Video-on-Demand Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

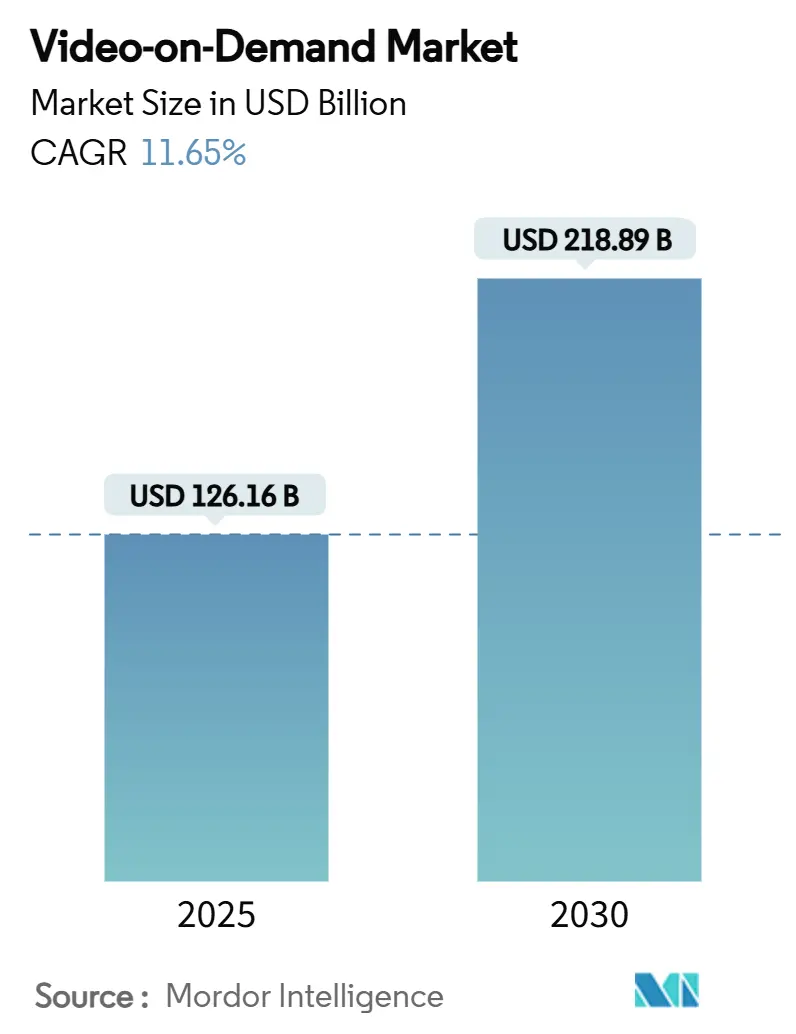

| Market Size (2025) | USD 126.16 Billion |

| Market Size (2030) | USD 218.89 Billion |

| Growth Rate (2025 - 2030) | 11.65% CAGR |

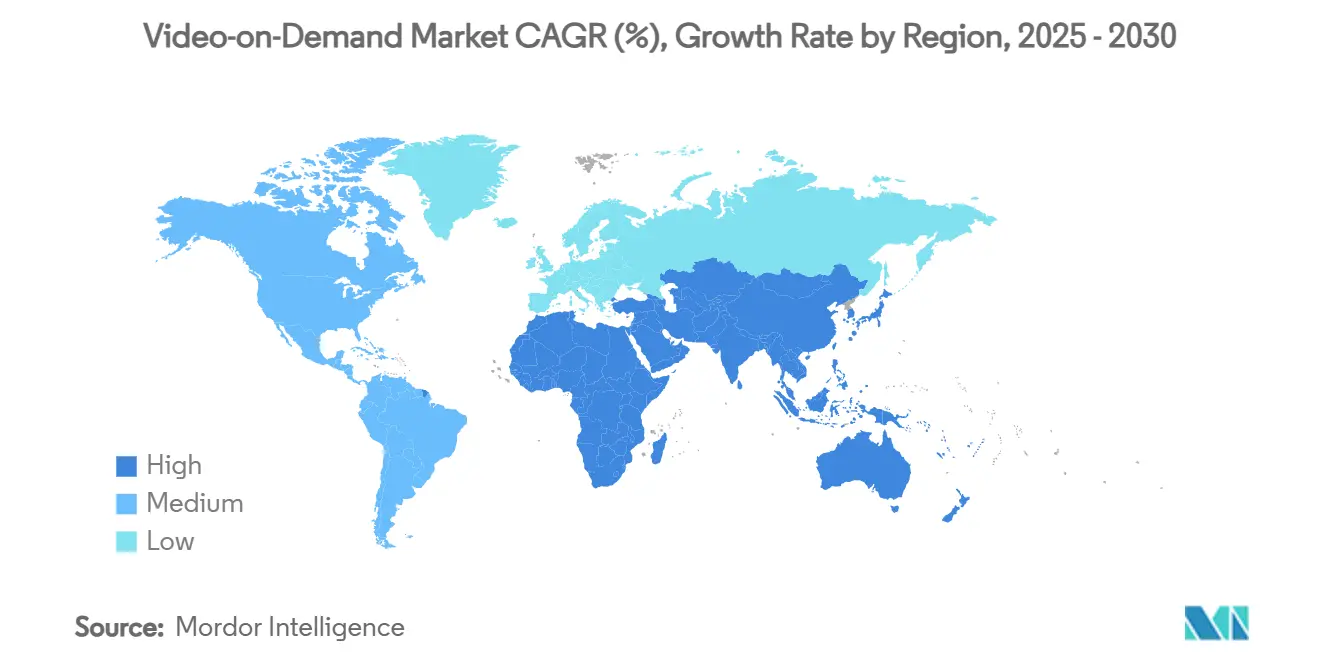

| Fastest Growing Market | Asia |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Video-on-Demand Market Analysis by Mordor Intelligence

The Video-on-Demand market size is estimated at USD 126.16 billion in 2025 and is forecast to reach USD 218.89 billion by 2030, advancing at an 11.65% CAGR over 2025-2030. This acceleration mirrors the steady shift from scheduled television to on-demand streaming, supported by rapid broadband rollouts, device proliferation, and richer content libraries. Ultra-high-speed fiber and 5G coverage in North America and Western Europe enable smooth 4K playback, while local-language production budgets in Asia keep regional viewers engaged. The surge of ad-supported tiers offers price-sensitive households alternative entry points, and telecom bundles are lowering acquisition costs in Latin America. The competitive intensity remains high as market leaders hedge churn risk through content exclusivity, cross-service bundles, and cost-efficient delivery networks.

Key Report Takeaways

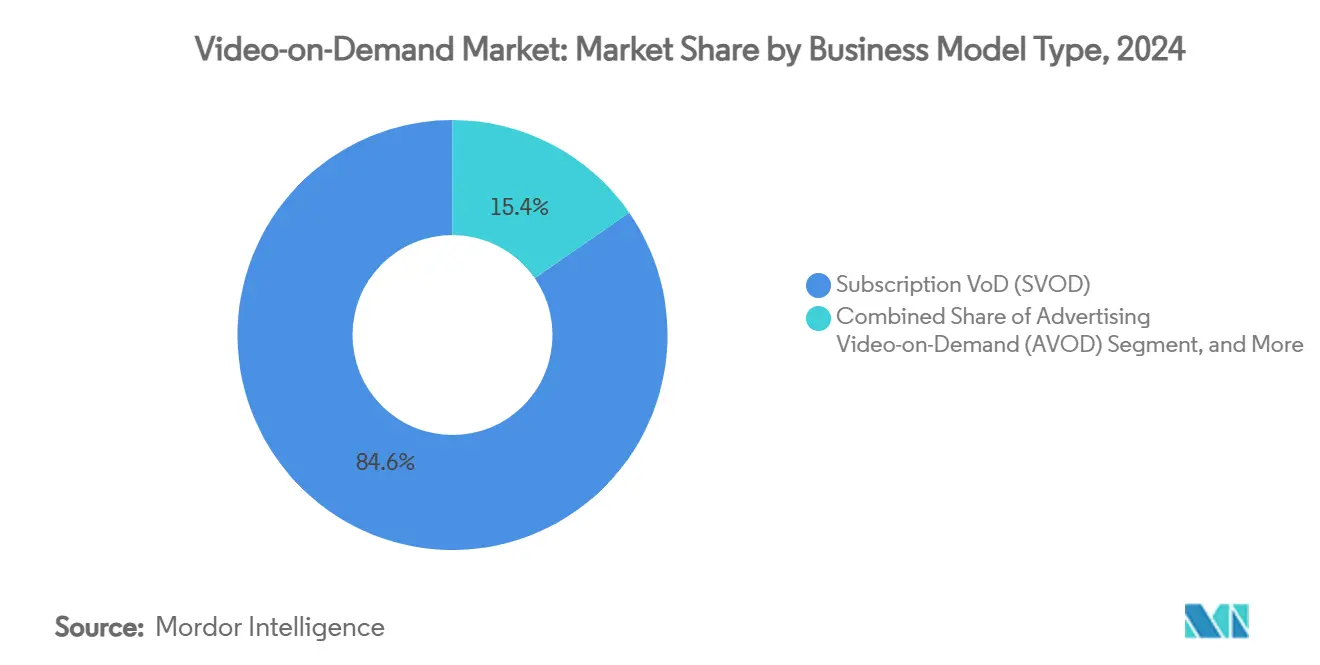

- By business model, the SVOD segment held 84.63% of the Video-on-Demand market share in 2024, whereas AVOD is set to expand at an 11.12% CAGR to 2030.

- By delivery technology, OTT streaming captured 72% of the Video-on-Demand market size in 2024 and is projected to grow at 11.3% CAGR through 2030.

- By device type, smartphones and tablets led with 43% revenue share in 2024; smart TVs are poised for the fastest growth at 15.1% CAGR to 2030.

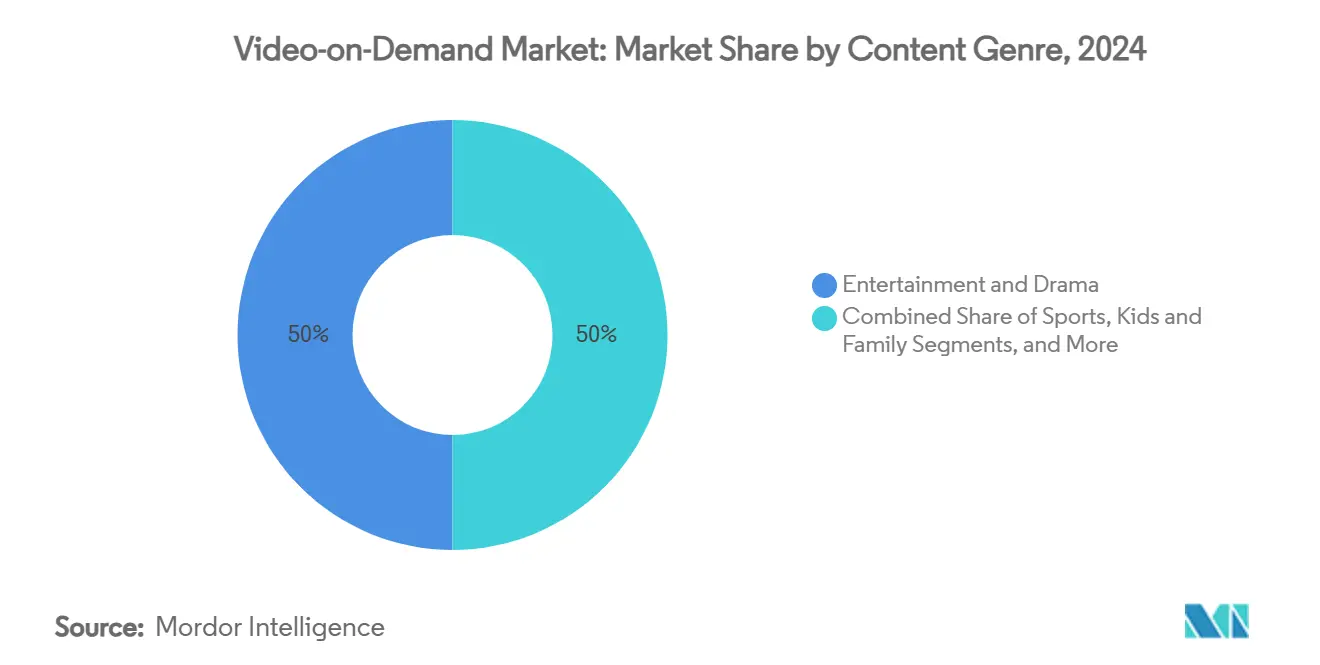

- By content genre, entertainment and drama retained a 50% share of the Video-on-Demand market size in 2024, while sports is advancing at a 14% CAGR through 2030.

- By end-user, residential subscribers took 82% of the Video-on-Demand market share in 2024, whereas the commercial segment is accelerating at 16% CAGR over 2025-2030.

- By Geogrpahy, North America retained 41.65% revenue share in 2024, while Asia-Pacific posts the fastest 12.2% CAGR through 2030

Global Video-on-Demand Market Trends and Insights

Drivers Impact Analysis

| Driver | (∼) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid AVOD uptake among price-sensitive households | +2.0% | Asia-Pacific, Latin America | Medium term (2-4 years) |

| Fiber and 5G expansion enabling friction-free UHD streaming | +1.8% | North America, Western Europe | Short term (≤ 2 years) |

| Record investments in local-language originals by global streamers | +1.5% | Global | Medium term (2-4 years) |

| Bundling of VoD with telecom and Pay-TV subscriptions | +1.2% | Latin America, parts of Europe | Short term (≤ 2 years) |

| Growing adoption of cloud-native CDN and edge compute lowering latency | +1.0% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of AVOD Platforms in Emerging Asia-Pacific Markets

Asia-Pacific audiences are embracing ad-supported offerings as platforms trade lower fees for higher reach, a tactic that garnered a USD 24.4 billion regional video revenue pool in 2023 avia.org. Advertisers value the 1.4 billion unique viewers who collectively streamed almost 14 billion hours of Asian content in the same year avia.org[1]Asia Video Industry Association, “AVIA: Asia’s Video Industry in 2023,” avia.org . Forecasts suggest the region will unlock another USD 21 billion in video earnings by 2030 as AVOD inventory scales advanced-television.com [2]Advanced Television, “Asia Pacific Video Revenues to Add USD 21 Billion by 2030,” advanced-television.com . Multilingual ad load personalization and audience-based buying is raising CPMs, allowing platforms to offset thinner subscription margins. Together, these dynamics elevate AVOD from a supplemental to a core monetization pillar across emerging economies.

Expansion of Ultra-High-Speed Broadband Rollout in North America & Western Europe

Fiber-to-the-home penetration, 5G fixed-wireless access, and dynamic CDN routing now underpin seamless UHD delivery. Western European OTT episode and movie revenue will jump to USD 48 billion by 2029 from USD 31 billion in 2023 digitaltvnews.net [3]StreamTV Insider, “Multicast-Assisted Unicast Delivery Cuts Live Bandwidth 90%,” streamtvinsider.com . Operators are piloting multicast-assisted unicast delivery that can trim bandwidth use by as much as 90% during live traffic peaks streamtvinsider.com [4]Digital TV News, “Western Europe OTT Revenues Forecast to Hit USD 48 Billion,” digitaltvnews.net . Viewers benefit through faster start times and reduced buffering across TVs, phones, and in-vehicle screens. Such quality upgrades raise engagement minutes, directly supporting ARPU stability within the Video-on-Demand market.

Increased Content Investments in Local-Language Originals by Global Streamers

Platforms have shifted up to one-third of annual content outlays to regional productions. The Asia Video Industry Association highlights how short-form Chinese dramas and other local formats now secure global demand avia.org. Originals reduce licensing risk and signal cultural relevance, supporting stickiness even when overall subscription costs rise. AI-assisted production workflows, cited by AVIA, are lowering per-hour costs, enabling more frequent series launches. In net terms these investments widen addressable audiences and deepen engagement, feeding a virtuous growth cycle inside the Video-on-Demand market.

Bundling of VoD with Telecom & Pay-TV Subscriptions Driving Uptake in South America

Latin America will climb to 165 million SVOD subs by 2029, up from 110 million in 2023, with Brazil and Mexico as twin engines advanced-television.com. Streamers leverage carrier billing, zero-rating, and hybrid Pay-TV set-top integration to cut churn and expand reach. Chile-Peru carrier Entel earmarked USD 618 million in 2024 capex, largely for fiber rollouts that embed Video-on-Demand market services into converged plans entel.cl. These linkages strengthen the economic moat for both operators and content providers by embedding streaming into household utility budgets.

Restraints Impact Analysis

| Restraint | (∼) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating premium content licensing costs | -1.9% | Global | Short term (≤ 2 years) |

| Rising churn due to subscription fatigue in mature markets | -1.7% | North America, Western Europe | Medium term (2-4 years) |

| Margin pressure on mid-tier platforms lacking economies of scale | -1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Content Licensing Costs Squeezing Platform Margins

Multiyear bidding wars over hit franchises inflate minimum guarantees, squeezing service profitability. Some mid-tier providers have culled libraries, positioning themselves either as buyers of exclusive hits or as sellers monetizing deep back catalogs. The European Commission notes that generative AI tools could eventually ease production costs but the near-term imbalance between spending and returns persists ec.europa.eu. Consequently, operators either push prices up or introduce lower-tier plans with ads, reinforcing the two-track monetization model visible throughout the Video-on-Demand market.

Rising Churn Rates Due to Subscription Fatigue in Matured SVOD Markets

Average monthly cancellation rates climbed in 2024 as cost-conscious households rotate services to chase flagship series. Research projects the subscription economy at USD 1.5 trillion by 2025, emphasizing the competitive tussle for wallet share ijcttjournal.org. Streaming bundles and longer-tenor discounts now act as primary defense. Still, the rise of “serial churners” undermines predictable cash flows and forces fresh spend on acquisition promotions, thereby nudging Video-on-Demand market operators toward diversified revenue streams such as live events and merchandising tie-ins.

Segment Analysis

By Business Model: AVOD Captures Growth Momentum

SVOD controlled 84.63% revenue in 2024, reflecting its early-mover status, but AVOD’s 11.12% forecast CAGR signals accelerating demand for low-cost entertainment. The Video-on-Demand market size attributable to AVOD will widen as global advertising outlays migrate to connected screens. Hybrid packages that merge limited ads with modest fees are emerging to curb subscription fatigue while preserving predictable cash receipts. Niche TVOD windows retain relevance for blockbuster premieres, with sports pay-per-view sustaining premium pricing elasticity.

Consumers in emerging economies increasingly treat AVOD as a first-choice service rather than a fallback, prompting platforms to localize ad creative and shorten ad loads. Advertisers, meanwhile, gain addressable targeting that rivals social media precision. For SVOD incumbents, gradual entry into advertising mitigates ARPU erosion. Together, these shifts refine monetization structures without altering the centrality of customer experience within the broader Video-on-Demand market.

Note: Segment shares of all individual segments available upon report purchase

By Delivery Technology: OTT Streaming Extends Lead

OTT streaming garnered 72% of 2024 revenues and is forecast at 11.3% CAGR through 2030. Unlike managed IPTV, OTT scales globally via open internet and adaptive bitrate protocols. MAUD trials that cut peak bandwidth needs by up to 90% further bolster cost efficiency for live events streamtvinsider.com. Thus, the Video-on-Demand market size for OTT channels will outpace legacy cable and satellite, even where Pay-TV VoD persists.

IPTV remains entrenched in regions with bundled DSL and fiber offerings, while HbbTV adoption in Europe and Brazil’s upcoming TV 3.0 highlight hybrid models that blend broadcast reach with broadband flexibility advanced-television.com. Looking ahead, the Video-on-Demand industry will integrate edge compute nodes to slash latency for immersive experiences such as volumetric video.

By Device Type: Smart TVs Ascend

Phones and tablets accounted for 43% of 2024 viewing time, cementing mobile’s convenience advantage. Yet smart TV shipments and app storefronts are scaling faster; smart-TV household penetration in the United States rose to 79% in 2024, with 62% of homes streaming weekly advanced-television.com. As panels grow brighter and cheaper, living-room screens reclaim primacy for premium dramas and sports.

Consequently, the Video-on-Demand market size captured by large-screen advertising is expanding. Plug-in streaming devices plateaued at 56% household usage in 2024 as built-in operating systems reduce cabling clutter thestreamable.com. PCs persist for educational video and dual-screen multitasking but no longer drive incremental subscriber growth.

By Content Genre: Sports Surges

Entertainment and drama anchored 50% of 2024 revenues, underscoring the evergreen appeal of scripted series. However, live sports leads in price elasticity, growing at 14% CAGR as leagues migrate online. The Video-on-Demand market size attached to sports commands premium CPMs, and rights holders negotiate platform-agnostic carve-outs to maximize global reach.

Kids and family libraries reduce churn because parents value safe-watch lists, while documentaries and educational content cultivate loyal micro-communities. Cross-category bundling mirrors linear pay-TV channel packs, but algorithmic row curation personalizes discovery, reinforcing engagement loops across the Video-on-Demand market.

Note: Segment shares of all individual segments available upon report purchase

By End-user: Commercial Uses Expand

Residential accounts captured 82% of spend in 2024, yet commercial venues like hotels, airlines, and hospitals register a 16% CAGR, making them a fast-emerging frontier. IBM’s enterprise-grade platform exemplifies how secure, scalable streams serve training, events, and customer amenity needs ibm.com.

Educational institutions embed lectures inside learning-management systems, while public agencies disseminate updates through on-demand portals. These diversified deployments broaden the Video-on-Demand market reach beyond direct consumer entertainment, anchoring new SaaS-style revenue models.

Geography Analysis

North America remained the largest contributor at 41.65% revenue share in 2024, benefiting from early broadband ubiquity and deep original-content pipelines. Industry bundles launched in 2025 combine multiple flagship services into discounted packages, an antidote to subscription fatigue. Federal infrastructure grants continue to extend rural fiber, reinforcing the Video-on-Demand market’s leadership position.

Asia-Pacific is the fastest-growing territory, tracking a 12.2% CAGR to 2030. National initiatives spanning 5G, cloud, and local-language production have spurred USD 24.4 billion in 2023 regional revenue avia.org. India and China top subscriber additions, while Japan and South Korea export cultural hits that travel well internationally. Growth is further supported by robust digital advertising spend, underpinning AVOD viability across emerging economies.

Latin America shows accelerating scale, projected to host 165 million SVOD accounts by 2029 advanced-television.com. Brazil alone may surpass 59 million subs. Telco partnerships ease payments and satisfy bandwidth requirements via ongoing fiber projects such as Entel’s USD 618 million 2024 investment entel.cl. Although global majors dominate, local platforms still secure 8% market share, reflecting regional storytelling demand within the Video-on-Demand market.

Competitive Landscape

Innovation and Adaptation Drive Market Success

Market structure is bifurcated: a small cohort of global giants holds outsized influence, while hundreds of regional or niche services chase underserved verticals. Six multibillion-dollar mergers announced since 2024 exemplify consolidation momentum, including the 2025 Hulu + Live TV and Fubo union creating a 6.2 million-subscriber pay-TV alternative cnn.com.

Content exclusivity remains the chief competitive lever. Platforms earmark record budgets for originals, and the European Commission has flagged potential concentration risk in data, chips, and cloud capacity underpinning AI-driven video workflows ec.europa.eu. To widen moats, tech-media hybrids patent immersive delivery methods such as Apple’s viewport-adaptive streaming patentscope.wipo.int.

Regional entrants differentiate via language, price, and live event specialization. FAST (Free Ad-Supported TV) channels aimed at U.S. Hispanic viewers, launched by Spanglish Movies in 2024, illustrate micro-targeting potential digitaltvnews.net. Collectively, these forces translate into relentless feature innovation and strategic bundling designed to stabilize engagement and defend share in the global Video-on-Demand market.

Video-on-Demand Industry Leaders

-

Netflix Inc.

-

The Walt Disney Company (Disney+ & Hulu)

-

Warner Bros. Discovery Inc. (Max)

-

Apple Inc. (Apple TV+)

-

Amazon.com Inc. (Prime Video)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Disney’s Hulu + Live TV and Fubo confirmed a merger, forming the second-largest U.S. pay-TV provider with 6.2 million subs cnn.com.

- undefinedDec 2024: DAZN acquired Foxtel for USD 2.2 billion, expanding its sports rights in Australia.

- undefinedOct 2024: DirecTV announced plans to purchase Dish, Sling TV, and EchoStar’s TV business, combining nearly 20 million satellite users

- May 2024: Disney Entertainment and Warner Bros. Discovery unveiled a Disney+, Hulu, and Max U.S. streaming bundle wbd.com.

Global Video-on-Demand Market Report Scope

Video on demand is a technology that enables users to stream video content over the internet on computers, televisions, and mobile devices through applications, such as OTT platforms, without the constraint of time. This includes a fee-based business model, transactional video-on-demand (TVoD), subscription video-on-demand (SVoD), and others. The video content comes from various categories: media and entertainment, education and training, health and fitness, and others.

The video-on-demand market for the study defines revenues generated from the business model, such as transactional video-on-demand (TVoD), subscription video-on-demand (SVoD), and other business models across the globe. The study also analyses the overall impact of the COVID-19 pandemic on the ecosystem. The study includes qualitative coverage of the most adopted strategies and an analysis of the key base indicators in emerging markets.

The video-on-demand The market is segmented by business model (transactional video-on-demand (TVoD) and subscription video-on-demand (SVoD)) and geography (North America, Europe, Asia Pacific, the Middle East and North Africa, and the Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the segments.

| Subscription Video-on-Demand (SVOD) |

| Advertising Video-on-Demand (AVOD) |

| Transactional/Pay-per-view (TVOD) |

| Hybrid and Other Models |

| Over-the-Top (OTT) Streaming |

| Internet Protocol Television (IPTV) VoD |

| Pay-TV VoD |

| Hybrid Broadcast Broadband TV (HbbTV) |

| Smartphones and Tablets |

| Smart TVs |

| PCs and Laptops |

| Connected Streaming Devices |

| Others |

| Entertainment and Drama |

| Sports |

| Kids and Family |

| Educational and Documentary |

| Others (News, Lifestyle) |

| Residential / Individual |

| Commercial and Enterprise (Hotels, Airlines, Hospitals) |

| Educational Institutions |

| Public Sector and Government |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Business Model | Subscription Video-on-Demand (SVOD) | |

| Advertising Video-on-Demand (AVOD) | ||

| Transactional/Pay-per-view (TVOD) | ||

| Hybrid and Other Models | ||

| By Delivery Technology | Over-the-Top (OTT) Streaming | |

| Internet Protocol Television (IPTV) VoD | ||

| Pay-TV VoD | ||

| Hybrid Broadcast Broadband TV (HbbTV) | ||

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| PCs and Laptops | ||

| Connected Streaming Devices | ||

| Others | ||

| By Content Genre | Entertainment and Drama | |

| Sports | ||

| Kids and Family | ||

| Educational and Documentary | ||

| Others (News, Lifestyle) | ||

| By End-user | Residential / Individual | |

| Commercial and Enterprise (Hotels, Airlines, Hospitals) | ||

| Educational Institutions | ||

| Public Sector and Government | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Video-on-Demand market?

The market is valued at USD 126.16 billion in 2025 and is projected to reach USD 218.89 billion by 2030, reflecting an 11.65% CAGR.

Which region is growing fastest in the Video-on-Demand market?

Asia-Pacific leads with a 12.2% CAGR outlook to 2030, supported by rising smartphone use, local originals, and expanding 5G connectivity.

Why is AVOD expanding faster than SVOD?

Ad-supported tiers address consumer price sensitivity and offer advertisers precise targeting, driving an 11.12% CAGR for AVOD through 2030.

How will smart TVs affect streaming consumption?

Smart-TV household penetration hit 79% in the United States in 2024, and this shift toward integrated large screens is projected to grow at 15.1% CAGR, challenging mobile dominance.

Page last updated on: