United States Home Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

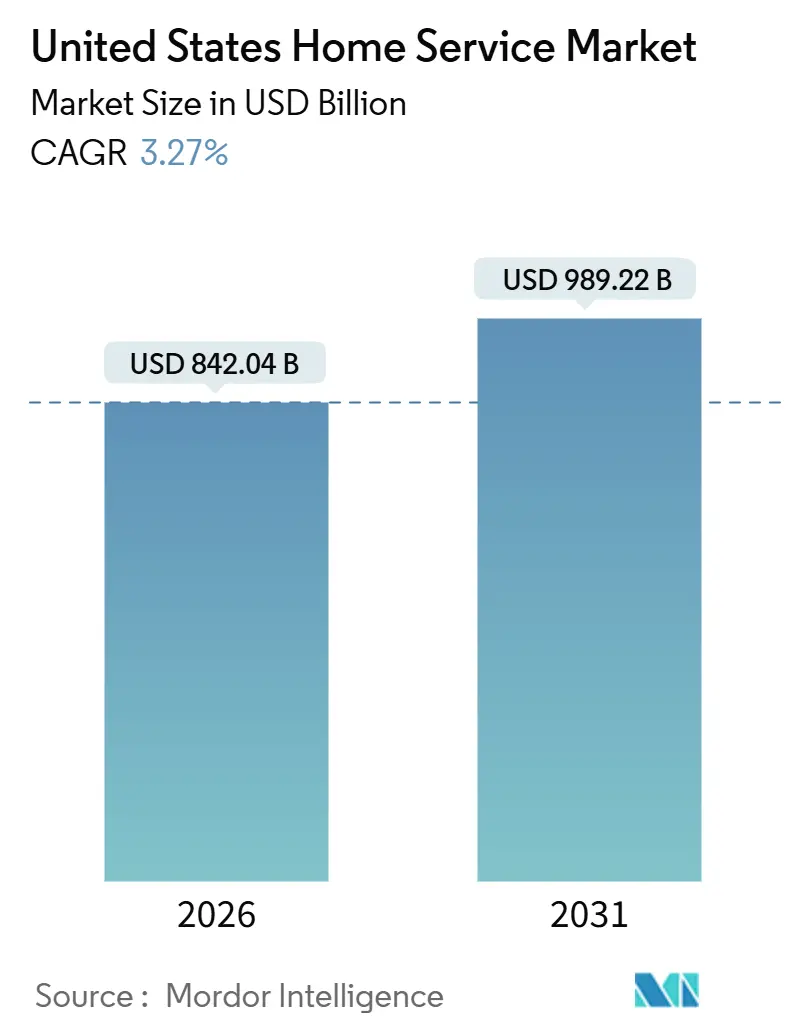

| Market Size (2026) | USD 842.04 Billion |

| Market Size (2031) | USD 989.22 Billion |

| Growth Rate (2026 - 2031) | 3.27% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Home Service Market Analysis by Mordor Intelligence

The United States home service market size is USD 842.04 billion in 2026 and is projected to reach USD 989.22 billion by 2031, reflecting a 3.27% CAGR through the forecast period. Demand is increasingly shaped by aging housing stock, homeowner lock-in due to higher mortgage rates, and a shift from reactive repairs toward AI-enabled maintenance plans that create recurring revenue relationships for service providers. The median American home purchased in 2024 was 36 years old, a full decade older than homes bought in 2012, underscoring the steady accumulation of deferred maintenance liabilities. Elevated mortgage rates expected to hover between 6% and 6.5% through 2026 have frozen household mobility, redirecting capital that might have funded relocations into renovation budgets instead[1]Mortgage Bankers Association, “MBA Forecast: Total Single-Family Mortgage Originations to Increase 8 percent to $2.2 Trillion in 2026,” Mortgage Bankers Association, www.mba.org. Tax credits for energy upgrades, along with state-administered rebates, continue to steer installation work toward heat pumps, weatherization, and panel upgrades, which supports the installation mix even as big-ticket remodels remain sensitive to financing costs. Digital marketplaces and embedded checkouts compress search and booking friction, moving more transactions online as platforms invest in AI-guided scoping and instant confirmations. Persistent labor shortages and uneven municipal licensing requirements widen cost dispersion across regions and push operators to apply technology, structured memberships, and route density strategies to protect margins.

Key Report Takeaways

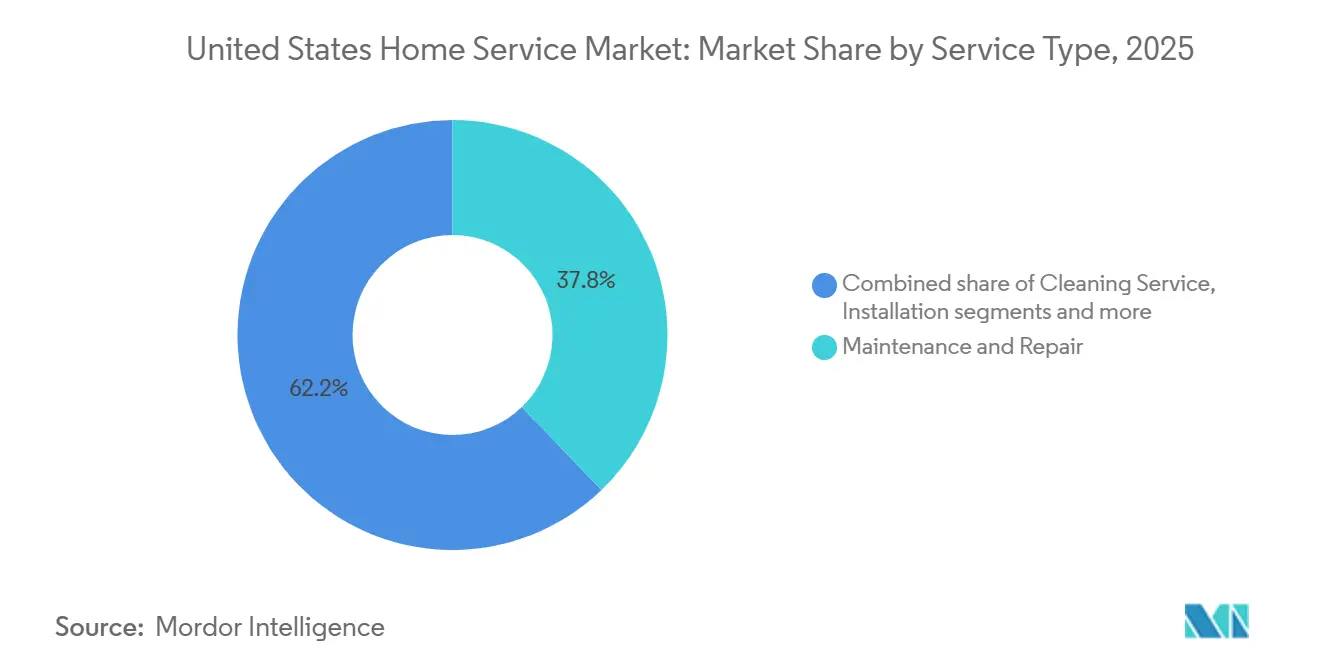

- By service type, maintenance & repair led with 37.82% of the United States home service market share in 2025, while installation & smart-home integration is forecast to expand at a 4.34% CAGR to 2031.

- By booking channel, offline/traditional accounted for 65.13% of the United States home service market size in 2025, while online marketplaces & apps are projected to grow at a 3.56% CAGR through 2031.

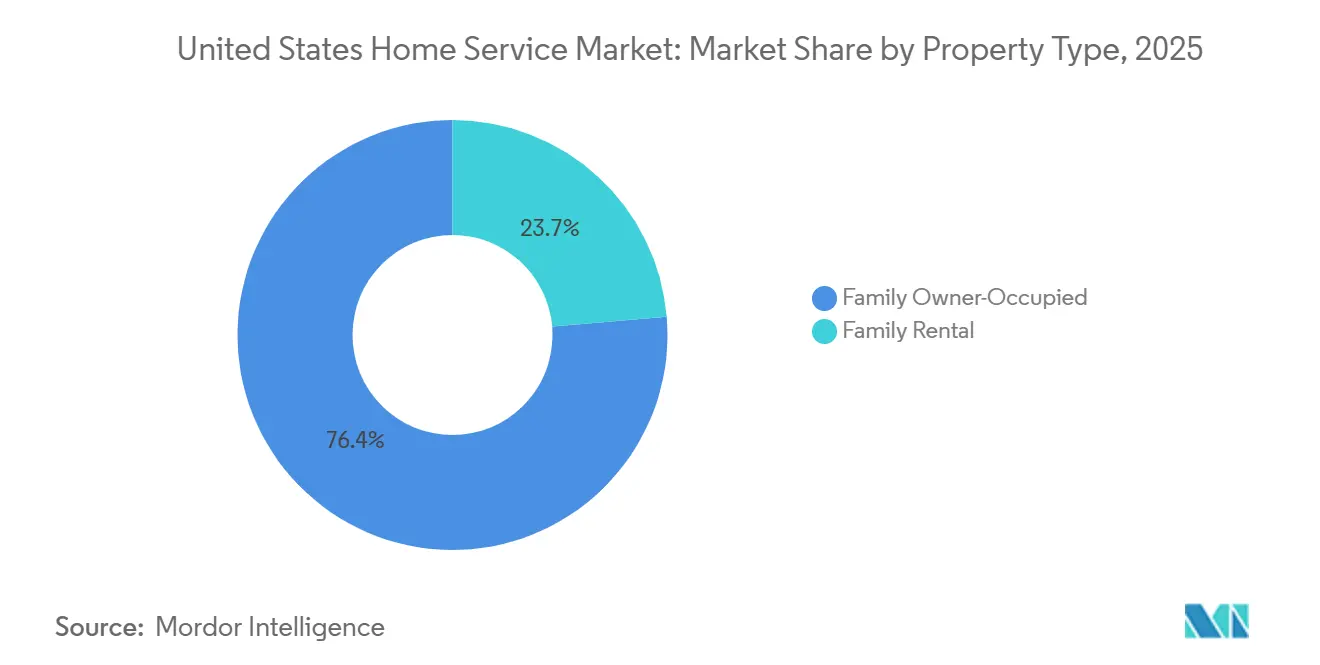

- By property type, family owner-occupied held 76.35% of the United States home service market share in 2025, while the family rental segment is advancing at a 4.13% CAGR to 2031.

- By geography, the South captured 34.73% of the United States home service market share in 2025, while the West is expected to register the fastest growth at a 3.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Home Service Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging housing stock boosting repair demand | +1.2% | National, particularly acute in Northeast and Midwest with oldest housing stock | Long term (≥ 4 years) |

| Elevated home equity levels supporting discretionary projects | +0.9% | National, with concentration in the Midwest & Northeast | Medium term (2-4 years) |

| Digital marketplaces simplifying pro discovery & booking | +0.5% | National, the highest urban density areas | Medium term (2-4 years) |

| Climate-resiliency incentives accelerating retrofit work | +0.4% | National, with early gains in California, the Northeast corridor | Short term (≤ 2 years) |

| AI-powered predictive-maintenance subscriptions are creating recurring revenue pools | +0.3% | National, early adoption in high-income coastal metros | Long term (≥ 4 years) |

| Growth of rental housing and property turnover | +0.3% | National, spill-over to high-growth Sun Belt markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Housing Stock Driving Structural Repair Demand

The aging profile of United States homes increases service intensity and tilts spending toward essential systems such as HVAC, plumbing, and electrical. Recent analysis from the Federal Reserve Bank of Philadelphia shows older homes carry higher average repair needs, with structural interventions and mechanical systems contributing meaningfully to the repair mix. Homes purchased in 2024 carried a median age of 36 years, up from 27 years in 2012, reflecting constrained new-construction supply and affordability barriers that push buyers toward older inventory. This demographic tilt translates directly into service intensity: the Federal Reserve Bank of Philadelphia estimates that homes built before 1940 require an average of USD 4,820 in repairs, compared to USD 3,276 for units constructed after 2000, with structural work alone averaging USD 5,179 per intervention[2]Federal Reserve Bank of Philadelphia, “Home Repair Costs 2025: Updated Estimates and New Measures of Cooling Needs,” Federal Reserve Bank of Philadelphia, www.philadelphiafed.org. As newer buyers take ownership of older inventory, deferred maintenance backlogs continue to convert into booked jobs, especially for emergency services that cannot be postponed in the United States home service market.

Elevated Home Equity Unlocking Discretionary Spending

Household equity remains a significant buffer for renovation budgets, even after a mild year-over-year softening in 2025. Harvard’s Joint Center for Housing Studies projects homeowner improvement and repair outlays of USD 520 billion in 2026, pointing to steady spending despite macro uncertainty[3]Forisk, “U.S. Housing Starts Outlook, Q4 2025 Update,” Forisk, forisk.com. In this context, mortgage lock-in that discourages relocations continues to redirect household dollars toward upgrades, maintenance, and mid-ticket projects in the United States home service market. Access to home equity lines of credit at rates below unsecured alternatives further supports planned improvements for qualified borrowers, which benefits trades with clear ROI narratives like weatherization and system efficiency upgrades in the United States home service market. However, equity is concentrated among higher-income owners and older households, which channels the strongest discretionary spend toward specific metros and suburban corridors. That distribution helps explain persistent strength in essential maintenance alongside selective upgrading in the United States home service market.

Digital Marketplaces Compressing Discovery and Booking Friction

Online platforms are moving beyond directories to integrated transaction engines that use AI to scope jobs, price tasks, and secure professionals with instant confirmation. Angi reports double-digit growth in proprietary service requests and leads, with the majority of volume now running through proprietary channels and AI tools lifting homeowner conversion and pro selection rates in the United States home service market. Thumbtack has continued to expand product features, financing access, and distribution partnerships, while also integrating conversational interfaces to streamline service requests for users who prefer chat-based experiences. TaskRabbit extended its national footprint to all 50 states and reinforced embedded checkout with IKEA and other retail brands so customers can book assembly or installation as part of product purchase flows in the United States home service market. These marketplace and embedded commerce dynamics cut search time and reduce returns by ensuring complex items are paired with professional assembly from the start. The path from discovery to confirmed booking has become shorter, which supports steady online share gains across categories in the United States home service market.

AI-Powered Predictive Maintenance Shifting Revenue Models

Memberships and predictive diagnostics are converting episodic calls into scheduled tune-ups and proactive interventions that reduce surprises for homeowners. Frontdoor reports strong revenue and profitability with high gross margins supported by scaled plan membership and digital troubleshooting that can eliminate truck rolls in the United States home service market. American Home Shield has extended plan features like video-chat support and expanded coverage limits while pairing installation services for smart devices with warranties to create bundled value for households. Service Experts highlights the role of Maintenance+ memberships that package tune-ups, priority scheduling, and discounts to improve retention and smooth seasonal revenue in the United States home service market. Porch has advanced property-level data products and fee-based insurance services that draw on inspection insights, positioning data as a lever to predict service needs and manage risk. As AI models learn from equipment telemetry, past work orders, and local weather patterns, operators can automate reminders, route technicians more efficiently, and capture higher lifetime value per household in the United States home service market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortages are inflating costs & lead times | -0.8% | National, acute in data-center construction hubs | Long term (≥ 4 years) |

| Interest-rate & inflation sensitivity of big-ticket remodels | -0.5% | National, with higher exposure in high-cost coastal metros | Medium term (2-4 years) |

| Patchwork municipal licensing rules are delaying market expansion | -0.3% | National, most restrictive in California, New York, and Washington | Long term (≥ 4 years) |

| High fragmentation and dominance of unorganized players | -0.2% | National, particularly rural and secondary markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortages Compressing Capacity and Raising Costs

Trade labor remains tight across the country, which extends lead times and pushes wages higher for in-demand crafts. Wage growth in 2025 outpaced general inflation in several construction categories, which passed through to higher project costs for homeowners. The Home Builders Institute quantifies the economic impact of this deficit at USD 10.8 billion annually, comprising higher carrying costs and USD 8.1 billion in lost production, equivalent to 19,000 homes[4]National Association of Home Builders, “HBI Report Reveals Economic Impact of Labor Shortages on Housing Production,” National Association of Home Builders, www.nahb.org. Large capital projects, including data centers, have also drawn electricians and other skilled trades with premium pay, which reduces available labor in residential markets in the United States home service market. Training pipelines are growing through union and apprenticeship programs, but credential gaps still affect field supervision and project management roles that are essential for scaling service capacity. The combination of scarce labor, rising wages, and project backlog increases the operational value of AI scheduling and customer self-service features in the United States home service market.

Interest-Rate Sensitivity Dampening Discretionary Remodeling

Borrowing costs remain higher than pandemic-era lows, which dampens financing-driven remodels even as lock-in sustains repair spending. MBA expects single-family origination volumes to stabilize with an improving 2026 backdrop, but the path of rates keeps many owners on the sidelines for large, discretionary projects in the United States home service market. Remodeler sentiment dipped in late 2025, and contractors cited economic and policy uncertainty as headwinds to near-term backlog growth. Harvard’s leading indicator points to slow but positive growth into mid-2026, which supports essential maintenance but limits upside for discretionary scope in the United States home service market. Input cost variability remains a factor for contractors who must price jobs across volatile categories like lumber and select imported materials, which can tighten margins when quotes are held for extended periods. In this environment, service providers emphasize smaller, high-ROI upgrades and maintenance plans that fit within household budgets in the United States home service market.

Segment Analysis

By Service Type: Installation & Smart-Home Integration Outpacing Legacy Categories

Maintenance & Repair commanded 37.82% of 2025 revenue and remains the anchor category as households prioritize essential systems that keep homes safe and functional in the United States home service market. The United States home service market share for Maintenance & Repair reflects the combination of aging assets, code compliance needs, and event-driven failures that cannot be deferred. Analysis of repair costs indicates higher per-job spend for older structures and specialized systems, which sustains a steady cadence of work for HVAC, plumbing, and electrical trades. Providers are also broadening service menus to capture adjacent tasks that can be bundled with diagnostics or seasonal tune-ups in the United States home service market. As labor constraints keep crews tight, many operators favor recurring visits and customer memberships that reduce acquisition friction and stabilize scheduling.

Installation & Smart-Home Integration posts the fastest forecast growth at a 4.34% CAGR from 2026 to 2031, supported by incentives, equipment advances, and mainstream adoption of connected devices. Heat pump credits under federal programs influence installation mix, while smart thermostats, cameras, and locks are now common add-ons during broader projects in the United States home service market. ADT’s platform integrates security and smart-home features with partners in the device ecosystem, which helps create managed experiences for homeowners who want interoperable systems. American Home Shield and other plan providers have extended their offerings to include smart device installation paired with protection plans, closing the loop between device purchase, setup, and ongoing support in the United States home service industry. As more households upgrade to efficient equipment and connected devices, installers who master both code requirements and digital integrations gain a durable advantage in the United States home service market.

Note: Segment shares of all individual segments available upon report purchase

By Booking Channel: Online Marketplaces Gaining Share Through AI and Integration

Offline/Traditional still accounts for 65.13% of 2025 revenue, signaling the role of trusted local relationships and in-person scoping for complex work in the United States home service market. Yet the United States home service market size is tilting toward digital as Online Marketplaces & Apps are forecast to grow at 3.56% through 2031, aided by AI features that price jobs, match professionals, and confirm bookings instantly. Angi reports that its proprietary channels now drive the vast majority of volume, and that AI tools like the AI Helper lift conversion while spam protections reduce refund requests in the United States home service market. Thumbtack has expanded category coverage and embedded new booking features while opening financing channels and aligning with conversational platforms that match modern user preferences. TaskRabbit’s expansion to all 50 states and its embedded checkout partnerships have shown that frictionless booking at the point of purchase drives service attachment and reduces product returns in the United States home service market.

Subscription and service plans are a growing pathway that translates emergency repair relationships into predictable revenue. Frontdoor has demonstrated that scaled membership models can deliver strong gross margins and stable growth, supported by digital diagnostics that resolve some issues without a truck roll in the United States home service market. Service Experts packages seasonal tune-ups, priority scheduling, and discounts within Maintenance+ memberships, which keep customers engaged throughout the year. As platforms standardize pricing and integrate with retail product checkouts, the United States home service industry benefits from lower acquisition costs and higher repeat rates. These models also create data loops that inform predictive maintenance, enabling proactive outreach before failures happen. Over time, the channel mix becomes more balanced as digital scale and trust systems mature in the United States home service market.

By Property Type: Family Rental Growth Reflecting Institutional Investment and HOA Expansion

Family Owner-Occupied generated 76.35% of 2025 spending, reflecting households’ direct stake in property upkeep and comfort in the United States home service market. The United States home service market share for this segment is supported by aging systems, code compliance, and energy savings opportunities that motivate essential service work. Equity-funded projects and tax-credited upgrades keep planned maintenance and mid-sized improvements in scope for qualified owners. Many providers are layering memberships and multi-system care plans to increase retention and lifetime value across owner-occupied homes in the United States home service market. Strength in essential services also insulates this segment from the full impact of slower big-ticket remodels.

Family Rental is expected to expand at a 4.13% CAGR through 2031 as institutional managers and associations professionalize maintenance schedules and vendor management. The United States home service market size for rental-related work benefits from standardized turn services, seasonal HVAC tune-ups, landscaping, and compliance-driven tasks that protect asset values and tenant satisfaction. Community associations number near 373,000 and continue to grow, which broadens centralized maintenance contracting and supports scale for regional providers. Elevated owning costs relative to renting keep renters in place longer, which supports sustained demand for landlord-funded upkeep and turnover preparation in the United States home service market. As portfolios expand in selected metros, rental maintenance pipelines become more predictable, supporting planned staffing and route density gains.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The South captured 34.73% of 2025 revenue, reflecting population scale, storm-related repairs, and large stocks of older homes in the region. The United States home service market size in the South is reinforced by higher average repair outlays per job and sustained demand for core systems that underpin habitability. Repair-cost inflation related to storm recovery added pressure to budgets for roofs, exteriors, and water-damaged systems, which preserved backlogs for specialty contractors. As insurance and building code requirements evolve, service providers that can navigate claim processes and code compliance strengthen their position in the United States home service market. Over the forecast horizon, demographic growth and weather-driven demand support steady activity levels in the South.

The West, while smaller in absolute value, is forecast to grow the fastest at 3.92% through 2031, aided by energy codes and higher adoption of efficient systems. California’s emphasis on performance standards encourages upgrades to insulation, windows, ventilation, and HVAC, which sustains premium installation opportunities in the United States home service market. Providers operating in coastal metros face tighter labor markets and higher compliance costs, which makes process digitization and predictive scheduling valuable for maintaining margins. Remodeler sentiment was softer in late 2025, but essential maintenance demand remained resilient in the West due to aging systems and energy-efficiency targets. Over time, code-driven upgrades and retrofit incentives help sustain installation pipelines for qualified contractors in the United States home service market.

The Northeast and Midwest show steady demand patterns tied to older housing stock, tight inventories, and concentration of equity-rich homeowners. The Northeast benefited from higher home values in 2025 and a large base of older properties that require regular upkeep, which supports contractor pricing power in core trades within the United States home service market. The Midwest posted pronounced price gains in several metros through 2025, while affordability and retiree migration sustained interest in maintenance and modest improvement projects in the United States home service market. Average repair costs in both regions remain meaningful, with specialty work in mechanicals and envelope systems a consistent source of demand. As owners in these regions hold properties longer due to rate lock-in, planned upgrades, and energy credits are likely to support installation and maintenance activity in the United States home service market.

Competitive Landscape

The market remains moderately consolidated at the platform and roll-up layer while still highly fragmented across local trades. Angi reported progress on an AI-first strategy with stronger proprietary channels and improved conversion from AI tools, while preparing to unify its technology stack and expand native applications in the United States home service market. Thumbtack invested in feature expansion, financing access, and conversational integrations to streamline matching and booking for a base of active professionals. TaskRabbit’s embedded checkout partnerships illustrated the value of attaching services at the point of sale, reinforcing omnichannel routes to growth in the United States home service market. These digital players rely on AI to reduce acquisition costs and to raise lifetime value through superior matching and repeat usage. At the same time, route-density roll-ups and specialty distributors are extending reach through acquisition and integration.

Regional consolidators demonstrate scale advantages in procurement, scheduling, and back-office operations. Rollins completed 44 acquisitions in 2024 and reported double-digit revenue growth in Q3 2025, highlighting the strength of service routes in pest control for the United States home service market. TopBuild acquired Progressive Roofing and Specialty Products & Insulation to expand its installation and specialty distribution businesses, with integration synergies expected to accrue over the next two years. Installed Building Products continued to add manufacturing and local installers, supported by balance-sheet actions that extend debt maturities and fund growth in the United States home service market. HomeServe grew through utility partnerships and selective acquisitions, which broadened repair capacity across North America. These moves reflect a search for scale where route density and category breadth can improve margins and service reliability.

Subscription and integrated service models continue to differentiate incumbents. Frontdoor recorded strong revenue and earnings performance in Q3 2025, supported by high-margin membership economics, while American Home Shield expanded plan features and smart device installation to create bundled value in the United States home service market. Porch pivoted toward a fee-based insurance services model anchored by a reciprocal exchange structure that reduces exposure to catastrophe losses and supports scalable premium growth. ADT highlighted an intelligent home roadmap that merges security with device interoperability, which aligns with rising consumer expectations for unified smart-home experiences in the United States home service market. With municipal licensing rules tightening in key states like California, firms that can maintain compliance footprints and credentialed labor while deploying AI to relieve scheduling and quoting bottlenecks are best positioned to scale profitably in the United States home service market.

United States Home Service Industry Leaders

Angi Inc.

Frontdoor Inc.

Rollins Inc.

Chemed Corporation

ServiceMaster Brands

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Installed Building Products priced USD 500 million of 5.625% senior unsecured notes due 2034 to refinance existing 2028 notes, pay fees, and for general corporate purposes.

- November 2025: Angi Inc. reported third-quarter 2025 results with revenue of about USD 265.6 million, reflecting a year-over-year decline but with growth in certain service channels such as proprietary service requests and leads.

- November 2025: Frontdoor Inc. delivered strong third-quarter 2025 results with USD 618 million in revenue, marking a 14 % year-over-year increase and improved profitability metrics.

- October 2025: TopBuild Corp completed the acquisition of Specialty Products & Insulation (SPI) for approximately USD 1 billion in cash, expanding its footprint in mechanical insulation distribution.

United States Home Service Market Report Scope

The United States home service market comprises professional services designed to maintain, repair, improve, and enhance residential properties to meet the functional and lifestyle needs of homeowners and tenants. The market is segmented by service type, booking channel, property type, and region. By service type, the market is segmented into maintenance & repair (including plumbing, electrical repair, HVAC servicing, and appliance repair), cleaning services (such as home cleaning, carpet & upholstery cleaning, and window cleaning), improvement & remodeling, installation & smart-home integration, exterior & landscaping, and others (including pest control services, security & safety services, and moving & relocation services). By booking channel, the market is segmented into offline/traditional, online marketplaces & apps, and subscription/service plans. By property type, the market is segmented into family owner-occupied and family rental properties. By region, the market is segmented into the Northeast, Midwest, South, and West. The report offers the market size in value terms in USD for all the above-mentioned segments.

| Maintenance & Repair | Plumbing |

| Electrical repair | |

| HVAC servicing | |

| Appliance repair | |

| Cleaning Services (home cleaning, Carpet & upholstery cleaning, Window cleaning etc.) | |

| Improvement & Remodeling | |

| Installation & Smart-Home Integration | |

| Exterior & Landscaping | |

| Others (Pest Control Services, Security & Safety Services ,Moving & Relocation Services etc) |

| Offline / Traditional |

| Online Marketplaces & Apps |

| Subscription / Service Plans |

| Family Owner-Occupied |

| Family Rental |

| Northeast |

| Midwest |

| South |

| West |

| By Service Type | Maintenance & Repair | Plumbing |

| Electrical repair | ||

| HVAC servicing | ||

| Appliance repair | ||

| Cleaning Services (home cleaning, Carpet & upholstery cleaning, Window cleaning etc.) | ||

| Improvement & Remodeling | ||

| Installation & Smart-Home Integration | ||

| Exterior & Landscaping | ||

| Others (Pest Control Services, Security & Safety Services ,Moving & Relocation Services etc) | ||

| By Booking Channel | Offline / Traditional | |

| Online Marketplaces & Apps | ||

| Subscription / Service Plans | ||

| By Property Type | Family Owner-Occupied | |

| Family Rental | ||

| By Region | Northeast | |

| Midwest | ||

| South | ||

| West |

Key Questions Answered in the Report

What is the current size and growth outlook for the United States home service market?

The United States home service market size is USD 842.04 billion in 2026 and is projected to reach USD 989.22 billion by 2031 at a 3.27% CAGR. This outlook reflects aging housing stock, steady essential maintenance, and rising use of AI-enabled service models.

Which service categories are leading and which are growing fastest in the United States home service market?

Maintenance & Repair leads with 37.82% of 2025 revenue, while Installation & Smart-Home Integration is the fastest with a 4.34% forecast CAGR through 2031, supported by energy-efficiency incentives and connected device adoption.

How are digital marketplaces changing homeowner behavior in the United States home service market?

Platforms embed AI for project scoping, instant booking, and spam control, which raises conversion and reduces friction from search to confirmed job. Proprietary channels now drive most volume for leading platforms, and embedded checkouts in retail lift service attachment.

What incentives are available for energy-efficient upgrades in the United States home service market?

Federal credits include up to USD 3,200 annually for qualifying energy-efficient home improvements and a 30% clean energy credit for eligible systems like solar and geothermal through 2032, subject to IRS guidance and equipment criteria.

What labor dynamics are most affecting the United States home service market?

The sector faces a worker shortfall that extends lead times and raises wages, with 2025 needs estimated at 439,000 additional workers. This environment increases the value of predictive scheduling, memberships, and AI-driven dispatch.

Which regions are most important and which are growing fastest in the United States home service market?

The South holds the largest 2025 revenue share at 34.73%, while the West is forecast to grow the fastest at 3.92% due to energy codes, efficiency upgrades, and higher adoption of connected systems.