Market Size of United States HVAC Equipment Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

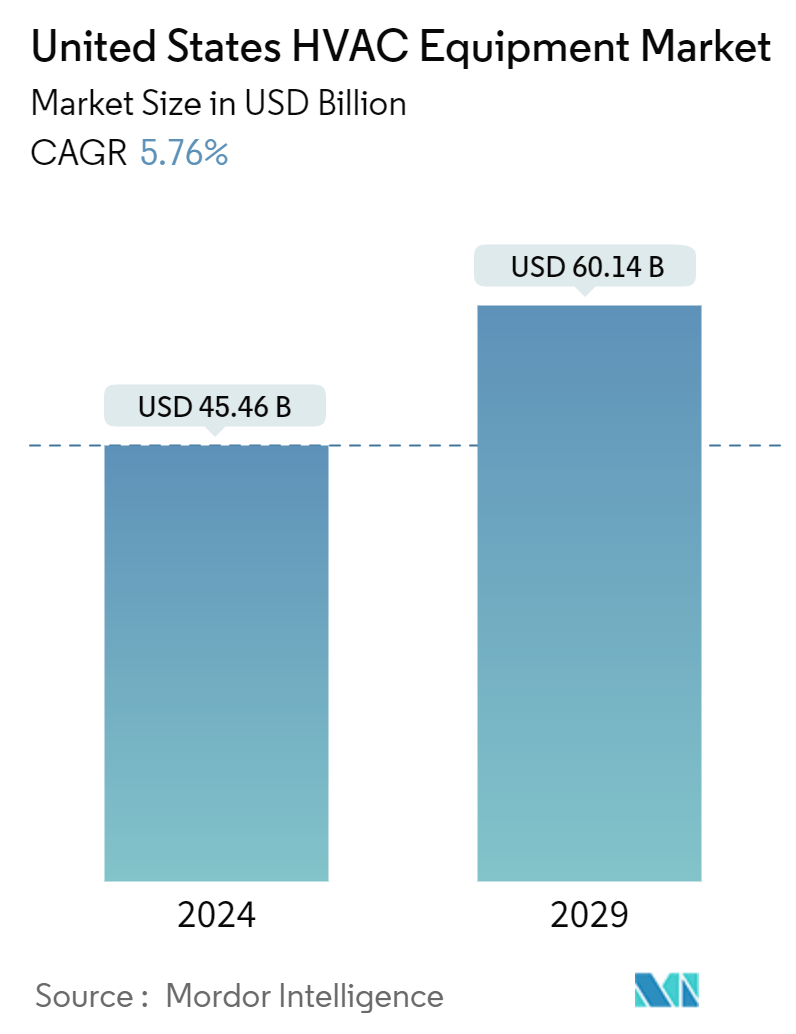

| Market Size (2024) | USD 45.46 Billion |

| Market Size (2029) | USD 60.14 Billion |

| CAGR (2024 - 2029) | 5.76 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

United States HVAC Equipment Market Analysis

The United States HVAC Equipment Market size is estimated at USD 45.46 billion in 2024, and is expected to reach USD 60.14 billion by 2029, growing at a CAGR of 5.76% during the forecast period (2024-2029).

The HVAC equipment market is thriving in the United States, fueled by various factors. Given the vast geographic expanse of the United States, temperatures can swing from extreme cold to intense heat, varying by state, city, and coast. This climatic variability makes HVAC installations essential in residential/commercial spaces. As a result, the pressing need to regulate indoor temperatures, regardless of external weather conditions, bolsters the HVAC industry's growth in the nation.

• In the United States, the government is ramping up its building renovation projects to enhance energy efficiency. These energy-efficient upgrades curtail greenhouse gas emissions and lower energy bills for homeowners and businesses. They bolster indoor air quality, underscoring their significance for public health and fostering a conducive environment for market growth.

• For example, in June 2024, the US General Services Administration (GSA) Administrator unveiled an investment plan: channeling USD 80 million from the Inflation Reduction Act (IRA) into intelligent building technologies. These technologies aim to cut emissions, boost efficiency, trim costs, and elevate comfort levels across approximately 560 federal buildings.

• The growing consumer awareness regarding sustainability and energy efficiency is also driving the country's adoption of smart home technologies, creating a favorable ecosystem for the growth of innovative HVAC systems. For instance, according to the Consumer Technology Association (CTA), the US smart home hardware sales revenue was estimated to reach USD 23.5 billion in 2023, compared to USD 19.70 billion in 2018. Hence, the confluence of such trends is expected to support the studied market's growth during the forecast period.

• Factors such as higher energy consumption, especially of legacy/older HVAC systems, and the high cost of replacement and new installation challenge the studied market's growth. The impact of such trends has intensified in recent years owing to the changing geopolitical dynamics between the United States and China, as trade restrictions continue to influence the supply chain and pricing of components/HVAC systems in the region.

• Starting in 2023, new regulations mandate that all HVAC systems in the country must achieve a seasonal energy efficiency ratio (SEER) between 14 and 15. Arizona legislators argue that these new mandates further strain an already challenging real estate market. They are advocating for a six-month extension to ease compliance, but this request remains unapproved.

• With the introduction of these mandates and the gradual elimination of specific refrigerants in residential air conditioning, the HVAC industry is witnessing a surge in demand for replacement systems that align with the new standards. While these advanced systems promise enhanced energy efficiency and environmental benefits, inflationary pressures and other factors are inflating their costs. Suppliers project a cost increase of up to 20%, translating to steeper prices for homeowners in 2023.

United States HVAC Equipment Industry Segmentation

HVAC equipment ensures thermal comfort and maintains acceptable indoor air quality in indoor and vehicular environments. This technology plays a crucial role in various settings, including residential structures like single-family homes, apartment complexes, hotels, and senior living facilities. In addition, it is vital for medium-to-large industrial and office buildings, such as hospitals, where conditions like temperature and humidity are meticulously regulated using fresh outdoor air to ensure safety and health.

The market is defined by the revenue accrued from the sales of HVAC equipment of different types by major market players in the United States. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period.

The US HVAC equipment market is segmented by type of equipment (air conditioning equipment [unitary air conditioners, room air conditioners, packaged terminal air conditioners, and chillers], heating equipment [warm air furnace [gas and oil], boilers, room & zone heating equipment, heat pumps [air-sourced and geothermal], and ventilation equipment [air handling units, fan coil units, building humidifiers, and dehumidifiers]), end user (residential, commercial, and industrial), region (West, South, Midwest, and Northeast). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type of Equipment | ||||||

| ||||||

| ||||||

|

| By End User | |

| Residential | |

| Commercial | |

| Industrial |

| By Region | |

| West | |

| South | |

| Midwest | |

| Northeast |

United States HVAC Equipment Market Size Summary

The United States HVAC Equipment Market is poised for significant growth, driven by the increasing demand for energy-efficient and eco-friendly heating, ventilation, and air conditioning systems. The market is influenced by several factors, including the rising need for climate control solutions due to changing weather patterns and the growing emphasis on energy efficiency by government regulations. The adoption of natural refrigerants and advanced technologies, such as smart HVAC control systems, is expected to further propel market expansion. The construction industry's growth and the rising disposable income in developing regions are also contributing to the increased demand for HVAC equipment across residential and commercial sectors.

The market landscape is characterized by a moderate level of fragmentation, with numerous vendors offering a range of services and products. Strategic partnerships and acquisitions are common as companies seek to enhance their market presence and expand globally. Notable players like Carrier, Trane, and Daikin are actively investing in innovative solutions and collaborations to meet the evolving needs of the market. The air conditioning segment, in particular, is expected to hold a substantial share, supported by government incentives and the high penetration of air conditioning systems in homes and businesses. Overall, the HVAC equipment market in the United States is set to experience robust growth, driven by technological advancements and increasing consumer demand for efficient climate control solutions.

United States HVAC Equipment Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitute Products

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

1.4 Impact of Macroeconomic Factors and COVID-19 on the HVAC Industry

-

1.5 HVAC Industry in the United States - Current Employment, Number of Enterprises, Major Hotspots in the US

-

-

2. MARKET SEGMENTATION

-

2.1 By Type of Equipment

-

2.1.1 Air Conditioning Equipment

-

2.1.1.1 Unitary Air Conditioners

-

2.1.1.2 Room Air Conditioners

-

2.1.1.3 Packaged Terminal Air Conditioners

-

2.1.1.4 Chillers

-

-

2.1.2 Heating Equipment

-

2.1.2.1 Warm Air Furnace (Gas and Oil)

-

2.1.2.2 Boilers

-

2.1.2.3 Room and Zone Heating Equipment

-

2.1.2.4 Heat Pumps (Air-sourced and Geo-thermal)

-

-

2.1.3 Ventilation Equipment

-

2.1.3.1 Air Handling Units

-

2.1.3.2 Fan Coil Units

-

2.1.3.3 Building Humidifiers and Dehumidifiers

-

-

-

2.2 By End User

-

2.2.1 Residential

-

2.2.2 Commercial

-

2.2.3 Industrial

-

-

2.3 By Region

-

2.3.1 West

-

2.3.2 South

-

2.3.3 Midwest

-

2.3.4 Northeast

-

-

United States HVAC Equipment Market Size FAQs

How big is the United States HVAC Equipment Market?

The United States HVAC Equipment Market size is expected to reach USD 45.46 billion in 2024 and grow at a CAGR of 5.76% to reach USD 60.14 billion by 2029.

What is the current United States HVAC Equipment Market size?

In 2024, the United States HVAC Equipment Market size is expected to reach USD 45.46 billion.