| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Market Size (2025) | USD 8.70 Billion |

| Market Size (2030) | USD 13.74 Billion |

| CAGR (2025 - 2030) | 9.57 % |

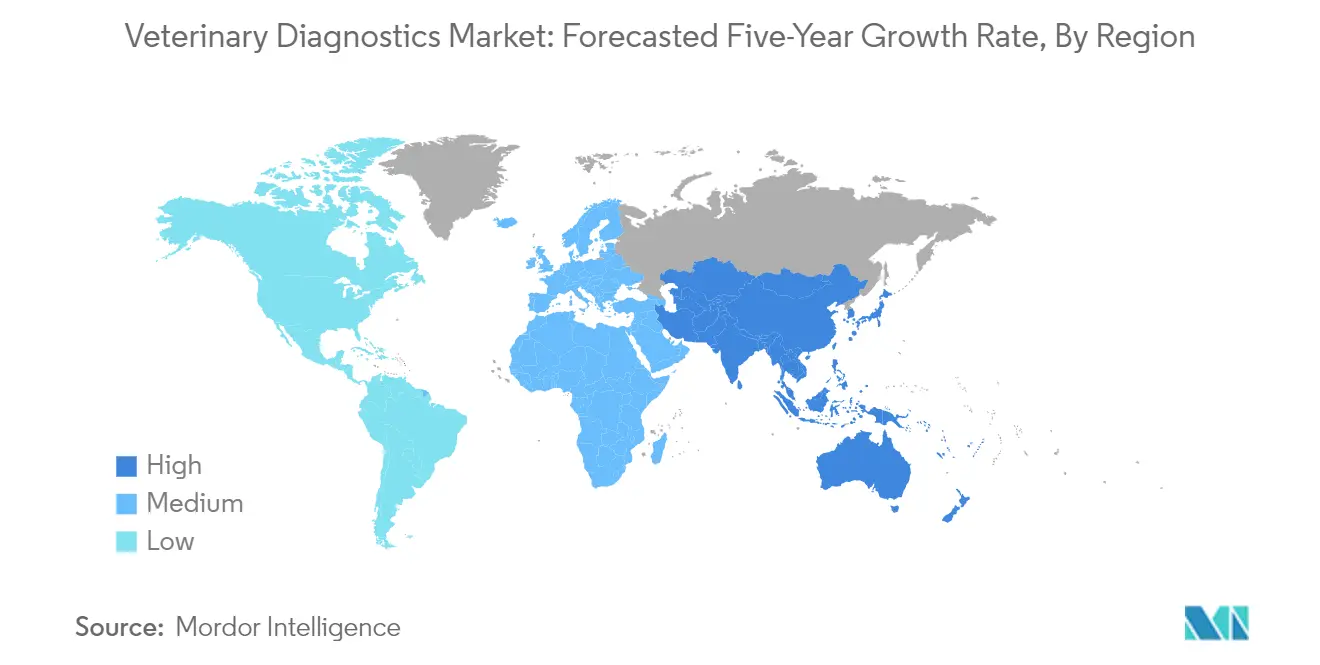

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Veterinary Diagnostics Market Analysis

The Veterinary Diagnostics Market size is estimated at USD 8.70 billion in 2025, and is expected to reach USD 13.74 billion by 2030, at a CAGR of 9.57% during the forecast period (2025-2030).

Location Flexibility: The New Normal in Veterinary Diagnostics

The veterinary diagnostics field is moving beyond clinic walls as services expand into mobile and virtual settings. This change comes from both new regulations and customers wanting more convenient care options. In 2023, Arizona and California changed their laws to let veterinarians establish professional relationships with patients remotely, removing old requirements for in-person visits. The market has responded well to these changes, with mobile veterinary practices earning USD 1,200,000 (median) in 2022—four times more than the USD 300,000 they earned just a year before. This shows a major shift in how and where animals receive diagnostic services. For companies in this industry, the takeaway is clear: veterinary diagnostic devices need to work well in mobile and remote settings. Businesses that design their products to be portable, durable in the field, and operable from a distance will gain market share. Meanwhile, those who only focus on traditional clinic settings may struggle as the industry moves toward more flexible service models that bring diagnostics to where animals and their owners are rather than the other way around.

Data Integration: The Cloud's Impact on Veterinary Care

Animal health diagnostics is improving through cloud technology that changes how health information moves through the veterinary care system. This digital approach is catching on quickly, with cloud-based Practice Information Management Systems reaching 35% adoption among veterinary practices in 2023, with more growth expected. This creates a connected environment where test results, patient records, and treatment outcomes can be easily accessed across different locations and platforms. For veterinary professionals, this means more than just convenience; better data integration allows them to spot patterns, analyze information, and diagnose problems in ways that weren't possible with older, disconnected systems. Forward-thinking veterinary diagnostic companies are using this connectivity to build smarter systems that make diagnoses more accurate, faster, and personalized for each animal. The message for businesses is clear: diagnostic tools that don't work well with cloud systems risk becoming outdated in today's connected veterinary world. The most successful companies will be those creating diagnostic solutions that both contribute data to and benefit from the growing network of veterinary information, adding value through connection rather than isolation.

Pet Owner Influence: Reshaping Diagnostic Priorities

The veterinary molecular diagnostics field is changing as pet owners take a more active role in healthcare decisions, influencing how diagnostic services are created and delivered. This trend is supported by research, with an American Society for the Prevention of Cruelty to Animals (ASPCA) survey finding that 69% of pet owners want to use remote care options when available. This consumer-driven change fits with the broader trend of treating pets as family members who deserve quality, convenient healthcare. For veterinary infectious disease diagnostics providers, this means success now depends on creating solutions that work for both veterinarians and pet owners who expect easy access and clear information. Companies are responding with innovations like consumer-friendly testing approaches, easier-to-understand test results, and educational tools that help pet owners make sense of diagnostic findings. Leading businesses are building systems with interfaces that work for both veterinary professionals and concerned pet parents. The conclusion for companies in this market is straightforward: companion animal diagnostics is no longer just a business-to-business service. Companies that successfully balance professional-grade accuracy with consumer-friendly accessibility will gain stronger market positions as pet owners continue to take more active roles in their animals' healthcare.

Veterinary Diagnostics Market Trends

The Pet Boom: Dollars Follow Devotion

The evolution of pets from backyard companions to full-fledged family members continues to fuel the veterinary diagnostics market. Household pet ownership in the United States grew remarkably from 56% in 1998 to 66% by 2023, creating a substantial base of animals requiring routine and specialized healthcare services. This shift isn't merely about more pets—it's about deeper relationships with those pets, translating directly into greater willingness to invest in their wellbeing. Pet industry expenditure in the US jumped from USD 90.5 billion in 2018 to USD 136.8 billion in 2022, representing growth of over 51%. For diagnostic providers, this spending surge creates opportunities to introduce more sophisticated testing options as pet owners increasingly approach animal healthcare decisions with human-grade expectations.

Perhaps most telling is the efficiency revolution happening within animal health diagnostics practices. In 2022, veterinary practices in the United States increased their revenue by 5.2% despite experiencing a 3.1% decrease in actual visits. This counterintuitive trend reveals how the companion animal diagnostics market is shifting toward higher-value services, with diagnostics playing a central role. Rather than depending solely on patient volume, clinics now leverage advanced diagnostics to deliver more comprehensive care per visit. Companies developing user-friendly, in-clinic diagnostic platforms stand to benefit most from this trend, particularly those targeting chronic condition monitoring and preventative screening. Forward-thinking providers are reengineering their service models around diagnostic capabilities that enable precision veterinary medicine, where treatment plans become as individualized for pets as they've become for people.

Crossing Species Barriers: The Zoonotic Imperative

As human and animal populations increasingly overlap, the veterinary infectious disease diagnostics market faces mounting pressure to address diseases that move between species. The stakes couldn't be higher—up to 40,000 people die from leishmania each year, with human cases directly correlated with parasite prevalence in dogs. This sobering reality has transformed animal disease detection from a veterinary concern into a critical public health priority. The animal disease diagnostic market now operates at the intersection of multiple healthcare domains, with diagnostic technologies serving as essential early warning systems. Surveillance programs increasingly depend on rapid, field-deployable diagnostic solutions that can identify potential outbreaks before they cross the species barrier.

This zoonotic awareness has particularly energized the veterinary molecular diagnostics market, where technologies originally developed for human medicine are being adapted for animal applications. The One Health approach—recognizing that human health, animal health, and environmental health are inextricably linked—has become more than philosophy; it's now driving diagnostic innovation. Multi-pathogen screening panels, which can simultaneously test for numerous disease agents from a single sample, represent the future of efficient disease surveillance. Organizations investing in diagnostic technologies that bridge the gap between human and animal testing platforms position themselves advantageously in both markets. As climate change expands the range of disease vectors, diagnostics that can quickly adapt to emerging pathogens will become essential tools in protecting both animal and human populations.

Risk Mitigation: The Insurance-Diagnostics Partnership

The growing alignment between pet insurance providers and veterinary diagnostic companies is reshaping how animal healthcare is delivered and financed. Insurance companies, recognizing that early detection reduces long-term claims, increasingly incentivize preventative diagnostic screening through premium structures and coverage terms. This symbiotic relationship elevates diagnostic testing from reactive problem-solving to proactive healthcare management—creating stable, recurring revenue streams for diagnostic providers. In a sector still struggling with veterinarian availability, with Mars Veterinary Health estimating a deficit of 15,000 veterinarians in the United States by 2030, insurer-backed diagnostic protocols help maximize the impact of limited professional resources.

The veterinary diagnostic market is further benefiting from pharmaceutical companies seeking to secure their position in the animal health ecosystem through strategic investments in diagnostic capabilities. These investments come at a critical time—according to the American Veterinary Medical Association, more than 40% of practitioners who graduated in the last 10 years are considering leaving the profession, citing mental health and work-life balance concerns. Pharmaceutical companies are responding by developing integrated animal health diagnosis market solutions that combine therapeutic products with diagnostic tools, creating more comprehensive disease management platforms. The most successful diagnostic technologies address this workforce challenge directly, emphasizing ease-of-use and interpretation support. Equipment manufacturers in the veterinary diagnostic equipment market are increasingly focusing on middleware and decision-support systems that extend the capabilities of existing staff, allowing veterinary practices to maintain quality care despite staffing challenges.

Segment Analysis: By Product Type

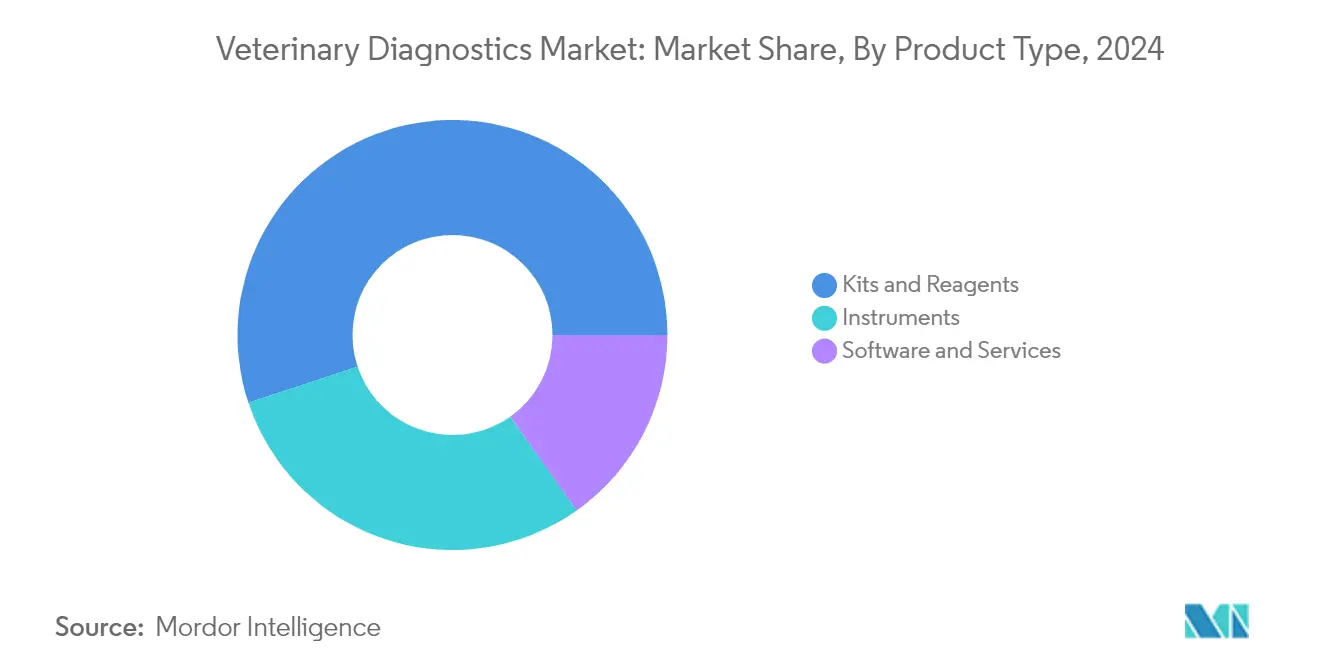

Kits and Reagents: The Backbone of Veterinary Diagnostics

Kits and reagents continue to dominate the veterinary diagnostics market with a substantial 55.1% market share, establishing themselves as the foundation of modern animal disease detection. This dominance stems from their versatility, cost-efficiency, and crucial role in routine testing procedures across both clinical and field settings. Practitioners increasingly depend on ready-to-use diagnostic kits to address the rising prevalence of parasitic infections—a concern highlighted by studies showing 20.7% of dogs in the United States parks testing positive for parasites. For manufacturers and suppliers, this commanding market position signals a need to focus on developing specialized, easy-to-use kits that address the most common testing needs while reducing technical complexity. The strategic imperative for stakeholders is clear: expanding product lines to cover emerging diseases while simultaneously enhancing the accuracy and user-friendliness of existing kits will be essential to maintaining relevance in this competitive segment.

Software and Services: Digitizing Diagnostic Intelligence

The software and services segment has emerged as the fastest-growing component within the veterinary diagnostic market, advancing at an impressive 12.5% annual growth rate. This acceleration reflects the industry's shift toward integrated digital solutions that enhance diagnostic accuracy, streamline workflows, and enable remote consultation capabilities. The demand for sophisticated data management systems is particularly evident as veterinary practices manage growing volumes of diagnostic information for the world's estimated billion-plus pets. For forward-thinking industry participants, this rapid growth trajectory presents a clear directive: investment in cloud-based platforms, AI-powered analytical tools, and seamless integration capabilities will yield significant competitive advantages. The transformative potential of diagnostic software lies not just in improving current testing protocols but in fundamentally changing how veterinarians interpret results, track disease progression, and implement treatment plans—creating opportunities for pioneering companies willing to lead this digital evolution.

Diagnostic Instruments: Engineering Precision at Point of Care

Diagnostic instruments represent the technological frontline of the animal health diagnostics landscape, with their value proposition centered on delivering rapid, accurate results at the point of care. The competitive differentiation among leading instruments is stark—IDEXX's Catalyst One completes testing in just 8 minutes while requiring larger sample volumes (700 μl for whole blood), whereas both Zoetis' VetScan2 and Seamaty's SMT-120VP operate with a 12-minute testing time but need only 100 μl samples. This variation in specifications reflects different approaches to balancing speed, convenience, and comprehensive testing capabilities. For veterinary practices and clinic operators, these distinctions translate into practical considerations around workflow efficiency, space utilization, and diagnostic comprehensiveness. Looking forward, the most successful instrument manufacturers will be those who optimize the balance between portability (with Seamaty's 4kg device contrasting Catalyst One's 12kg weight) and testing breadth (IDEXX offering 40 test parameters versus Seamaty's 47)—addressing the growing demand for comprehensive diagnostics in space-constrained clinical environments.

Segment Analysis: By Technology

Molecular Diagnostics: The Powerhouse of Precision Detection

Molecular diagnostics has established itself as both the largest and fastest-growing technology segment in the veterinary molecular diagnostics market, commanding 34.3% of the technology market while expanding at an exceptional 13.5% annual rate. This dual dominance reflects the transformative impact of DNA/RNA-based testing methods in revolutionizing disease detection sensitivity, specificity, and speed. The technology's remarkable growth is driven by increasing demands for early detection of zoonotic diseases and hereditary conditions, particularly relevant given studies showing widespread parasite prevalence across companion animals in multiple regions. For industry stakeholders, the implications are profound: molecular techniques are rapidly transitioning from specialized reference laboratory offerings to accessible in-clinic tools, reshaping diagnostic capabilities across the veterinary sector. As PCR, genomic sequencing, and other nucleic acid-based methods continue their expansion, manufacturers who successfully simplify these technologies for everyday clinical use—while maintaining their diagnostic power—will capture the most significant share of this high-growth segment.

Complementary Diagnostic Technologies: The Integrated Approach

Beyond molecular methods, the veterinary diagnostics landscape encompasses a diverse ecosystem of complementary technologies that collectively address the full spectrum of clinical needs. Immunodiagnostics excels in antibody detection and immunological response assessment, while clinical biochemistry provides essential insights into organ function and metabolic status. Hematology continues to serve as a frontline tool for identifying blood disorders and infections, exemplified by its role in detecting the parasitic conditions found in 50.7% of cats across European Union studies. For veterinary practices, the most effective diagnostic strategy emerges not from relying on a single technology but from strategically integrating multiple approaches based on specific clinical scenarios. This complementary relationship between diagnostic methodologies creates a nuanced market dynamic where technologies compete in some contexts while reinforcing each other in others. The key takeaway for industry participants is clear: success will increasingly favor companies offering integrated diagnostic platforms that seamlessly combine multiple technologies—allowing veterinarians to select the optimal testing approach for each unique clinical situation while maintaining workflow efficiency.

Segment Analysis: By Animal Type

Companion Animals: The Primary Focus of Diagnostic Innovation

The companion animal segment firmly anchors the companion animal diagnostics market with a dominant 62.4% market share, reflecting both the emotional and economic significance of pets in modern society. This leadership position stems from pet owners' growing willingness to invest in sophisticated diagnostic procedures, preventive screenings, and early disease detection for their animal companions. The critical importance of diagnostics is underscored by concerning statistics: 1 in 4 cats and 1 in 7 dogs in the United Kingdom may have fleas, while compliance with preventive care recommendations remains strikingly low—only 8.6% of United Kingdom dogs and 5.5% of Portuguese cats meet recommended deworming regimens. For diagnostic companies and veterinary service providers, this market concentration presents both opportunity and responsibility: developing more accessible, affordable screening tools could dramatically improve preventive care compliance rates while expanding the overall market. The decisive strategic advantage will belong to companies that effectively bridge the gap between diagnostic capabilities and practical implementation—creating solutions that not only detect health issues but also seamlessly integrate into preventive care protocols that pet owners can consistently follow.

Livestock Animals: The Rising Economic Imperative

The livestock animal segment has emerged as the fastest-growing category in the livestock diagnostics market, advancing at a robust annual rate. This accelerating growth trajectory reflects the increasing economic pressures on food production systems to optimize animal health while simultaneously addressing concerns about zoonotic disease transmission, antibiotic resistance, and production efficiency. Modern livestock operations increasingly rely on diagnostic technologies to implement targeted treatment protocols rather than broad preventive medication regimens—a shift driven by both regulatory requirements and consumer demands for reduced antibiotic use in food animals. For agricultural producers and veterinary service providers, this growth rate signals the need for strategic investments in herd-level diagnostic capabilities that can efficiently process multiple samples while delivering actionable results. The defining opportunity in this segment lies in developing diagnostic solutions specifically optimized for production contexts—offering the scalability, durability, and economic feasibility required in agricultural settings while maintaining the sensitivity needed to detect emerging disease threats before they impact production outcomes.

Geography Analysis

North America: The Established Leader in Veterinary Diagnostics

North America dominates the veterinary diagnostics market, commanding 41.6% of the global market share. This leadership position comes from strong pet insurance coverage, advanced veterinary facilities, and high spending on animal healthcare. The region benefits from ongoing technological innovation and strong partnerships between diagnostic companies and veterinary schools. While growing at 7.3% annually, the market is seeing strategic consolidation as key players seek economies of scale. Companies targeting North America should focus on delivering comprehensive diagnostic solutions that address both companion animal practices and livestock production systems, particularly as antimicrobial use faces increasing scrutiny.

United States: Where Scale Meets Sophistication in Veterinary Care

The United States leads the North American veterinary diagnostics landscape with 32% of the global market share. This dominance reflects high pet ownership rates, advanced veterinary infrastructure, and willingness to invest in cutting-edge diagnostic technologies. The market increasingly emphasizes preventive care diagnostics, driven by consumers who view pets as family members deserving quality healthcare. This trend has led to more specialized diagnostic laboratories and point-of-care testing solutions for quick results. Market leaders are developing integrated platforms that combine traditional testing with digital health monitoring, creating opportunities for veterinary diagnostic companies to generate ongoing revenue through both equipment sales and consumable purchases.

Mexico: The Emerging Growth Engine for Diagnostics Innovation

Mexico is the fastest-growing market in North America's veterinary diagnostics sector, expanding at 7.8% annually. This growth comes from rising middle-class pet ownership, modernization of livestock production, and increased focus on food safety standards for exports. The market offers significant opportunities for diagnostic companies willing to adapt their products to meet local price sensitivities and infrastructure limitations. There's growing demand for affordable point-of-care diagnostic tools that work reliably in various settings—from urban veterinary hospitals to remote rural facilities. Success in Mexico requires balancing technological capability with practical considerations of affordability and ease of use, especially as the country strengthens its position as an agricultural exporter needing enhanced disease monitoring.

Canada's Balanced Approach to Veterinary Healthcare

Canada completes North America's veterinary diagnostics landscape with a unique market profile reflecting its vast rural areas and concentrated urban centers. The Canadian market differs from the United States with greater public sector involvement in livestock disease monitoring and stronger regulatory oversight of diagnostic testing. The country balances technological advancement with cost-effectiveness, creating opportunities for diagnostic solutions serving diverse needs across extensive territories. The market shows particular strength in technologies supporting Canada's significant dairy and beef sectors, with emphasis on rapid detection of production-limiting diseases. Canadian veterinarians increasingly prefer integrated diagnostic platforms that combine laboratory testing with digital monitoring capabilities, allowing for comprehensive health management across challenging geography and climate conditions.

Europe: Where Precision and Regulation Drive Diagnostic Excellence

Europe holds approximately 26% of the global veterinary diagnostics market with an 8.3% annual growth rate. The region stands out for its regulatory framework emphasizing animal welfare, responsible antibiotic use, and food safety—creating specific market requirements for diagnostic solutions. The European Green Deal's focus on sustainable farming is increasing demand for testing solutions that support reduced antimicrobial use. This trend is highlighted by recent research where swine influenza A virus was detected in 20 out of 25 farms in Germany using RT-qPCR, demonstrating the importance of molecular diagnostics in disease surveillance. Companies targeting Europe need strategies addressing both technological sophistication and compliance with stringent regulations.

Germany: The Industrial Powerhouse of European Veterinary Diagnostics

Germany anchors the European veterinary diagnostics sector with approximately 8.3% of the global market share. The country's strength comes from its industrial capacity in diagnostic manufacturing, strong research infrastructure, and tradition of precision engineering in medical technologies. German veterinary practices show high adoption rates for advanced diagnostic platforms, reflecting the market's emphasis on quality and accuracy. The country leads in developing testing solutions supporting antimicrobial stewardship initiatives. This focus is evident in recent research where 26.1% of samples from RT-qPCR positive farms in Germany tested positive for swine influenza virus, showing the importance of sensitive detection methods. For diagnostic companies, Germany represents both a major market and a strategic hub for product development that influences adoption across Europe.

United Kingdom: Leading Europe's Shift Toward Integrated Veterinary Care

The United Kingdom is Europe's fastest-growing veterinary diagnostics market at 9.9% annual growth. This rapid expansion reflects the UK's approach to animal healthcare that emphasizes integrated care models covering prevention, diagnosis, and ongoing management. The post-Brexit regulatory environment creates both challenges and opportunities as the country establishes independent frameworks for veterinary products. Market dynamics are changing with the consolidation of veterinary practices into corporate groups using standardized diagnostic protocols. The UK's companion animal diagnostics sector is particularly strong, supported by high insurance coverage that reduces financial barriers to advanced testing. Companies should focus on diagnostic platforms that integrate with practice management software, supporting data-driven decisions while improving workflow efficiency.

Europe's Diverse Diagnostic Landscape: From Mediterranean to Nordic Markets

Beyond Germany and the UK, Europe's veterinary diagnostics landscape includes diverse markets with distinct characteristics requiring targeted approaches. France has a sophisticated market strong in companion animal diagnostics, reflecting cultural attitudes that view pets as family members. Italy shows notable growth in production animal diagnostics, supporting its significant agricultural sector with emphasis on dairy and specialty livestock products. Spain is increasingly adopting point-of-care testing solutions meeting the needs of geographically dispersed veterinary practices. Nordic countries represent a smaller but technologically advanced market segment characterized by early adoption of digital integration. Eastern European markets offer growing opportunities as veterinary infrastructure modernizes and pet ownership increases. Success across these markets requires flexible approaches adapting to varying clinical practices, reimbursement models, and technological infrastructure while navigating specific regulatory requirements.

Asia-Pacific: The New Frontier in Veterinary Diagnostic Growth

Asia-Pacific represents 26% of the global veterinary diagnostics market while growing at an industry-leading 9.9% annually. This impressive growth is driven by rapidly increasing pet ownership, modernizing livestock production, and greater focus on food safety and security. The region features extreme market diversity—from sophisticated urban centers with advanced veterinary facilities to developing rural areas with basic diagnostic needs. India exemplifies the region's potential, with the livestock sector contributing over 30% to the country's agricultural Gross Valued Added (GVA), highlighting the economic importance of animal health diagnostics. Companies targeting Asia-Pacific need strategies addressing diverse needs—from affordable point-of-care solutions for emerging markets to advanced molecular platforms for urban practices. Success requires not just technology but business models adaptable to different regulatory environments, veterinary infrastructures, and economic conditions.

Middle East and Africa: Untapped Potential in Veterinary Diagnostics

The Middle East and Africa represent an emerging frontier in the veterinary diagnostics market, currently holding 5.2% of global market share with 8.8% annual growth. The region combines traditional livestock practices deeply connected to cultural heritage with rapidly modernizing urban centers showing increased pet ownership. GCC countries lead regional development with investments in advanced veterinary infrastructure for both livestock and companion animals, while South Africa represents the continent's most developed market. The region's diagnostic landscape addresses two key priorities: supporting food security through livestock health monitoring and meeting growing demand for pet care among expanding middle-class populations. Companies targeting this region should recognize opportunities for technological leapfrogging—where markets without established systems can directly adopt new-generation diagnostic platforms, particularly those offering digital integration and telemedicine capabilities suited to widely dispersed veterinary services.

South America: Where Livestock Production Drives Diagnostic Innovation

South America market is growing in the global veterinary diagnostics market with 8.3% annual growth. The region's diagnostic landscape is shaped by its position as a global agricultural powerhouse, with emphasis on cattle and poultry production creating specific demand for testing solutions supporting herd health and productivity. Brazil dominates the regional market, using its position as a leading global meat exporter to drive adoption of advanced diagnostic technologies ensuring production efficiency and meeting international trade requirements. The region prioritizes solutions delivering clear economic returns for livestock systems, with growing but still secondary focus on companion animal applications in major cities. Diagnostic companies should develop testing platforms optimized for production animal applications—particularly those supporting herd-level screening, antimicrobial stewardship, and export compliance. Success requires not just effective technology but also strong distribution networks capable of reaching widely dispersed veterinary providers across challenging terrain.

Veterinary Diagnostics Industry Overview

Strategic Diversification Beyond Core Diagnostics

In the veterinary diagnostics landscape, market leaders are no longer content with merely providing standalone testing solutions. Companies like IDEXX Laboratories and Zoetis are strategically expanding their portfolios to create integrated ecosystems that address the entire veterinary workflow—from sample collection to result interpretation and treatment recommendations. This evolution reflects a deeper understanding that veterinary practices seek end-to-end solutions rather than isolated diagnostic tools. The rapid growth of the molecular diagnostics segment, projected to expand at approximately 13.5% CAGR and command a 34.3% market share by 2025, underscores how leading players are investing in advanced technologies to differentiate themselves from competitors. Furthermore, companies are increasingly pursuing strategic partnerships with pet insurance providers and veterinary clinic networks, recognizing that diagnostic access and reimbursement pathways are becoming as critical as the technology itself. The competitive edge now belongs to those veterinary diagnostic companies that can seamlessly integrate their offerings into the broader animal healthcare ecosystem while addressing the specific needs of both companion and livestock segments.

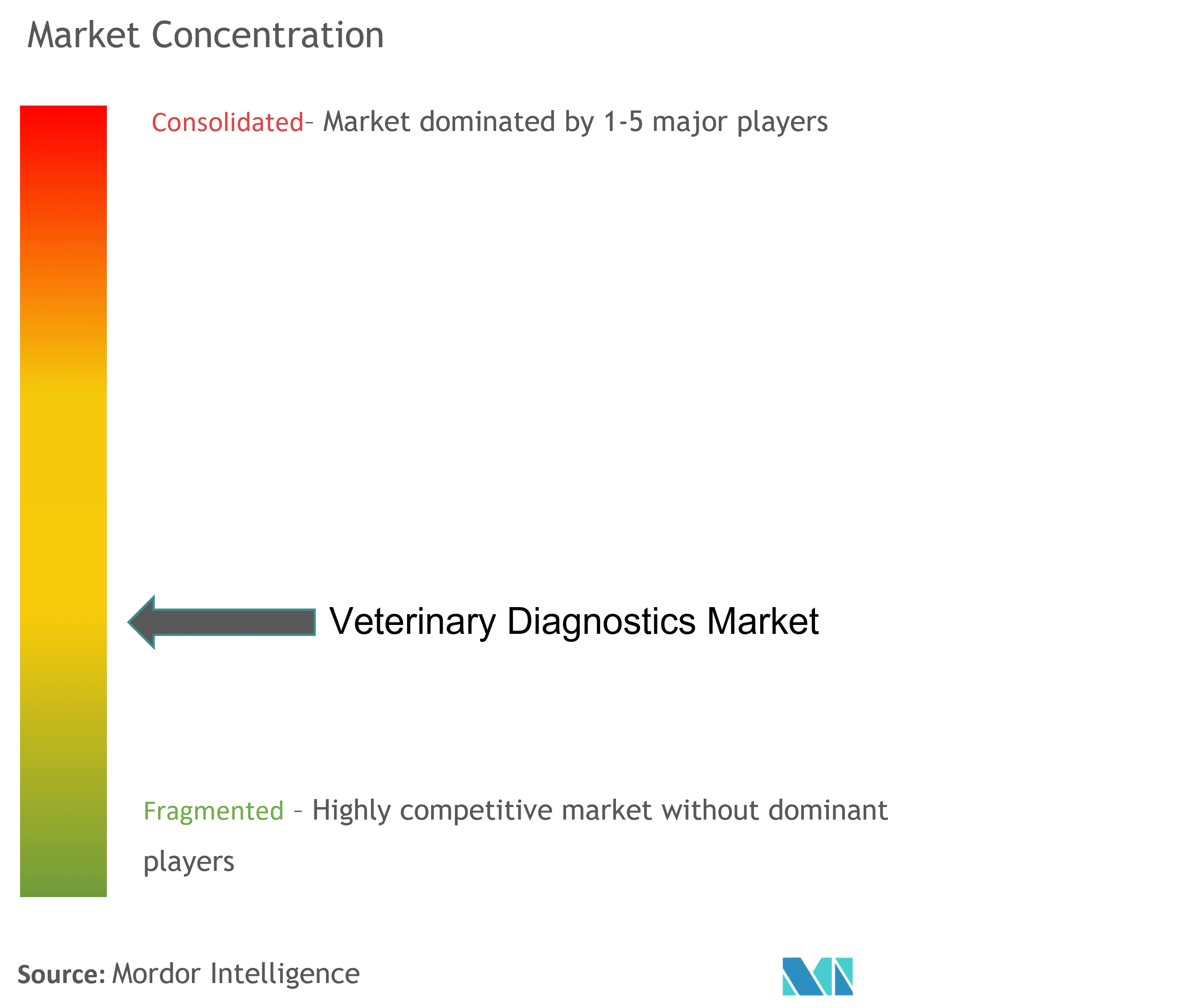

Consolidation vs. Specialization: The Two-Track Competitive Model

The veterinary diagnostics market is witnessing a fascinating dual-track competitive evolution where both consolidation and specialization are simultaneously reshaping the competitive landscape. On one track, industry giants like Thermo Fisher Scientific and BioMerieux are leveraging their substantial resources to acquire specialized players, enabling them to quickly expand their technological capabilities and geographic footprint. This consolidation strategy is particularly evident in the companion animal diagnostics market, which commands approximately 62.4% of the overall market, where larger players seek to capitalize on the emotional bond between pets and owners that drives higher spending on advanced diagnostics. On the parallel track, specialized firms like BIOCHEK BV and INDICAL Bioscience are carving out defensible niches by focusing exclusively on specific technologies or animal segments, developing deep expertise that broader players struggle to match. These specialists are particularly successful in the livestock diagnostics segment, where they can rapidly respond to emerging disease threats with targeted solutions. The market rewards both approaches—scale provides negotiating power and research capabilities, while specialization delivers agility and focused innovation—creating a dynamic ecosystem where different competitive strategies can coexist and thrive.

Data Intelligence: Transforming Diagnostics into Decision Support

The competitive battleground in animal health diagnostics is rapidly shifting from hardware capabilities to data intelligence, with forward-thinking competitors transforming their offerings from isolated diagnostic tools into comprehensive decision support platforms. Market leaders recognize that the true value lies not just in accurate test results but in contextualizing these results within broader animal health trends and treatment protocols. This strategic pivot explains why the Software and Services segment within the veterinary diagnostic devices market is projected to grow at a robust 12.5% CAGR through 2025, outpacing the overall market growth of 9.61%. Companies like Heska Corporation and Randox Laboratories are investing heavily in cloud-based platforms that aggregate diagnostic data across practices, enabling veterinarians to benchmark their findings against regional or national datasets and receive AI-powered treatment suggestions. This transition from selling products to delivering insights creates higher switching costs for customers and generates recurring revenue streams through subscription models. The competitive advantage now belongs to companies that can effectively combine their diagnostic hardware with sophisticated algorithms and user-friendly interfaces that seamlessly integrate into daily veterinary workflows, allowing them to capture greater value from each customer relationship.

Veterinary Diagnostics Market Leaders

-

Idexx Laboratories

-

Zoetis, Inc

-

Thermo Fisher Scientific Inc

-

Biomérieux SA

-

Virbac Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Veterinary Diagnostics Market News

- August 2022: PepiPets launched a new mobile diagnostic testing service. Launching this new service in a company release will allow clients to receive diagnostic testing at home for their pets. PepiPets hopes the at-home testing service will help pets feel more comfortable with the procedure and save time on travel to an in-person office visit.

- March 2022: Companion Animal Health promulgated a strategic agreement, including an equity investment, with HT BioImaging to co-brand and exclusively sell the HTVet product in the US and Canada.

Veterinary Diagnostics Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Adoption of Pet Ownership and Animal Health Expenditure

- 4.2.2 Increased Burden of Animal Zonotic Diseases

- 4.2.3 Growing Pet Insurance and Animal Health Investments by Pharmaceutical Companies

-

4.3 Market Restraints

- 4.3.1 Lack of Veterinarians

- 4.3.2 High Cost of Pet Care and Imaging Devices

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

-

5.1 By Product Type

- 5.1.1 Instruments

- 5.1.2 Kits and Reagents

- 5.1.3 Software and Services

-

5.2 By Technology

- 5.2.1 Immunodiagnostics

- 5.2.2 Clinical Biochemistry

- 5.2.3 Molecular Diagnostics

- 5.2.4 Hematology

- 5.2.5 Other Technologies

-

5.3 By Animal Type

- 5.3.1 Companion Animals

- 5.3.1.1 Dogs

- 5.3.1.2 Cats

- 5.3.1.3 Other Companion Animals

- 5.3.2 Livestock Animals

- 5.3.2.1 Cattle

- 5.3.2.2 Swine

- 5.3.2.3 Poultry

- 5.3.2.4 Other Livestock Animals

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 BioMerieux SA

- 6.1.2 Heska Corporation

- 6.1.3 Idexx Laboratories

- 6.1.4 IDVet

- 6.1.5 Randox Laboratories Ltd.

- 6.1.6 Thermo Fisher Scientific Inc.

- 6.1.7 Virbac Corporation

- 6.1.8 Zoetis Inc.

- 6.1.9 BIOCHEK BV

- 6.1.10 INDICAL Bioscience GmbH

- 6.1.11 Neogen Corporation

- 6.1.12 Bio-Rad Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Veterinary Diagnostics Industry Segmentation

As per the scope of this report, veterinary diagnostics provide medical diagnostic testing for infectious agents, toxins, and other causes of diseases in animal diagnostic samples. The Veterinary Diagnostics Market is Segmented by Product (Instruments, Kits & Reagents, and Software & Services), Technology (Immunodiagnostics, Molecular Diagnostics, Hematology, and Other Technologies), Animal Type (Companion Animals (Dogs, Cats, and Other Companion Animals) and Livestock Animals (Cattle, Swine, Poultry and Other Livestock Animals)), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD million) for the above segments.

| By Product Type | Instruments | ||

| Kits and Reagents | |||

| Software and Services | |||

| By Technology | Immunodiagnostics | ||

| Clinical Biochemistry | |||

| Molecular Diagnostics | |||

| Hematology | |||

| Other Technologies | |||

| By Animal Type | Companion Animals | Dogs | |

| Cats | |||

| Other Companion Animals | |||

| Livestock Animals | Cattle | ||

| Swine | |||

| Poultry | |||

| Other Livestock Animals | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Veterinary Diagnostics Market Research Faqs

How big is the Veterinary Diagnostics Market?

The Veterinary Diagnostics Market size is expected to reach USD 8.70 billion in 2025 and grow at a CAGR of 9.57% to reach USD 13.74 billion by 2030.

What is the current Veterinary Diagnostics Market size?

In 2025, the Veterinary Diagnostics Market size is expected to reach USD 8.70 billion.

Which is the fastest growing region in Veterinary Diagnostics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Veterinary Diagnostics Market?

In 2025, the North America accounts for the largest market share in Veterinary Diagnostics Market.

What years does this Veterinary Diagnostics Market cover, and what was the market size in 2024?

In 2024, the Veterinary Diagnostics Market size was estimated at USD 7.87 billion. The report covers the Veterinary Diagnostics Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Veterinary Diagnostics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Veterinary Diagnostics Industry Report

This comprehensive report offers a deep dive into the veterinary diagnostics industry, providing a detailed analysis of key market drivers and market segments. Mordor Intelligence offers customization based on your specific interests, including: 1. End-User: Hospitals, Clinics, POC/In-House, Labs 2. Technology: Pathology, Diagnostics Imaging, and Biochemistry