expands access to documented, standard-compliant inputs used in kitchen cabinets where developers and commercial buyers increasingly require traceability and consistent performance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers kitchen-focused furniture and built-in units sold in Vietnam for residential and commercial kitchens, measured as revenue at current prices. It includes items used for storage, preparation, and dining within the kitchen space.

Scope exclusions: We exclude loose home decor, standalone major appliances, and installation labor that is billed separately from the furniture invoice.

Segmentation Overview

- By Product

- Kitchen Cabinets

- Kitchen Chairs

- Kitchen Tables

- Other Products (Trolley, Cart, Pantry Shelves)

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By End-User

- Residential

- Commercial

- By Distribution Channel

- B2C / Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B / Project

- B2C / Retail

- By Geography

- Ho Chi Minh City Metropolitan Area

- Hanoi & Red River Delta

- Central Key Economic Region (Da Nang & environs)

- Rest of Vietnam

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public signals that explain furniture demand in Vietnam, and then we mapped those signals to kitchen-specific consumption. We used sources such as the General Statistics Office of Vietnam for housing completions and household spending context, and customs trade statistics for furniture-related import and export flows that impact local supply and pricing.

To keep the model grounded, we also reviewed sources such as the World Bank for macro indicators tied to renovation and home purchases, and UN Comtrade for cross-checking trade category movements where relevant. This was supplemented with company filings and investor presentations for revenue mix clues, along with association and reputed press updates on retail expansion, e-commerce penetration, and construction project pipelines. We also referenced paid subscriptions for company financials and news intelligence, and for patent databases when product shifts (materials, modular designs) needed validation. The desk sources listed here are illustrative, and many other public and paid references were used to collect, verify, and clarify data points.

Primary Interviews and Surveys

Primary interviews and surveys were used to check what is actually being sold, at what price points, and through which channels, before we locked the market totals. We spoke with respondents across Vietnam, including retail channel operators, project-focused sellers, distributors, and manufacturing-side experts. Their input was then used to confirm mix splits, demand triggers, and realistic price movement assumptions for the Vietnam kitchen furniture value pool.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | |

| Mid tier: 52% | Functional/Unit leaders: 36% | |

| Smaller Players: 20% | Managers: 50% |

Market-Sizing & Forecasting

Sizing was built from the demand pool first, where housing additions and renovation activity in Vietnam are translated into kitchen fitting and replacement needs, and then expressed as value using category-level pricing. We stated the top-down approach once in this way because housing turnover and kitchen refit cycles are the most consistent anchors for kitchen furniture demand in this country.

The model uses a mix of practical inputs, such as new apartment handovers, residential renovation intensity, typical kitchen cabinet and dining set attachment rates, channel mix shifts between project supply and retail, and average selling price movement by material and finish level. To keep totals realistic, the result is corroborated with selective bottom-up approximations, including supplier and retailer roll-ups from interviews, sampled price lists that were normalized, and simple volume checks against production and trade direction.

For forecasting, we used scenario analysis supported by expert inputs, where a base case is framed around construction pipeline expectations and household spending direction, and then adjusted for slower or faster renovation cycles. When a bottom-up datapoint was missing for a city or channel, the gap was handled by applying validated mix ratios from similar urban clusters, followed by a re-check with field respondents so we did not over-extend any single assumption.

Data Validation & Update Cycle

Validation is done in steps so the final value is not driven by one dataset or one interview set. We compare modeled demand and pricing outputs with independent signals like construction completions, trade direction, and retailer expansion observations, and then anomalies are reviewed until the variance has a clear reason.

Before sign-off, the work goes through multi-step analyst reviews that include assumption testing, year-over-year trend sanity checks, and a final reconciliation of key ratios that affect value, such as attachment rates and price progression. Reports refresh annually, and interim updates are triggered when material events occur, such as sharp shifts in housing starts, policy changes affecting real estate timelines, or sudden input-cost moves. Right before delivery, a fresh analyst pass is done so clients receive the latest updated view available at that time.

Mordor Intelligence's Vietnam Kitchen Furniture Market Size Measured Against Other Published Estimates

Published market values for Vietnam kitchen furniture can look far apart because the boundary of what counts as kitchen furniture is not always the same, and the demand anchors also vary by publisher. Differences often come from how project sales are treated versus retail-only views, and from whether items like countertops and sinks are counted within the furniture total.

Housing handover trends, channel checks on project-led procurement, and normalized price observations are the signals that link Mordor Intelligence's estimate to a repeatable demand pool rather than a broad furniture spend proxy. Once those checks are applied, the remaining spread usually comes down to what is counted as kitchen furniture, how ASPs are moved forward year to year, and how recently the assumptions were refreshed in local currency terms.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 339.64 M (2026) | |

| Trade Journal A | USD 191.78 M (2025) | Uses a narrower kitchen scope centered on cabinets and related components, and the earlier base year can understate current channel expansion and price progression if not revalidated with local sellers. |

| Industry Publication B | USD 359.44 M (2030) | Reports a forward-year number without clear product inclusions, and the CAGR-led projection can drift if housing pipeline and renovation-cycle assumptions are not reconciled with on-ground channel mix and realistic ASP movement. |

The comparison shows that timing and scope are the two practical levers behind most gaps, followed by how prices are carried through the forecast. By keeping the market tied to housing and renovation signals, and by checking channel behavior and price bands directly, the final estimate stays easier to trace back to real-world drivers and to reproduce on an annual refresh cadence.

Key Questions Answered in the Report

What is the current size and growth outlook for the Vietnam Kitchen Furniture Market?

The Vietnam Kitchen Furniture market size is USD 339.64 million in 2026 and is projected to reach USD 401.30 million by 2031 at a 3.39% CAGR, reflecting steady expansion driven by developer bundling and retail omnichannel upgrades.

Which product categories lead and which are growing fastest in the Vietnam Kitchen Furniture Market?

Kitchen Cabinets lead with 46.11% of value in 2025, while Kitchen Chairs record the fastest growth at a 3.91% CAGR through 2031, supported by open-plan living layouts and coordinated seating demand.

How are channels shifting in the Vietnam Kitchen Furniture Market?

B2C/Retail accounts for 70.41% of value in 2025, but B2B/Project expands faster at a 4.28% CAGR as developers specify turnkey kitchens early in project cycles to support pre-sales and standardized installations.

Which regions are most important for demand in the Vietnam Kitchen Furniture Market?

Ho Chi Minh City Metropolitan Area holds a 36.56% share in 2025 due to scale and developer ecosystems, while the Central Key Economic Region is the fastest growing at a 3.83% CAGR on hospitality and mixed-use pipelines.

What materials are shaping specifications in the Vietnam Kitchen Furniture Market?

Wood leads at 71.42% share due to aesthetics and certified supply, while Metal grows fastest at a 4.17% CAGR as stainless systems gain traction for hygiene and durability, supported by green-building requirements and traceability needs.

Page last updated on: