| Study Period | 2021 - 2030 |

| Market Size (2025) | USD 128.73 Billion |

| Market Size (2030) | USD 163.52 Billion |

| CAGR (2025 - 2030) | 4.90 % |

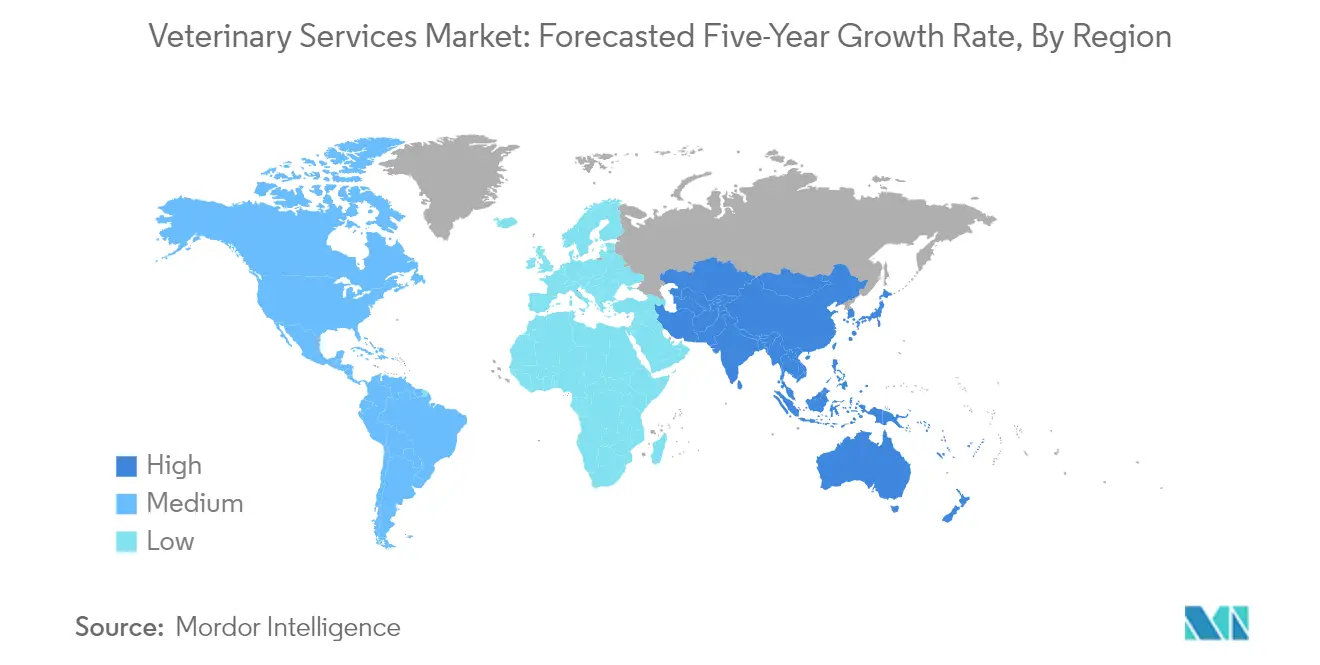

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Veterinary Services Market Analysis

The Veterinary Services Market size is estimated at USD 128.73 billion in 2025, and is expected to reach USD 163.52 billion by 2030, at a CAGR of 4.9% during the forecast period (2025-2030).

The Humanization of Pets: Redefining Expectations in Veterinary Care

The relationship between humans and their animals has fundamentally transformed, creating ripple effects throughout the veterinary industry. In 2025, the depth of this human-animal bond continues to intensify, with research showing that 66% of North Americans now consider their pets as family members. This shift is not merely sentimental—it's restructuring spending patterns, service expectations, and the very nature of veterinary services. Pet parents are increasingly seeking specialized care including preventive wellness plans, advanced diagnostics, and even mental health services for their animals.

The veterinary sector is responding with premium service offerings, expanded clinic hours, and personalized care plans that mirror human healthcare models. Particularly notable is the emergence of boutique veterinary practices catering to specific niches like geriatric pet care, holistic medicine, and sports medicine for active pets. The actionable insight for industry participants is clear: success in today's veterinary market requires more than clinical excellence—it demands a deep understanding of the emotional connection between owners and pets, and the ability to deliver services that honor and support that bond.

The Hidden Crisis: Workforce Sustainability in Veterinary Services

Beneath the growing demand curves of the veterinary industry lies a workforce challenge that threatens long-term market stability. The profession faces concerning occupational wellness statistics, with U.S. veterinarian suicide rates 50% higher than the general population as of 2022. Meanwhile, financial pressures continue to mount, with 88% of veterinary professionals citing student debt as their primary stressor. These realities have created staffing shortages across the vet industry, shifting the balance of power toward practitioners and driving up service costs. Progressive practices are responding with comprehensive staff wellness programs, flexible scheduling options, and innovative compensation models that include equity participation. Corporate consolidators are leveraging their scale to offer career advancement pathways and work-life balance initiatives that independent practices struggle to match.

The critical inference for stakeholders is that addressing workforce sustainability isn't merely a human resources consideration—it's becoming the determining factor in market competitiveness, service pricing, and practice valuation. Organizations investing in practitioner well-being today are positioning themselves for optimal growth in a talent-constrained marketplace.

Beyond the Traditional Clinic: New Frontiers in Animal Healthcare Delivery

The delivery infrastructure of the veterinary services market is undergoing a significant evolution, breaking free from the constraints of traditional brick-and-mortar clinics. Mobile veterinary services, telehealth platforms, and in-home care options are expanding rapidly, responding to pet owners' preference for convenience and reduced stress for their animals. These alternative delivery models are particularly effective for routine preventive care and chronic disease management, areas where continuity rather than facility-based intervention is paramount. The success of these approaches is evidenced in part by impressive outcomes in various care settings—for instance, shelter medicine services achieved a remarkable 97.12% live release rate in 2024, with 98% for dogs and 96.5% for cats. These veterinary industry trends signal opportunities for market differentiation beyond traditional service boundaries.

Forward-thinking companies are investing in hybrid care models that combine virtual triage with targeted in-clinic diagnostics, creating seamless experiences for both clients and patients. The strategic implication is clear: geographical limitations are becoming less relevant than digital accessibility and care consistency, creating opportunities for providers to expand their service footprint without proportional increases in physical infrastructure.

Veterinary Services Market Trends

Zoonotic Threats: Driving Demand for Advanced Veterinary Care

The connection between animal and human health is creating new opportunities in veterinary services. Over 60% of known human infectious pathogens are zoonoses, transmitted between animals and humans. This fact is pushing veterinary services beyond basic animal care into critical public health roles. Veterinary industry practices that invest in advanced diagnostics for emerging animal diseases can capture both preventive care markets and public health partnerships. This evolution makes veterinary professionals essential players in disease monitoring systems, not just animal healthcare providers.Consider that approximately 70% of new pathogens originate in animals, including major threats like SARS-CoV-2, influenza strains, and Ebola virus. This reality is changing how veterinary clinics operate, with many expanding their infectious disease capabilities.

The business opportunity is clear: veterinary services providers who develop expertise in zoonotic disease management and build partnerships with human healthcare systems will access new funding streams focused on biosecurity and disease surveillance, while delivering better care to animal patients.

Pet Adoption Surge: Creating New Demands for Veterinary Services

The significant increase in pet ownership is transforming veterinary service requirements. With 68% of North Americans living with at least one pet as of 2022, veterinary practices are seeing more clients with higher expectations. Today's "pet parents" want animal healthcare that matches human standards. Smart veterinary industry businesses are responding by improving the clinic experience with better digital communication, more convenient hours, and enhanced facilities that resemble human healthcare settings.This pet ownership trend reflects broader social changes: later parenthood, more single-person households, and pets becoming central family members. The 68% pet ownership rate in North America creates opportunities for veterinary services market providers to offer specialized services.

Practices that develop expertise in behavioral medicine, elder pet care, and family-centered preventive services are particularly well-positioned. The most successful veterinary services recognize that pet care now requires both standard medical services and premium "family member" experiences tailored to different client segments.

Rising Pet Healthcare Spending: From Optional to Essential

Pet healthcare spending patterns increasingly mirror human healthcare priorities, with veterinary care now viewed as essential rather than optional. This shift aligns with the pet humanization trend evident in North America's 68% pet ownership rate. Unlike spending on pet toys or accessories, veterinary services expenditures remain stable even during economic downturns. Veterinary market practices that communicate value rather than focusing solely on price are particularly successful in this environment, especially when offering payment plans and wellness programs that make costs more manageable.

The growth in pet healthcare spending is creating markets for specialized services previously unavailable in many regions. High pet ownership rates provide enough demand to support veterinary services industry specialties like cardiology, oncology, rehabilitation therapy, and nutritional counseling. For veterinary industry businesses, the key opportunity lies in developing focused expertise in high-demand specialties rather than attempting to cover all advanced care areas. Practices that align their specialized services with local client needs and spending capacity will outperform more generalized competitors in the veterinary sector.

Segment Analysis: By Service

Surgical Services: The Core Revenue Driver

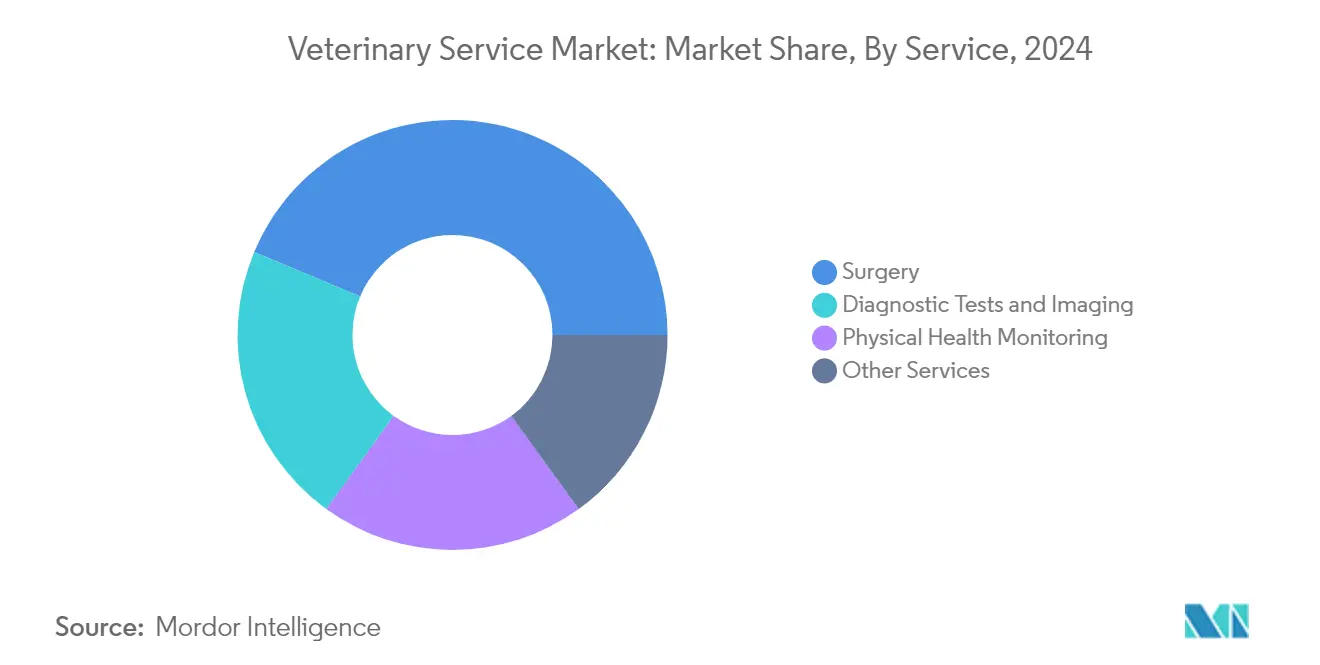

Surgery continues to be the main revenue driver in the veterinary services market, holding a substantial 43.7% share. This dominance stems from the essential nature of surgical procedures for both emergency situations and planned interventions. The growing adoption of pet insurance has particularly strengthened this segment by making expensive surgical procedures more accessible to pet owners. For veterinary practices looking to maximize their market position, focused investments in surgical specialization and modern equipment provide a competitive advantage, especially as veterinary industry trends show clients increasingly expect surgical outcomes comparable to human healthcare standards.

Advanced Diagnostics: Technology-Driven Growth

Diagnostic tests and imaging is expanding at a CAGR of 7.81%, transforming precision capabilities in the veterinary market. This growth is powered by significant technological improvements that enhance diagnostic accuracy. Modern 3T MRI imaging equipment used in veterinary diagnostics now delivers twice the resolution and performs scans in half the time compared to previous models. This reflects a shift toward evidence-based approaches and early intervention in the veterinary industry. The key takeaway for service providers is straightforward: clinics that invest in advanced diagnostic technologies gain substantial market advantage, as accurate early diagnosis increasingly drives treatment success and client satisfaction.

Preventive Care & Specialized Services: Creating Client Value

Physical health monitoring and complementary services are becoming increasingly important components of comprehensive animal care in the veterinary services industry. Preventive health services have evolved from basic check-ups to sophisticated monitoring systems, including remote technologies and preventive care programs. Specialized offerings like rehabilitation therapy, behavior management, and nutritional counseling continue to grow as animal owners recognize their impact on overall wellbeing. These service categories represent significant opportunities for practices seeking to stand out in the competitive veterinary sector. Particularly effective is the combination of telehealth with in-person monitoring, creating continuous care models that strengthen client relationships while optimizing resources. For forward-thinking veterinary businesses, these services offer a path to increased client retention without requiring the major investments needed for surgical or diagnostic capabilities.

Segment Analysis: By Animal Type

Companion Animal Care: Leading Market Growth and Share

Companion animals dominate the vet industry with a 62.5% market share while also leading in growth at 9.0% CAGR. This reflects a fundamental change in how people view pet ownership, with pets increasingly considered family members rather than simply animals. Pet owners now regularly approve advanced treatments and preventive care similar to human healthcare standards. This trend is particularly significant for veterinary practices in urban and suburban areas, where the veterinary market for premium services remains far from saturated. The clear strategy for service providers is to develop comprehensive care packages addressing the full lifecycle needs of pets while emphasizing both emotional connection and clinical outcomes to capture more of this growing market segment.

Farm Animal Services: Economics-Driven Veterinary Care

The farm animal veterinary sector operates under different economic principles than companion animal care, focusing primarily on productivity and livestock value rather than emotional factors. Cost efficiency is crucial, with 60-70% of variable costs in dairy farms going to feed and fodder. Veterinary services in this segment increasingly focus on herd-level health management systems designed to optimize reproduction, nutrition, and disease prevention across the entire operation. Timing in reproductive management is particularly critical, as missing an insemination opportunity can delay conception by at least 21 days, affecting overall profitability. For veterinary providers targeting this segment, success depends on presenting their services as investments rather than expenses by clearly demonstrating the financial returns of preventive health protocols and strategic interventions to livestock operation managers, a critical factor driving the overall veterinary services market size and veterinary market size.

Geography Analysis

North America: The Established Powerhouse of Veterinary Care

North America leads the global veterinary services market, holding 41.2% of global market share. This dominance reflects the region's strong pet culture and advanced veterinary infrastructure. High pet ownership rates, willingness to spend on animal health, and cutting-edge technologies have created a market where quality often matters more than cost. However, urban market saturation has pushed providers to innovate through telemedicine and mobile clinics. Rising care costs have also created an interesting trend - pet medical tourism. Data shows that dogs and cats traveling from the U.S. to Mexico for cheaper veterinary services increased by 68%, from about 20,000 in 2019 to over 33,500 in 2022. For businesses in this space, the key opportunity isn't just expanding market presence but developing deeper service offerings and addressing the affordability gap that prevents many pet owners from accessing care.

United States: Where Premium Care Drives Market Leadership

The United States dominates North America's veterinary market, accounting for about 70% of regional market share. This leadership stems from America's strong pet insurance sector, technological advances in veterinary medicine, and consumers who readily pursue advanced treatments for their pets. The high-end segment continues to grow, with specialty veterinary services commanding premium prices - a specialty hospital stay for a dog with acute pancreatitis can cost up to USD 8,000 for just 36 hours of care. This pricing reality creates both opportunity and challenge: while premium services thrive, they leave a gap that innovative companies are filling through subscription-based preventive care and tiered service options. For businesses in this market, the most promising growth strategy involves creating hybrid care models that maintain quality while making services accessible across different price points.

Canada: The Value-Conscious Veterinary Market

Canada makes up roughly 20% of North America's veterinary services industry and has developed a market known for balanced pricing and consumer-focused care models. The country's veterinary sector operates with more transparent pricing than the US, with diagnostic services like X-rays ranging from CAD USD 116 to CAD USD 188 for small plates and CAD USD 174 to CAD USD 217 for larger plates. This transparency extends to other services, with standard sedation for cats costing about CAD USD 145 to CAD USD 217, while larger dogs may require sedation costing up to CAD USD 362. Canada's regulatory framework supports this approach, with Statistics Canada's classification system specifically designating veterinary services to include medicine, dentistry, surgery, and laboratory services. For companies operating in Canada, a significant opportunity exists in expanding rural access to specialized care by connecting remote areas to urban veterinary expertise through hub-and-spoke models.

Mexico: The Emerging Cross-Border Veterinary Destination

Mexico's impact on the North American veterinary landscape goes beyond its 10% regional market share, as it increasingly becomes a destination for price-sensitive pet owners from the United States. This cross-border trend represents a meaningful market shift rather than a temporary phenomenon, creating a distinct segment where Mexican providers balance international standards with affordable pricing. The 68% increase in pets traveling from the U.S. to Mexico for veterinary care between 2019 and 2022 highlights this change in consumer behavior. Mexican veterinary practices are adapting by offering bilingual services, international payment options, and recovery accommodations designed for traveling pets and their owners. This development offers valuable insights for veterinary practices everywhere: in markets with rising care costs, emphasizing value-for-money rather than competing solely on clinical capabilities can unlock significant growth.

Asia-Pacific: The Growth Engine Reshaping Veterinary Care

The Asia-Pacific region stands as the most dynamic area in the global veterinary market, growing at 9.05% CAGR - the highest among all regions. This rapid growth comes from urbanization, rising middle-class incomes, changing attitudes toward pet ownership, and growing animal welfare awareness. Unlike mature markets where service expansion drives growth, Asia-Pacific's momentum comes from market development - new pet owners entering the care system and agricultural modernization improving livestock healthcare standards. This creates growth in both companion animal and farm animal segments simultaneously.

The region's veterinary education is evolving to support this growth, with specialized programs like the Certificate in Veterinary Diagnostic Imaging at GADVASU in India offering 6-month courses for approximately USD 650 to train new veterinary professionals. For global veterinary companies, the key question isn't whether to invest in Asia-Pacific but how to adapt services to diverse markets at different development stages while establishing early brand presence.

China: The Volume-Driven Market Leader

China leads the Asia-Pacific veterinary services market, representing about 40% of regional market share. This position comes from China's massive scale in both urban pet ownership and rural livestock production, creating a huge market for veterinary services. China's market is developing at two speeds - rapid modernization of urban veterinary care alongside gradual transformation of rural animal healthcare. Urban growth is driven by pet humanization among China's growing middle class, who increasingly see pets as family members deserving quality healthcare. Meanwhile, the country's push to modernize livestock production creates parallel demand for veterinary expertise focused on herd health and efficiency. For companies in this market, the biggest opportunity lies in developing scalable care models that can be quickly deployed across China's vast geography while addressing the significant differences in consumer spending power between major cities and developing regions.

India: The Veterinary Market's Emerging Powerhouse

India is becoming a key growth driver in Asia-Pacific's veterinary services landscape, with development outpacing even the region's impressive 9.05% CAGR. This accelerated growth comes from India's unique market characteristics - the simultaneous modernization of its large livestock sector and rapid growth in pet ownership among urban middle-class families. The country is building its veterinary infrastructure at both educational and practice levels, with programs like GADVASU's Certificate in Veterinary Diagnostic Imaging representing efforts to develop specialized capabilities. This program, with its approximately USD 650 tuition fee and limited enrollment of just 4 students, shows both the premium nature of advanced veterinary education and current capacity limitations. The dairy sector remains particularly important, with programs like GADVASU's B.Tech in Dairy Technology (USD 1,560 for 4 years) and M.Tech (USD 871 for 2 years) preparing professionals for an industry where veterinary services are increasingly integrated with production systems. For companies entering this market, India offers an opportunity to establish early leadership in specialized veterinary segments where competition remains limited.

The Diverse Veterinary Landscapes of Japan, Australia, and Southeast Asia

Beyond China and India, Asia-Pacific's other veterinary markets present a diverse mix of development stages, each with unique characteristics requiring market-specific approaches. Japan's mature veterinary sector focuses on preventive care and wellness services, reflecting the country's aging pet population and owners willing to invest in extending their pets' healthy lives. Australia's veterinary ecosystem has evolved to address both conventional pet care and the unique needs of native wildlife, creating specialized capabilities that could potentially be exported to other markets. South Korea's rapidly modernizing veterinary sector increasingly resembles Western care models but with cultural adaptations that combine traditional Eastern and modern Western veterinary practices. This diversity extends throughout Southeast Asia, where countries at various economic development stages are establishing regulatory frameworks and professional standards. For companies operating across multiple countries, success requires localization strategies that respect each country's unique veterinary traditions while introducing standardized quality measures and operational efficiencies.

Europe: The Innovation Hub for Integrated Veterinary Care Models

Europe's veterinary services market combines mature market characteristics with areas of innovation that influence global veterinary practices. The region approaches veterinary care with greater emphasis on preventive services, wellness care, and integration into broader One Health initiatives that connect animal, human, and environmental health. This creates distinctive market opportunities, particularly where public and private veterinary services overlap. Within Europe, Germany leads with roughly 30% of the regional market, followed by the United Kingdom (25%), France (20%), Italy (15%), and Spain (10%). The region embraces technology adoption, as seen at France's Livet Equine Veterinary Medical Center, which reported that upgrading to Agfa's DR system enabled them to work three times faster, reducing bottlenecks and shortening wait times for equine patients. This focus on efficiency through technology investment helps maintain service quality while managing costs in a market where pricing is often more constrained than in North America.

Middle East and Africa: The Emerging Veterinary Frontier

The Middle East and Africa region presents perhaps the most diverse veterinary industry landscape globally, covering markets at very different development stages - from sophisticated urban veterinary hospitals in GCC countries to emerging rural veterinary networks in Sub-Saharan Africa. This diversity creates a segmented market where service sophistication and pricing vary dramatically between and even within countries. The GCC area drives market value through high-end companion animal care and specialized services for valuable livestock, particularly in equine medicine and camel health - niches where regional expertise has global relevance. South Africa serves as another regional center of excellence, with established veterinary education and practices addressing both pet care and wildlife conservation needs. The broader African continent offers significant growth potential as livestock productivity becomes a development priority and pet ownership gradually increases with urbanization. For businesses in this region, the most promising approach involves creating tiered service models that can address diverse needs and payment abilities while developing training programs to expand the currently limited veterinary workforce.

South America: Where Livestock Excellence Meets Companion Animal Care

South America's veterinary market stands out for its balance between companion animal and livestock segments, with farm animals playing a more prominent role than in most developed markets. This balance comes from the region's importance in global meat and dairy production, creating substantial demand for sophisticated farm animal veterinary services. Brazil dominates with approximately 60% market share, leveraging its position as an agricultural powerhouse to drive veterinary service demand, while Argentina contributes roughly 40% with its similarly strong agricultural base. The region has developed recognized expertise in areas including reproductive technologies, tropical disease management, and sustainable livestock health programs for extensive grazing systems. While pet care continues to grow, particularly in cities, what makes South America's veterinary market distinctive is how practices often successfully combine companion and production animal medicine rather than specializing in just one area. This integration creates resilient business models less vulnerable to economic fluctuations affecting discretionary spending on pet care. For veterinary companies, the region offers significant opportunities to develop specialized expertise in sustainable livestock health management that balances productivity with reduced antimicrobial use and environmental impact.

Veterinary Services Industry Overview

Capital Infusion Fuels Strategic Consolidation: The Race for Scale and Scope

The veterinary services market is seeing major players secure significant funding to grow through acquisitions and new clinic openings. In 2022, Modern Animal raised USD 75 million in Series C funding, bringing its total to USD 164 million to support its expansion across the US. Similarly, Bond Vet grew from 11 to 16 clinics in just six months, with plans to reach over 30 locations by year-end. This pattern reveals an important reality: size matters in today's veterinary industry. Companies with stronger financial backing can invest in advanced equipment for high-margin services like surgery (which makes up about 43.7% of the market) while expanding their geographic reach. For industry players, this means capital efficiency and smart acquisition strategies are now must-have capabilities. Smaller, independent practices face growing pressure to either join forces with others or find specialized niches to remain competitive in this consolidating marketplace.

Beyond Traditional Care: Technology as the New Competitive Frontier

The veterinary sector is evolving beyond basic care models, with technology integration becoming a key factor separating market leaders from followers. Top companies now compete not just on clinical skills but on tech-enabled services that improve client convenience, boost efficiency, and support data-driven care decisions. The Diagnostic Tests and Imaging segment, growing at approximately 7.81% annually (faster than any other service category), highlights this tech-driven shift. Industry leaders know that investing in advanced diagnostics creates significant advantages over smaller competitors who can't match these investments. Today's competitive edge comes from creating seamless digital experiences—from AI diagnostics to virtual vet visits and user-friendly apps—that meet the expectations of tech-savvy pet owners. For veterinary services industry participants, developing a practical technology roadmap has become essential to stay relevant and gain market share in an increasingly digital competitive landscape.

Strategic Geographic Expansion: Targeting High-Growth Regional Opportunities

The global veterinary market shows distinct regional growth patterns, requiring companies to develop targeted strategies rather than universal approaches. While North America leads with about 41.2% of the global market, Asia-Pacific is growing much faster at around 9.05% annually, driven by increasing pet ownership, higher incomes, and growing animal healthcare awareness. This growth difference is changing how companies compete, with established Western players looking east for new opportunities while defending their home markets.

The Companion Animals segment, which represents about 62.5% of the market and is growing at roughly 9.0% yearly, offers particularly promising opportunities in Asian urban centers where pet ownership is rising among middle-class consumers. For companies in this space, developing specific market entry plans that address different regulations, cultural attitudes toward pets, and service preferences has become crucial for long-term growth, requiring a careful balance between maintaining strength in mature markets and establishing early positions in emerging ones.

Veterinary Services Market Leaders

-

CVS Group PLC

-

Ethos Veterinary Health

-

Idexx Laboratories

-

Mars Inc.

-

Zoetis

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Veterinary Services Market News

- May 2022: The Chief Minister of Andhra Pradesh, Sri YS Jagan Mohan Reddy, officially launched 175 Mobile Ambulatory Veterinary Clinics (MAVCs) with an investment of Rs 278 crore. The state government planned to establish 340 Dr. YSR Sanchaara Pasu Aarogya Seva, or Mobile Ambulatory Veterinary Clinics (MAVC), in the state to improve the service delivery system and ensure that the veterinary services provided by the animal husbandry department are more easily accessible to the public.

- March 2022: Hacarus Inc. launched its ECG platform along with DS Pharma Animal Health. The device measures and analyzes the heart condition of dogs to aid in the early detection of cardiac disease, the second leading cause of death for canines.

Veterinary Services Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Various Diseases in Animals

- 4.2.2 Rising Adoption of Animals

- 4.2.3 Growing Expenditure on Animals/Pets

-

4.3 Market Restraints

- 4.3.1 Shortage of Skilled Personnel

- 4.3.2 Increasing Cost of Veterinary Services

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

-

5.1 By Service

- 5.1.1 Surgery

- 5.1.2 Diagnostic Tests and Imaging

- 5.1.3 Physical Health Monitoring

- 5.1.4 Other Services

-

5.2 By Animal Type

- 5.2.1 Companion Animal

- 5.2.2 Farm Animal

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 CVS Group PLC

- 6.1.2 Ethos Veterinary Health

- 6.1.3 Greencross Limited

- 6.1.4 Idexx laboratories

- 6.1.5 Mars Inc.

- 6.1.6 Armor Animal Health (Animart)

- 6.1.7 Kremer Veterinary Services

- 6.1.8 FirstVet AB

- 6.1.9 CityVet Inc.

- 6.1.10 Zoetis

- 6.1.11 Elanco

- 6.1.12 ELIAS Animal Health

- 6.1.13 Karyopharm Therapeutics, Inc.

- 6.1.14 Torigen Pharmaceuticals Inc.

- 6.1.15 Elekta

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape Covers - Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Veterinary Services Industry Segmentation

As per the scope of the report, veterinary services refer to all kinds of facilities, solutions, systems, and services targeted at animal health welfare, including hospitalization, dentistry, diagnostics, surgery, nursing, medication, medical devices, specialist referral, alternative therapies, and behavioral therapies performed by a veterinarian. The Veterinary Services Market is segmented by Service (Surgery, Diagnostic Tests and Imaging, Physical Health Monitoring, and Other Services), Animal Type (Companion Animal, and Farm Animal), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Service | Surgery | ||

| Diagnostic Tests and Imaging | |||

| Physical Health Monitoring | |||

| Other Services | |||

| By Animal Type | Companion Animal | ||

| Farm Animal | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Veterinary Services Market Research Faqs

How big is the Veterinary Services Market?

The Veterinary Services Market size is expected to reach USD 128.73 billion in 2025 and grow at a CAGR of 4.90% to reach USD 163.52 billion by 2030.

What is the current Veterinary Services Market size?

In 2025, the Veterinary Services Market size is expected to reach USD 128.73 billion.

Which is the fastest growing region in Veterinary Services Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Veterinary Services Market?

In 2025, the North America accounts for the largest market share in Veterinary Services Market.

What years does this Veterinary Services Market cover, and what was the market size in 2024?

In 2024, the Veterinary Services Market size was estimated at USD 122.42 billion. The report covers the Veterinary Services Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Veterinary Services Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Veterinary Services Industry Report

The veterinary services market is experiencing robust growth, fueled by heightened pet health awareness, an uptick in animal diseases, and an escalated demand for both medical and non-medical animal care. With companion animals leading the market due to increased pet adoption and advancements in veterinary services, surgery emerges as the dominant service segment, reflecting significant medical care needs. The Asia-Pacific region, characterized by a burgeoning pet population and improved economic status, is poised for remarkable growth, supported by government initiatives aiming to enhance animal health. Trends such as pet humanization and sustainable animal husbandry practices further propel market growth. Key market segments also encompass diagnostic tests, grooming, and vaccination services for both companion and food-producing animals. Despite the hurdles of high service costs and personnel shortages, the veterinary industry is set for advancement, driven by service innovations and expansions. Statistics for the Veterinary Services market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Veterinary Services analysis includes a market forecast outlook and historical overview. Get a sample of this industry analysis as a free report PDF download.