| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 2.78 Billion |

| Market Size (2030) | USD 3.42 Billion |

| CAGR (2025 - 2030) | 4.21 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

US Turf and Ornamental Protection Market Analysis

The US Turf and Ornamental Protection Market size is estimated at 2.78 billion USD in 2025, and is expected to reach 3.42 billion USD by 2030, growing at a CAGR of 4.21% during the forecast period (2025-2030).

The US turf and ornamental protection industry continues to evolve with changing landscape preferences and an increasing focus on sustainable urban development. The sector has witnessed substantial growth in commercial and residential landscaping projects, driven by the expanding real estate sector and a growing emphasis on creating attractive outdoor spaces. The industry's transformation is evident from the rising number of floriculture producers, with 9,558 producers spread across 17 states in 2021, marking an 8% increase from the previous year. This growth in production capacity has been accompanied by significant technological advancements in pest management solutions and application methods, enabling more efficient and targeted protection of turf and ornamental plants.

The market has experienced notable shifts in product development and formulation technologies, with manufacturers focusing on creating more environmentally conscious solutions. Precision farming methods have gained significant traction, with advanced technologies like GPS, sensors, and drones being increasingly utilized for targeted pesticide application. The integration of these technologies has revolutionized application methods, particularly in large-scale operations such as golf courses and sports fields, emphasizing sports turf protection. The industry has also witnessed a growing trend toward integrated pest management approaches, combining chemical and biological control methods to achieve optimal results while minimizing environmental impact.

Export opportunities have emerged as a significant growth avenue for the US turf and ornamental sector, with the country's ornamental plant exports reaching USD 535 million in 2022, representing a 3.3% increase from the previous year. This growth in international trade has been supported by stringent quality control measures and advanced protection solutions that ensure plant health and appearance during transportation and establishment in foreign markets. The industry has also seen increased adoption of native grass varieties, particularly in regions like Texas, where buffalo grass, blue grama, and thunder turf are replacing traditional varieties due to their superior water conservation properties.

The market landscape is characterized by ongoing innovation in product formulations and application technologies. Active ingredient pricing trends have significantly influenced product development strategies, with key ingredients like cypermethrin commanding premium prices of USD 21.2 thousand per metric ton in 2022. This has prompted manufacturers to focus on developing more cost-effective formulations while maintaining efficacy. The industry has also witnessed a shift toward specialized solutions for specific applications, with manufacturers developing products tailored to the unique requirements of different turf management and ornamental varieties, including sports turf, golf course turf, and commercial and residential lawns. The focus on professional turf care has further driven innovation in this sector.

US Turf and Ornamental Protection Market Trends

Growing adoption of turf & ornamental crops in various applications, extending cultivation area under these crops may drive the market

- Neonicotinoids are the most commonly used in turf care as a preventive material for the control of white grubs. Turf and ornamental crops comprise about 4% of neonicotinoid usage in the United States. There is a rising demand for well-maintained turf and ornamental landscapes, such as in parks, golf courses, gardens, and public spaces, leading to higher pesticide usage to control pests and maintain the desired appearance.

- The area under the turf and ornamental increased by 649.8 thousand hectares between 2017 and 2022 due to the rising demand for flowers in the United States. The increase in cultivation area and meeting the quality requirements led to the increase in the consumption of pesticides during the same period.

- Homeowners, landscapers, and property managers are more aware of the importance of pest management to maintain the value and appeal of their landscapes, leading to higher adoption of pesticide products. Golf courses, sports fields, and public parks often require pest management to maintain their quality, contributing to the consumption of pesticides in the turf segment.

- Additionally, an increase in pest pressures affecting turfs and ornamental areas, such as weeds, insects, or diseases, could lead to an increase in the consumption of pesticides for effective control during the coming years. As urban areas expand, green spaces become more concentrated, creating conducive environments for pests to thrive, which could lead to a higher demand for pest management solutions.

- Changing climate patterns can influence pest populations, which may drive the consumption of pesticides in the coming years.

Understand The Key Trends Shaping This Market

Download PDF

Effectiveness in controlling various insects such as aphids, beetles, spotted ball worms, pink ball worms, early spot borers, hairy caterpillars, and limited availability in the country is increasing the price of it

- In 2022, cypermethrin was priced at USD 21.2 thousand per metric ton. It has been widely adopted in turf & ornamental crops for its effectiveness in controlling various types of insects, including aphids, beetles, spotted ball worms, pink ball worms, early spot borers, and hairy caterpillars. Its effectiveness has made it popular for farmers seeking to protect their crops from pests and ensure a successful harvest.

- Atrazine, a systemic herbicide belonging to the chlorinated triazine group, is utilized for targeted control of annual grasses and broadleaf weeds before their emergence. Pesticide formulations containing atrazine are approved for application on various turf & ornamental such as sports turf, golf course turf, and commercial and residential lawns, in addition to agricultural applications like corn, sweet corn, sorghum, sugarcane, wheat, macadamia nuts, and guava. Atrazine was priced at USD 13.8 thousand per metric ton in 2022.

- Malathion is used to control a wide range of pests, including aphids, fleas, and other sucking pests on several valuable ornamental crops. Crops extensively grown in the United States and frequently use malathion are chrysanthemums, evergreens, roses, camellias, and azaleas. Malathion was priced at USD 12.6 thousand per metric ton in 2022.

- Mancozeb is a broad-spectrum contact fungicide labeled for outdoor and greenhouse crops in the United States. It protects against a wide spectrum of fungal diseases, including leaf, stem, stripe rusts, botrytis blight, leaf spot, and Cercospora blight. It serves as a seed treatment for crops such as potatoes, corn, sorghum, tomatoes, and cereal grains. In 2022, its market value reached USD 7.8 thousand per metric ton.

Segment Analysis: Function

Herbicide Segment in US Turf and Ornamental Protection Market

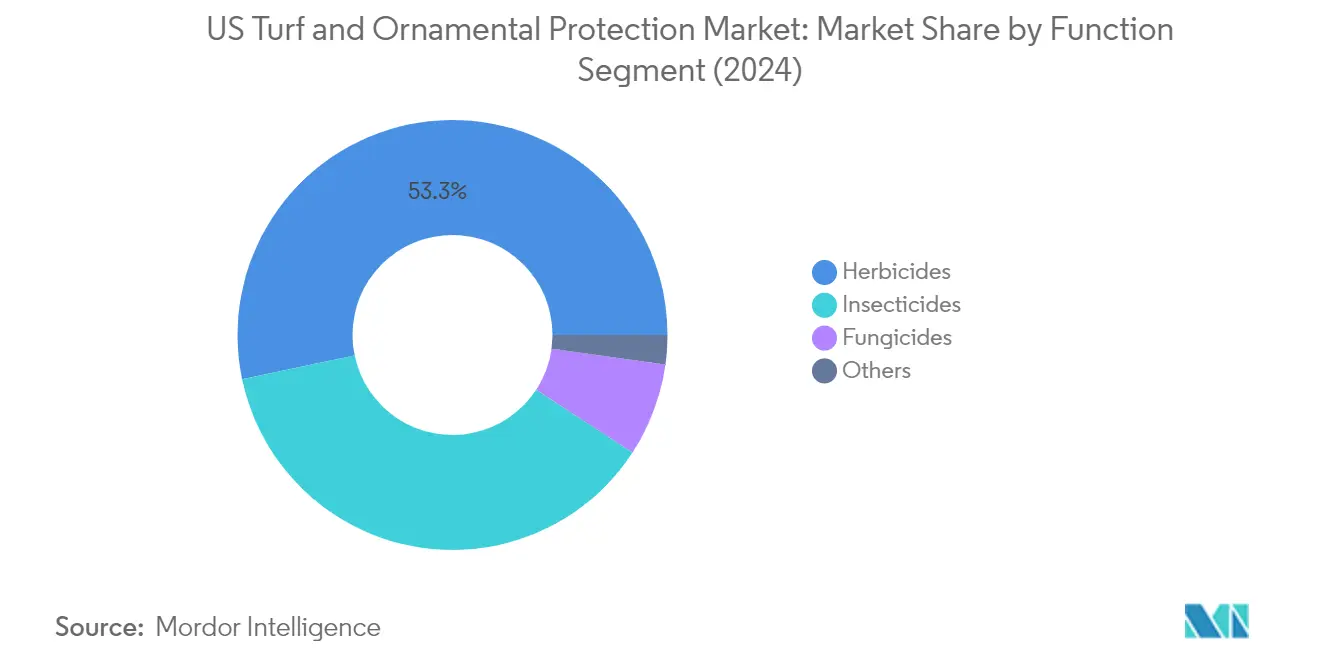

Turf herbicides dominate the US turf and ornamental protection market, commanding approximately 53% market share in 2024. This significant market presence is primarily driven by the widespread prevalence of weed infestation in turf and ornamental crops. Common weeds affecting these crops include crabgrass, goosegrass, barnyard grass, and foxtail, necessitating extensive turf herbicide application. The segment is also experiencing the fastest growth trajectory, projected to expand at nearly 5% CAGR from 2024 to 2029. This growth is attributed to rising domestic demand for turf and ornamental plants, coupled with the increasing need for effective weed control solutions. The segment's strong performance is further supported by the development of advanced herbicide formulations that provide targeted and efficient weed management while minimizing environmental impact.

Remaining Segments in Function

The ornamental insecticide segment represents the second-largest portion of the market, addressing challenges posed by various pests including northern and southern masked chafers, Asiatic garden beetles, weevils, billbugs, Japanese beetles, oriental beetles, European chafers, cutworms, and chinch bugs. Ornamental fungicides play a crucial role in protecting turf and ornamental plants from diseases such as dollar spots, brown patches, powdery mildew, and leaf spots. Nematicides are essential for controlling soil-dwelling nematodes that can damage root systems, while molluscicides provide specialized protection against snails and slugs that can severely impact plant health. Each of these segments contributes to the comprehensive pest management approach required in the turf and ornamental sector.

Segment Analysis: Application Mode

Foliar Segment in US Turf and Ornamental Protection Market

Foliar application dominates the US turf and ornamental protection market, commanding approximately 41% market share in 2024. This application method's prominence can be attributed to its versatility and efficiency in delivering crop protection chemicals directly to plant surfaces. Foliar application is particularly favored due to its compatibility with precision farming methods, allowing farmers to administer pesticides in a targeted manner based on specific crop needs. The method's popularity is further enhanced by its ease of implementation using various equipment options, including backpack sprayers, tractor-mounted sprayers, and specialized turf sprayers, making it a practical choice for turf managers handling large areas. Insecticides represent the largest share of foliar applications, followed by herbicides and fungicides, demonstrating the method's versatility in addressing various pest management needs.

Soil Treatment Segment in US Turf and Ornamental Protection Market

The soil treatment segment is experiencing the fastest growth trajectory in the US turf and ornamental protection market, projected to expand at approximately 5% CAGR from 2024 to 2029. This robust growth is driven by the segment's effectiveness in controlling soil-borne pests and diseases through enhanced absorption and distribution of pesticides within the soil profile. The method's ability to allow chemicals to penetrate deeply and reach target organisms effectively makes it particularly valuable for comprehensive pest management strategies. The growth is further supported by the method's effectiveness in addressing resistance issues, as it provides an alternative delivery mechanism for pesticides. The segment's expansion is also bolstered by its optimal performance when soil moisture conditions are favorable, enabling better pesticide penetration into root zones and improved efficacy against target pests.

Remaining Segments in Application Mode

The US turf and ornamental protection market features several other significant application modes, including chemigation, seed treatment, and fumigation. Chemigation has gained traction due to its integration with modern irrigation systems, offering precise timing and uniform distribution of pesticides. Seed treatment serves as a preventive measure, providing protection during critical early growth stages and improving seedling establishment. Fumigation, while representing a smaller share, plays a crucial role in managing soil-dwelling pests and pathogens, particularly in intensive cultivation systems. Each of these application methods addresses specific challenges in turf and ornamental protection, contributing to a comprehensive approach to pest and disease management.

US Turf and Ornamental Protection Industry Overview

Top Companies in US Turf and Ornamental Protection Market

The US turf and ornamental protection market is characterized by continuous product innovation and strategic expansion initiatives by leading companies. Major players are focusing on developing specialized formulations and novel active ingredients to address evolving pest management challenges in turf and ornamental applications. Companies are strengthening their market positions through research and development investments, particularly in creating sustainable and environmentally friendly solutions. Operational agility is demonstrated through the establishment of new manufacturing facilities and distribution networks, enabling better market coverage and customer service. Strategic partnerships and collaborations with research institutions and universities are becoming increasingly common to enhance product development capabilities. The industry also witnesses a strong emphasis on digital solutions and precision application technologies to improve product efficacy and user experience.

Consolidated Market Led By Global Players

The US turf and ornamental protection market exhibits a highly consolidated structure dominated by global agricultural science companies with diverse product portfolios. These major players leverage their extensive research capabilities, established distribution networks, and strong brand recognition to maintain their market positions. The market is primarily controlled by multinational corporations that offer comprehensive solutions across various agricultural segments, including specialized turf management and ornamental protection products. These companies benefit from their ability to invest in advanced technologies and maintain robust supply chains, giving them a competitive advantage over smaller players.

The competitive landscape is characterized by strategic acquisitions and partnerships aimed at expanding product portfolios and geographical reach. Large agrochemical companies are actively pursuing vertical integration strategies to strengthen their market presence and control over the value chain. Local players and specialists maintain their relevance through niche market focus and specialized product offerings for specific regional requirements. The industry structure promotes innovation and quality standards while creating significant barriers to entry for new market participants.

Innovation and Sustainability Drive Future Success

Success in the turf and ornamental protection market increasingly depends on companies' ability to develop innovative, sustainable solutions that meet evolving environmental regulations and customer preferences. Market leaders must focus on developing products with improved efficacy and reduced environmental impact while maintaining cost-effectiveness. Companies need to invest in digital technologies and precision application methods to differentiate their offerings and provide value-added services to customers. Building strong relationships with distributors and end-users through technical support and education programs is becoming crucial for maintaining market share.

For contenders looking to gain ground, specialization in specific market segments or geographical regions offers opportunities for growth. Companies must focus on developing unique value propositions through specialized formulations or application technologies that address specific customer needs. Success also depends on building efficient distribution networks and establishing strong technical support capabilities. Regulatory compliance and environmental stewardship will continue to be critical factors, with companies needing to demonstrate their commitment to sustainable practices and product safety. The ability to adapt to changing customer preferences and regulatory requirements while maintaining operational efficiency will be key to long-term success in the market. The emphasis on landscape protection and professional turf care is essential for companies aiming to lead in this industry.

US Turf and Ornamental Protection Market Leaders

-

BASF SE

-

Corteva Agriscience

-

Environmental Science US LLC (Envu)

-

FMC Corporation

-

Nufarm Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

US Turf and Ornamental Protection Market News

- April 2023: Nufarm launched a new liquid formulation fungicide, Tourney EZ, exclusively for turf and ornamental crops based on customer demand, which further strengthens the company's role in turf and ornamental crop protection.

- November 2022: Lier Chemical Company Ltd and Nufarm Ltd Americas Inc. established a partnership to deliver glufosinate to the turf and ornamental (T&O) industry.

- March 2022: With the QuickPHlo-R (QPR) phosphine generator, which uses a special granular formulation in an enclosed application system, UPL Environmental Solutions expanded its fumigation product line.

Free With This Report

Along with the report, We also offer a comprehensive and exhaustive data pack with 50+ graphs on insecticide, fungicides, and herbicides consumption per hectare and the average price of active ingredients used in insecticides, fungicides, herbicides, nematicides, and molluscicides. The data pack includes Globe, North America, Europe, Asia-Pacific, South America, and Africa.

US Turf and Ornamental Protection Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

-

4.3 Regulatory Framework

- 4.3.1 United States

- 4.4 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

-

5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 American Vanguard Corporation

- 6.4.2 BASF SE

- 6.4.3 Corteva Agriscience

- 6.4.4 Environmental Science US LLC (Envu)

- 6.4.5 FMC Corporation

- 6.4.6 Gowan Company

- 6.4.7 Mitsui & Co. Ltd (Certis Belchim)

- 6.4.8 Nufarm Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7. KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- PESTICIDE CONSUMPTION PER HECTARE, GRAMS, UNITED STATES, 2017 - 2022

- Figure 2:

- ACTIVE INGREDIENT PRICE PER METRIC TON, USD, UNITED STATES, 2017 - 2022

- Figure 3:

- CROP PROTECTION CHEMICALS VOLUME METRIC TON, UNITED STATES, 2017 - 2029

- Figure 4:

- CROP PROTECTION CHEMICALS VALUE USD, UNITED STATES, 2017 - 2029

- Figure 5:

- CROP PROTECTION CHEMICALS MARKET BY FUNCTION, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 6:

- CROP PROTECTION CHEMICALS MARKET BY FUNCTION, USD, UNITED STATES, 2017 - 2029

- Figure 7:

- VALUE SHARE OF CROP PROTECTION CHEMICALS BY FUNCTION, %, UNITED STATES, 2017 VS 2023 VS 2029

- Figure 8:

- VOLUME SHARE OF CROP PROTECTION CHEMICALS BY FUNCTION, %, UNITED STATES, 2017 VS 2023 VS 2029

- Figure 9:

- CONSUMPTION OF FUNGICIDE, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 10:

- CONSUMPTION OF FUNGICIDE, USD, UNITED STATES, 2017 - 2029

- Figure 11:

- VALUE SHARE OF FUNGICIDE BY APPLICATION MODE, %, UNITED STATES, 2022 VS 2029

- Figure 12:

- CONSUMPTION OF HERBICIDE, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 13:

- CONSUMPTION OF HERBICIDE, USD, UNITED STATES, 2017 - 2029

- Figure 14:

- VALUE SHARE OF HERBICIDE BY APPLICATION MODE, %, UNITED STATES, 2022 VS 2029

- Figure 15:

- CONSUMPTION OF INSECTICIDE, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 16:

- CONSUMPTION OF INSECTICIDE, USD, UNITED STATES, 2017 - 2029

- Figure 17:

- VALUE SHARE OF INSECTICIDE BY APPLICATION MODE, %, UNITED STATES, 2022 VS 2029

- Figure 18:

- CONSUMPTION OF MOLLUSCICIDE, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 19:

- CONSUMPTION OF MOLLUSCICIDE, USD, UNITED STATES, 2017 - 2029

- Figure 20:

- VALUE SHARE OF MOLLUSCICIDE BY APPLICATION MODE, %, UNITED STATES, 2022 VS 2029

- Figure 21:

- CONSUMPTION OF NEMATICIDE, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 22:

- CONSUMPTION OF NEMATICIDE, USD, UNITED STATES, 2017 - 2029

- Figure 23:

- VALUE SHARE OF NEMATICIDE BY APPLICATION MODE, %, UNITED STATES, 2022 VS 2029

- Figure 24:

- CROP PROTECTION CHEMICALS MARKET BY APPLICATION MODE, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 25:

- CROP PROTECTION CHEMICALS MARKET BY APPLICATION MODE, USD, UNITED STATES, 2017 - 2029

- Figure 26:

- VALUE SHARE OF CROP PROTECTION CHEMICALS BY APPLICATION MODE, %, UNITED STATES, 2017 VS 2023 VS 2029

- Figure 27:

- VOLUME SHARE OF CROP PROTECTION CHEMICALS BY APPLICATION MODE, %, UNITED STATES, 2017 VS 2023 VS 2029

- Figure 28:

- CROP PROTECTION CHEMICALS APPLIED THROUGH CHEMIGATION, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 29:

- CROP PROTECTION CHEMICALS APPLIED THROUGH CHEMIGATION, USD, UNITED STATES, 2017 - 2029

- Figure 30:

- VALUE SHARE OF CHEMIGATION BY FUNCTION, %, UNITED STATES, 2022 VS 2029

- Figure 31:

- CROP PROTECTION CHEMICALS APPLIED THROUGH FOLIAR, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 32:

- CROP PROTECTION CHEMICALS APPLIED THROUGH FOLIAR, USD, UNITED STATES, 2017 - 2029

- Figure 33:

- VALUE SHARE OF FOLIAR BY FUNCTION, %, UNITED STATES, 2022 VS 2029

- Figure 34:

- CROP PROTECTION CHEMICALS APPLIED THROUGH FUMIGATION, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 35:

- CROP PROTECTION CHEMICALS APPLIED THROUGH FUMIGATION, USD, UNITED STATES, 2017 - 2029

- Figure 36:

- VALUE SHARE OF FUMIGATION BY FUNCTION, %, UNITED STATES, 2022 VS 2029

- Figure 37:

- CROP PROTECTION CHEMICALS APPLIED THROUGH SEED TREATMENT, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 38:

- CROP PROTECTION CHEMICALS APPLIED THROUGH SEED TREATMENT, USD, UNITED STATES, 2017 - 2029

- Figure 39:

- VALUE SHARE OF SEED TREATMENT BY FUNCTION, %, UNITED STATES, 2022 VS 2029

- Figure 40:

- CROP PROTECTION CHEMICALS APPLIED THROUGH SOIL TREATMENT, METRIC TON, UNITED STATES, 2017 - 2029

- Figure 41:

- CROP PROTECTION CHEMICALS APPLIED THROUGH SOIL TREATMENT, USD, UNITED STATES, 2017 - 2029

- Figure 42:

- VALUE SHARE OF SOIL TREATMENT BY FUNCTION, %, UNITED STATES, 2022 VS 2029

- Figure 43:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, UNITED STATES, 2017-2022

- Figure 44:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, UNITED STATES, 2017-2022

- Figure 45:

- MARKET SHARE OF MAJOR PLAYERS, %, UNITED STATES

US Turf and Ornamental Protection Industry Segmentation

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode.| Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment |

Need A Different Region or Segment?

Customize Now

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Turf and Ornamental crops in United States

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF