United States MLCC Market Size

| Study Period | 2017 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Market Size (2024) | USD 2.55 Billion |

| Market Size (2029) | USD 8 Billion |

| CAGR (2024 - 2029) | 25.69 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

United States MLCC Market Analysis

The United States MLCC Market size is estimated at 2.55 billion USD in 2024, and is expected to reach 8 billion USD by 2029, growing at a CAGR of 25.69% during the forecast period (2024-2029).

The United States MLCC market is experiencing significant transformation driven by the ongoing trend of miniaturization and increasing component density requirements across various industries. Manufacturers are focusing on developing compact designs without compromising performance, particularly in portable and connected devices. This shift is especially evident in the telecommunications sector, where 5G component technology adoption is rapidly accelerating. Industry projections indicate that 5G component mobile connections in the United States are expected to surge from 15% in 2021 to approximately 68% by 2025, highlighting the growing demand for advanced MLCCs in network infrastructure and mobile devices.

The healthcare technology landscape is witnessing substantial integration of MLCCs in medical devices, ranging from portable diagnostic equipment to implantable devices. With approximately 695,000 people succumbing to heart disease in 2021 in the United States, the demand for sophisticated medical devices incorporating ceramic capacitors continues to rise. The medical equipment manufacturing sector has attracted significant foreign direct investment, reaching USD 107.2 billion, demonstrating the industry's robust growth potential and technological advancement requirements.

The power and utilities sector is undergoing a significant digital transformation, with smart meter deployment at the forefront of this evolution. Currently, over 100 million advanced smart electric meters have been installed throughout the country, with residential installations representing 88% of the total. This widespread adoption of smart meters, coupled with the government's Smart Grid Investment Grant (SGIG) Program, is driving the demand for electronic capacitors in smart grid technology applications.

The emphasis on energy efficiency and sustainable technologies is reshaping the MLCC market landscape. LED lighting applications, which currently save approximately 185 terawatt-hours (TWh) of site energy per year compared to conventional lighting technologies, represent a growing application area for MLCCs. The U.S. Department of Energy's initiatives and stringent government regulations are accelerating the adoption of energy-efficient technologies, creating new opportunities for MLCC manufacturers to develop specialized components for these applications.

United States MLCC Market Trends

The development of third-party logistic providers may propel the demand for light commercial vehicles

- The market for light commercial vehicles (LCVs) is primarily driven by the e-commerce and logistics industries. As more people have access to the Internet and smartphones, online retail sales and e-commerce have been increasing. Purchases of LCVs are anticipated to increase, thereby facilitating quick delivery of items to customers. The country produced 8.03 million units in 2019.

- The COVID-19 pandemic and the Russia-Ukraine War resulted in unprecedented levels and types of mobility and transportation restrictions, resulting in a 17.17% Y-o-Y drop in production. Lockdowns and other restrictions caused previously unheard-of problems in the commercial vehicle industry's supply chain. Tightening emissions regulations, vehicle safety improvements, driver-assist systems in cars, and the explosive growth of logistics in the retail and e-commerce sectors have all fueled demand for new and innovative commercial vehicles.

- Third-party logistic providers, such as FedEx, UPS, and DHL, use a variety of LCVs to transport products to the nearest product delivery station. These businesses have a larger fleet of LCVs because smaller LCVs use less fuel than heavy commercial vehicles when commuting within a city. To combat climate change and city pollution, big logistics operators have started replacing their fleets of combustion engines with electric or low-emission vehicles. For instance, in December 2021, FedEx announced a global target to make 50% of all newly purchased vehicles electric by 2025, rising to 100% for the new fleet by 2030. By 2040, FedEx wants to achieve global carbon neutrality through the electrification of pickups and delivery vehicles as a significant investment area.

Customers in the United States are demanding higher safety, which is propelling the demand for passenger vehicles

- The United States has one of the largest automotive markets in the world and ranks 8th in the production of passenger cars, producing 2.5 million units in 2019.

- Post the COVID-19 outbreak, there has been a major decline in production, registering a Y-o-Y drop of 24%, along with a decline in the usage of personal vehicles for commuting. Maintenance activities of passenger vehicles have significantly declined. With the ease of lockdown measures, there has been a surge in the usage of personal vehicles, which may drive the recovery of passenger vehicle consumption.

- The production of passenger vehicles in the United States reached 1.72 million units as several OEMs became interested in increasing their production capacity to meet the growing demand for electric vehicles. The government policy of banning ICE engines helped boost the sales of electric vehicles. The increase in the price of gasoline and diesel due to various global reasons has also made it easy for EV companies to boost their sales. Electric car sales in the United States, the third largest market, increased by 55% in 2022, reaching a sales share of 8%.

- Sales of ICE models have been steadily decreasing. The number of available ICE options was 3% to 4% lower in the United States in 2022 than in 2016. Several factors help increase sales of electric cars in the United States. More available models beyond those offered by OEMs help close the supply gap.

- The United States holds the second largest FCEV stock, with over 15,000 FCEVs. Most of these are fuel-cell cars. In 2022, the stock of FCEVs in the United States increased by more than 20%. These key elements fuel production demand for passenger vehicles and are expected to increase in the future.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Copper prices decline as the US dollar’s strength declines

- The tightening of monetary policy to hamper the market

- Prices increase due to an increase in travel

- Zinc prices may increase owing to fierce competition with Europe

- Increasing residential construction activities and energy-efficient ACs, which consume less energy, are driving the demand

- Price rises, rising interest rate hikes, and semiconductor shortages decreased the demand

- Technological advancements and the introduction of 5G services drive the demand

- The rise in cloud adoption drives the demand

- The increasing focus of consumers on eco-friendly, energy-efficient refrigerators propels the demand

- The rapid adoption of 5G networks and the emergence of budget-centric smartphones drive the demand

- Supply chain disruptions and raw material and electronic component shortages decreased the growth of storage unit sales

- Innovative designs with advanced features are driving the demand

- The affordable prices of larger screens and increasing viewing of online streaming platforms are driving the demand

- Electric heavy commercial vehicles are expected to impact the demand positively

- The development of third-party logistic providers may propel the demand for light commercial vehicles

- Supportive infrastructure and electric vehicle regulations are driving the demand

- Supportive government policies to deploy public charging infrastructure are expected to promote battery electric vehicles

- Advancements in battery technology to propel PHEVs in the United States

- The emergence of smart factories is expected to drive the growth of industrial robots

- The growing demand for service robots in the healthcare sector fuels the market's growth

Segment Analysis: Dielectric Type

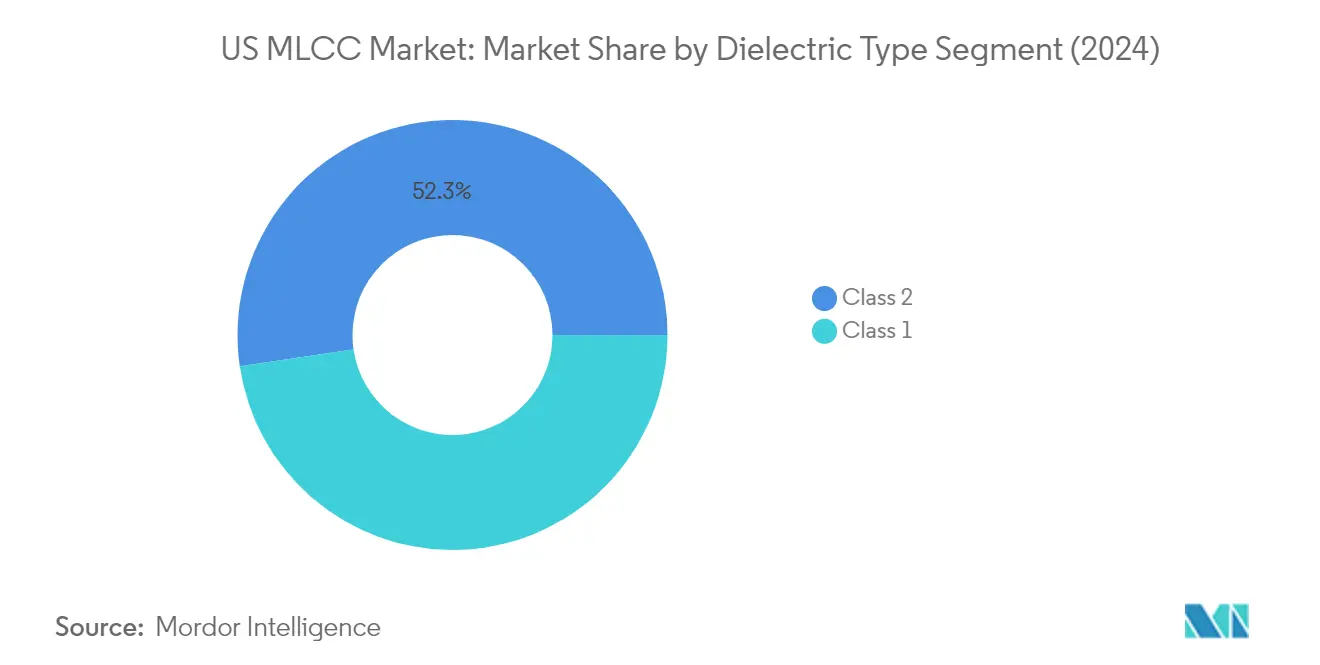

Class 2 Segment in US MLCC Market

Class 2 dielectric type dominates the US MLCC market, commanding approximately 52% of the market share in 2024. This segment's prominence is primarily driven by its extensive application in industrial hardware and manufacturing automation. The growing trend toward full-scale automation in the manufacturing sector is creating substantial demand for Class 2 MLCCs, which include popular variants like X7R, X5R, and Y5V. These components are particularly valued for their superior performance characteristics and stability across diverse operating conditions. The US government's recent focus on boosting local manufacturing industries through initiatives like "Make in America" has significantly contributed to the segment's growth, particularly through increased adoption of industrial robots. Class 2 MLCCs are experiencing robust growth with a projected CAGR of nearly 32% from 2024 to 2029, driven by their essential role in supporting the evolving needs of industrial automation and manufacturing advancement.

Class 1 Segment in US MLCC Market

The Class 1 dielectric type segment, which includes C0G, X8G, and U2J variants, plays a crucial role in the telecommunications sector due to its exceptional performance capabilities at high frequencies. This segment is particularly vital in the gaming industry, where the United States maintains its position as one of the largest markets globally. The extensive library of games available to US citizens continues to drive demand for gaming consoles, with cloud gaming and VR gaming technologies emerging as significant growth catalysts. Class 1 MLCCs are especially valued for their stability and reliability in high-frequency applications, making them indispensable in modern gaming hardware and telecommunications infrastructure. The segment's growth is further supported by the increasing adoption of online gaming platforms and the ongoing evolution of gaming technology, which demands high-performance electronic components.

Segment Analysis: Case Size

0201 Segment in US MLCC Market

The 0201 case size segment has established itself as the dominant force in the US MLCC market, commanding approximately 22% market share in 2024. This segment's prominence is primarily driven by the increasing demand for compact electronic devices, particularly in smartphones, wearables, and IoT devices. The ongoing trend of miniaturization, coupled with the need for higher component density, continues to drive the demand for these components. The increasing popularity of portable and connected devices further contributes to the demand for 0201 chip capacitors, enabling manufacturers to achieve compact designs without compromising performance. The United States' position as home to several prominent laptop manufacturers and multinational companies with significant market presence has further strengthened this segment's leadership position.

0402 Segment in US MLCC Market

The 0402 case size segment is projected to experience the fastest growth in the US MLCC market during 2024-2029, with an expected CAGR of approximately 26%. This remarkable growth trajectory is primarily attributed to its widespread adoption in automotive applications, including engine control units, infotainment systems, and advanced driver-assistance systems (ADAS). These SMD capacitors provide reliable performance in harsh automotive environments, making them indispensable for modern vehicle electronics. The segment's growth is further fueled by the increasing demand for autonomous vehicles in North America, driven by enhanced focus on automotive safety, rising demand for comfort features, and growing desire to reduce human error in accidents. The automotive industry's reliance on 0402 MLCCs for various critical applications positions this segment for substantial growth in the coming years.

Remaining Segments in Case Size

The other case sizes in the US MLCC market, including 0603, 1005, 1210, and miscellaneous sizes, each serve specific applications and contribute significantly to the market's diversity. The 0603 segment is particularly notable in medical device applications and power supply circuits, while the 1005 case size finds extensive use in automotive ADAS components and high-frequency applications. The 1210 segment is crucial for consumer electronics and high-power applications, offering robust performance in demanding environments. The remaining miscellaneous sizes cater to specialized applications across various industries, ensuring that manufacturers have access to MLCCs that meet their specific requirements across different use cases and operating conditions.

Segment Analysis: Voltage

Less than 500V Segment in US MLCC Market

The Less than 500V segment has established itself as the dominant force in the United States MLCC market, commanding approximately 51% market share in 2024. This segment's prominence is primarily driven by its extensive application across various end-user industries, including consumer electronics, medical devices, telecommunications, and automotive sectors. The segment's growth is particularly notable in the medical devices industry, where the rising geriatric population and increasing prevalence of chronic diseases are driving demand for advanced medical equipment. Additionally, the automotive sector's transition towards electric vehicles has significantly boosted the demand for less than 500V MLCCs, as these components are essential in various automotive applications including advanced driver assistance systems (ADAS), infotainment systems, and engine control units. The segment is also experiencing robust growth with a projected growth rate of around 26% from 2024 to 2029, driven by the increasing adoption of IoT devices, smartphones, and other consumer electronics that predominantly utilize lower voltage MLCCs.

Remaining Segments in Voltage Segmentation

The 500V to 1000V segment plays a crucial role in high-power applications, particularly in industrial equipment and power supply units. This segment is particularly vital in applications such as switching power supplies for audiovisual and business equipment, as well as lighting ballasts. The More than 1000V segment, while smaller in market share, serves specialized applications in high-voltage systems, particularly in the power and utilities sector. This segment is essential for applications requiring high voltage handling capabilities, such as industrial machinery, power distribution systems, and specialized electronic equipment. Both segments continue to maintain their significance in the market due to their specific applications in critical industries, contributing to the overall growth and development of the MLCC market in the United States.

Segment Analysis: Capacitance

Less than 100µF Segment in US MLCC Market

The Less than 100μF segment has established itself as the dominant force in the US MLCC market, commanding approximately 55% market share in 2024. These MLCCs, characterized by tolerances ranging from ±5% to ±20%, are exceptionally well-suited for deployment in various consumer electronic applications. Premium smartphone models are witnessing an increased demand for Less than 100μF MLCCs as they grapple with the complexities of evolving 5G technology. Key players in the industry, including Samsung and Murata, are taking proactive measures to enhance their offerings by upgrading their existing 0402 MLCCs, which feature a capacitance range from 0.01 F to 1uF and a voltage rating of 6.3 V. In response to the evolving landscape of 5G devices, these companies are actively developing new MLCCs in the 0201 case size, featuring a capacitance of 0.1uF. This strategic move reflects the demand driven by the increasing versatility and complexity of 5G smartphones that must effectively manage a multitude of frequency bands within a single device. The segment is projected to maintain its robust growth trajectory at around 26% through 2029, driven by the continuous evolution of smartphone technology and the increasing integration of 5G capabilities as standard features in flagship smartphones.

Remaining Segments in Capacitance

The 100μF to 1000μF and More than 1000μF segments play crucial roles in different applications within the MLCC market. The 100μF to 1000μF segment is particularly vital in medical devices and automotive applications, where these capacitors contribute to the efficiency and functionality of electronic devices by providing reliable performance and optimal energy storage. The More than 1000μF segment serves specialized applications in high-power electronics and industrial equipment, particularly in semiconductor applications for LED headlamps, ensuring precise energy storage and delivery, stability, and high voltage durability. These segments complement each other by addressing different market needs, from consumer electronics to industrial applications, contributing to the overall growth and diversification of the MLCC market.

Segment Analysis: MLCC Mounting Type

Surface Mount Segment in US MLCC Market

Surface mount capacitors have emerged as the dominant mounting type in the United States MLCC market, commanding approximately 40% market share in 2024. This segment's prominence can be attributed to its widespread adoption in mass-production circuit designs, particularly in consumer electronics and automotive applications. Surface mount capacitors are increasingly preferred in electronic designs due to their smaller footprint and superior performance at higher frequencies compared to traditional capacitors. The segment's growth is being driven by the expanding American TV market, which is experiencing positive momentum due to increased utilization of high-quality internet for socialization, educational purposes, and telehealth applications. Additionally, companies are actively producing surface mount capacitors that meet the requirements of modems, AEC-Q200 standards, and AC-DC power supplies, particularly in applications where lightning strikes or other voltage transients pose threats to electronic equipment. The widespread adoption of Surface Mount Technology (SMT) has led to economies of scale, making SMD capacitors more cost-effective in numerous applications, further solidifying their market position.

Remaining Segments in MLCC Mounting Type

The Radial Lead and Metal Cap segments represent significant portions of the MLCC mounting type market, each offering unique advantages for specific applications. Radial Lead MLCCs are particularly valued in automotive applications requiring high voltages and temperatures, finding extensive use in engine control units, lighting modules, infotainment systems, and sensors. These components are often preferred over surface mount capacitors in applications where reliability under extreme conditions is paramount. Meanwhile, Metal Cap MLCCs utilize temperature-compensating ceramic with minimal capacitance variation, making them ideal for snubber circuits and industrial applications. The increasing digitization initiatives across various industries continue to drive demand for both these mounting types, particularly in applications where their specific characteristics provide advantages over surface mount alternatives. Both segments continue to maintain their relevance in the market through ongoing technological advancements and expanding application areas.

Segment Analysis: End User

Consumer Electronics Segment in US MLCC Market

The Consumer Electronics segment maintains its dominant position in the US MLCC market, commanding approximately 32% market share in 2024. This segment's strength is primarily driven by the increasing integration of MLCCs in smartphones, tablets, laptops, and other consumer devices, with high-end smartphones requiring between 800-1000 MLCCs per unit. The segment's growth is further bolstered by the rapid adoption of 5G technology, which has become a standard feature in flagship smartphones, leading to increased demand for MLCCs in mobile devices. Additionally, the expansion of streaming platforms and the growing consumer preference for immersive audio-visual experiences have driven the demand for smart TVs with larger screens, contributing significantly to the segment's market leadership.

Power and Utilities Segment in US MLCC Market

The Power and Utilities segment is projected to exhibit the highest growth rate of approximately 28% during the forecast period 2024-2029. This remarkable growth is primarily driven by the widespread implementation of smart meters across the United States, with over 100 million advanced smart electric meters already installed nationwide. The segment's expansion is further supported by various government initiatives, including the Smart Grid Investment Grant (SGIG) Program, which aims to accelerate smart meter deployment. The increasing adoption of LED lighting systems, coupled with declining LED product prices and stringent energy efficiency regulations, is also contributing to the segment's growth. Furthermore, the emergence of smart cities and green building concepts is creating new opportunities for innovative smart meter applications, driving the demand for MLCCs in power and utility applications.

Remaining Segments in End User Segmentation

The other segments in the US MLCC market include Automotive, Telecommunication, Industrial, Medical Devices, and Aerospace and Defense, each serving distinct market needs. The Automotive segment is experiencing significant growth due to the increasing adoption of electric vehicles and advanced driver assistance systems. The Telecommunication segment is driven by the ongoing establishment of 5G infrastructure, while the Industrial segment benefits from the increasing automation in manufacturing processes. The Medical Devices segment is expanding due to the rising demand for advanced healthcare equipment and implantable devices. The Aerospace and Defense segment continues to grow with increased investments in space exploration and defense technologies, showcasing the diverse applications and opportunities within the MLCC market.

United States MLCC Industry Overview

Top Companies in United States MLCC Market

The US MLCC market is characterized by intense innovation and strategic initiatives from leading players like Murata Manufacturing, YAGEO Group, Taiyo Yuden, Samsung Electro-Mechanics, and Kyocera AVX. Companies are heavily focusing on product innovations, particularly in developing miniaturized MLCCs with enhanced capacitance and voltage ratings to meet the evolving demands of the automotive and consumer electronics sectors. Operational agility is demonstrated through rapid adaptation to market changes and supply chain optimization, with manufacturers expanding their production capabilities to address growing demand. Strategic partnerships, especially with automotive and telecommunications companies, have become increasingly common as players seek to strengthen their market positions. Companies are also investing significantly in research and development to develop advanced MLCC technologies, particularly for emerging applications in 5G devices and electric vehicles.

Market Dominated by Global Technology Conglomerates

The US MLCC market structure is characterized by the strong presence of global technology conglomerates, primarily from Japan, South Korea, and Taiwan, who have established robust manufacturing and distribution networks across the country. These major players leverage their extensive research capabilities, technological expertise, and economies of scale to maintain their market positions. The market shows high consolidation, with the top five companies collectively controlling a significant portion of the market share, creating substantial barriers to entry for new players.

The competitive landscape has been shaped by strategic mergers and acquisitions, as demonstrated by key moves like YAGEO's acquisition of Kemet Corporation, which has strengthened market positions and expanded product portfolios. Companies are increasingly focusing on vertical integration strategies to secure supply chains and maintain competitive advantages. The market also sees collaboration between major players and automotive manufacturers, particularly in developing specialized ceramic capacitors for electric vehicles and advanced driver assistance systems.

Innovation and Specialization Drive Future Success

For incumbent players to maintain and expand their market share, a focus on technological innovation and product customization will be crucial. Companies need to invest in developing next-generation MLCCs with higher capacitance and smaller form factors while maintaining reliability and performance. Establishing strong relationships with key end-users in growing sectors like automotive and telecommunications will be essential. Additionally, vertical integration and supply chain optimization will become increasingly important to maintain cost competitiveness and ensure a stable supply.

Contenders looking to gain ground in the market should focus on identifying and serving niche market segments, particularly in emerging applications like renewable energy and industrial automation. Success will depend on developing specialized products that meet specific industry requirements while maintaining competitive pricing. The risk of substitution remains relatively low due to the essential nature of electronic capacitors in electronic devices, but companies must stay ahead of technological advances. Regulatory compliance, particularly in automotive and medical applications, will continue to play a crucial role in market success, requiring companies to maintain robust quality management systems and certifications.

United States MLCC Market Leaders

-

Kyocera AVX Components Corporation (Kyocera Corporation)

-

Murata Manufacturing Co., Ltd

-

Samsung Electro-Mechanics

-

Taiyo Yuden Co., Ltd

-

Yageo Corporation

*Disclaimer: Major Players sorted in no particular order

United States MLCC Market News

- July 2023: KEMET, part of the Yageo Corporation developed the X7R automotive grade MLCC X7R. This MLCC is designed to meet the high voltage requirements of automotive subsystems, ranging from 100pF-0.1uF and with a DC voltage range of 500V-1kV. The range of cases available is EIA 0603-1210, and is suitable for both automotive under hoods and in-cabin applications. These MLCCs demonstrate the essential and reliable nature of capacitors, which are essential for the mission and safety of automotive subsystems.

- June 2023: The growing demand for industrial equipments has driven the company to introduce NTS/NTF NTS/NTF Series of SMD type MLCC. These capacitors are rated with 25 to 500 Vdc with a capacitance ranging from 0.010 to 47µF. These MLCCs are used in on-board power supplies,voltage regulators for computers,smoothing circuit of DC-DC converters,etc.

- May 2023: Murata has introduced the EVA series of MLCC, which are beneficial to EV manufacturers due to their versatility. These MLCC's can be used in a variety of applications, including OBC (On-Board Charger), inverter and DC/DC Converter, BMS (Battery Management System), and WPT (Wireless Power Transfer) implementations. As a result, they are ideal to the increased isolation that the 800V powertrain migration will require, while also meeting the miniaturization requirements of modern automotive systems.

United States MLCC Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4. KEY INDUSTRY TRENDS

4.1 Price Trend

4.1.1 Copper Price Trend

4.1.2 Nickel Price Trend

4.1.3 Oil Price Trend

4.1.4 Zinc Price Trend

4.2 Consumer Electronics Sales

4.2.1 Air Conditioner Sales

4.2.2 Desktop PC's Sales

4.2.3 Gaming Console Sales

4.2.4 Laptops Sales

4.2.5 Refrigerator Sales

4.2.6 Smartphones Sales

4.2.7 Storage Unit Sales

4.2.8 Tablets Sales

4.2.9 Television Sales

4.3 Automotive Production

4.3.1 Heavy Trucks Production

4.3.2 Light Commercial Vehicles Production

4.3.3 Passenger Vehicles Production

4.3.4 Total Motor Production

4.4 Ev Production

4.4.1 BEV (Battery Electric Vehicle) Production

4.4.2 PHEV (Plug-in Hybrid Electric Vehicle) Production

4.5 Industrial Automation Sales

4.5.1 Industrial Robots Sales

4.5.2 Service Robots Sales

4.6 Regulatory Framework

4.7 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

5.1 Dielectric Type

5.1.1 Class 1

5.1.2 Class 2

5.2 Case Size

5.2.1 0 201

5.2.2 0 402

5.2.3 0 603

5.2.4 1 005

5.2.5 1 210

5.2.6 Others

5.3 Voltage

5.3.1 500V to 1000V

5.3.2 Less than 500V

5.3.3 More than 1000V

5.4 Capacitance

5.4.1 100µF to 1000µF

5.4.2 Less than 100µF

5.4.3 More than 1000µF

5.5 Mlcc Mounting Type

5.5.1 Metal Cap

5.5.2 Radial Lead

5.5.3 Surface Mount

5.6 End User

5.6.1 Aerospace and Defence

5.6.2 Automotive

5.6.3 Consumer Electronics

5.6.4 Industrial

5.6.5 Medical Devices

5.6.6 Power and Utilities

5.6.7 Telecommunication

5.6.8 Others

6. COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles

6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

6.4.2 Maruwa Co ltd

6.4.3 Murata Manufacturing Co., Ltd

6.4.4 Nippon Chemi-Con Corporation

6.4.5 Samsung Electro-Mechanics

6.4.6 Samwha Capacitor Group

6.4.7 Taiyo Yuden Co., Ltd

6.4.8 TDK Corporation

6.4.9 Vishay Intertechnology Inc.

6.4.10 Walsin Technology Corporation

6.4.11 Würth Elektronik GmbH & Co. KG

6.4.12 Yageo Corporation

7. KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8. APPENDIX

8.1 Global Overview

8.1.1 Overview

8.1.2 Porter’s Five Forces Framework

8.1.3 Global Value Chain Analysis

8.1.4 Market Dynamics (DROs)

8.2 Sources & References

8.3 List of Tables & Figures

8.4 Primary Insights

8.5 Data Pack

8.6 Glossary of Terms

United States MLCC Industry Segmentation

Class 1, Class 2 are covered as segments by Dielectric Type. 0 201, 0 402, 0 603, 1 005, 1 210, Others are covered as segments by Case Size. 500V to 1000V, Less than 500V, More than 1000V are covered as segments by Voltage. 100µF to 1000µF, Less than 100µF, More than 1000µF are covered as segments by Capacitance. Metal Cap, Radial Lead, Surface Mount are covered as segments by Mlcc Mounting Type. Aerospace and Defence, Automotive, Consumer Electronics, Industrial, Medical Devices, Power and Utilities, Telecommunication, Others are covered as segments by End User.| Dielectric Type | |

| Class 1 | |

| Class 2 |

| Case Size | |

| 0 201 | |

| 0 402 | |

| 0 603 | |

| 1 005 | |

| 1 210 | |

| Others |

| Voltage | |

| 500V to 1000V | |

| Less than 500V | |

| More than 1000V |

| Capacitance | |

| 100µF to 1000µF | |

| Less than 100µF | |

| More than 1000µF |

| Mlcc Mounting Type | |

| Metal Cap | |

| Radial Lead | |

| Surface Mount |

| End User | |

| Aerospace and Defence | |

| Automotive | |

| Consumer Electronics | |

| Industrial | |

| Medical Devices | |

| Power and Utilities | |

| Telecommunication | |

| Others |

United States MLCC Market Research FAQs

How big is the United States MLCC Market?

The United States MLCC Market size is expected to reach USD 2.55 billion in 2024 and grow at a CAGR of 25.69% to reach USD 8.00 billion by 2029.

What is the current United States MLCC Market size?

In 2024, the United States MLCC Market size is expected to reach USD 2.55 billion.

Who are the key players in United States MLCC Market?

Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd and Yageo Corporation are the major companies operating in the United States MLCC Market.

Which segment has the biggest share in the United States MLCC Market?

In the United States MLCC Market, the 0 402 segment accounts for the largest share by case size.

Which is the fastest growing segment in the United States MLCC Market?

In 2024, the 0 201 segment accounts for the fastest growing by case size in the United States MLCC Market.

What years does this United States MLCC Market cover, and what was the market size in 2023?

In 2023, the United States MLCC Market size was estimated at 2.55 billion. The report covers the United States MLCC Market historical market size for years: 2017, 2018, 2019, 2020, 2021, 2022 and 2023. The report also forecasts the United States MLCC Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

United States MLCC Market Research

Mordor Intelligence provides a comprehensive analysis of the United States MLCC market. We leverage our extensive experience in tracking passive electronic components and semiconductor technologies. Our detailed report, available as an easy-to-download PDF, covers the entire spectrum of multi layer ceramic capacitor technologies. This includes segments like surface mount capacitor, tantalum capacitor, and electronic capacitor.

The analysis encompasses various applications, ranging from smartphone components to 5G components. It provides detailed insights into developments in industrial capacitor and power capacitor technologies. The report offers stakeholders crucial intelligence on emerging trends in ceramic capacitor technologies. It focuses particularly on innovations in miniature capacitor and chip capacitor.

Our analysis examines how automotive electronic component requirements are shaping the industry, especially regarding automotive MLCC applications. The comprehensive coverage includes a detailed evaluation of SMD capacitor technologies and their implementation across various sectors. This is supported by extensive data on passive electronic components market dynamics. This invaluable resource helps industry participants understand current trends and future opportunities in the evolving landscape of electronic component manufacturing and integration.