Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 13.47 Billion |

| Market Size (2031) | USD 20.06 Billion |

| Growth Rate (2026 - 2031) | 8.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Snack Bar Market Analysis by Mordor Intelligence

The United States snack bar market was valued at USD 12.44 billion in 2025 and estimated to grow from USD 13.47 billion in 2026 to reach USD 20.06 billion by 2031, at a CAGR of 8.30% during the forecast period (2026-2031). The increasing frequency of snacking among consumers is a key driver of this growth, with 88% of United States consumers consuming at least one snack daily and 37% of main meals now including a snack component. This trend highlights the evolving role of snacks in daily diets. The market is further shaped by the rising demand for snack bars that are high in protein and low in sugar, alongside a growing preference for minimally processed formulations based on fruits and nuts. Additionally, premiumization through smaller, more convenient pack sizes is influencing consumer purchasing behavior. Acquisition-driven consolidation, exemplified by Mars’s USD 35.9 billion acquisition of Kellanova, is intensifying competition within the market. However, regulatory costs linked to the United States Food and Drug Administration’s (FDA) 2028 front-of-package labeling mandate may pose challenges by compressing profit margins for brands that fail to comply. Furthermore, the expansion of online retail subscriptions, direct-to-consumer product bundles, and the functional positioning of snack bars—offering benefits such as energy enhancement, cognitive support, and digestive health—are unlocking new consumption occasions that extend beyond traditional breakfast and sports-nutrition scenarios.

Key Report Takeaways

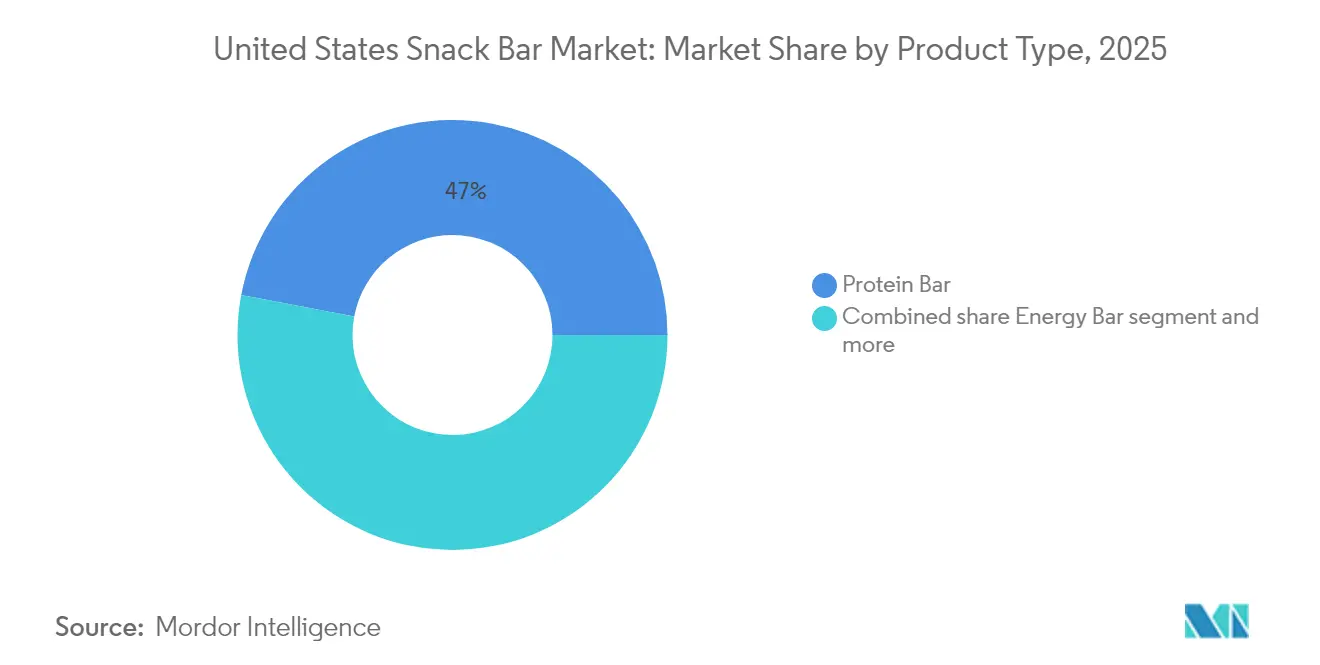

- By product type, protein bars led the United States snack bar market share with 47.02% in 2025, while fruit and nut bars are forecast to grow at a 9.29% CAGR to 2031.

- By ingredient base, nut-based formats captured 32.88% of the United States snack bar market size in 2025, whereas dairy and other protein blends are set to post the fastest 9.44% CAGR through 2031.

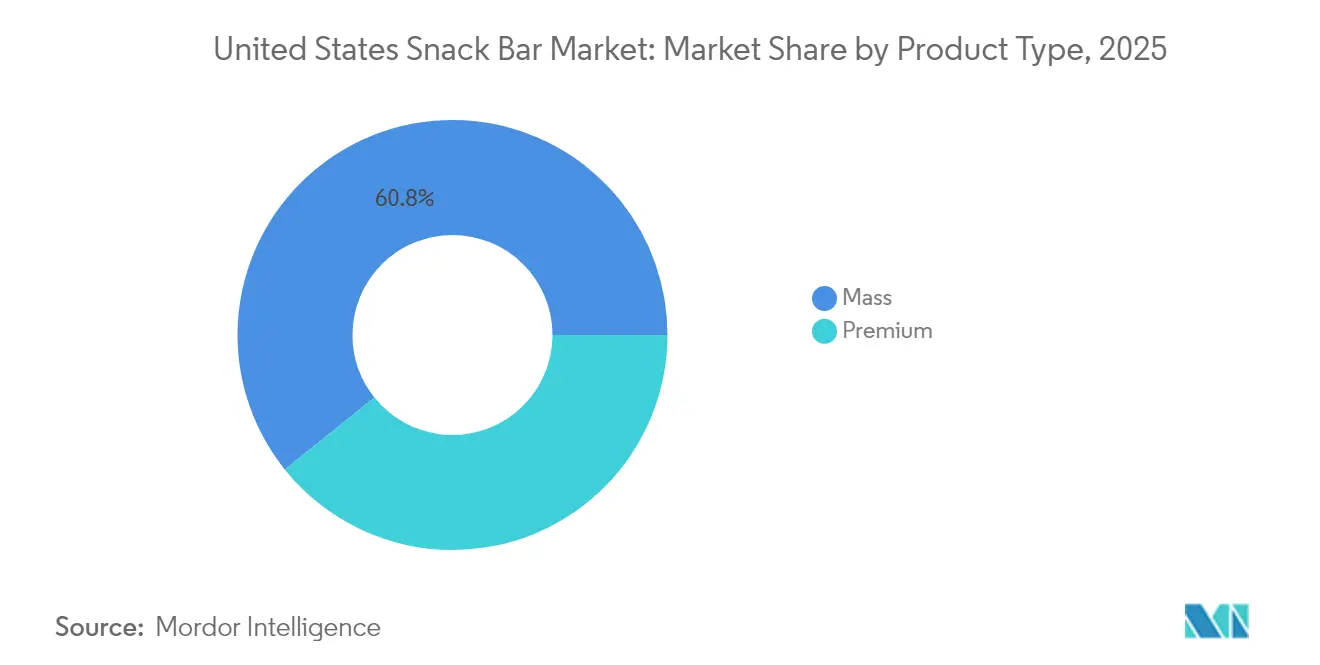

- By price tier, mass-market items held 60.75% revenue share in 2025, yet premium offerings are projected to expand at a 9.18% CAGR between 2026 and 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 40.88% of 2025 sales, but online retail is poised to achieve an 8.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Snack Bar Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and wellness trends emphasizing nutritious ingredients | +0.9% | National, concentrated in coastal metros and college towns | Medium term (2-4 years) |

| Increasing demand for high-protein, low-sugar, and clean-label products | +1.2% | National, with premium adoption in urban centers | Short term (≤ 2 years) |

| Popularity of fitness culture driving demand for energy and protein bars | +1.0% | National, strongest in Sun Belt and Mountain West states | Medium term (2-4 years) |

| Growing interest in organic and clean-label snack bars | +0.8% | National, early gains in Pacific Northwest and Northeast | Medium term (2-4 years) |

| Consumers' preference for sustainable and ethically sourced ingredients | +0.7% | National, led by Gen Z and Millennial cohorts | Long term (≥ 4 years) |

| Development of functional snack bars targeting cognitive and digestive health | +0.9% | National, initial traction in tech hubs and wellness communities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising Health and Wellness Trends Emphasizing Nutritious Ingredients

American consumers are redefining snacking as a means of nutrient delivery rather than indulgence, with energy cited as a primary motivation and mood enhancement increasingly sought through food choices. This evolving perspective has elevated snack bars from simple convenience items to essential platforms for functional nutrition. Active adults aged 18 to 45, who prioritize health-conscious decisions, are leading this trend by choosing better-for-you options at significantly higher rates compared to older demographics. Brands that incorporate whole grains, seeds, and ancient grains—such as quinoa, amaranth, and chia—are successfully capturing shelf space that was once dominated by traditional candy bars and cookies. The United States Food and Drug Administration (FDA) finalized its updated "healthy" nutrient-content claim in 2024, allowing snack bars with higher levels of unsaturated fats to qualify as long as they include nutrient-dense ingredients [1]Source: United States Food & Drug Administration, “FDA Finalizes Updated “Healthy” Nutrient Content Claim,” fda.gov. This regulatory change opens new pathways for reformulation, enabling manufacturers to align their products with both compliance requirements and evolving consumer expectations. Companies that take proactive steps to reformulate their products ahead of the 2028 front-of-package labeling deadline can avoid the reputational risks associated with "high in" warnings for saturated fat, sodium, or added sugars, which could discourage health-conscious shoppers from purchasing their products.

Increasing Demand for High-Protein, Low-Sugar, and Clean-Label Products

Protein bars maintained a significant market share in 2024, reflecting a growing consumer focus on transparency and macronutrient optimization. While 56% of Americans seek to increase protein intake, 67% also prioritize portion control, driving demand for compact products that provide 15 to 20 grams of protein within a 200-calorie limit. Clean-label claims, such as the absence of artificial colors, flavors, and preservatives, have become standard expectations. Certifications like Non-GMO (Non-Genetically Modified Organism) Project verification and USDA (United States Department of Agriculture) Organic certification act as trust indicators, often allowing brands to command higher price points. Abbott's Ensure Max Protein line, reformulated in 2024 to include 30 grams of protein and zero added sugar, highlights how established nutrition brands are adapting to snack-bar formats to meet the needs of on-the-go consumers. Alternative sweeteners, including allulose, monk fruit, and stevia, are increasingly replacing high-fructose corn syrup and cane sugar. This shift enables brands to reduce added sugars to below 5 grams per serving while maintaining taste, addressing a formulation challenge that has previously hindered broader adoption among casual snackers.

Popularity of Fitness Culture Driving Demand for Energy and Protein Bars

The integration of gym memberships, wearable fitness trackers, and social media wellness influencers has significantly contributed to the normalization of pre- and post-workout snacking, with 70% of consumers associating snack consumption with their fitness objectives. Energy bars, often fortified with caffeine, B vitamins, and electrolytes, are increasingly replacing traditional sports drinks and energy gels among endurance athletes and CrossFit enthusiasts. These individuals prioritize solid-food formats for their ability to provide sustained energy release during intense physical activities. Quest Nutrition's Hero bar, launched in 2024, contains 15 grams of protein and 4 grams of net carbohydrates, catering specifically to ketogenic dieters and low-carbohydrate consumers. This group represents a highly vocal and brand-loyal customer base. Retailers are responding to this trend by expanding dedicated "sports nutrition" aisles, which strategically group products such as bars, powders, and ready-to-drink shakes. This merchandising strategy not only increases the average basket size but also reinforces the functional and performance-oriented positioning of the category. Partnerships between energy bar brands and fitness chains—such as KIND's sampling programs at Equinox and SoulCycle—are fostering product trials among high-intent consumers. These consumers are typically willing to pay premium prices for formulations designed to enhance athletic performance and meet specific nutritional needs.

Growing Interest in Organic and Clean-Label Snack Bars

The United States Department of Agriculture (USDA) Organic certification and clean-label positioning have shifted from being niche differentiators to essential expectations for brands targeting millennial and Generation Z consumers. In 2024, organic snack bars outpaced the growth of their conventional counterparts, driven by increasing consumer concerns about pesticide residues, genetically modified organisms (GMOs), and synthetic additives. Nature's Bakery, a company that uses organic whole grains and fruit purees, has successfully leveraged its clean ingredient profile to secure distribution in school cafeterias and workplace vending machines, which prioritize allergen-free and minimally processed options to meet the growing demand for healthier and more transparent food choices. The Non-GMO Project's butterfly logo, a trusted and recognizable symbol, is featured on 30% of new bar launches, reflecting a strong supply chain commitment to sourcing non-GMO lecithin, glucose syrup, and natural flavors. Brands achieving both USDA Organic certification and Non-GMO verification can command retail prices 20% to 30% higher than conventional bars, despite challenges such as higher ingredient costs and limited availability of organic dates, nuts, and oats, which are particularly vulnerable to weather-related supply disruptions. Millennials and Generation Z, driven by sustainability, transparency, and health consciousness, prioritize value-based eating and demonstrate a strong willingness to pay premiums for USDA-certified organic products, fundamentally transforming expectations within the snack bar market [2]Source: Organic Trade Association, “Conscious Consumption: Younger Generations Fueling Growth in the Organic Industry,” ota.com.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory pressure on labeling and health claims | -0.6% | National, with compliance timelines extending to 2028 | Medium term (2-4 years) |

| Concerns about high sugar, unhealthy fats, and artificial ingredients | -0.8% | National, amplified by social media and nutrition advocacy groups | Short term (≤ 2 years) |

| High competition from traditional snacks and alternative snack options | -1.0% | National, most acute in convenience and mass-grocery channels | Short term (≤ 2 years) |

| Difficulty in balancing taste with health and nutritional value | -0.7% | National, affecting trial and repeat purchase rates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure on Labeling and Health Claims

The United States Food and Drug Administration (FDA)'s proposed front-of-package labeling rule, published in 2024, introduces a requirement for packaged foods to display "high in" warnings for saturated fat, sodium, or added sugars if these nutrients exceed specified thresholds. This regulation is expected to impose an annual cost of approximately USD 333 million on the snack-bar industry, covering expenses related to compliance, reformulation of products, and packaging redesign. Brands that fail to reformulate their products by the 2028 implementation deadline face significant risks, including potential backlash from consumers and the possibility of being de-listed by retailers. Supermarkets are increasingly curating their shelves to feature products that align with public health guidelines, further pressuring manufacturers to comply. Additionally, the updated "healthy" nutrient-content claim, finalized in 2024, permits snack bars to contain higher levels of unsaturated fats if they include nutrient-dense ingredients. However, meeting the stringent criteria—such as limits on saturated fat, sodium, and added sugars while ensuring the inclusion of meaningful amounts of food-group components—poses significant challenges. These requirements necessitate extensive research and development (R&D) efforts, leading to delays in product launches and increased costs. Smaller brands, often lacking dedicated regulatory affairs teams, bear a disproportionate burden, which widens the competitive gap in favor of multinational corporations like General Mills, Nestlé, and PepsiCo. These larger companies are better positioned to absorb compliance costs across their extensive product portfolios, giving them a distinct advantage in navigating the evolving regulatory landscape.

Concerns About High Sugar, Unhealthy Fats, and Artificial Ingredients

Consumer skepticism toward ultra-processed foods has grown, driven by social media influencers and nutrition advocates highlighting bars containing 15 to 20 grams of added sugar, partially hydrogenated oils, or synthetic preservatives such as butylated hydroxytoluene (BHT) and tert-butylhydroquinone (TBHQ). A 2024 Washington Post investigation into ultra-processed snacks further raised concerns, revealing that many "healthy" bars have calorie and sugar levels comparable to candy bars. This has diminished consumer trust and led some individuals to shift toward whole foods like nuts, seeds, and fresh fruit. Additionally, the increasing use of glucagon-like peptide-1 (GLP-1) receptor agonist medications, such as semaglutide and tirzepatide, has reduced snacking frequency among users by 75%. This demographic change has significantly impacted indulgent subcategories, including candy-coated granola bars and chocolate-dipped protein bars. To address these shifts, manufacturers must reformulate their products to align with evolving consumer definitions of "clean," which now often exclude artificial additives, refined sugars, seed oils, and isolated proteins perceived as overly processed.

Segment Analysis

By Product Type: Protein Bars Lead, Yet Fruit and Nut Bars Accelerate

Protein bars accounted for 47.02% of the market share in 2025, driven by consistent demand from fitness enthusiasts, weight-management consumers, and meal-replacement users. These consumers prioritize macronutrient density over ingredient simplicity, making protein bars a preferred choice for their dietary needs. The segment's dominance reflects its ability to cater to individuals seeking convenient, high-protein options that align with their active lifestyles and nutritional goals. However, fruit and nut bars are emerging as a strong contender, projected to grow at a compound annual growth rate (CAGR) of 9.29% from 2026 to 2031, the highest growth rate among all product types. This growth is fueled by a shift in consumer preferences toward minimally processed products that utilize natural ingredients such as dates, figs, and cashews as binders and sweeteners. These bars appeal to health-conscious individuals looking to avoid synthetic isolates and sugar alcohols commonly found in protein-focused products.

Energy bars, enriched with caffeine and B vitamins, continue to serve specific needs such as pre-workout energy boosts and mid-afternoon pick-me-ups. These products are designed to provide a quick and efficient source of energy for busy consumers. On the other hand, cereal bars, often positioned as convenient breakfast alternatives, are facing challenges. Declining cold-cereal consumption and increasing competition from portable breakfast options like oatmeal cups and Greek yogurt pouches have created headwinds for this segment. In response to evolving consumer demands, companies are innovating to retain market share. For instance, Quest Nutrition's 2024 launch of Hero bars, which combine 15 grams of protein with candy-bar-inspired flavors, demonstrates how established players are addressing the taste preferences of consumers while maintaining the nutritional benefits of protein bars. This strategy highlights the ongoing efforts to balance indulgence with health-focused attributes in the competitive snack market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Ingredient Base: Nut-Based Dominance Meets Dairy-Protein Innovation

Nut-based bars accounted for 32.88% of the ingredient-based segment in 2025, driven by the inclusion of almonds, cashews, and peanuts. These ingredients are valued for their ability to provide healthy fats, plant-based protein, and a satisfying texture, making them a popular choice among health-conscious consumers. Dairy and protein-based formulations are expected to grow at the fastest rate, with a compound annual growth rate (CAGR) of 9.44% through 2031. This growth is fueled by manufacturers incorporating whey protein isolates, casein, and milk protein concentrates into date-sweetened or oat-based formulations. These products cater to the increasing demand for clean-label and high-protein options while avoiding soy or pea protein, which some consumers perceive as less favorable due to concerns about taste and bioavailability. This trend highlights the evolving preferences of consumers who seek both nutritional benefits and superior taste profiles in their snack choices.

Granola and oat-based bars, a traditional subcategory, are facing stagnation as private-label products from brands such as Costco's Kirkland and Trader Joe's offer prices that are 20% to 30% lower than branded alternatives. This pricing pressure has compelled established players like Nature Valley and Quaker to differentiate their offerings by emphasizing organic certifications or incorporating functional ingredients such as chia seeds, flaxseed, and hemp hearts to justify their premium positioning. Meanwhile, date-based bars, popularized by brands like RXBAR and Larabar, occupy a premium niche but are constrained by the limited availability and price volatility of dates. Hybrid blends, which combine nuts, oats, dates, and dairy proteins, are emerging as a promising formulation that balances taste, texture, and nutritional profiles. However, these blends require advanced extrusion and baking technologies, leading to higher capital expenditures and creating significant barriers to entry for smaller brands. This dynamic underscores the importance of innovation and operational efficiency in maintaining competitiveness within the market.

By Price Tier: Mass Market Holds Share, Premium Gains Momentum

In 2025, mass-market bars accounted for 60.75% of sales, highlighting their role as a convenient, impulse-purchase option typically priced below USD 2.00 per unit. Premium tiers are expected to grow at a compound annual growth rate (CAGR) of 9.18% from 2026 to 2031, driven by brands focusing on smaller pack sizes, functional ingredients, and sustainability claims to support retail prices ranging from USD 2.50 to USD 4.00 per bar. Companies such as PepsiCo, Mondelēz, and Campbell's have introduced smaller stock-keeping units (SKUs)—often 20% to 30% lighter than traditional formats—offered at lower absolute prices but with higher per-ounce costs. This strategy appeals to budget-conscious consumers while maintaining profitability.

The divide between mass-market and premium tiers reflects broader trends in the grocery market, where mid-tier brands face challenges like margin compression and declining volumes as consumers either opt for private-label products or upgrade to artisanal offerings. Mass-market players need to innovate in areas such as flavor, texture, and functional claims to avoid becoming commoditized. However, they are constrained by rising ingredient costs, including nuts, oats, and cocoa, which limit reformulation budgets. Meanwhile, premium brands can pass on higher input costs to consumers but must ensure their products match the taste quality of indulgent snacks to justify premium pricing and encourage repeat purchases.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Supermarkets Anchor, Online Retail Surges

Supermarkets and hypermarkets accounted for 40.88% of the distribution share in 2025. These channels utilized their extensive shelf space, promotional displays, and checkout impulse sections to drive product trials and repeat purchases. Online retail is projected to grow at a compound annual growth rate (CAGR) of 8.86% through 2031. This growth is supported by initiatives such as Amazon's Subscribe & Save, brand-specific websites, and specialty online retailers like Thrive Market, which emphasize clean-label and allergen-free product offerings. In the United States, e-commerce is expected to account for over 16% of total retail sales in 2025. With its growth outpacing overall retail expansion, online retail is poised to play an increasingly significant role .

Convenience stores, while contributing smaller overall sales, achieve high per-unit margins and cater to on-the-go consumption needs. However, their limited shelf space typically prioritizes established brands with strong distributor relationships and promotional backing. Other distribution channels, including club stores, natural-food retailers, vending machines, and workplace micro-markets, collectively account for the remaining share. These channels address specific consumer needs, such as bulk purchasing, specialty diets, and workplace snacking, requiring tailored assortments and packaging formats.

Geography Analysis

The United States snack bar market reflects unique regional consumption patterns shaped by demographic factors, lifestyle choices, and distribution networks. In the Pacific and Mountain West regions, protein and energy bars see the highest per-capita consumption. This trend is driven by a strong culture of outdoor recreation, higher gym membership rates, and younger populations focused on fitness and active lifestyles. Notably, 70% of consumers in these regions associate snacking with fitness goals, particularly in states like Colorado, Utah, California, and Washington. These preferences highlight the growing importance of health-conscious snacking in these areas.

Coastal metropolitan areas such as San Francisco, Seattle, Boston, and New York have been early adopters of organic, clean-label, and functional snack bars. Certifications like United States Department of Agriculture (USDA) Organic and Non-GMO (Genetically Modified Organism) Project Verified are key purchase drivers for affluent, health-conscious consumers in these cities. Meanwhile, the Northeast benefits from a dense network of retail outlets and high foot traffic in convenience stores and specialty natural-food retailers. These channels support the sale of premium-priced bars that emphasize transparent sourcing and sustainability claims, catering to the preferences of urban consumers.

In the Southeast, where traditional snacks like cookies and crackers have historically dominated, demand for protein bars is rising. This shift is influenced by increasing obesity rates and diabetes prevalence, which are driving interest in portion-controlled, macronutrient-optimized snack formats that support weight management and blood sugar regulation. The Midwest presents a mixed opportunity, with urban centers like Chicago, Minneapolis, and Columbus aligning with coastal trends toward premium and functional bars. However, rural and exurban areas remain focused on mass-market cereal and granola bars, distributed primarily through Walmart, Dollar General, and regional grocery chains. The Southwest, encompassing Texas, Arizona, and New Mexico, is experiencing rapid population growth and rising Hispanic household incomes. This has led to demand for bilingual packaging, flavors like dulce de leche and horchata, and distribution through Hispanic-focused retailers such as H-E-B and Fiesta Mart. Texas, with the largest convenience-store footprint in the United States, is a critical market for single-serve, impulse-oriented bars competing with candy, jerky, and salty snacks for checkout placement.

Competitive Landscape

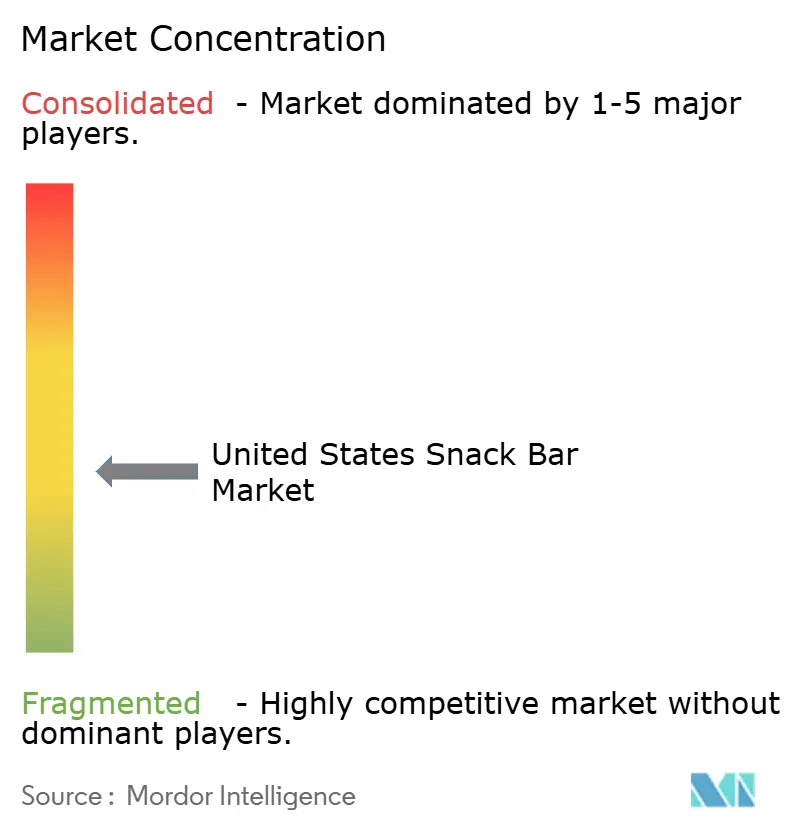

The United States snack bar market is moderately fragmented, with multinational companies such as General Mills, Nestlé, PepsiCo, Mondelēz International, and Mars competing alongside emerging players like Quest Nutrition, KIND Snacks, RXBAR, and GoMacro. These smaller companies have reshaped consumer expectations by focusing on clean labels, functional ingredients, and transparent sourcing. Mars's USD 35.9 billion acquisition of Kellanova, finalized in the first half of 2025, consolidated ownership of brands such as RXBAR, Nutri-Grain, Rice Krispies Treats, and MorningStar Farms. This acquisition created a diverse portfolio spanning protein bars, cereal bars, and plant-based snacks. The deal reflects a strategic shift toward healthier product platforms that can command premium pricing and compete against private-label alternatives. However, it also introduces challenges in integrating supply chains, distribution networks, and innovation processes across Mars's existing and newly acquired brands.

There are significant opportunities in functional snack subcategories, including cognitive support, digestive health, and stress management. Established players have been slow to incorporate ingredients such as adaptogens, probiotics, and nootropics at clinically effective doses. This has created space for startups that can back their health claims with clinical evidence while effectively navigating the United States Food and Drug Administration (FDA) structure-function regulations.

Technological advancements are transforming the competitive landscape, with brands using artificial intelligence (AI) for flavor optimization, blockchain for traceability, and precision fermentation to stand out in terms of taste, transparency, and sustainability. For instance, PepsiCo's regenerative agriculture program sources oats from farms employing cover cropping and reduced tillage practices. This initiative not only delivers environmental benefits but also supports marketing narratives that resonate with environmentally conscious consumers.

United States Snack Bar Industry Leaders

1440 Foods Company

Abbott Laboratories

Mondelēz International Inc.

Ferrero International SA

General Mills Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: JiMMYBAR! Functional Protein, a family-run brand based in Illinois, launched its creatine protein bar. Available nationwide through retailers such as Walmart, Amazon, and TikTok Shop, the bar provides 20g of protein, 5g of creatine, and 4g of sugar, offered in Double Fudge Brownie and Chocolate Peanut Butter flavors.

- October 2025: GHOST launched its first-ever protein bar in partnership with General Mills, featuring a distinctive two-stick layered format inspired by classic candy bars. The bars offer 20g protein, 2g sugar, and 250-270 calories in three flavors.

- June 2025: One Brands collaborated with The Hershey Company to introduce the One x Hershey's Double Chocolate protein bar in the United States market. The product provides 18 grams of protein and contains only 1 gram of sugar, incorporating authentic Hershey's cocoa and chocolate chips. This partnership aims to cater to on-the-go consumers looking for convenient, nutritious snacks with a premium chocolate flavor.

United States Snack Bar Market Report Scope

Cereal Bar, Fruit & Nut Bar, Protein Bar are covered as segments by Confectionery Variant. Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others are covered as segments by Distribution Channel.By Product Type

| Cereal Bar |

| Energy Bar |

| Protein Bar |

| Fruit and Nut Bar |

By Ingredient Base

| Nut-based bars |

| Granola/Oat-based |

| Date-based |

| Dairy/Protein-based |

| Hybrid blends |

| Other Forms |

By Price Tier

| Mass |

| Premium |

By Distribution Channel

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

| By Product Type | Cereal Bar |

| Energy Bar | |

| Protein Bar | |

| Fruit and Nut Bar | |

| By Ingredient Base | Nut-based bars |

| Granola/Oat-based | |

| Date-based | |

| Dairy/Protein-based | |

| Hybrid blends | |

| Other Forms | |

| By Price Tier | Mass |

| Premium | |

| By Distribution Channel | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels |

Need A Different Region or Segment?

Customize Now

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF