Market Size of Vietnam Diabetes Care Drugs Industry

| Study Period | 2018 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

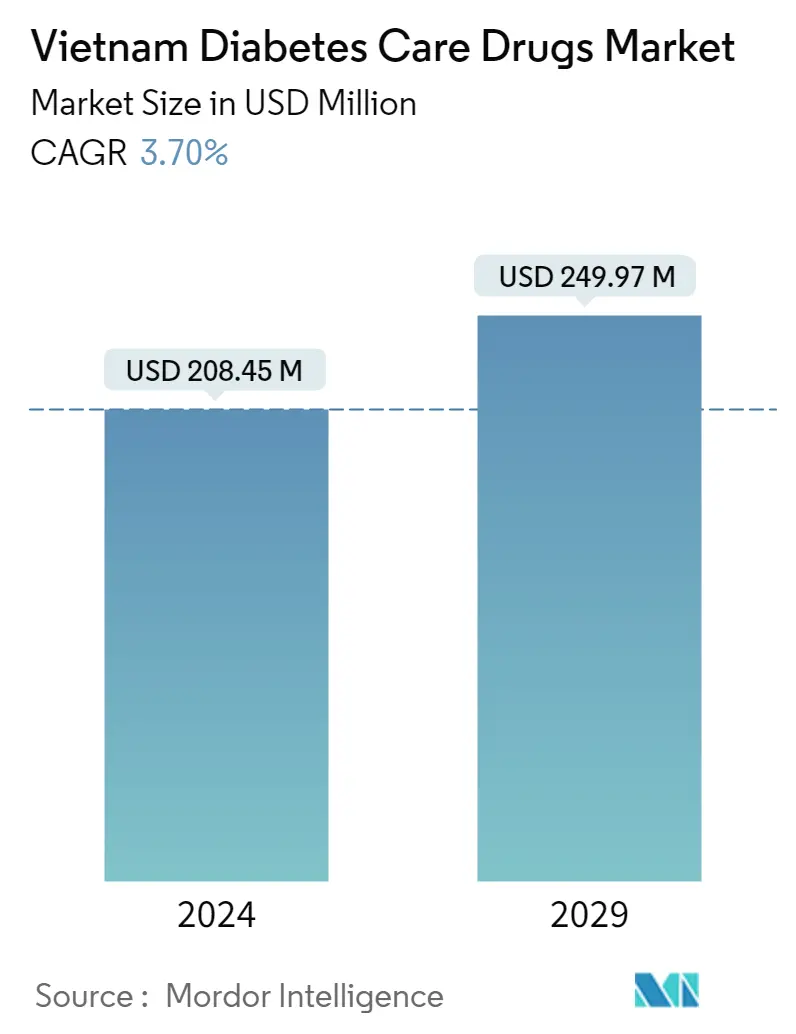

| Market Size (2024) | USD 208.45 Million |

| Market Size (2029) | USD 249.97 Million |

| CAGR (2024 - 2029) | 3.70 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Vietnam Diabetes Care Drugs Market Analysis

The Vietnam Diabetes Care Drugs Market size is estimated at USD 208.45 million in 2024, and is expected to reach USD 249.97 million by 2029, growing at a CAGR of 3.70% during the forecast period (2024-2029).

Vietnam has effectively stopped transmission of the COVID-19 outbreak since the outset, with no deaths for months. Since then, however, the fourth wave of the COVID-19 outbreak has wreaked devastation on Vietnam. According to the Ministry of Health, Vietnam has seen four waves of the COVID-19 epidemic (MOH).

COVID-19 (coronavirus disease) has been found as a highly infectious viral infection caused by coronavirus-2 that produces severe acute respiratory syndrome (SARS-CoV-2). Diabetes is a major risk factor for fatal COVID-19 outcomes. Diabetes patients are vulnerable to infection due to hyperglycemia, impaired immune function, vascular issues, and comorbidities such as hypertension, dyslipidemia, and cardiovascular disease. Furthermore, angiotensin-converting enzyme 2 (ACE2) is a SARS-CoV-2 receptor in humans. As a result, angiotensin-converting enzyme (ACE) inhibitors must be used with caution in diabetic individuals. COVID-19 severity and mortality were significantly higher in diabetics than in non-diabetics. As a result, diabetics should exercise caution during the COVID-19 epidemic.

COVID-19 (coronavirus disease) has been found as a highly infectious viral infection caused by coronavirus-2 that produces severe acute respiratory syndrome (SARS-CoV-2). Diabetes is a major risk factor for fatal COVID-19 outcomes. Diabetes patients are vulnerable to infection due to hyperglycemia, impaired immune function, vascular issues, and comorbidities such as hypertension, dyslipidemia, and cardiovascular disease. Furthermore, angiotensin-converting enzyme 2 (ACE2) is a SARS-CoV-2 receptor in humans. As a result, angiotensin-converting enzyme (ACE) inhibitors must be used with caution in diabetic individuals. COVID-19 severity and mortality were significantly higher in diabetics than in non-diabetics. As a result, diabetics should exercise caution during the COVID-19 epidemic.

In terms of medicines, the insulin category commands a sizable market share. Over 100 million people worldwide use insulin, including all persons with Type 1 diabetes and 10% to 25% of people with Type 2 diabetes. Insulin production is extremely sophisticated, and there are only a few insulin manufacturers on the market. As a result, there is fierce rivalry among these producers, who are continually striving to satisfy the demands of patients by providing the highest-quality insulin.

Vietnam Diabetes Care Drugs Industry Segmentation

Diabetes, or diabetes mellitus, describes a group of metabolic disorders characterized by a high blood sugar level in a person. With diabetes, the body either does not produce enough insulin or the body's cells do not respond properly to insulin, or both. The Vietnam diabetes care drugs market is segmented by drugs into insulin (basal or long-acting, bolus or fast-acting, traditional human insulin drugs, and insulin biosimilars), oral anti-diabetic drugs (alpha-glucosidase inhibitors, DPP-4 inhibitors, and SGLT-2 inhibitors), non-insulin injectable drugs (GLP-1 receptor antagonists, and Amylin analogs), and combination drugs (combined insulin, oral combination). The report offers the value (in USD million) and volume (in unit million) for the above segments.

| Oral Anti-diabetic Drugs | ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

|

| Insulin Drugs | |||||||

| |||||||

| |||||||

| |||||||

|

| Combination Drugs | |||||

| |||||

|

| Non-Insulin Injectable Drugs | |||||||

| |||||||

|

Vietnam Diabetes Care Drugs Market Size Summary

The Vietnam diabetes care drugs market is poised for growth, driven by an increasing prevalence of diabetes and the demand for effective treatment options. The market is characterized by a significant share of insulin products, which are essential for managing Type 1 diabetes and a portion of Type 2 diabetes cases. The complexity of insulin production and the limited number of manufacturers contribute to intense competition among key players, who are continually innovating to meet patient needs. Additionally, the oral anti-diabetic drugs segment is expected to expand, reflecting the growing diabetes population in the country. Despite the challenges posed by limited health insurance coverage and the high cost of diabetes treatment, efforts are underway to enhance access to affordable medications, particularly in urban areas where diabetes prevalence is rising.

Vietnam's healthcare landscape is evolving, with the government aiming to achieve universal health insurance coverage and decentralizing health management to improve efficiency. The diabetes burden is recognized as a public health challenge, prompting public health officials to implement strategies to mitigate its impact. Economic growth and lifestyle changes have contributed to the rising incidence of diabetes, making it a leading cause of death and disability in the country. The market is moderately fragmented, with major players like Novo Nordisk, Sanofi, and AstraZeneca dominating the insulin and SGLT-2 segments, while generic players are more prevalent in the oral drug market. Recent partnerships and technological transfers aim to boost local drug production, enhancing patient access to essential medications.

Vietnam Diabetes Care Drugs Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining Power of Consumers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products and Services

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Oral Anti-diabetic Drugs

-

2.1.1 Biguanides

-

2.1.1.1 Metformin

-

-

2.1.2 Alpha-Glucosidase Inhibitors

-

2.1.2.1 Alpha-Glucosidase Inhibitors

-

-

2.1.3 Dopamine D2 receptor agonist

-

2.1.3.1 Bromocriptin

-

-

2.1.4 SGLT-2 inhibitors

-

2.1.4.1 Invokana (Canagliflozin)

-

2.1.4.2 Jardiance (Empagliflozin)

-

2.1.4.3 Farxiga/Forxiga (Dapagliflozin)

-

2.1.4.4 Suglat (Ipragliflozin)

-

-

2.1.5 DPP-4 inhibitors

-

2.1.5.1 Onglyza (Saxagliptin)

-

2.1.5.2 Tradjenta (Linagliptin)

-

2.1.5.3 Vipidia/Nesina(Alogliptin)

-

2.1.5.4 Galvus (Vildagliptin)

-

-

2.1.6 Sulfonylureas

-

2.1.6.1 Sulfonylureas

-

-

2.1.7 Meglitinides

-

2.1.7.1 Meglitinides

-

-

-

2.2 Insulin Drugs

-

2.2.1 Basal or Long Acting Insulins

-

2.2.1.1 Lantus (Insulin Glargine)

-

2.2.1.2 Levemir (Insulin Detemir)

-

2.2.1.3 Toujeo (Insulin Glargine)

-

2.2.1.4 Tresiba (Insulin Degludec)

-

2.2.1.5 Basaglar (Insulin Glargine)

-

-

2.2.2 Bolus or Fast Acting Insulins

-

2.2.2.1 NovoRapid/Novolog (Insulin Aspart)

-

2.2.2.2 Humalog (Insulin Lispro)

-

2.2.2.3 Apidra (Insulin Glulisine)

-

-

2.2.3 Traditional Human Insulins

-

2.2.3.1 Novolin/Actrapid/Insulatard

-

2.2.3.2 Humulin

-

2.2.3.3 Insuman

-

-

2.2.4 Biosimilar Insulins

-

2.2.4.1 Insulin Glargine Biosimilars

-

2.2.4.2 Human Insulin Biosimilars

-

-

-

2.3 Combination Drugs

-

2.3.1 Insulin combinations

-

2.3.1.1 NovoMix (Biphasic Insulin Aspart)

-

2.3.1.2 Ryzodeg (Insulin Degludec and Insulin Aspart)

-

2.3.1.3 Xultophy (Insulin Degludec and Liraglutide)

-

-

2.3.2 Oral Combinations

-

2.3.2.1 Janumet (Sitagliptin and Metformin)

-

-

-

2.4 Non-Insulin Injectable Drugs

-

2.4.1 GLP-1 receptor agonists

-

2.4.1.1 Victoza (Liraglutide)

-

2.4.1.2 Byetta (Exenatide)

-

2.4.1.3 Bydureon (Exenatide)

-

2.4.1.4 Trulicity (Dulaglutide)

-

2.4.1.5 Lyxumia (Lixisenatide)

-

-

2.4.2 Amylin Analogue

-

2.4.2.1 Symlin (Pramlintide)

-

-

-

Vietnam Diabetes Care Drugs Market Size FAQs

How big is the Vietnam Diabetes Care Drugs Market?

The Vietnam Diabetes Care Drugs Market size is expected to reach USD 208.45 million in 2024 and grow at a CAGR of 3.70% to reach USD 249.97 million by 2029.

What is the current Vietnam Diabetes Care Drugs Market size?

In 2024, the Vietnam Diabetes Care Drugs Market size is expected to reach USD 208.45 million.