| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 51.61 Billion |

| Market Size (2030) | USD 74.36 Billion |

| CAGR (2025 - 2030) | 7.58 % |

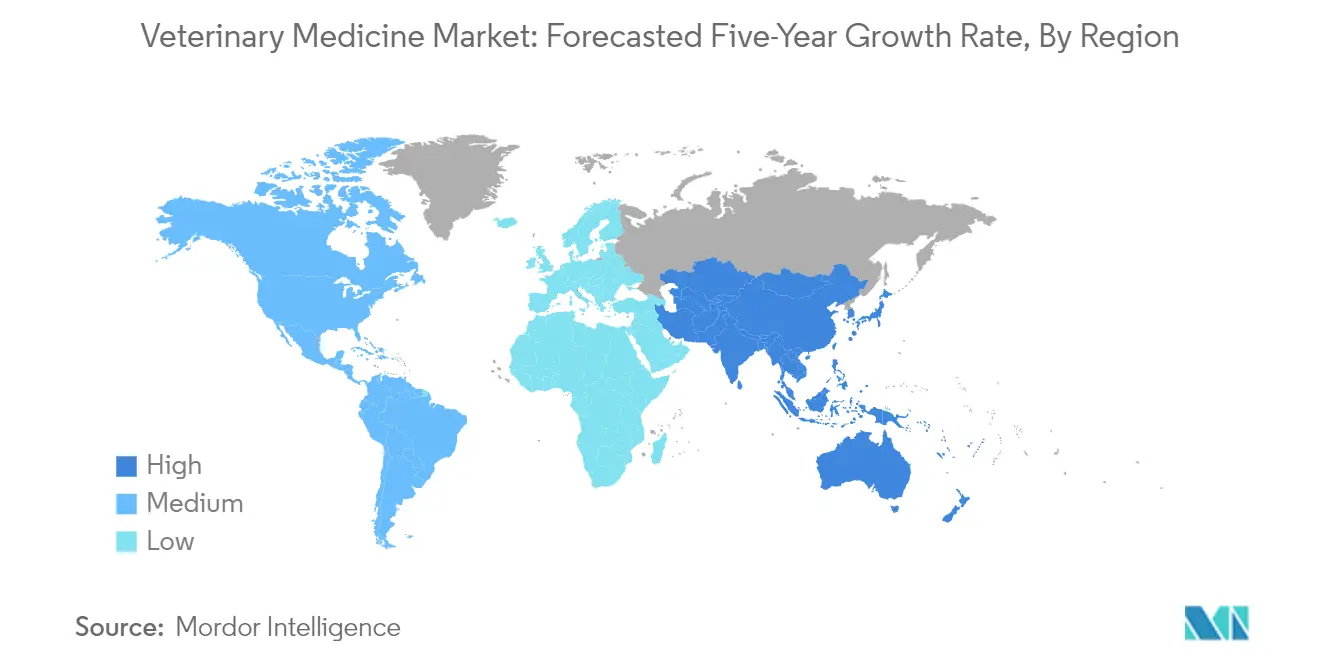

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

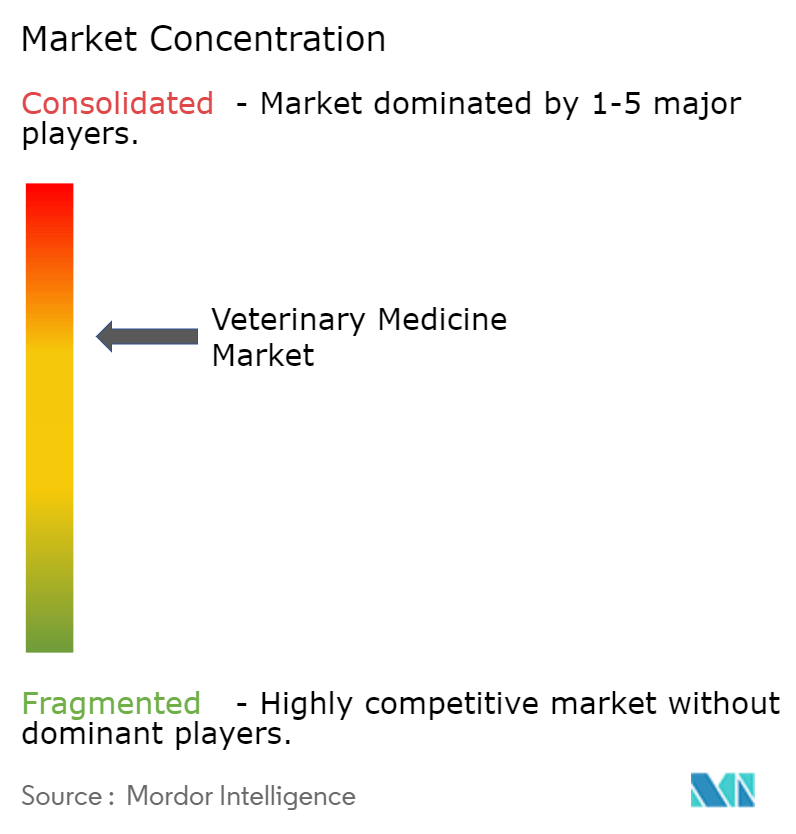

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Veterinary Medicine Market Analysis

The Veterinary Medicine Market size is estimated at USD 51.61 billion in 2025, and is expected to reach USD 74.36 billion by 2030, at a CAGR of 7.58% during the forecast period (2025-2030).

The veterinary medicine industry is experiencing significant transformation driven by technological advancements and changing animal healthcare needs. According to the United States Department of Agriculture (USDA) data from February 2022, the livestock population in the United States alone comprises approximately 91.9 million cattle and calves and 5.07 million sheep, highlighting the substantial scale of the veterinary market's potential. The industry is witnessing increased investment in research and development, particularly in areas such as precision medicine and targeted therapies for both companion and livestock animals. Major pharmaceutical companies are expanding their veterinary divisions through strategic acquisitions and partnerships, recognizing the growing importance of animal health in the global healthcare landscape.

The sector is seeing a notable shift toward preventive healthcare and wellness solutions for animals, moving beyond traditional treatment approaches. This evolution is particularly evident in the companion animal segment, where sophisticated diagnostic tools and personalized treatment plans are becoming increasingly common. The industry has also witnessed a surge in the development of innovative drug delivery systems and novel therapeutic approaches, with several new products receiving regulatory approvals in 2023. According to USDA data from May 2022, the identification of highly pathogenic avian influenza affecting approximately 37.96 million birds has accelerated the development of more effective diagnostic and treatment protocols in the veterinary medicine sector.

Market consolidation continues to reshape the competitive landscape, with several significant mergers and acquisitions occurring throughout 2023. For instance, in September 2023, major industry players completed strategic acquisitions to expand their product portfolios and geographical presence. These consolidations are driving innovation and creating more comprehensive animal health solutions, particularly in areas such as vaccines and specialized medications. The industry is also witnessing increased collaboration between pharmaceutical companies and research institutions to develop next-generation veterinary medicines.

The regulatory environment continues to evolve, with authorities implementing stricter guidelines for animal drug development and safety standards. This has led to an increased focus on quality control and documentation requirements for veterinary pharmaceutical industry manufacturers. The industry is also seeing a growing emphasis on sustainable practices and environmentally conscious production methods, with companies investing in green technologies and eco-friendly packaging solutions. These regulatory changes and sustainability initiatives are driving innovation in manufacturing processes and product formulations, leading to the development of more efficient and environmentally responsible veterinary medicines.

Veterinary Medicine Market Trends

Growing Burden of Chronic Disease Conditions in Animals, Coupled with the Increasing Adoption of Animals

The rising prevalence of chronic diseases in companion animals, particularly cancer and obesity, has become a significant concern driving the demand for animal medicine. Cancer affects dogs at nearly identical rates to humans, and according to ELIAS Animal Health's 2022 report, it has emerged as one of the leading causes of death in dogs, sometimes exceeding human rates. Additionally, approximately 75% of pet owners have expressed concerns about the health effects of obesity in their pets, highlighting the growing awareness of chronic health conditions affecting companion animals.

The substantial increase in pet adoption rates across developed regions has created a parallel demand for veterinary healthcare services and medicines. According to the European Pet Food Industry Association's (FEDIAF) 2022 annual report, Europe alone recorded approximately 72.7 million dogs in 2021, with continued growth expected. This trend is similarly reflected in North America, where the Canadian Animal Health Institute (CAHI) reported in 2022 that 60% of Canadian households own at least one dog or cat, with the cat population reaching 8.5 million and the dog population hitting 7.9 million. The combination of increasing pet ownership and rising awareness of animal health issues has led to greater investment in the veterinary medicines market, with annual routine visit expenditures reaching USD 242 for dogs and USD 178 for cats in 2021.

Understand The Key Trends Shaping This Market

Download PDF

Increase in Drug Preferences by Pet and Poultry Farm Owners

The growing sophistication of veterinary drugs and increased awareness among pet owners have led to a significant shift in preferences toward advanced therapeutic options and preventive care medications. Pet owners are increasingly seeking specialized treatments and innovative drug formulations for various conditions, from chronic diseases to acute infections. This trend is evidenced by the continuous stream of new drug approvals and innovations in the market, such as new cancer treatments, obesity management medications, and advanced parasiticides for both companion animals and livestock.

The poultry sector has witnessed a parallel trend in drug preferences, with farm owners increasingly adopting preventive medication strategies and specialized feed additives to maintain flock health and productivity. The focus has shifted toward more effective and targeted treatments, particularly in disease prevention and growth optimization. This evolution in drug preferences is supported by regulatory bodies' continued approval of new veterinary drugs, such as the FDA's approval of Pennitracin MD 50G in 2022 for preventing mortality caused by necrotic enteritis in broiler and replacement chickens, demonstrating the industry's response to changing market demands and treatment preferences.

Increased Demand for Meat and Animal-Based Products in Agriculture and Human Healthcare

The growing global demand for meat and animal-based products has created a substantial need for animal medicine to maintain animal health and ensure productive livestock operations. This trend extends beyond basic animal health maintenance to encompass the quality and safety of animal-derived products used in both food production and healthcare applications. The increasing consumption of meat products has led to a greater emphasis on preventive healthcare measures and disease management in livestock, driving the demand for various veterinary medications, vaccines, and feed additives.

The healthcare sector's reliance on animal-derived products has emerged as another significant driver for the veterinary medicines market. Various critical healthcare products, including vaccines, therapeutic proteins, and other pharmaceutical ingredients, depend on healthy livestock populations. This interconnection between animal health and human healthcare has led to increased investment in the veterinary therapeutics market research and development, particularly in areas focused on maintaining the health of animals used for pharmaceutical and healthcare product development. The trend has been further reinforced by stringent quality requirements for animal-derived products used in human healthcare applications, necessitating comprehensive veterinary care protocols and specialized medications.

Segment Analysis: By Product

Drugs Segment in Veterinary Medicine Market

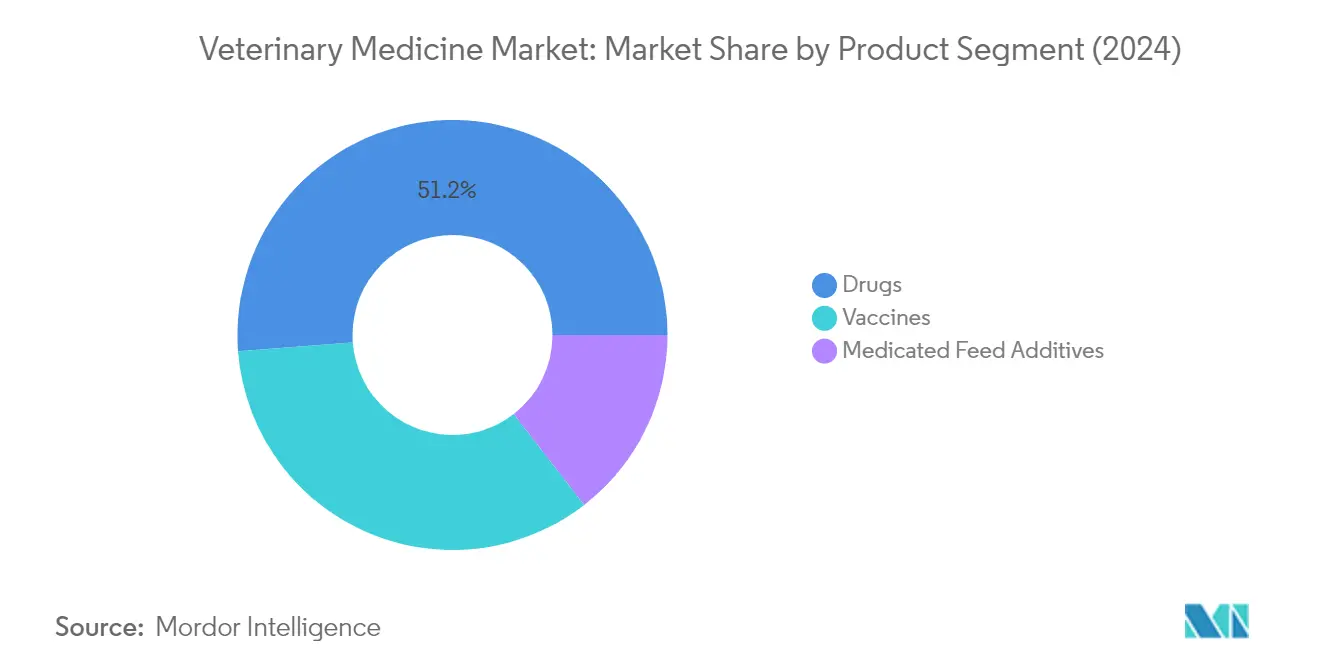

The veterinary drug segment dominates the veterinary medicine market, accounting for approximately 51% of the total market share in 2024. This significant market position is driven by the increasing prevalence of chronic diseases in animals, particularly in companion pets, coupled with the rising adoption of animals globally. The segment encompasses various therapeutic categories, including anti-infectives, anti-inflammatory drugs, parasiticides, and other specialized medications. The robust growth is further supported by continuous product innovations and approvals, particularly in areas like cancer treatment, pain management, and chronic disease management for both companion and livestock animals. Major pharmaceutical companies are actively expanding their drug portfolios through research and development initiatives, focusing on developing novel therapeutic solutions for emerging animal health challenges.

Vaccines Segment in Veterinary Medicine Market

The veterinary medicines vaccines market is emerging as the fastest-growing category in the veterinary medicine market, projected to grow at approximately 8% CAGR from 2024 to 2029. This remarkable growth is primarily attributed to the increasing focus on preventive healthcare measures in both companion animals and livestock. The segment's expansion is driven by technological advancements in vaccine development, including the introduction of novel recombinant vaccines and DNA vaccines. The rising awareness about zoonotic diseases and the implementation of mandatory vaccination programs in many countries have further accelerated the demand for animal vaccines. Additionally, the development of innovative delivery systems and the increasing investment in research and development activities by major market players are contributing to the segment's rapid growth trajectory.

Remaining Segments in Product Segmentation

The medicated feed additives segment represents a crucial component of the veterinary medicine market, playing a vital role in livestock health management and production efficiency. This segment includes amino acids, antibiotics, and other medicated feed additives that are essential for maintaining animal health and promoting growth. The segment's significance is particularly evident in the livestock industry, where these products are crucial for disease prevention and nutritional supplementation. The increasing focus on reducing antibiotic usage in animal feed has led to the development of alternative feed additives, driving innovation in this segment. Additionally, the growing demand for protein-rich animal products and the emphasis on animal nutrition have created new opportunities for medicated feed additive manufacturers.

Segment Analysis: By Animal Type

Companion Animals Segment in Veterinary Medicine Market

The companion animal pharmaceuticals market dominates the veterinary medicine market, accounting for approximately 52% of the total market share in 2024. This significant market position is primarily driven by the increasing adoption of pets globally, particularly dogs and cats, coupled with rising expenditure on pet healthcare. The segment's growth is further supported by the expansion of pet insurance coverage and the increasing awareness about animal health among pet owners. The rising prevalence of chronic diseases in companion animals, such as cancer, arthritis, and other age-related conditions, has led to increased demand for advanced veterinary medicines and treatments. Additionally, the growing trend of the humanization of pets, where animals are considered family members, has resulted in a higher willingness among pet owners to invest in quality healthcare products and preventive medicines for their pets.

Livestock Animals Segment in Veterinary Medicine Market

The livestock animals segment is experiencing the fastest growth in the veterinary medicine market, with a projected growth rate of approximately 8% from 2024 to 2029. This robust growth is primarily attributed to the increasing demand for animal-derived food products and the rising focus on food security and safety. The segment is witnessing significant advancements in disease prevention and treatment solutions, particularly for cattle, poultry, and swine. The growing awareness about zoonotic diseases and their prevention has led to increased investment in livestock healthcare. Furthermore, the implementation of stringent regulations regarding the use of antibiotics in livestock and the rising adoption of preventive healthcare measures are driving the demand for innovative veterinary medicines in this segment. The segment is also benefiting from technological advancements in animal health monitoring and disease diagnosis, leading to more effective treatment solutions.

Segment Analysis: By Mode of Administration

Oral Segment in Veterinary Medicine Market

The oral mode of administration continues to dominate the veterinary formulation market, holding approximately 32% of the market share in 2024. This significant market position is primarily driven by the increasing preference for oral medications among pet owners and veterinarians due to their ease of administration and better compliance rates. Oral medications, including tablets, capsules, solutions, and suspensions, are particularly popular in companion animal treatment, where they can be easily administered through food or treats. The segment's growth is further supported by technological advancements in drug formulation that have improved the palatability and bioavailability of oral medications. Additionally, the expanding portfolio of oral medications for various conditions, from parasitic infections to chronic diseases, has strengthened this segment's market position. The development of innovative drug delivery systems and taste-masking technologies has also contributed to the increased adoption of oral medications in veterinary practice.

Intravenous Segment in Veterinary Medicine Market

The intravenous administration segment is emerging as the fastest-growing segment in the veterinary medicine market, with a projected growth rate of approximately 9% from 2024 to 2029. This remarkable growth is attributed to the increasing adoption of advanced therapeutic procedures in veterinary clinics and hospitals, particularly for emergency treatments and critical care situations. The segment's expansion is further driven by technological advancements in drug delivery systems and the rising demand for precise medication administration in complex veterinary procedures. The growing sophistication of veterinary healthcare facilities, coupled with the increasing availability of specialized intravenous medications, has significantly contributed to this segment's rapid growth. Additionally, the rising prevalence of chronic diseases in animals requiring immediate and effective treatment through intravenous administration has boosted the segment's expansion. The segment is also benefiting from increased investments in veterinary healthcare infrastructure and the growing number of skilled veterinary professionals capable of administering intravenous medications.

Remaining Segments in Mode of Administration

The veterinary medicine market's other administration routes, including intramuscular, subcutaneous, topical, and other modes, each play crucial roles in animal healthcare delivery. The subcutaneous route is particularly important for vaccines and long-acting medications, while intramuscular administration is preferred for certain antibiotics and pain medications. Topical administration has gained significance in treating skin conditions and external parasites, offering convenient application methods for pet owners. These segments collectively provide veterinarians with diverse options for tailoring treatment approaches to specific conditions and animal species. The choice of administration route often depends on factors such as the type of medication, the condition being treated, the animal's size and species, and the desired onset and duration of action. The continuous development of new drug formulations and delivery systems across these segments ensures comprehensive treatment options for various veterinary conditions.

Segment Analysis: By Type

Injectables Segment in Veterinary Medicine Market

The injectables segment has emerged as both the dominant and fastest-growing segment in the veterinary biologics market, commanding approximately 45% of the market share in 2024. This substantial market position is attributed to the high efficacy and rapid onset of action associated with injectable medications in both companion and livestock animals. The segment's growth is driven by technological advancements in drug delivery systems, increasing adoption of long-acting injectable formulations, and the rising prevalence of chronic diseases in animals requiring injectable treatments. The development of novel injectable vaccines, antibiotics, and pain management solutions has further strengthened this segment's position. Additionally, the increasing preference for injectable medications in emergency veterinary care and the growing demand for preventive healthcare measures through vaccination programs have contributed to its market leadership. The segment has also benefited from the expanding livestock industry and the rising need for efficient drug administration in large-scale animal farming operations.

Remaining Segments in Veterinary Medicine Market by Type

The veterinary medicine market encompasses several other significant segments, including oral tablets, oral powders, oral solutions, spot-on formulations, and other delivery formats. Oral tablets represent a substantial portion of the market, offering convenience in administration, particularly for companion animals. Oral powders have gained traction in the livestock sector due to their ease of incorporation into animal feed and cost-effectiveness in treating large herds. Spot-on formulations have become increasingly popular in the companion animal segment, especially for parasitic treatments, offering pet owners a simple and effective application method. Oral solutions provide versatility in dosing and are particularly valuable for young animals and those requiring precise medication amounts. The remaining formats, including medicated feed additives and topical preparations, continue to serve specific therapeutic needs across various animal species and conditions. Each of these segments plays a crucial role in providing veterinarians and animal owners with diverse options for maintaining animal health and treating various conditions effectively.

Veterinary Medicine Market Geography Segment Analysis

Veterinary Medicine Market in North America

North America represents a dominant force in the global veterinary medicine market, characterized by advanced healthcare infrastructure and high pet ownership rates. The region encompasses key markets including the United States, Canada, and Mexico, each contributing uniquely to the regional landscape. The presence of major veterinary pharmaceutical companies, extensive research and development activities, and stringent regulatory frameworks has positioned North America at the forefront of veterinary medicine innovation. The region's growth is further supported by increasing pet adoption rates, rising awareness about animal health, and growing expenditure on veterinary care.

Veterinary Medicine Market in the United States

The United States leads the North American veterinary market with approximately 84% market share in the region. The country's dominance is attributed to its robust healthcare infrastructure, high pet ownership rates, and presence of leading veterinary medicine companies. The American market is characterized by sophisticated veterinary facilities, advanced treatment options, and comprehensive pet insurance coverage. The increasing prevalence of chronic diseases in companion animals, coupled with rising pet adoption rates, continues to drive market growth. The country's strong regulatory framework, overseen by the FDA, ensures high-quality standards in veterinary medicines while promoting innovation in animal healthcare solutions.

Veterinary Medicine Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 8% from 2024-2029. The Canadian market is witnessing rapid expansion due to increasing pet ownership, growing awareness about animal health, and rising investments in veterinary healthcare infrastructure. The country's veterinary medicine sector benefits from strong government support, comprehensive healthcare policies, and an increasing focus on preventive care for animals. Canadian veterinary practices are increasingly adopting advanced technologies and treatment methods, while the market sees a continuous introduction of innovative veterinary products and services. The growing emphasis on animal welfare and rising disposable income are further accelerating market growth.

Veterinary Medicine Market in Europe

Europe represents a significant market for veterinary medicines, characterized by stringent regulations, advanced research capabilities, and high standards of animal healthcare. The region encompasses major markets including Germany, the United Kingdom, France, Italy, and Spain, each contributing significantly to the overall market landscape. The European market benefits from well-established healthcare infrastructure, increasing pet ownership, and growing awareness about animal health. The presence of leading veterinary pharmaceutical companies and research institutions further strengthens the region's position in veterinary medicine development and innovation.

Veterinary Medicine Market in Germany

Germany maintains its position as the largest veterinary medicine market in Europe, commanding approximately 26% of the regional market share. The country's leadership is supported by its advanced healthcare infrastructure, strong research and development capabilities, and high pet ownership rates. German veterinary practices are known for adopting innovative treatment approaches and maintaining high standards of animal care. The market benefits from the presence of major veterinary drug manufacturers, robust distribution networks, and increasing investments in veterinary healthcare development. The country's comprehensive pet insurance coverage and growing focus on preventive care further drive market growth.

Veterinary Medicine Market in France

France emerges as the fastest-growing market in Europe, with a projected growth rate of approximately 9% from 2024-2029. The French veterinary medicine market is experiencing rapid expansion driven by increasing pet adoption rates and growing awareness about animal health. The country's strong focus on research and development in veterinary medicine, coupled with supportive government policies, creates a favorable environment for market growth. French veterinary practices are increasingly incorporating advanced technologies and treatment methods, while the market witnesses a continuous introduction of innovative veterinary products. The rising emphasis on animal welfare and increasing pet healthcare expenditure further accelerate market development.

Veterinary Medicine Market in Asia-Pacific

The Asia-Pacific region represents a rapidly evolving market for veterinary medicines, characterized by increasing pet ownership, a growing livestock population, and rising awareness about animal health. The region encompasses diverse markets including China, Japan, India, Australia, and South Korea, each contributing uniquely to the market dynamics. The veterinary medicine sector in Asia-Pacific is witnessing significant transformation driven by modernizing healthcare infrastructure, increasing disposable income, and a growing focus on animal welfare. The region's market is further strengthened by government initiatives supporting animal healthcare and rising investments in veterinary research and development.

Veterinary Medicine Market in China

China stands as the largest veterinary medicine market in the Asia-Pacific region, driven by its extensive livestock population and growing pet ownership trends. The Chinese market is characterized by the rapid modernization of veterinary healthcare facilities and increasing adoption of advanced treatment methods. The country's veterinary sector benefits from strong government support, growing investments in research and development, and rising awareness about animal health. The market shows particular strength in both companion animal and livestock segments, supported by improving healthcare infrastructure and expanding distribution networks.

Veterinary Medicine Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, driven by increasing pet adoption rates and growing awareness about animal healthcare. The Indian veterinary medicine market is experiencing rapid transformation with modernizing healthcare infrastructure and rising investments in animal health. The country's large livestock population and growing companion animal segment create diverse opportunities for market expansion. The market benefits from government initiatives supporting animal healthcare, increasing private sector investments, and a rising focus on preventive care for animals. The India veterinary medicine manufacturing market is poised to contribute significantly to this growth.

Veterinary Medicine Market in the Middle East & Africa

The Middle East & Africa region presents a growing market for veterinary medicines, characterized by increasing awareness about animal health and rising investments in veterinary healthcare infrastructure. The region, including key markets such as GCC countries and South Africa, shows significant potential for growth in both companion animal and livestock segments. Within this region, GCC emerges as the largest market, while South Africa shows the fastest growth potential. The market is driven by modernizing healthcare facilities, government initiatives supporting animal health, and increasing pet ownership trends, particularly in urban areas. The region's focus on livestock health and growing investments in veterinary research contribute to market expansion.

Veterinary Medicine Market in South America

South America represents an emerging market for veterinary medicines, characterized by its large livestock population and growing pet ownership trends. The region, with key markets including Brazil and Argentina, shows significant potential for growth in both companion animal and livestock segments. Brazil emerges as the largest and fastest-growing market in the region, driven by its extensive livestock industry and increasing pet adoption rates. The market benefits from improving healthcare infrastructure, rising awareness about animal health, and growing investments in veterinary services. Government initiatives supporting animal healthcare and an increasing focus on preventive care further contribute to market development across the region.

Get Analysis on Important Geographic Markets

Download PDF

Veterinary Medicine Industry Overview

Top Companies in Veterinary Medicine Market

The veterinary medicine companies market features prominent players like Zoetis, Boehringer Ingelheim, Merck & Co., and Elanco, leading the industry through continuous innovation and strategic expansion. These veterinary pharmaceutical companies are heavily investing in research and development to introduce novel therapeutic solutions, particularly in areas like companion animal health and livestock disease prevention. The industry demonstrates strong product development initiatives, with companies focusing on both chemical and biological solutions while expanding their geographical presence through strategic partnerships and acquisitions. Market leaders are increasingly adopting digital technologies and innovative delivery systems to enhance their product efficacy and market reach. Companies are also strengthening their distribution networks and technical support services to maintain competitive advantages and market position.

Consolidated Market with Strong Regional Players

The veterinary medicine market exhibits a relatively consolidated structure at the global level, with major pharmaceutical conglomerates holding significant market share through their animal health divisions. These large players leverage their extensive research capabilities, global distribution networks, and strong financial resources to maintain their market positions. However, the market also supports numerous regional and specialized players who have carved out strong positions in specific therapeutic areas or geographical regions. The industry has witnessed considerable merger and acquisition activity, with larger companies acquiring smaller innovative firms to expand their product portfolios and geographical reach.

The competitive dynamics vary significantly across regions, with developed markets showing higher consolidation and emerging markets featuring a mix of global and local players. Market leaders are increasingly focusing on strategic partnerships with research institutions and biotechnology companies to enhance their innovation capabilities. The industry also sees active collaboration between companies for product development and distribution, particularly in emerging markets where local expertise and networks are crucial for market penetration.

Innovation and Market Access Drive Success

Success in the veterinary medicine market increasingly depends on companies' ability to innovate while maintaining cost-effectiveness and ensuring broad market access. Incumbent veterinary drug companies are focusing on developing comprehensive product portfolios that address both companion animal and livestock segments, while also investing in preventive solutions and digital health technologies. Companies are strengthening their research and development capabilities while simultaneously building robust distribution networks and technical support services to maintain their competitive edge. The ability to navigate regulatory requirements across different regions while maintaining product quality and safety standards has become a crucial success factor.

For emerging players and contenders, success lies in identifying and focusing on specific market niches or underserved geographical regions while building strong relationships with veterinarians and animal health professionals. Companies need to balance their product innovation efforts with market-specific requirements and pricing considerations, particularly in emerging markets where cost sensitivity is high. The increasing focus on animal welfare and sustainable farming practices presents opportunities for companies to differentiate themselves through specialized solutions. Building strong relationships with key stakeholders, including veterinary professionals, research institutions, and regulatory bodies, remains crucial for long-term success in this market. Additionally, a generic veterinary medicine company can leverage cost advantages to penetrate price-sensitive markets effectively.

Veterinary Medicine Market Leaders

-

Zoetis

-

Merck & Co., Inc

-

Elanco

-

Ceva

-

Boehringer Ingelheim

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Veterinary Medicine Market News

- September 2024: Elanco Animal Health Incorporated received approval from the U.S. Food and Drug Administration (FDA) for Zenrelia, a once-daily oral JAK inhibitor for control of pruritus (itching) associated with allergic dermatitis and control of atopic dermatitis in dogs at least 12 months of age.

- September 2024: Merck Animal Health received marketing authorization in the European Union from the European Medicines Agency for PORCILIS PCV M Hyo ID, a ready-to-use intradermal vaccine that offers protection against two of the most common swine pathogens: Porcine Circovirus Type 2 (PCV2) and Mycoplasma hyopneumoniae (M. hyo).

Veterinary Medicine Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Growing Burden of Chronic Disease Conditions in Animals, Coupled with the Increasing Adoption of Animals

- 4.2.2 Increase in Drug Preferences by Pet and Poultry Farm Owners

- 4.2.3 Increased Demand for Meat and Animal-based Products in Agriculture and Human Healthcare

-

4.3 Market Restraints

- 4.3.1 High Costs Associated with Animal Healthcare

- 4.3.2 Lack of Awareness about Animal Health in the Emerging Nations

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

-

5.1 By Product Type

- 5.1.1 Drugs

- 5.1.1.1 Anti-infectives

- 5.1.1.2 Anti-inflammatory

- 5.1.1.3 Parasiticides

- 5.1.1.4 Other Drugs

- 5.1.2 Vaccines

- 5.1.2.1 Inactive Vaccines

- 5.1.2.2 Attenuated Vaccines

- 5.1.2.3 Recombinant Vaccines

- 5.1.2.4 Other Vaccines

- 5.1.3 Medicated Feed Additives

- 5.1.3.1 Aminoacids

- 5.1.3.2 Antibiotics

- 5.1.3.3 Other Medicated Feed Additives

-

5.2 By Animal Type

- 5.2.1 Companion Animals

- 5.2.1.1 Dogs

- 5.2.1.2 Cats

- 5.2.1.3 Other Companion Animals

- 5.2.2 Livestock Animals

- 5.2.2.1 Cattle

- 5.2.2.2 Poultry

- 5.2.2.3 Swine

- 5.2.2.4 Sheep

- 5.2.2.5 Other Livestock Animals

-

5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Boehringer Ingelheim

- 6.1.2 Ceva Animal Health LLC

- 6.1.3 China Animal Husbandry Co. Ltd

- 6.1.4 Dechra Pharmaceuticals PLC

- 6.1.5 Elanco

- 6.1.6 Merck & Co. Inc.

- 6.1.7 Neogen Corporation

- 6.1.8 Phibro Animal Health Corporation

- 6.1.9 Sanofi SA

- 6.1.10 Vetoquinol SA

- 6.1.11 Virbac

- 6.1.12 Zoetis

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Veterinary Medicine Industry Segmentation

As per the scope of the report, veterinary drugs are used by veterinary professionals to treat diseases and injuries and help to promote growth in animals. These are majorly used to cure diseases and prevent the spread of infectious diseases among animals. These drugs indirectly benefit human healthcare by restricting the spread of infectious diseases from animals to humans.

The market is segmented by product type, animal type, and geography. By Product Type, the market is segmented into drugs, vaccines, and medicated feed additives. By drugs, the market is segmented into anti-infectives, anti-inflammatory, parasiticides, and other drugs. By vaccines, the market is segmented into inactive vaccines, attenuated vaccines, recombinant vaccines, and other vaccines. By medicated feed additives, the market is segmented into amino acids, antibiotics, and other medicated feed additives. By animal type, the market is segmented into companion animals and livestock animals. By companion animals, the market is segmented into dogs, cats, and other companion animals. By livestock animals, the market is segmented into cattle, poultry, swine, sheep, and other livestock animals. By geography, the market is North America, Europe, Asia-Pacific, Middle East and Africa, and South America.

The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| By Product Type | Drugs | Anti-infectives | |

| Anti-inflammatory | |||

| Parasiticides | |||

| Other Drugs | |||

| Vaccines | Inactive Vaccines | ||

| Attenuated Vaccines | |||

| Recombinant Vaccines | |||

| Other Vaccines | |||

| Medicated Feed Additives | Aminoacids | ||

| Antibiotics | |||

| Other Medicated Feed Additives | |||

| By Animal Type | Companion Animals | Dogs | |

| Cats | |||

| Other Companion Animals | |||

| Livestock Animals | Cattle | ||

| Poultry | |||

| Swine | |||

| Sheep | |||

| Other Livestock Animals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Veterinary Medicine Market Research FAQs

How big is the Veterinary Medicine Market?

The Veterinary Medicine Market size is expected to reach USD 51.61 billion in 2025 and grow at a CAGR of 7.58% to reach USD 74.36 billion by 2030.

What is the current Veterinary Medicine Market size?

In 2025, the Veterinary Medicine Market size is expected to reach USD 51.61 billion.

Who are the key players in Veterinary Medicine Market?

Zoetis, Merck & Co., Inc, Elanco, Ceva and Boehringer Ingelheim are the major companies operating in the Veterinary Medicine Market.

Which is the fastest growing region in Veterinary Medicine Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Veterinary Medicine Market?

In 2025, the North America accounts for the largest market share in Veterinary Medicine Market.

What years does this Veterinary Medicine Market cover, and what was the market size in 2024?

In 2024, the Veterinary Medicine Market size was estimated at USD 47.70 billion. The report covers the Veterinary Medicine Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Veterinary Medicine Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Veterinary Medicine Industry Report

Mordor Intelligence provides a comprehensive analysis of the veterinary medicine market, drawing on decades of expertise in healthcare industry research. Our extensive coverage includes the entire ecosystem of veterinary pharmaceutical companies and veterinary drug manufacturers. We offer detailed insights into manufacturing processes, supply chains, and market dynamics. The report thoroughly examines veterinary medicine companies in global markets, including both established veterinary drug companies and emerging players in the veterinary therapeutics market.

Stakeholders gain valuable insights through our detailed analysis of veterinary drug suppliers and manufacturing trends. This information is available in an easy-to-download report PDF format. The research covers crucial segments such as companion animal pharmaceuticals, farm animal drugs, and veterinary biologics. It offers strategic intelligence for decision-makers. Our report provides actionable data on veterinary formulation developments, regulatory landscapes, and emerging opportunities in veterinary medicine manufacturing across key regions. This enables businesses to make informed strategic decisions in this dynamic market environment.