Market Size of Video Encoder Industry

| Study Period | 2019 - 2029 |

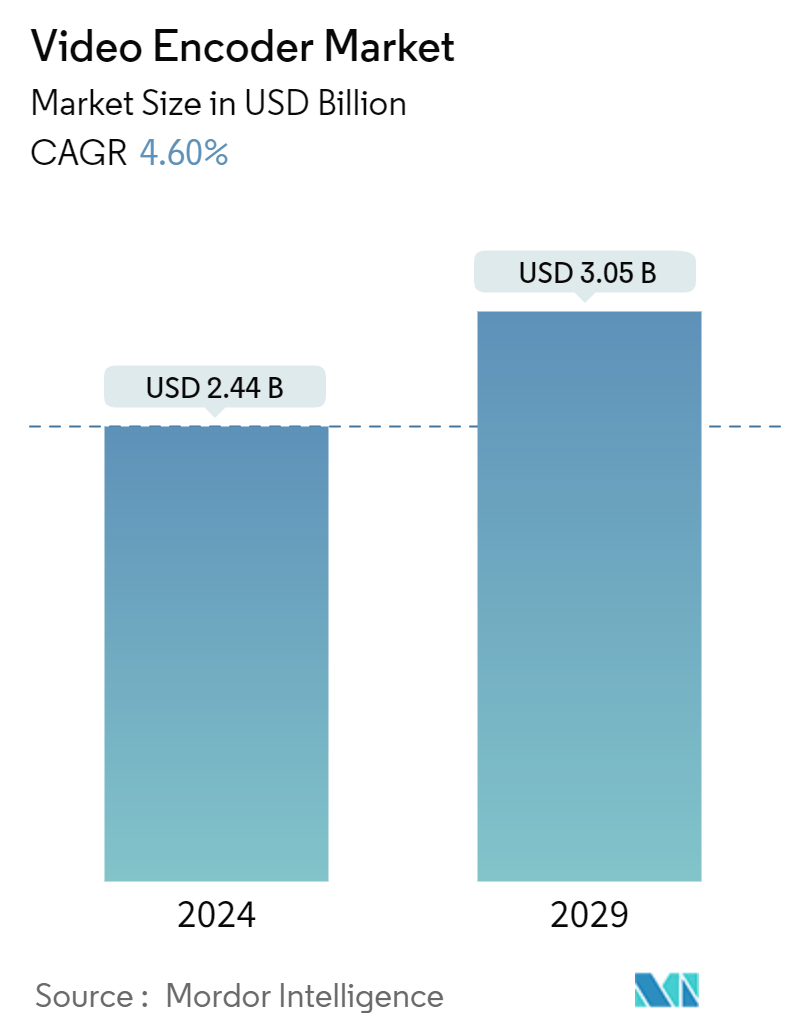

| Market Size (2024) | USD 2.44 Billion |

| Market Size (2029) | USD 3.05 Billion |

| CAGR (2024 - 2029) | 4.60 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Video Encoder Market Analysis

The Video Encoder Market size is estimated at USD 2.44 billion in 2024, and is expected to reach USD 3.05 billion by 2029, growing at a CAGR of 4.60% during the forecast period (2024-2029).

- The video encoder market is witnessing strong growth, driven by the rising demand for high-quality video streaming and broadcasting across various platforms. Video encoders convert video signals into digital formats suitable for transmission over the Internet or other networks. This market's expansion is fueled by the increasing consumption of online video content, the proliferation of over-the-top (OTT) services, and the surge in live-streaming activities. The widespread adoption of social media platforms, where video content is a key engagement tool, further propels the demand for advanced video encoding solutions.

- Technological advancements are pivotal in shaping the video encoder market. Innovations in compression algorithms, such as H.265 (HEVC) and the emerging AV1 codec, enhance compression rates while maintaining video quality, facilitating efficient data transmission and storage. These advancements support the increasing demand for 4K and 8K video resolutions, which require significantly more bandwidth and storage capacity.

- Additionally, the development of hardware encoders that integrate artificial intelligence (AI) and machine learning (ML) represents a significant trend. These integrations improve real-time video processing capabilities and optimize network resources.

- Moreover, major players such as Cisco Systems Inc., Harmonic Inc., and Axis Communications AB (Canon Inc.) lead the pack in the video encoder market. Alongside these industry stalwarts, newer firms are making waves with innovative solutions. These players are actively pursuing strategies like mergers, acquisitions, partnerships, and product launches to bolster their market positions. Notably, many are forging strategic ties with OTT service providers and broadcasters, seeking to tap into synergies and broaden their customer reach.

- The video encoder market exhibits a highly promising outlook with significant growth opportunities. The ongoing evolution of video standards, the global deployment of 5G networks, and the increasing demand for immersive experiences, such as virtual reality (VR) and augmented reality (AR), are set to drive further innovations and applications. Companies prioritizing research and development and swiftly adapting to technological shifts will be well-positioned to capitalize on emerging trends and maintain their competitive advantage.

- While the video encoder market boasts numerous growth drivers, a notable hurdle emerges in the form of the steep initial costs associated with hardware video encoders. These devices, pivotal for transforming raw video into digital formats for broadcasting and streaming, often demand a significant upfront investment. This financial outlay can pose a formidable obstacle, especially for smaller enterprises and startups. The resulting high costs may dissuade potential customers from embracing new technologies or modernizing their existing setups, constraining market expansion and stifling innovation. Moreover, these expenses can directly impact a company's overall return on investment, underscoring the importance for manufacturers to explore cost-cutting measures or offer flexible financing options to spur wider adoption.

Video Encoder Industry Segmentation

The video encoder market encompasses the industry involved in producing, selling, and developing video encoding hardware and software. The scope of the study focuses on the market analysis segmented by application (pay TV [cable video encoder, satellite video encoder, IPTV video encoder], broadcast and digital terrestrial television (DTT) [contribution video encoder, backhaul and distribution video encoder, DTT video encoder], and security and surveillance) and geography (Americas [United States, Canada, Brazil, Mexico, and Rest of the Americas], Europe [Germany, United Kingdom, France, Russia, Poland, and Rest of Europe], Asia-Pacific [China, India, South Korea, Japan, and Rest of Asia-Pacific], and Middle East and Africa [Turkey, Israel, United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa]. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Application | |||||

| |||||

| |||||

| Security and Surveillance |

| By Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Video Encoder Market Size Summary

The video encoder market is experiencing robust growth, driven by the increasing demand for high-quality video streaming and broadcasting across various platforms. This growth is largely attributed to the rising consumption of online video content, the expansion of over-the-top (OTT) services, and the surge in live-streaming activities. The widespread use of social media platforms, where video content plays a crucial role in user engagement, further fuels the demand for advanced video encoding solutions. Technological advancements, particularly in compression algorithms like H.265 (HEVC) and the emerging AV1 codec, are enhancing compression rates while maintaining video quality, supporting the demand for higher resolutions such as 4K and 8K. Additionally, the integration of artificial intelligence (AI) and machine learning (ML) in hardware encoders is improving real-time video processing capabilities, optimizing network resources, and driving market innovation.

The market is characterized by significant competition, with major players such as Cisco Systems Inc., Harmonic Inc., and Axis Communications AB (Canon Inc.) leading the industry. These companies, along with newer entrants, are actively engaging in mergers, acquisitions, partnerships, and product launches to strengthen their market positions. The video encoder market is poised for further growth, driven by the evolution of video standards, the global rollout of 5G networks, and the increasing demand for immersive experiences like virtual reality (VR) and augmented reality (AR). However, the high initial costs associated with hardware video encoders pose a challenge, particularly for smaller enterprises and startups, potentially hindering market expansion. Despite this, the ongoing advancements and strategic collaborations among industry players are expected to sustain the market's promising outlook.

Video Encoder Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Analysis of Video Codecs and Their Evolution

-

1.3 List of VVC-approved and Incorporated Companies

-

1.4 List of Companies Contributing to the VVC Standard

-

1.5 Impact of COVID-19 on the Market

-

1.6 Industry Attractiveness - Porter's Five Forces Analysis

-

1.6.1 Bargaining Power of Suppliers

-

1.6.2 Bargaining Power of Buyers

-

1.6.3 Threat of New Entrants

-

1.6.4 Threat of Substitutes

-

1.6.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Application

-

2.1.1 Pay TV

-

2.1.1.1 Cable Video Encoder

-

2.1.1.2 Satellite Video Encoder

-

2.1.1.3 IPTV Video Encoder

-

-

2.1.2 Broadcast and Digital Terrestrial Television (DTT)

-

2.1.2.1 Contribution Video Encoder

-

2.1.2.2 Backhaul and Distribution Video Encoder

-

2.1.2.3 DTT Video Encoder

-

-

2.1.3 Security and Surveillance

-

-

2.2 By Geography

-

2.2.1 Americas

-

2.2.1.1 United States

-

2.2.1.2 Canada

-

2.2.1.3 Brazil

-

2.2.1.4 Mexico

-

2.2.1.5 Rest of the Americas

-

-

2.2.2 Europe

-

2.2.2.1 Germany

-

2.2.2.2 United Kingdom

-

2.2.2.3 France

-

2.2.2.4 Russia

-

2.2.2.5 Poland

-

2.2.2.6 Rest of Europe

-

-

2.2.3 Asia-Pacific

-

2.2.3.1 China

-

2.2.3.2 India

-

2.2.3.3 South Korea

-

2.2.3.4 Japan

-

2.2.3.5 Rest of Asia-Pacific

-

-

2.2.4 Middle East and Africa

-

2.2.4.1 Turkey

-

2.2.4.2 Israel

-

2.2.4.3 United Arab Emirates

-

2.2.4.4 Saudi Arabia

-

2.2.4.5 South Africa

-

2.2.4.6 Rest of Middle East and Africa

-

-

-

Video Encoder Market Size FAQs

How big is the Video Encoder Market?

The Video Encoder Market size is expected to reach USD 2.44 billion in 2024 and grow at a CAGR of 4.60% to reach USD 3.05 billion by 2029.

What is the current Video Encoder Market size?

In 2024, the Video Encoder Market size is expected to reach USD 2.44 billion.