| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| CAGR | 4.00 % |

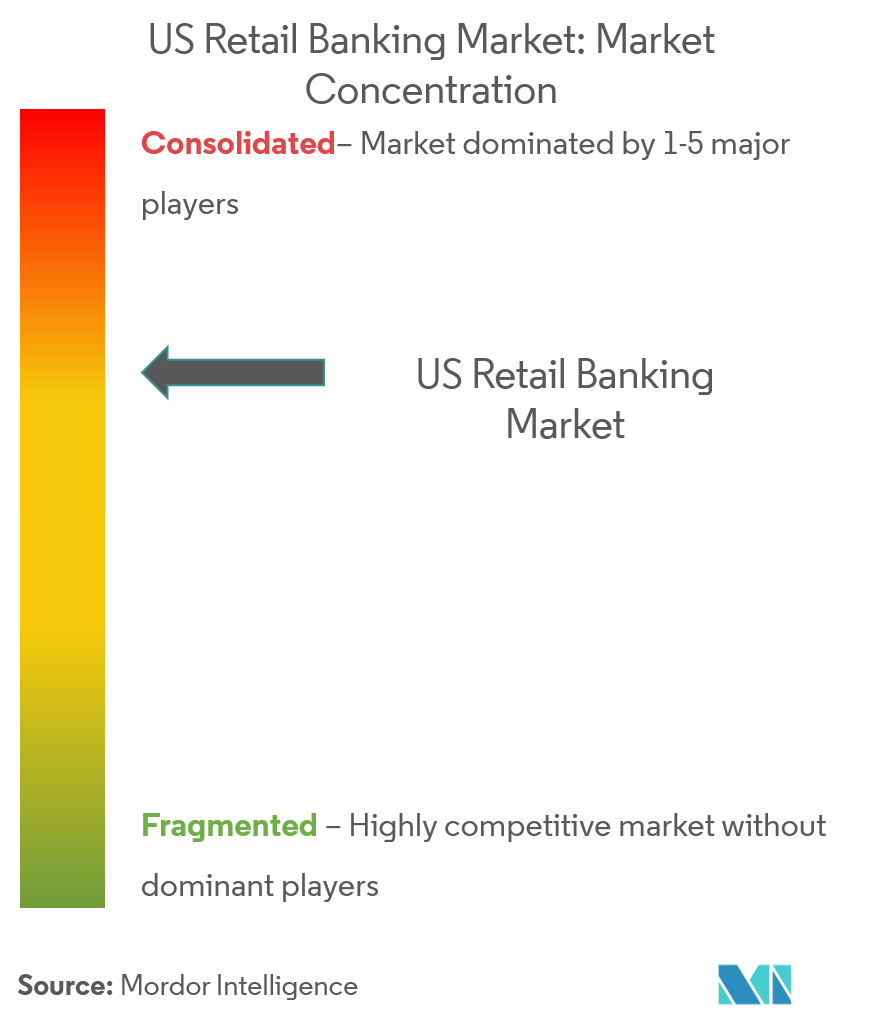

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

US Retail Banking Market Analysis

The US Retail Banking Market is expected to register a CAGR of 4% during the forecast period.

The US retail banking landscape is experiencing a fundamental shift in consumer behavior and service delivery models. Digital banking channels have become the primary banking interface, with recent studies showing that 82% of US consumers now primarily use online banking services for their financial needs. This transformation has prompted traditional banks to accelerate their digital initiatives, with many institutions implementing advanced analytics and artificial intelligence to enhance customer experience. The integration of open banking APIs and automated routing capabilities has enabled banks to create seamless customer journeys and determine optimal delivery options for each situation, leading to faster service delivery and higher conversion rates.

The payments landscape has evolved significantly, driven by changing consumer preferences and technological advancements. According to recent industry data, 77% of consumers now report having a debit card, with 67% using it for at least one transaction monthly, highlighting the growing preference for digital payment methods. Banks are responding by expanding their digital wallet offerings and implementing sophisticated fraud prevention systems. The rise of real-time payments and the integration of blockchain technology are further reshaping transaction capabilities, with many institutions investing in modernizing their payment infrastructure to meet evolving customer expectations.

Customer experience has emerged as a critical differentiator in retail banking, with personalization becoming increasingly important. Industry research indicates that 66% of Millennials are willing to share personal data in exchange for more personalized banking services, driving investments in data analytics and customer relationship management systems. Banks are leveraging artificial intelligence and machine learning to deliver tailored financial advice, product recommendations, and personalized user experiences across digital platforms. This focus on personalization has contributed to improved customer satisfaction levels, with credit card satisfaction reaching an all-time high according to recent J.D. Power studies.

The traditional branch-based distribution model is undergoing significant transformation as banks adapt to changing consumer preferences. Financial institutions are implementing intelligent routing of customer requests between digital and assisted channels, shifting from traditional contact centers to comprehensive customer care platforms. Banks are optimizing their remaining physical branches while expanding their digital banking capabilities, creating an omnichannel experience that combines the efficiency of digital services with the personal touch of human interaction when needed. This hybrid approach allows banks to maintain customer relationships while reducing operational costs and improving service delivery efficiency.

US Retail Banking Market Trends

Digital Transformation and Fintech Integration

The retail banking landscape is experiencing a fundamental shift driven by digital transformation and fintech integration. Digital lenders have more than doubled their market share as consumers across various credit spectrums increasingly turn to digital banking providers for their banking needs. This transformation is further evidenced by the fact that 55% of business professionals have identified digital payments as their top B2B payments priority, highlighting the growing importance of electronic banking solutions in the commercial banking sector. Major US banks are responding to this trend by heavily investing in retail fintech competitors to form strategic partnerships, allowing them to leverage innovative technologies while maintaining their competitive edge.

The integration of specialized fintech APIs has enabled traditional banks to expand beyond their core products and offer enhanced services to meet evolving customer demands. This technological advancement has particularly resonated with younger generations, with studies showing that Millennials and Gen Z demonstrate significantly higher interest in digital retail banking solutions. The transformation extends to payment technologies as well, with businesses increasingly adopting real-time payments, tap-and-go solutions, and even exploring cryptocurrency options to improve liquidity management, enable quicker supplier invoice settlements, and reduce fraud exposure.

Understand The Key Trends Shaping This Market

Download PDF

Evolving Consumer Preferences and Demographics

Consumer preferences in retail banking are undergoing a significant transformation, driven largely by demographic shifts and changing expectations around personalized services. Nearly 66% of Millennials have expressed willingness to share personal data in exchange for more personalized consumer financial services, indicating a fundamental shift in how younger generations view the relationship between privacy and service quality. This demographic shift is reshaping how banks approach customer engagement, with a growing emphasis on tailored financial solutions and personalized banking experiences that resonate with younger, tech-savvy consumers.

The evolution of consumer behavior is particularly evident in channel preferences, with internet banking emerging as the predominant method of banking interaction. Traditional branch-based distribution models are being challenged as consumers increasingly demand seamless digital experiences similar to those they encounter in other aspects of their lives, such as shopping and entertainment. Banks are responding by developing omni-channel strategies that combine digital convenience with human engagement when needed, creating a more flexible and responsive banking environment that caters to diverse consumer preferences across different age groups and technological comfort levels.

Financial Innovation and Market Accessibility

Financial innovation is dramatically reshaping market accessibility in retail banking, with digital technologies breaking down traditional barriers to financial services. The emergence of digital banks and fintechs offering faster and more cost-effective services than traditional incumbents has revolutionized banking accessibility. These innovations are particularly significant given that approximately 2.5 billion adults worldwide still transact only in cash, representing a massive opportunity for digital financial services to expand market reach and promote financial inclusion.

The innovation landscape is further characterized by the development of sophisticated payment technologies and banking solutions. Banks are increasingly focusing on implementing intelligent routing of customer requests between digital and assisted channels, which can generate up to a 25% increase in profitability. This technological advancement is complemented by the embedding of distribution services on partner platforms through APIs, creating new avenues for customer engagement and service delivery. The innovation drive is also evident in the transformation of contact centers into customer care platforms, representing a fundamental shift in how banks interact with and serve their customers.

Regulatory Environment and Open Banking Initiatives

The regulatory landscape in US retail banking is uniquely characterized by its industry-driven approach to open banking, contrasting with other regions where regulatory mandates drive adoption. This market-led approach has created opportunities for banks to establish their own technical and customer experience standards for data-sharing and APIs, allowing for more flexible and innovative solutions. The evolution of open banking in the United States is particularly significant as it enables banks to accelerate their digital transformation efforts and explore new business models while maintaining control over implementation timelines and strategies.

The regulatory environment is further shaped by consumer attitudes toward data privacy and security, with surveys indicating that while one in five US consumers find open banking valuable, there are significant concerns about personal data protection. This has led to a balanced approach where banks must navigate between innovation and consumer protection, particularly in areas of data sharing and third-party access. The regulatory framework is increasingly focusing on establishing technical standards that ensure secure data sharing while promoting innovation, creating an environment that supports both technological advancement and consumer protection in retail banking services.

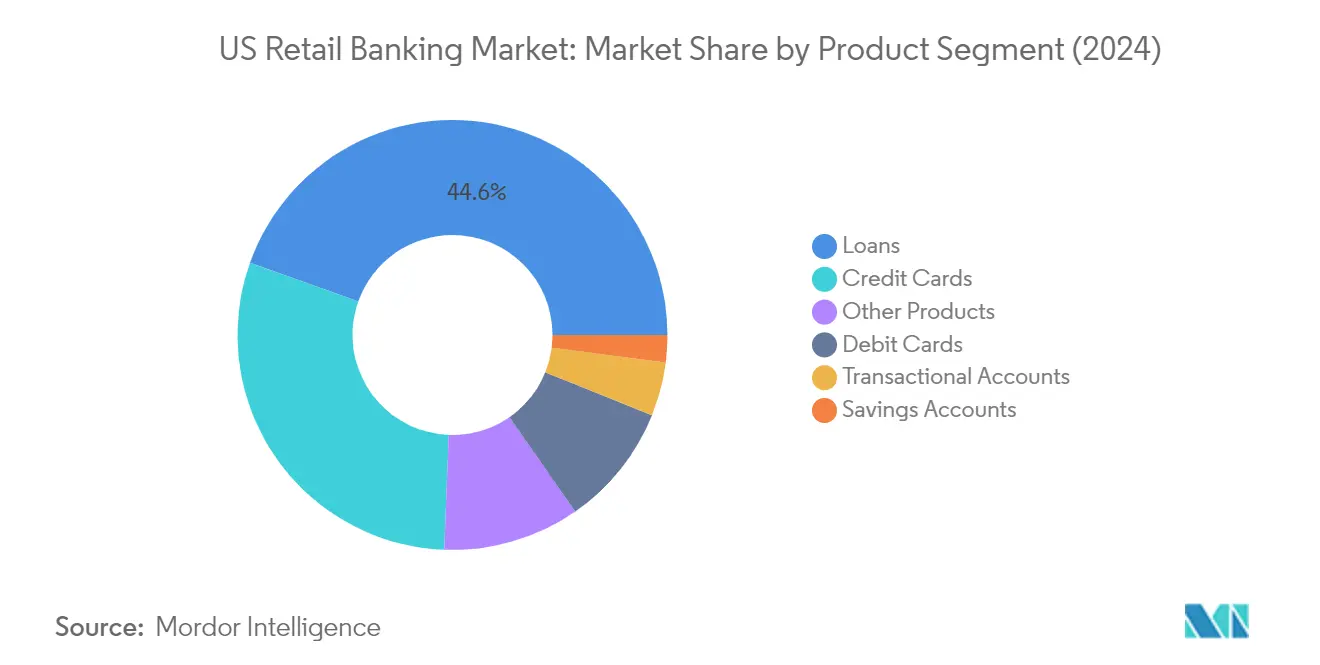

Segment Analysis: By Product

Loans Segment in US Retail Banking Market

The loans segment continues to dominate the US retail banking market, commanding approximately 45% market share in 2024, representing the largest product category with a value of USD 377.23 billion. This substantial market position is driven by the diverse portfolio of loan products, including auto loans, home loans, mortgages, and personal loans, that cater to various consumer needs. The segment's strength is particularly evident in the mortgage industry, where loans are treated as commercial paper, allowing lenders to convey and assign them freely, thereby maintaining liquidity in the market. The robust performance is further supported by the increasing demand from both new and existing customers, particularly in residential mortgages and consumer finance sectors. The segment's leadership position is reinforced by banks' strategic focus on maintaining strong credit quality while expanding their loan portfolios across different categories to meet evolving consumer needs.

Savings Accounts Segment in US Retail Banking Market

The savings accounts segment has emerged as the fastest-growing product category in the US retail banking market, with an expected growth rate of approximately 6% during 2024-2029. This accelerated growth is primarily driven by the shift towards relationship-based savings products and the increasing adoption of online savings accounts. The segment's expansion is further supported by banks' strategic initiatives to offer competitive interest rates and innovative digital banking features that enhance customer experience. Online-only personal savings accounts are particularly gaining traction, yielding significantly higher returns compared to their branch-based counterparts. The growth momentum is also sustained by banks' efforts to develop specialized savings products for different customer segments, including high-yield savings accounts and goal-based savings solutions that cater to specific customer needs and preferences.

Remaining Segments in US Retail Banking Market

The US retail banking market encompasses several other significant product segments, including credit cards, debit cards, transactional accounts, and other banking products. Credit cards represent a substantial portion of the market, offering various rewards programs and benefits to attract and retain customers. Debit cards continue to be an essential banking tool, particularly popular among younger demographics who prefer direct access to their funds. Transactional accounts serve as the fundamental banking relationship product, providing basic banking services and payment capabilities. Other products, including certificates of deposits and forex products, play a complementary role in providing diverse financial solutions to meet varying customer needs and preferences. Each of these segments contributes uniquely to the overall market dynamics, reflecting the evolving preferences of consumers and technological advancements in banking services.

Segment Analysis: By Channel

Direct Sales Segment in US Retail Banking Market

Direct sales continue to dominate the US retail banking market, commanding approximately 74% of the total market share in 2024. This channel encompasses branch sales, direct digital channels through hybrid methods, and tele-caller sales channels for retail banking products and services. The segment's strong performance is driven by the increasing adoption of digital banking solutions, with banks investing heavily in enhancing their direct-to-consumer platforms. The transformation of traditional branch-based services to digital-first experiences has strengthened this segment's position, as consumers increasingly prefer seamless, integrated banking solutions. Major banks have responded by developing sophisticated mobile applications, online banking platforms, and AI-powered customer service solutions to maintain their competitive edge in direct sales channels.

Distributor Segment in US Retail Banking Market

The distributor segment has emerged as the fastest-growing channel in the US retail banking market, with projections indicating robust growth of approximately 8% during 2024-2029. This growth is primarily driven by banks' strategic partnerships with fintech companies, digital platforms, and third-party service providers. The segment's expansion reflects the industry's shift towards more diverse distribution models that extend beyond traditional banking channels. Financial institutions are increasingly leveraging partnerships with e-commerce platforms, digital marketplaces, and technology companies to reach new customer segments and deliver innovative banking solutions. The integration of banking services into non-banking platforms and the rise of embedded finance solutions have created new opportunities for distributors to facilitate banking services, contributing to the segment's accelerated growth trajectory.

US Retail Banking Industry Overview

Top Companies in US Retail Banking Market

The US retail banking landscape is dominated by major players including JPMorgan Chase, Bank of America, Wells Fargo, Citigroup, and US Bank, who are driving innovation through digital transformation initiatives. These institutions are increasingly collaborating with fintech companies to enhance their digital capabilities and customer experience, while simultaneously maintaining their traditional branch networks strategically. The focus has shifted towards developing omnichannel experiences, with significant investments in mobile banking platforms, artificial intelligence, and data analytics capabilities. Banks are also expanding their product portfolios through strategic partnerships and internal innovation labs, particularly in areas like digital payments, wealth management, and personalized retail financial services. Market leaders are demonstrating operational agility by optimizing their branch banking networks while investing in digital infrastructure, reflecting a balanced approach between traditional banking and digital banking channels.

Consolidation and Innovation Drive Market Evolution

The US retail banking market exhibits a high level of consolidation, with the top four banks controlling more than half of the total banking assets in the country. The market structure is characterized by a mix of large national banks, regional players, and emerging digital-only challengers, creating a dynamic competitive environment. Traditional banks are increasingly facing competition from fintech companies and tech giants entering the financial services space, leading to a surge in strategic partnerships and acquisitions. The market has witnessed significant merger and acquisition activity, exemplified by deals like the merger of BB&T and SunTrust to form Truist Bank, indicating a trend toward consolidation among regional banks to achieve scale and competitive advantage.

The competitive dynamics are evolving with the rise of digital banking platforms and non-traditional financial service providers. Large banks are leveraging their extensive resources and established customer relationships to maintain market dominance, while regional banks are focusing on specialized services and local market expertise. The industry is seeing increased collaboration between traditional banks and fintech companies, as established players seek to enhance their technological capabilities and digital offerings. This has led to a hybrid competitive landscape where traditional banking strengths are being combined with digital innovation to create new value propositions for customers.

Digital Innovation Key to Future Success

Success in the retail banking market increasingly depends on the ability to deliver seamless digital banking experiences while maintaining personal relationships with customers. Banks must focus on developing robust digital platforms that can compete with fintech offerings while leveraging their established trust and regulatory compliance capabilities. The market is seeing a shift towards platform-based banking models, where banks are creating ecosystems that integrate various financial services and third-party offerings. Regulatory changes, particularly around open banking and data sharing, are creating new opportunities for innovation while also presenting challenges for maintaining competitive advantages.

Future market leaders will need to excel in data analytics and personalization while maintaining strong cybersecurity measures and regulatory compliance. Banks must balance investment in digital transformation with maintaining operational efficiency and managing risk. The ability to adapt to changing customer preferences, particularly among younger generations who prefer direct banking solutions, will be crucial for maintaining market share. Success will also depend on effectively managing the transition from traditional banking models to digital-first approaches while maintaining customer trust and satisfaction. The competitive landscape will continue to evolve as regulatory frameworks adapt to new technologies and business models, potentially creating opportunities for both incumbents and new entrants.

US Retail Banking Market Leaders

-

PNC Financial Services

-

Bank of America

-

US Bank

-

JP Morgan Chase and Co.

-

Wells Fargo

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

US Retail Banking Market News

- In May 2021, HSBC announced that it is exiting the retail and small business banking market in the United States, in line with its strategy to refocus on corporate and investment banking in Asia.

- In November 2020, Wells Fargo announced a new solution to help business customers eliminate paper checks by using one-time virtual card numbers to digitally pay invoices through the WellsOne Virtual Card Payments service.

US Retail Banking Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Trends Shaping the US Retail Banking Market

- 4.3 Consumer Behavior and Loyalty Analysis

- 4.4 Government Regulations And Industry Policies

- 4.5 Fintech Disruption in the US Retail Banking Market

- 4.6 Affect of Retail Banking on the US Economy

- 4.7 Recent Developments in the Market

- 4.8 The Future of US Retail Banking Distribution

-

4.9 Market Drivers

- 4.9.1 Next generation technologies

- 4.9.2 Optimized physical distribution: Analytics and workforce fluidity

- 4.9.3 Developing an omnichannel workforce

-

4.10 Market Restraints

- 4.10.1 Big Tech is a growing disintermediation threat

-

4.11 Porters 5 Force Analysis

- 4.11.1 Threat of New Entrants

- 4.11.2 Bargaining Power of Buyers/Consumers

- 4.11.3 Bargaining Power of Suppliers

- 4.11.4 Threat of Substitute Products

- 4.11.5 Intensity of Competitive Rivalry

- 4.12 Impact of Covid 19 on the Market

5. MARKET SEGMENTATION

-

5.1 By Product

- 5.1.1 Transactional Accounts

- 5.1.2 Savings Accounts

- 5.1.3 Debit Cards

- 5.1.4 Credit Cards

- 5.1.5 Loans

- 5.1.6 Other Products

-

5.2 By Channel

- 5.2.1 Direct Sales

- 5.2.2 Distributor

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Mergers & Acquisitions

-

6.3 Company Profiles

- 6.3.1 JPMorgan Chase & Co

- 6.3.2 Bank of America Corp.

- 6.3.3 Wells Fargo & Co.

- 6.3.4 Citigroup Inc.

- 6.3.5 U.S. Bancorp

- 6.3.6 Truist Bank

- 6.3.7 PNC Financial Services Group Inc.

- 6.3.8 TD Group US Holdings LLC

- 6.3.9 Bank of New York Mellon Corp.

- 6.3.10 Capital One Financial Corp.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

US Retail Banking Industry Segmentation

Retail banking, also known as consumer banking or personal banking, is banking that provides financial services to individual consumers rather than businesses. Retail banking is a way for individual consumers to manage their money, have access to credit, and deposit their money in a secure manner. Services offered by retail banks include checking and savings accounts, mortgages, personal loans, credit cards, and certificate of deposit (CDs).The report offers a complete background analysis of the US retail banking market, including an assessment of the parental market, emerging trends by segments and regional markets, significant changes in market dynamics, and market overview.

| By Product | Transactional Accounts |

| Savings Accounts | |

| Debit Cards | |

| Credit Cards | |

| Loans | |

| Other Products | |

| By Channel | Direct Sales |

| Distributor |

Need A Different Region or Segment?

Customize Now

US Retail Banking Market Research FAQs

What is the current US Retail Banking Market size?

The US Retail Banking Market is projected to register a CAGR of 4% during the forecast period (2025-2030)

Who are the key players in US Retail Banking Market?

PNC Financial Services, Bank of America, US Bank, JP Morgan Chase and Co. and Wells Fargo are the major companies operating in the US Retail Banking Market.

What years does this US Retail Banking Market cover?

The report covers the US Retail Banking Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the US Retail Banking Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

US Retail Banking Market Research

Mordor Intelligence delivers a comprehensive analysis of the retail banking sector. We combine expertise in traditional banking with deep insights into the transformation of digital banking. Our extensive research covers the full spectrum of banking services. This includes personal banking, consumer banking, and electronic banking solutions. The report provides a detailed examination of online banking trends and mobile banking adoption. It also explores the evolution of branch banking operations, offering stakeholders a complete view of both direct banking and internet banking developments.

This detailed market analysis benefits stakeholders across retail financial services, consumer financial services, and retail lending segments. The report, available as an easy-to-download PDF, examines crucial areas including digital payments, consumer lending, and deposit services. It also covers the infrastructure of ATM services. Our research encompasses emerging retail fintech innovations and retail payment services. It highlights the transformation toward digital retail banking, providing actionable insights for both individual banking providers and B2C banking institutions. The analysis particularly focuses on the integration of commercial banking solutions within the retail sector, offering valuable perspectives on the evolution of banking services.