Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

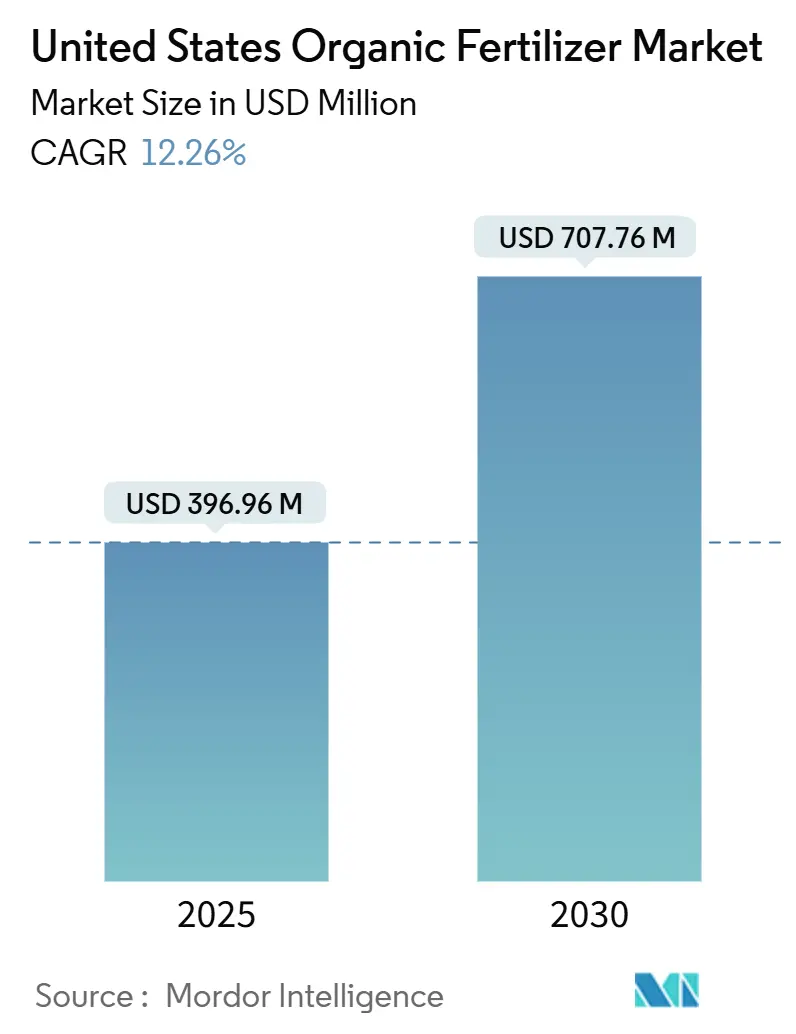

| Market Size (2025) | USD 396.96 Million |

| Market Size (2030) | USD 707.76 Million |

| Growth Rate (2025 - 2030) | 12.26% CAGR |

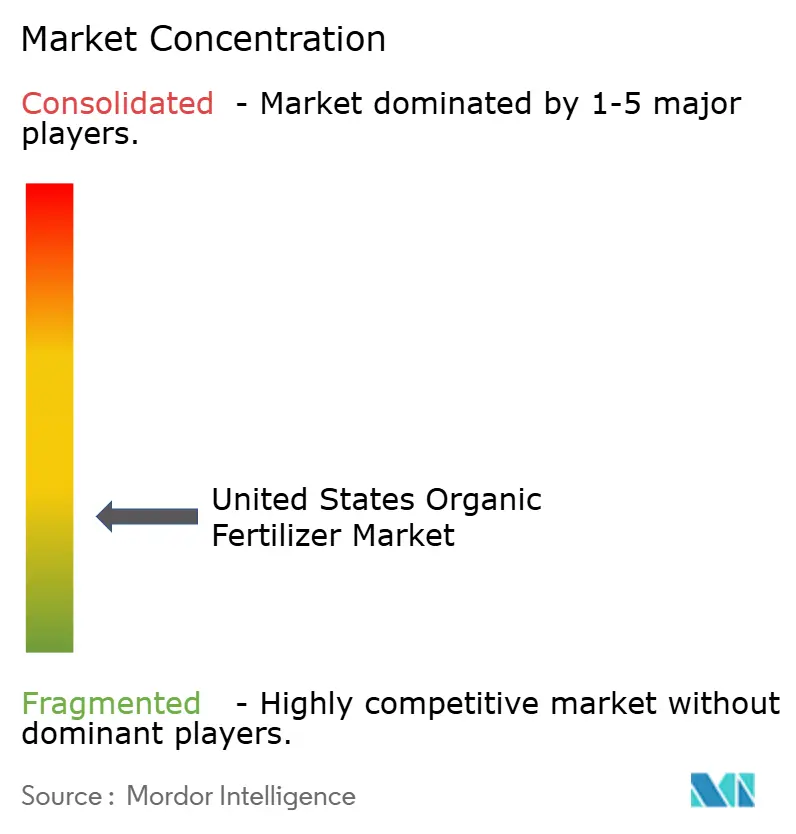

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Organic Fertilizer Market Analysis by Mordor Intelligence

The United States organic fertilizer market size is valued at USD 396.96 million in 2025 and is forecast to reach USD 707.76 million by 2030, advancing at a 12.26% CAGR. Federal cost-share programs that now reimburse up to 75% of organic input expenses, a steady 5% annual expansion in certified organic farmland, and organic food sales that doubled to USD 67 billion between 2014 and 2024 collectively anchor this uptick. Technology adoption, notably anaerobic digesters that convert livestock manure into pathogen-free digestate, cuts production risks while creating new revenue streams, a shift that strengthens farmer confidence in premium inputs. Carbon-credit incentives running at USD 15–30 per metric ton of compost add an extra income layer for producers who apply high-quality organic amendments. Supply growth remains brisk even as state pathogen rules push testing costs higher, signaling a market that rewards compliant scale players yet leaves space for nimble regional specialists.

Key Report Takeaways

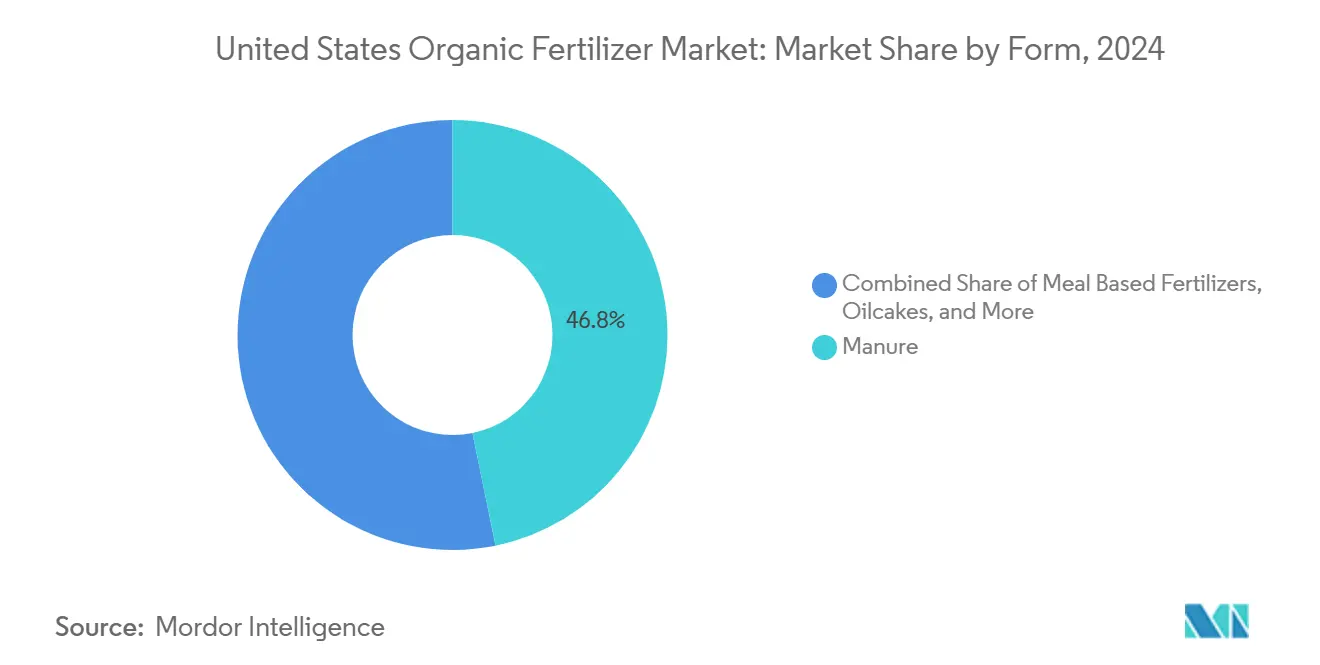

- By form, manure-based products led with 46.8% of the United States organic fertilizer market share in 2024 and are projected to climb at a 12.5% CAGR through 2030.

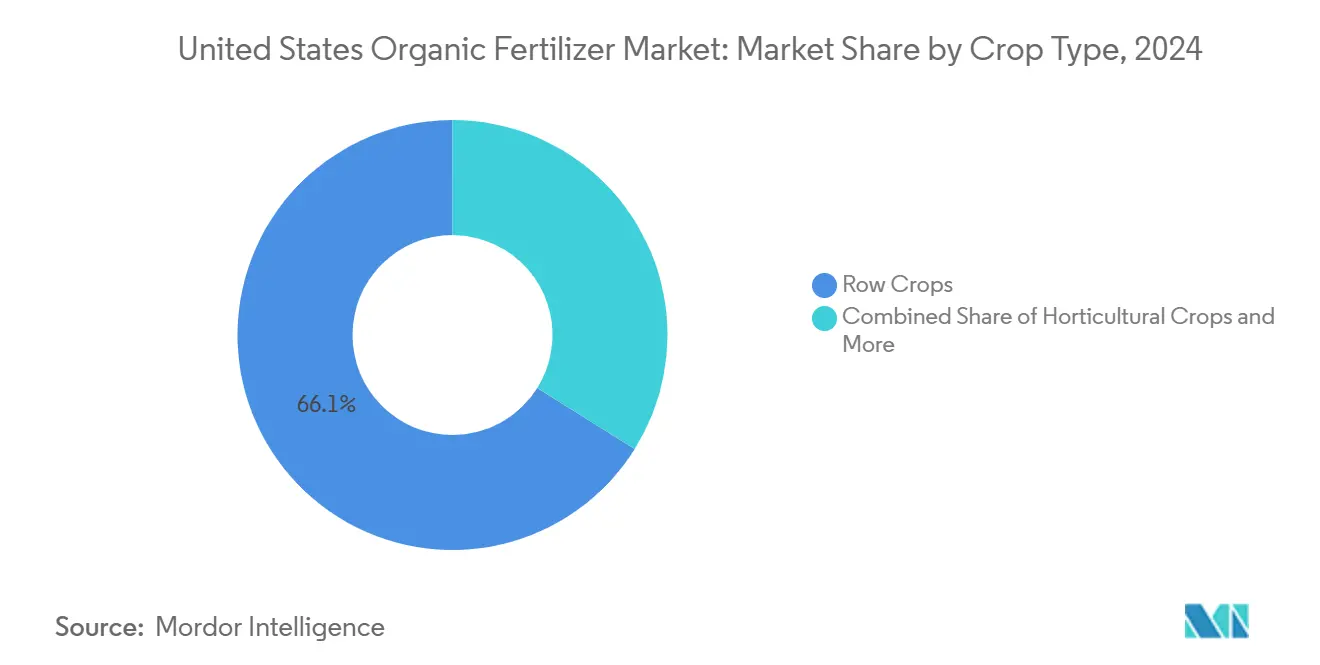

- By crop type, row crops accounted for 66.1% of the United States organic fertilizer market size in 2024 and are set to expand at a 12.5% CAGR to 2030.

United States Organic Fertilizer Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of Certified Organic Farmland | +2.10% | California, Iowa, and Wisconsin | Medium term (2-4 years) |

| Rising Consumer Demand for Chemical-Free Produce | +2.80% | Northeast and West Coast | Long term (≥ 4 years) |

| Federal Cost-Share Incentives for Transitioning Farms | +1.90% | Midwest corn belt | Short term (≤ 2 years) |

| Expansion of Organic Livestock Operations | +1.40% | Wisconsin, California, and New York | Medium term (2-4 years) |

| Carbon-Credit Monetization for Compost Use | +1.60% | California, Northeast, and Pacific Northwest | Long term (≥ 4 years) |

| On-Farm Bio-Digester Adoption Generating High-Value Digestate | +1.30% | Wisconsin, California, Vermont, and Pennsylvania | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rapid Growth of Certified Organic Farmland

Certified organic acreage reached 5.6 million acres in 2024, up 5.2% year over year, far surpassing the 0.8% rise in conventional farmland [1]Source: USDA Economic Research Service, “Organic Agriculture,” ers.usda.gov. New acreage concentrates in California and Montana yet shows the sharpest gains in Midwest corn and soybean zones where export premiums justify conversion costs. The United States Department of Agriculture (USDA) Organic Transition Initiative extends crop-insurance tools and risk-sharing grants that cushion producers during the mandatory three-year no-synthetic input window. Layered state aid, such as Iowa’s 75% certification reimbursement, magnifies the pull, creating a pipeline of transitioning acres that will depend exclusively on approved nutrient sources. This land expansion compounds fertilizer demand because transitioning ground often needs heavier organic applications to restore soil biology and meet nutrient needs without synthetic supplements. With more than 15,000 farms presently in conversion, baseline consumption of organic inputs is set to climb steadily through the medium term.

Rising Consumer Demand for Chemical-Free Produce

Organic food spending grew to USD 67 billion in 2024, driven mainly by health-focused millennials and Gen Z shoppers willing to absorb 20–40% retail price premiums. Retail scanners show organic produce sales advancing 8.4% annually as conventional produce slides 1.2%, a divergence amplified by ingredient transparency rules under the Food Safety Modernization Act. Food-service chains such as Chipotle and grocery leaders like Whole Foods sign long-term supply agreements that require exclusive use of OMRI-certified inputs. This downstream commitment pulls through demand for field-level nutrient products that adhere to National Organic Program rules. As household preference consolidates, growers who meet organic standards gain durable price insulation, a dynamic that encourages continued investment in high-quality fertilizers despite their higher upfront cost.

Federal Cost-Share Incentives for Transitioning Farms

The Natural Resources Conservation Service earmarked USD 47 million to the Environmental Quality Incentives Program (EQIP) in 2024 exclusively for organic and transitional farms, a 23% jump from the prior year [2]Source: USDA Natural Resources Conservation Service, “Environmental Quality Incentives Program,” nrcs.usda.gov. These grants can cover up to three-quarters of fertilizer expenses during transition, helping offset yield variability and input price spikes. Complementary CSP payments run USD 15–25 per acre for farms that follow comprehensive organic nutrient plans. States such as Wisconsin match federal funds to accelerate adoption in priority watersheds. By absorbing early-stage financial strain, cost-share packages lower entry barriers for row-crop growers who previously viewed organic certification as economically risky, thereby broadening the customer base for suppliers within the United States organic fertilizer market.

Expansion of Organic Livestock Operations

Certified organic livestock farms grew 7.3% to 15,800 operations in 2024, fueled by demand for antibiotic-free meat and dairy. Organic dairies in Wisconsin, California, and Vermont account for 1.1 billion pounds of milk and typically manage 200–500 acres of organic feed crops per 100 cows, driving steady fertilizer use. Poultry shows an even faster 12.4% annual rise, pulling corn and soybean output under organic protocols. National Organic Program standards require detailed records of all nutrient inputs, favoring large, well-documented fertilizer brands over ad-hoc supplies. Taken together, livestock expansion multiplies demand not only for feed crops but for compliant nutrient inputs that keep those feed crops certified, reinforcing market stability.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Nutrient Density Versus Synthetic Alternatives | -1.80% | Nationwide, acute in vegetable belts | Long term (≥ 4 years) |

| Volatility in Feedstock Supply Prices | -1.40% | Areas reliant on crop by-products | Short term (≤ 2 years) |

| Slow Release Profile Unsuitable for Certain Cash Crops | -0.90% | California, Florida, and Arizona | Medium term (2-4 years) |

| Stringent State-Level Pathogen Regulations Increasing Compliance Costs | -1.10% | California, and Washington | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Nutrient Density Versus Synthetic Alternatives

Typical organic fertilizers deliver only 2–6% nitrogen compared with synthetic urea’s 46%, so freight charges run 8–12 times higher per unit of plant-available nitrogen. Row-crop systems that need 150–200 pounds of nitrogen per acre must haul 2.5–5 metric tons of organic material versus less than half a metric ton of synthetic. Diesel averaged USD 3.85 per gallon in 2024, inflating long-haul costs [3]Source: Energy Information Administration, “Petroleum and Other Liquids,” eia.gov. Pelletization raises nutrient density yet adds USD 50–75 per metric ton in processing expenses, offsetting freight gains. Seasonal trucking shortages further elevate spot rates by 25–40% during spring application windows. These economic frictions deter adoption by commodity farmers operating on tight margins, tempering volume growth even as price premiums for organic commodities rise.

Volatility in Feedstock Supply Prices

Seed meals, a primary organic nitrogen source, swung 30–40% quarter to quarter in 2024, with soybean meal moving between USD 285 and USD 425 per metric ton. Drought-driven cattle inventory declines of 3.2% tightened manure supplies, sending poultry litter prices up 22%. Import delays for kelp meal and fish emulsions stretched lead times to eight weeks amid port congestion, forcing manufacturers to build costly inventories when producers cannot pass these spikes through annual farm contracts, profit margins contract, and capital requirements swell, slowing investment in new capacity within the United States organic fertilizer market.

Segment Analysis

By Form: Manure Drives Growth Through Bio-Digester Integration

Manure-based products secured 46.8% of the United States organic fertilizer market share in 2024 and are projected to maintain leadership with a 12.5% CAGR through 2030. The segment benefits from digestate with nutrient content triple that of raw manure, alongside renewable-energy credits that improve dairy farm economics. Cost-share incentives under the Environmental Quality Incentives Program (EQIP) grant higher reimbursement rates for processed organic amendments, further propelling adoption. As variable-rate applicators spread, growers favor pelletized or composted manure that delivers uniform flow, bolstering demand for upgraded formulations.

Processed manure also improves pathogen safety, enabling penetration into specialty crops that once avoided raw manure. Meal-based fertilizers sit in second place, valued for consistent nutrient profiles and shelf stability, yet face supply swings tied to global oilseed markets. Oilcakes continue to serve orchards and perennial systems that desire slow-release traits, while niche categories such as fish emulsion cater to greenhouse and hydroponic growers willing to pay top-tier prices.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop Type: Row Crops Anchor Volume Expansion

Row crops captured 66.1% of the United States organic fertilizer market size in 2024 and head toward a 12.5% CAGR to 2030 as corn and soybean producers chase export premiums of USD 2–4 per bushel. Large equipment fleets allow uniform spreading of high volumes without extra labor, lowering incremental cost per acre. Crop-insurance parity with conventional systems reduces financial risk during transition, encouraging broader participation.

Horticultural crops, though smaller in acreage, clock the fastest relative gains because premium pricing in nuts, grapes, and berries rewards nutrient management upgrades. California almonds add USD 0.50–1.20 per pound when certified organic, while wine grapes gain USD 500–800 per metric ton, numbers that readily absorb higher fertilizer bills. Quick-cycle vegetables remain partly constrained by nutrient timing limits, but targeted research in soluble organic extracts may chip away at this restraint over time.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

California commands both the largest acreage and the strictest regulations, pushing producers to allocate USD 8–15 more per metric ton for pathogen compliance, yet also offering carbon payments of USD 15–30 per metric ton of compost that help offset those outlays. The state’s 1.2 million organic acres span row crops in the Central Valley and high-value salads on the coast, creating broad fertilizer demand for multiple formulations.

Midwest states deliver the steepest acreage growth, with Iowa, Nebraska, and Wisconsin expanding organic land 15–20% per year. Abundant livestock manure supports a burgeoning compost supply, and rising digester adoption adds high-quality digestate that travels shorter distances to nearby corn and soybean fields, cutting freight costs.

The Northeast and Southeast collectively account for a smaller footprint but show rising interest as dairy, vegetable, and pasture operations pivot to capture local, premium consumers. State rules are less uniform here, allowing producers in certain jurisdictions to avoid California-style testing costs. However, limited processing infrastructure can still raise delivered prices, making the region a promising but infrastructure-dependent frontier for the United States' organic fertilizer market.

Competitive Landscape

The top five suppliers together owned a significant share in 2024, illustrating a fragmented playing field. Cedar Grove Composting Inc. holds long-term municipal waste contracts that supply low-cost, reliable feedstock and strengthen negotiating power with retailers. Darling Ingredients’ majority stake in Nature Safe, secured for USD 85 million, signals a move toward vertical integration that captures rendering by-products for fertilizer production, cutting raw-material risk.

Technology serves as a separator. Atlas Organics’ USD 25 million digester rollout in Wisconsin and California widens access to pathogen-free digestate, while Perfect Blend’s new Nebraska pelletization plant slices transportation costs by 35%. Patent filings on nutrient concentration technologies surged 23% in 2024, spotlighting a race to deliver higher analysis products that narrow the cost gap with synthetics.

OMRI certification under the National Organic Program creates regulatory moats for established players with documented compliance histories, while stringent state-level pathogen regulations in California and Washington increase barriers to entry that benefit larger producers with quality assurance capabilities. Patent filings in organic fertilizer processing technologies increased 23% in 2024, indicating intensifying innovation competition around nutrient concentration and pathogen reduction methods the United States Patent and Trademark Office (USPTO) Patent Database.

United States Organic Fertilizer Industry Leaders

-

Cedar Grove Composting Inc.

-

EB Stone & Sons Inc.

-

The Espoma Company

-

California Organic Fertilizers Inc.

-

Morgan Composting Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2024: Cedar Grove Composting activated an automated screening and packaging line that lifts annual Washington output 40% to 180,000 metric tons, targeting landscapers and retail garden centers.

- September 2024: Perfect Blend LLC completed construction of a new palletization facility in Nebraska, reducing transportation costs by 35% while improving product handling characteristics for large-scale row crop applications. The facility processes 15,000 metric tons annually of organic materials into concentrated pellets with consistent nutrient profiles.

- August 2024: The Espoma Company introduced “Climate Smart,” a carbon-negative compost blend eligible for Healthy Soils incentives, priced at USD 15–30 per metric ton applied.

United States Organic Fertilizer Market Report Scope

Manure, Meal Based Fertilizers, Oilcakes are covered as segments by Form. Cash Crops, Horticultural Crops, Row Crops are covered as segments by Crop Type.

Form

| Manure |

| Meal Based Fertilizers |

| Oilcakes |

| Other Organic Fertilizer |

Crop Type

| Cash Crops |

| Horticultural Crops |

| Row Crops |

| Form | Manure |

| Meal Based Fertilizers | |

| Oilcakes | |

| Other Organic Fertilizer | |

| Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops |

Need A Different Region or Segment?

Customize Now

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of organic fertilizers applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The crop nutrition function of agricultural biological consists of various products that provide essential plant nutrients and enhance soil quality.

- TYPE - Organic fertilizers are applied to provide essential crop nutrients and enhance the soil quality.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.

Get More Details On Research Methodology

Download PDF