Market Size of United States In Vitro Diagnostics Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

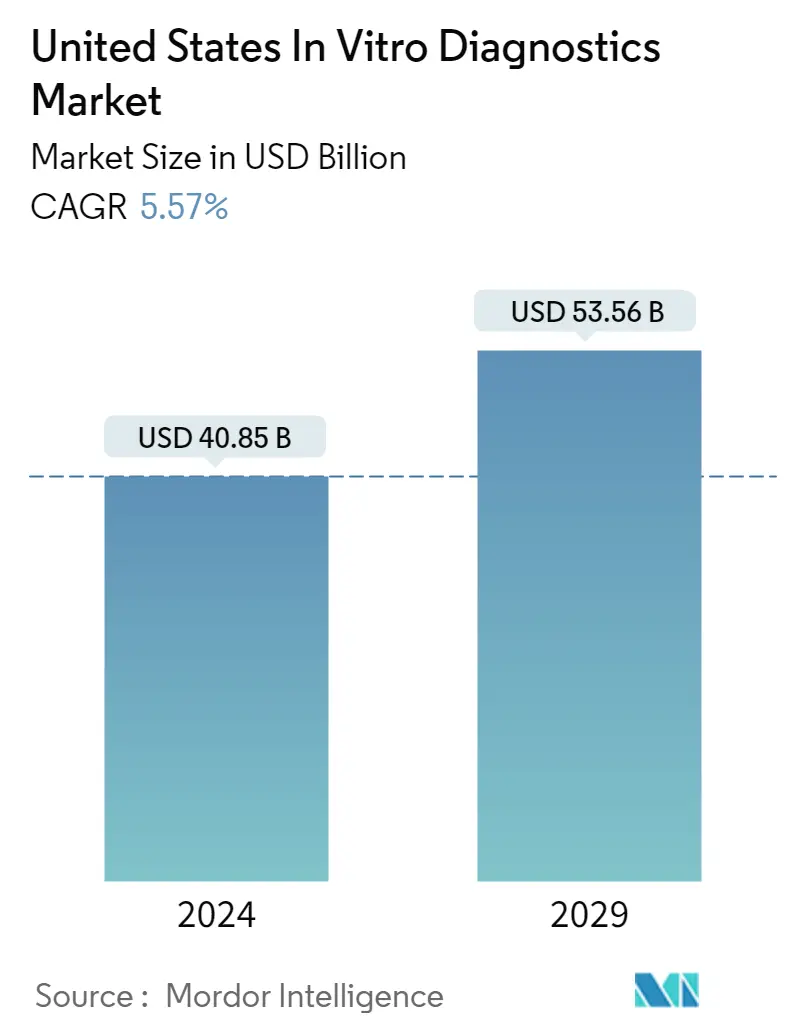

| Market Size (2024) | USD 40.85 Billion |

| Market Size (2029) | USD 53.56 Billion |

| CAGR (2024 - 2029) | 5.57 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

United States In Vitro Diagnostics Market Analysis

The United States In Vitro Diagnostics Market size is estimated at USD 40.85 billion in 2024, and is expected to reach USD 53.56 billion by 2029, growing at a CAGR of 5.57% during the forecast period (2024-2029).

The COVID-19 pandemic turned the spotlight on in vitro diagnostics since there is an increasing demand for IVD kits and reagents for the rapid and accurate diagnosis of SARS-CoV2 virus infection among the global population. The outbreak of COVID-19 is expected to positively impact the market, as in vitro diagnostics involve the testing of various biological samples. This is expected to aid the diagnosis of infectious diseases, such as COVID-19. Testing remains a crucial step in controlling the COVID-19 pandemic. There has been a shift in the industry dynamics, with the increasing number of players focusing on launching tests for home-based testing. Moreover, in 2021, the United States Food and Drug Administration also prioritized home-based molecular diagnostic tests. In March 2021, BATM Advanced Communications Ltd. announced the launch of its molecular diagnostics self-test kit for the detection of COVID-19. Moreover, these tests enable the early detection of diseases, maintaining a low threat of substitutes. Thus, an increase in demand for newly developed emergency use permitted IVD tests used for COVID-19 detection had a favorable influence on the market.

Key factors propelling the growth of the market are the high prevalence of chronic diseases, increasing the use of POC (Point-of-care) diagnostics, advanced technologies, and increasing awareness, and acceptance of personalized medicines. The increasing government healthcare expenditure and consumer healthcare spending are also responsible for the growth of the market.

According to the United States Census Bureau updates from June 2020, there were more than 54 million people aged 65 and above accounting for around 16.5% of the United States population in 2019. Moreover, it is expected to reach more than 85 million, around 20% of the country's population in 2050. Aging affects the immune system, which increases susceptibility to various diseases. Hence, a large geriatric population requires better healthcare, especially for chronic diseases. The increase in chronic disease cases is expected to increase the demand for in vitro diagnostics, thereby boosting the growth of the market over the forecast period.

Moreover, the increasing product launches with advanced features are expected to drive the market. For instance, in May 2021, Kroger announced the availability of Abbott's BinaxNOW COVID-19 Ag Card for self-testing. This is anticipated to improve the adoption of the product and help manage SARS-CoV-2. Furthermore, in April 2021, Abbott announced the distribution of BinaxNOW COVID-19 Ag Self-Test to retailers, including Walgreens, Walmart, and CVS Pharmacy, in the United States market. Moreover, in January 2020, Quest Diagnostics partnered with Memorial Hermann Health System to provide 21 hospital laboratories in Houston with better, cost-effective, high-quality, and creative diagnostic services.

There are also emerging technological innovations, such as lab-on-a-chip, wearable devices, and POC diagnostics, that are increasingly becoming an important part of the healthcare landscape. These POC diagnostic products have been developed to be used at a patient's bedside in hospitals to get instant results, without the need of sending the samples to the lab. Thus, owing to the ease of use and the ability to provide instant results, the use of POC diagnostics in the United States is increasing rapidly, thereby, boosting the growth of the market studied.

Thus, given the aforementioned factors, the United States in vitro diagnostic market is anticipated to propel over the forecast period.

United States In Vitro Diagnostics Industry Segmentation

As per the scope of the report, in vitro diagnostics are the medical devices and consumables utilized to perform in vitro tests on various biological samples. They are used for the diagnosis of various medical conditions. These in vitro diagnostic products can be instruments, reagents, or any system used for the diagnosis of diseases. The United States In Vitro Diagnostics Market is segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, Immuno Diagnostics, Haematology, and Other Test Types), Product (Instruments, Reagents, and Other Products), Usability (Disposable IVD and Reusable IVD), Application (Infectious Diseases, Diabetes, Cancer/Oncology, Cardiology, Autoimmune Diseases, Nephrology, and Other Applications), and End User (Diagnostic Laboratories, Hospitals and Clinics, and Other End Users). The report offers the value (in USD million) for the above segments.

| By Test Type | |

| Clinical Chemistry | |

| Molecular Diagnostics | |

| Immuno Diagnostics | |

| Haematology | |

| Other Test Types |

| By Product | |

| Instruments | |

| Reagents | |

| Other Products |

| By Usability | |

| Disposable IVD | |

| Reusable IVD |

| By Application | |

| Infectious Diseases | |

| Diabetes | |

| Cancer/Oncology | |

| Cardiology | |

| Autoimmune Diseases | |

| Nephrology | |

| Other Applications |

| By End User | |

| Diagnostic Laboratories | |

| Hospitals and Clinics | |

| Other End Users |

United States In Vitro Diagnostics Market Size Summary

The United States in vitro diagnostics market is poised for significant growth over the forecast period, driven by several key factors. The COVID-19 pandemic has underscored the critical role of in vitro diagnostics, with heightened demand for diagnostic kits and reagents facilitating rapid and accurate disease detection. This has led to a shift in industry dynamics, with an increasing focus on home-based testing solutions, supported by regulatory approvals from the United States Food and Drug Administration. The market is further bolstered by the high prevalence of chronic diseases, the rising adoption of point-of-care diagnostics, and advancements in technology. These factors, combined with increased government and consumer healthcare spending, are expected to propel market expansion.

The market landscape is characterized by moderate competition, with major players like Abbott Laboratories, Becton, Dickinson and Company, and Danaher Corporation actively engaging in strategic initiatives, mergers, and technological innovations to maintain their market positions. The aging population in the United States, coupled with the rising incidence of chronic conditions and cancer, is driving demand for in vitro diagnostics. Innovations such as lab-on-a-chip and wearable devices are becoming integral to healthcare, offering ease of use and instant results. The oncology segment is anticipated to experience the fastest growth, fueled by the increasing number of cancer cases and the demand for early-stage diagnosis. Regulatory approvals and government initiatives, such as the Cancer Moonshot, are further expected to enhance market growth by improving screening rates and early diagnosis capabilities.

United States In Vitro Diagnostics Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 High Burden of Chronic Diseases

-

1.2.2 Increasing Use of Point-of-care (POC) Diagnostics Spurring the IVD Market

-

1.2.3 Increasing Government Healthcare Expenditure and Consumer's Healthcare Spending

-

1.2.4 Advanced Technologies Fueling the IVD Market

-

1.2.5 Increasing Awareness and Acceptance of Personalized Medicine and Companion Diagnostics

-

-

1.3 Market Restraints

-

1.3.1 Lack of Proper Reimbursement

-

1.3.2 Stringent Regulatory Framework

-

1.3.3 Need For High Complexity Testing Centers

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD million)

-

2.1 By Test Type

-

2.1.1 Clinical Chemistry

-

2.1.2 Molecular Diagnostics

-

2.1.3 Immuno Diagnostics

-

2.1.4 Haematology

-

2.1.5 Other Test Types

-

-

2.2 By Product

-

2.2.1 Instruments

-

2.2.2 Reagents

-

2.2.3 Other Products

-

-

2.3 By Usability

-

2.3.1 Disposable IVD

-

2.3.2 Reusable IVD

-

-

2.4 By Application

-

2.4.1 Infectious Diseases

-

2.4.2 Diabetes

-

2.4.3 Cancer/Oncology

-

2.4.4 Cardiology

-

2.4.5 Autoimmune Diseases

-

2.4.6 Nephrology

-

2.4.7 Other Applications

-

-

2.5 By End User

-

2.5.1 Diagnostic Laboratories

-

2.5.2 Hospitals and Clinics

-

2.5.3 Other End Users

-

-

United States In Vitro Diagnostics Market Size FAQs

How big is the United States In Vitro Diagnostics Market?

The United States In Vitro Diagnostics Market size is expected to reach USD 40.85 billion in 2024 and grow at a CAGR of 5.57% to reach USD 53.56 billion by 2029.

What is the current United States In Vitro Diagnostics Market size?

In 2024, the United States In Vitro Diagnostics Market size is expected to reach USD 40.85 billion.