Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

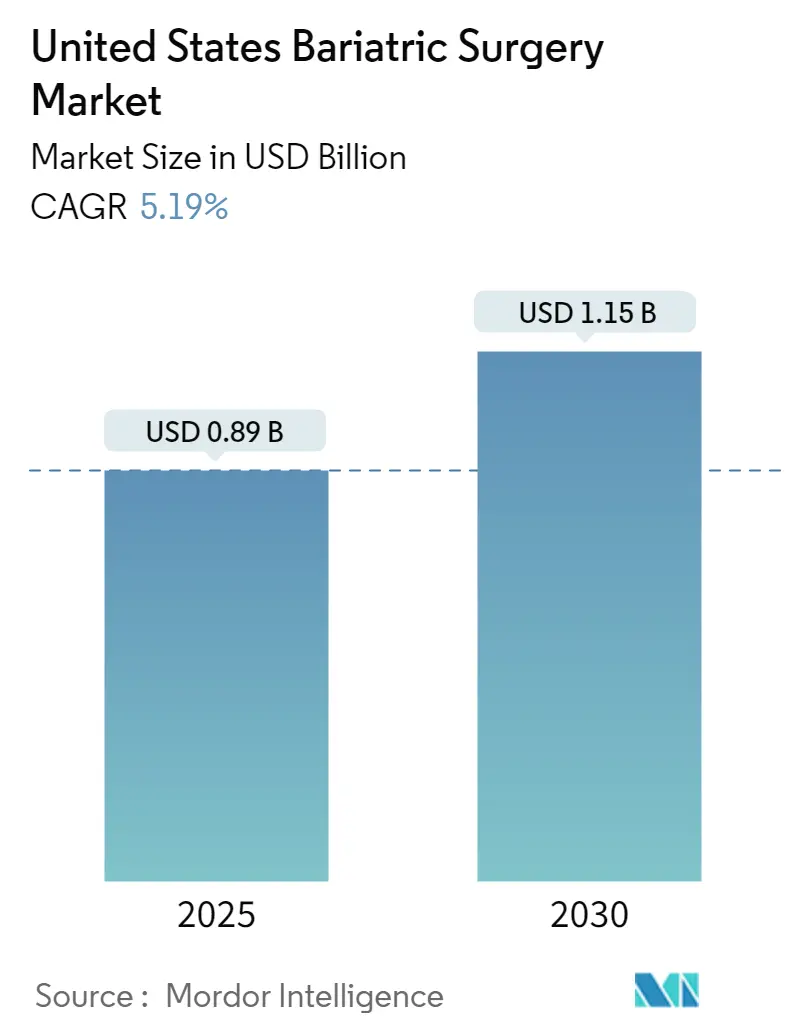

| Market Size (2025) | USD 0.89 Billion |

| Market Size (2030) | USD 1.15 Billion |

| Growth Rate (2025 - 2030) | 5.19% CAGR |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Bariatric Surgery Market Analysis by Mordor Intelligence

The United States Bariatric Surgery Market size is estimated at USD 0.89 billion in 2025, and is expected to reach USD 1.15 billion by 2030, at a CAGR of 5.19% during the forecast period (2025-2030).

The United States bariatric surgery landscape continues to evolve within the broader healthcare ecosystem, driven by significant technological advancements and changing patient demographics. According to the United States National Health Statistics Reports published in June 2021, the prevalence of obesity among adults aged 20 and over reached 41.9%, while severe obesity affected 9.2% of the adult population. This demographic shift has prompted healthcare providers to enhance their obesity treatment capabilities, leading to increased investments in advanced surgical technologies and specialized care facilities. The integration of robotic bariatric surgery systems and minimally invasive bariatric surgery techniques has become increasingly prevalent, transforming the standard of care in weight loss surgery procedures.

The technological landscape of bariatric surgery has witnessed remarkable advancement, particularly in surgical instrumentation and procedural techniques. Major medical device manufacturers have introduced innovative solutions to enhance surgical outcomes and patient safety. For instance, in September 2023, Ethicon, a Johnson & Johnson subsidiary, launched the ECHELON ENDOPATH Staple Line Reinforcement (SLR), representing a significant advancement in buttressing technology for bariatric procedures. This development exemplifies the industry's commitment to reducing complications and improving surgical precision through technological innovation. The emergence of robotic bariatric surgery platforms has further revolutionized the field, offering enhanced visualization and precise control during procedures.

The healthcare infrastructure supporting bariatric surgery has undergone substantial transformation, with an increasing number of specialized centers of excellence emerging across the United States. These centers have implemented comprehensive care protocols that encompass pre-operative assessment, surgical intervention, and post-operative support services. The establishment of multidisciplinary teams, including surgeons, nutritionists, psychologists, and support staff, has become standard practice, ensuring holistic patient care. Healthcare providers have also expanded their telemedicine capabilities, enabling better access to pre-operative consultations and post-operative follow-up care for patients in remote areas.

Insurance coverage and accessibility to weight loss surgery have evolved significantly, reflecting the growing recognition of obesity as a serious health condition requiring medical intervention. Healthcare providers and insurance companies have worked to streamline the approval process for bariatric procedures, acknowledging their long-term cost-effectiveness in managing obesity-related complications. The implementation of standardized protocols for patient selection and pre-operative preparation has helped optimize outcomes and justify coverage decisions. Additionally, the development of specialized bariatric surgery programs within major healthcare networks has improved access to these procedures for eligible patients, while maintaining high standards of care and safety.

United States Bariatric Surgery Market Trends and Insights

INCREASE IN RATE OF OBESITY

The United States continues to face a significant public health challenge with rising obesity rates across all age groups and demographics. According to the Trust for America's Health organization, the national adult obesity rate has reached an unprecedented level of 42.4%, marking the first time it has exceeded the 40% threshold. This represents a concerning 26% increase in obesity rates since 2008, highlighting the growing magnitude of this health crisis. The geographical distribution of obesity rates reveals significant variations across states, with Mississippi and West Virginia recording the highest adult obesity rates at 39.5%, while Colorado maintained the lowest rate at 23%. The severity of this situation is further emphasized by the fact that obesity rates have exceeded 35% in nine states, 30% in 31 states, and 25% in 48 states.

The increasing prevalence of obesity among younger populations is particularly alarming, as it indicates a potential long-term public health challenge. The Centers for Disease Control and Prevention reports that obesity affects about 14.4 million children and adolescents, with a prevalence rate of 19.3% among children aged 2-19 years. This trend is primarily attributed to poor diet plans, high urbanization, and a lack of physical activities. The Office of Disease Prevention and Health Promotion highlights that more than 80% of adults in the United States do not meet the guidelines for both aerobic and muscle-strengthening activities, contributing to the growing obesity epidemic. These factors collectively drive the demand for obesity treatments and weight management services, including bariatric surgical interventions, as proven solutions for weight management.

Understand The Key Trends Shaping This Market

Download PDF

INCREASE IN PREVALENCE OF TYPE-2 DIABETES AND OTHER CHRONIC DISORDERS

The escalating burden of diabetes and associated chronic disorders continues to be a significant driver for bariatric patient care and surgical interventions in the United States. According to the American Diabetes Association, approximately 34.2 million Americans are diagnosed with diabetes, with about 1.5 million new cases being diagnosed annually. The prevalence of diagnosed diabetes shows notable disparities among different ethnic groups, with American Indians/Alaska Natives having the highest rate at 14.7%, followed by Hispanic adults at 12.5%, and non-Hispanic Blacks at 11.7%. Additionally, an estimated 88 million adults aged 18 years or older have prediabetes, representing a substantial at-risk population that may benefit from obesity treatments and weight loss procedures.

The correlation between obesity and cardiovascular diseases presents another compelling factor driving market growth. The American Heart Association reports that between 2015 and 2018, 126.9 million American adults had some form of cardiovascular disease, with coronary heart disease being the leading cause of CVD-related deaths at 42.1%. The prevalence of high cholesterol among U.S. adults remains concerning, with 93.9 million individuals, or 38.1% of the population, having total cholesterol levels of 200 mg/dL or higher. These statistics underscore the critical role of obesity care and bariatric surgery in managing not only obesity but also its associated comorbidities, particularly among patients with multiple chronic conditions.

INITIATIVES AND PROGRAMS TO INCREASE OBESITY AWARENESS

The Centers for Disease Control and Prevention (CDC) has implemented comprehensive funding initiatives to support states, universities, and communities in advancing obesity prevention and health promotion efforts. The State Physical Activity and Nutrition (SPAN) Program currently funds 16 state recipients to implement evidence-based strategies at state and local levels to improve nutrition and physical activity. These initiatives specifically focus on reducing health disparities among groups at higher risk for poor nutrition and physical inactivity. The program's strategic approach includes improving access to healthier foods and creating safe spaces for physical activity, particularly in communities with significant health disparities.

The High Obesity Program (HOP), another significant CDC initiative, provides funding to 15 land grant universities to work with community extension services in counties where more than 40% of adults have obesity. This program has demonstrated substantial impact through its targeted approach, with significant funding allocations to various institutions. For instance, Auburn University received USD 1,092,000 to work across 13 counties, while Louisiana State University was granted USD 1,033,822 to implement programs in seven parishes. These initiatives are complemented by research and development efforts, such as clinical trials investigating new approaches to obesity treatment. The comprehensive nature of these programs, combined with substantial financial support, creates a supportive environment for addressing obesity-related health challenges and promotes awareness about available treatment options, including weight loss procedures and bariatric surgery.

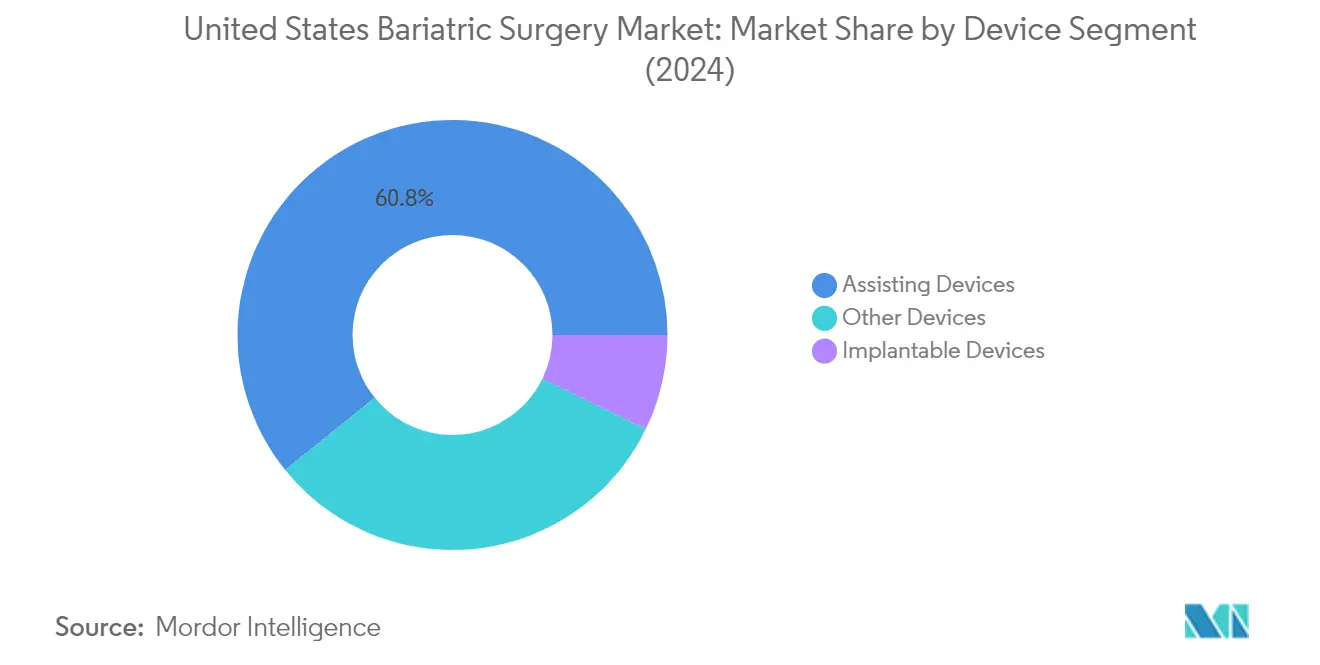

Segment Analysis: By Device

Assisting Devices Segment in United States Bariatric Surgery Market

The assisting devices segment dominates the United States bariatric surgery market, commanding approximately 61% of the total market share in 2024. This segment includes critical bariatric surgical instruments such as suturing devices, stapling devices, trocars, and other essential assisting instruments used in bariatric procedures. The segment's leadership position is primarily driven by the increasing adoption of minimally invasive bariatric surgery techniques and the growing preference for advanced surgical tools that enhance precision and reduce recovery time. The segment is also experiencing the highest growth rate in the market, projected to expand at approximately 8% from 2024 to 2029, driven by technological advancements in surgical instruments and the rising number of weight loss procedures being performed across the United States. Continuous innovation in surgical tools, particularly in areas such as robotic-assisted surgery and advanced stapling technologies, is further strengthening this segment's market position.

Remaining Segments in United States Bariatric Surgery Market

The implantable devices and other devices segments constitute the remaining portions of the bariatric surgery market, each playing crucial roles in different aspects of weight loss procedures. The implantable devices segment encompasses various products such as gastric bands, electrical stimulation devices, gastric balloons, and gastric emptying systems, offering less invasive alternatives to traditional surgical procedures. The other devices segment includes essential equipment such as laparoscopes, insufflation devices, endoscopes, surgical robots, and surgical smoke evacuation systems, which are fundamental to the successful execution of bariatric procedures. These segments continue to evolve with technological advancements and innovations in surgical techniques, contributing to the overall growth of the bariatric surgery market in the United States.

Competitive Landscape

Top Companies in United States Bariatric Surgery Market

The weight loss surgery market in the United States is characterized by continuous product innovation and strategic developments by major players like Medtronic PLC, Intuitive Surgical, Johnson & Johnson, and Olympus Corporation. Companies are heavily investing in research and development to expand their product portfolios through technological advancements, particularly in minimally invasive and robotic bariatric surgery solutions. The industry witnesses frequent collaborations and partnerships to enhance technological capabilities and market reach, exemplified by strategic acquisitions in robotics and artificial intelligence domains. Operational agility is demonstrated through global supply chain optimization and manufacturing facility consolidations, while geographic expansion is pursued through distribution network enhancement and the establishment of new subsidiaries. Market leaders are increasingly focusing on developing integrated solutions that combine surgical devices with advanced visualization systems and digital technologies to improve surgical outcomes.

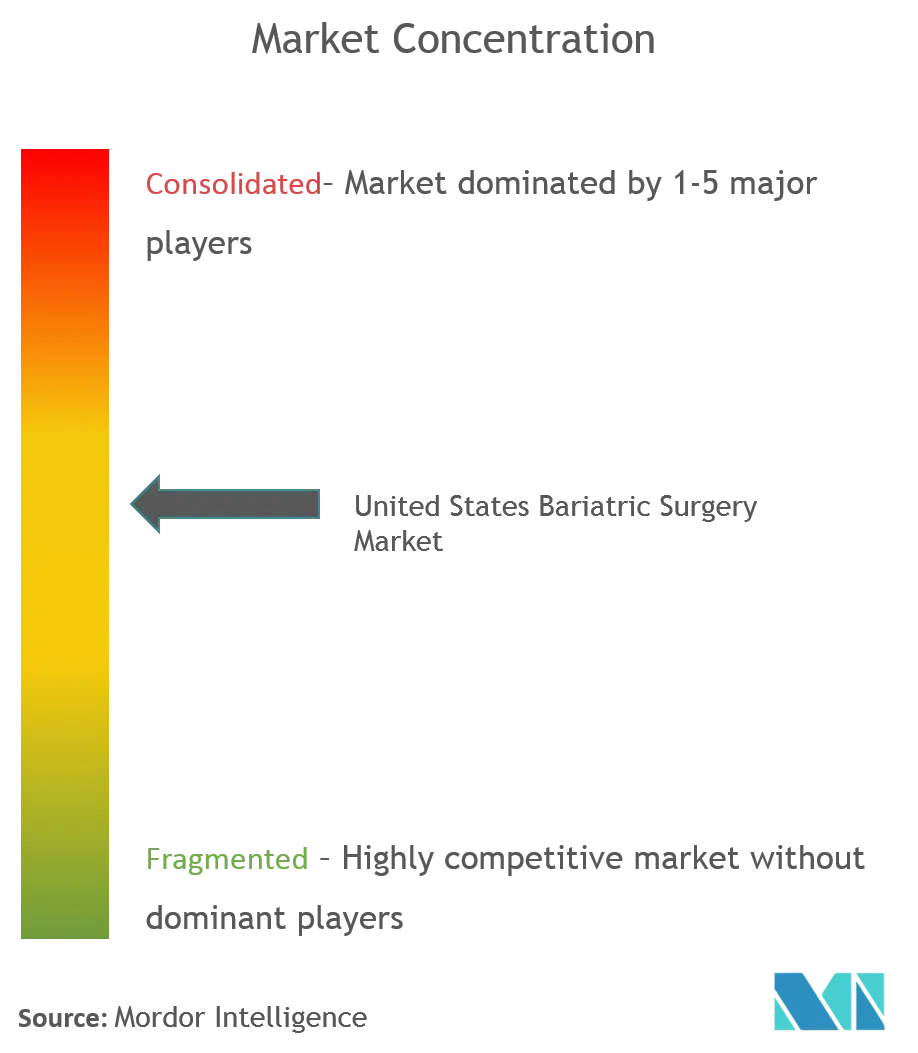

Consolidated Market with Strong Innovation Focus

The United States obesity surgery market exhibits a relatively consolidated structure dominated by large multinational medical device conglomerates with diverse healthcare portfolios. These major players leverage their extensive research capabilities, established distribution networks, and strong financial resources to maintain their market positions. The landscape is characterized by high entry barriers due to stringent regulatory requirements, substantial capital investments, and the need for significant technological expertise, which limits new entrant penetration. The market has witnessed active merger and acquisition activities, particularly focused on acquiring innovative technologies and expanding product portfolios.

The competitive dynamics are shaped by a mix of global leaders and specialized players, with the latter focusing on niche segments such as gastric balloons and specialized bariatric surgical instruments. Market consolidation continues through strategic acquisitions, particularly targeting companies with complementary technologies or a strong regional presence. The industry structure is further influenced by the presence of teaching facilities and research institutions that contribute to product development and surgical technique advancement, creating a collaborative ecosystem between commercial entities and healthcare institutions.

Innovation and Integration Drive Market Success

Success in the weight loss surgery market increasingly depends on companies' ability to develop comprehensive solution portfolios that combine surgical devices with advanced technologies. Incumbent players must focus on continuous innovation in minimally invasive techniques, robotic surgery capabilities, and digital integration while maintaining strong relationships with healthcare providers and ensuring the cost-effectiveness of their solutions. Market leaders are strengthening their positions through investments in clinical research, professional education programs, and enhanced post-operative support services, while also expanding their geographic presence through strategic partnerships and distribution agreements.

For emerging players and contenders, success lies in identifying and exploiting underserved market segments while developing differentiated products that address specific surgical needs or improve patient outcomes. The increasing focus on value-based healthcare and the growing importance of real-world evidence create opportunities for companies that can demonstrate superior clinical outcomes and cost-effectiveness. Regulatory compliance remains crucial, with companies needing to navigate complex approval processes while maintaining quality standards. The relatively low threat of substitution from non-surgical alternatives provides stability, but companies must continue to innovate to address evolving surgical techniques and changing healthcare provider preferences. Additionally, the integration of weight management services into surgical offerings is becoming a key differentiator in enhancing patient outcomes and satisfaction.

United States Bariatric Surgery Industry Leaders

-

Medtronic PLC

-

Johnson and Johnson (Ethicon Inc)

-

Apollo Endosurgery, Inc

-

Aspire Bariatrics Inc.

-

Intuitive Surgical Inc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- In September 2021, Olympus launched the POWERSEAL advanced bipolar surgical energy devices to Strengthen its Surgical Portfolio. The POWERSEAL devices can be used in numerous forms of surgical intervention including bariatric surgical procedures.

- In June 2021, Ethicon, part of the Johnson & Johnson Medical Devices Companies launched the ENSEAL X1 Curved Jaw Tissue Sealer for colorectal, gynecological, bariatric surgery, and thoracic procedures.

United States Bariatric Surgery Market Report Scope

As per the scope of the report, bariatric surgery or weight loss surgery is used as one of the major treatment procedures for treating obesity. It is generally the last option for patients who have failed to lose weight by several other means. During this procedure, the size of the stomach is reduced by either removing some parts of the stomach or by using a gastric band. The United States Bariatric Surgery Market is segmented by the device (Assisting Devices, and Implantable Devices). The report offers the value (in USD million) for the above segments.

By Device

| Assisting Devices | Suturing Device |

| Closure Device | |

| Stapling Device | |

| Trocars | |

| Other Assisting Devices | |

| Implantable Devices | Gastric Bands |

| Electrical Stimulation Devices | |

| Gastric Balloons | |

| Gastric Emptying | |

| Other Devices |

| By Device | Assisting Devices | Suturing Device |

| Closure Device | ||

| Stapling Device | ||

| Trocars | ||

| Other Assisting Devices | ||

| Implantable Devices | Gastric Bands | |

| Electrical Stimulation Devices | ||

| Gastric Balloons | ||

| Gastric Emptying | ||

| Other Devices | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the United States Bariatric Surgery Market?

The United States Bariatric Surgery Market size is expected to reach USD 0.89 billion in 2025 and grow at a CAGR of 5.19% to reach USD 1.15 billion by 2030.

What is the current United States Bariatric Surgery Market size?

In 2025, the United States Bariatric Surgery Market size is expected to reach USD 0.89 billion.

Who are the key players in United States Bariatric Surgery Market?

Medtronic PLC, Johnson and Johnson (Ethicon Inc), Apollo Endosurgery, Inc, Aspire Bariatrics Inc. and Intuitive Surgical Inc are the major companies operating in the United States Bariatric Surgery Market.

What years does this United States Bariatric Surgery Market cover, and what was the market size in 2024?

In 2024, the United States Bariatric Surgery Market size was estimated at USD 0.84 billion. The report covers the United States Bariatric Surgery Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United States Bariatric Surgery Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: