Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 12.12 Billion |

| Market Size (2031) | USD 14.19 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Food Sweetener Market Analysis by Mordor Intelligence

The United States food sweetener market was valued at USD 11.74 billion in 2025 and estimated to grow from USD 12.12 billion in 2026 to reach USD 14.19 billion by 2031, at a CAGR of 3.22% during the forecast period (2026-2031). This overall growth masks significant shifts within the product portfolio. Sucrose is expected to account for 68.39% of the market value in 2024, but high-intensity sweeteners are anticipated to experience the fastest growth, with a CAGR of 3.96% through 2030. This trend is driven by increasing demand for calorie control, heightened scrutiny of product labels, and the rising use of glucagon-like peptide-1 (GLP-1) receptor agonist drugs, which are contributing to reduced sugar consumption. The number of GLP-1 receptor agonist users is projected to expand from approximately 7 million to as many as 30 million by 2030. Early data indicates that patients using these medications reduce their purchases of sweet baked goods within six months of starting therapy. Regulatory developments are also influencing the market. The United States Food and Drug Administration (FDA) approved enzyme-modified steviol glycosides in October 2024 and Brazzein preparations in July 2025, shortening the approval cycle for natural high-intensity sweeteners to approximately two years. Additionally, major beverage companies are meeting stringent added-sugar reduction targets, while retailers are emphasizing organic and non-genetically modified organism (non-GMO) certifications. These factors are encouraging cost-conscious manufacturers to adopt blended sweetener systems that maintain taste, bulk, and browning properties.

Key Report Takeaways

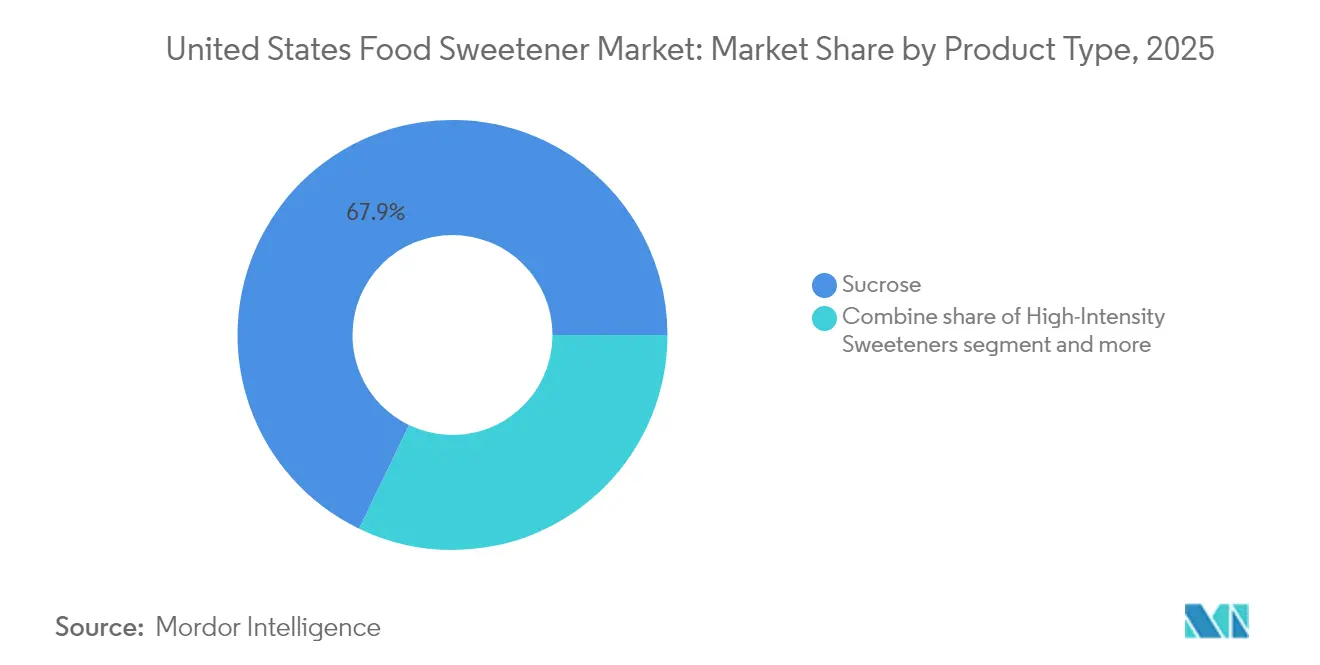

- By product type, sucrose accounted for 67.85% of the United States food sweetener market share in 2025, while high-intensity sweeteners are projected to grow at a CAGR of 3.84% through 2031.

- By application, beverages held a 44.55% value share in 2025, with the bakery and confectionery segment expected to grow at a CAGR of 3.61% by 2031.

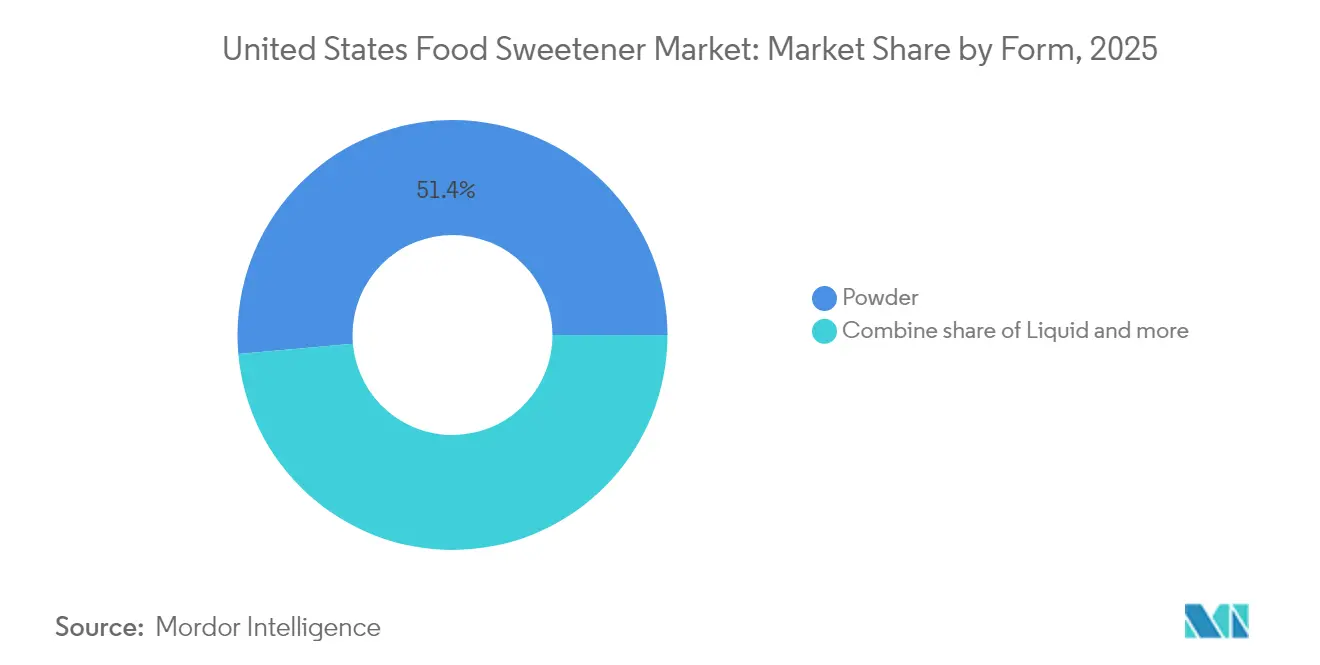

- By form, powder formats represented 51.40% of the market share in 2025, whereas liquid formats are anticipated to grow at a CAGR of 3.75% during the forecast period.

- By category, conventional variants dominated with an 82.35% share in 2025, while organic offerings are forecast to expand at a CAGR of 3.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Food Sweetener Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing obesity and diabetes drive demand for sugar reduction and alternatives | +0.8% | National, with acute prevalence in Southern and Midwestern states | Medium term (2-4 years) |

| Health awareness and label scrutiny promote low-calorie and better-for-you reformulations | +0.6% | National, urban clusters lead adoption | Short term (≤ 2 years) |

| Expansion of reduced-sugar and sugar-free products in beverages, bakery, confectionery, and dairy | +0.5% | National, beverage-heavy in West Coast and Northeast | Short term (≤ 2 years) |

| Innovations in high-intensity and natural sweeteners enhance taste and functionality | +0.4% | National, R&D hubs in Illinois, California, New Jersey | Medium term (2-4 years) |

| Technological advancements minimize off-tastes and bitterness in sweetener formulations | +0.3% | National, premium segments in coastal metros | Long term (≥ 4 years) |

| Clean-label trends boost demand for plant-based and minimally processed sweeteners | +0.2% | National, strongest in organic retail channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing obesity and diabetes in the United States drive demand for sugar reduction and alternatives

Adult obesity prevalence reached 40.3% during the 2021-2023 National Health and Nutrition Examination Survey (NHANES) cycle, with 23 states reporting rates at or above 35% in 2024. This widespread public health issue has a direct impact on sweetener demand: 38.4 million Americans are currently living with diabetes, while an additional 97.6 million individuals have prediabetes. Together, these conditions contribute to an economic burden of USD 413 billion annually in medical expenses and lost productivity [1]Source: National Center for Health Statistics, “Obesity and Severe Obesity Prevalence in Adults: United States, August 2021–August 2023,” cdc.gov. This significant financial strain has prompted payers, employers, and policymakers to actively support sugar-reduction initiatives, fostering a regulatory environment that is increasingly favorable for alternative sweeteners. Additionally, the growing use of glucagon-like peptide-1 (GLP-1) receptor agonist medications, such as semaglutide and tirzepatide, has introduced another dynamic. Users of these medications have been observed to reduce their spending on sweet baked goods by approximately 10% within six months, indicating a behavioral shift that further erodes baseline demand. As a result, product formulators are now tasked with addressing a dual challenge: replacing sugar to align with health guidelines while simultaneously creating products that remain appealing to consumers whose taste preferences are being influenced by these medications.

Health awareness and label scrutiny promote low-calorie and "better-for-you" sweetener reformulations

Label literacy has reached a critical juncture: 66% of Americans actively limited their sugar intake in 2024, an increase from 61% in the previous year. Among these consumers, 60% specifically targeted added sugars rather than naturally occurring sugars [2]Source: International Food Information Council, “Public Perceptions of Dietary Sweeteners,” ific.org. This heightened awareness is compelling brands to reformulate their products or risk becoming obsolete on store shelves. PepsiCo surpassed its 2025 target a year early, achieving 67% of its beverage volume meeting the less than or equal to 100 calories per 12-ounce threshold in 2024. Similarly, Coca-Cola reported that 30% of its global beverage volume now consists of low-calorie or no-calorie options, alongside the launch of 250 reduced-sugar products in 2024. However, a paradox remains: only 16% of sugar-limiting consumers prefer low-calorie sweeteners, while 30% still favor traditional sugars despite associated health concerns. This gap between consumer preferences and behavior underscores that taste and texture continue to be decisive factors for market success. It also highlights the strategic importance of next-generation sweeteners that replicate sucrose-like sensory profiles without the added caloric content.

Expansion of reduced-sugar and sugar-free products in beverages, bakery, confectionery, and dairy

Beverage reformulation continues to lead the market, while bakery and confectionery applications are steadily advancing. Kraft Heinz has committed to reducing 60 million pounds of sugar by the year 2025, with a notable achievement of removing 2.9 million pounds from its Brazil portfolio by 2024. Nestlé USA has taken significant steps by eliminating high-fructose corn syrup (HFCS) from more than 60 beverage recipes. Additionally, the company has introduced a proprietary sugar-restructuring technology that can achieve up to a 40% reduction in sugar content without compromising the taste of its products. Capri Sun has also made strides by reformulating its core juice drinks with monk fruit concentrate, resulting in an approximate 40% reduction in sugar content. These efforts underscore a strategic focus on capturing consumer loyalty early in the market. However, the competitive advantage for early adopters is narrowing as ingredient suppliers increasingly democratize access to innovative sweeteners through co-manufacturing partnerships and white-label solutions.

Innovations in high-intensity and natural sweeteners enhance taste and functionality

The United States Food and Drug Administration (FDA) issued no-objection letters for enzyme-modified steviol glycosides developed by Tate & Lyle in October 2024, as well as brazzein preparations from Oobli and Nanjing Bestzyme in 2025. This development highlights that natural high-intensity sweeteners can now achieve Generally Recognized as Safe (GRAS) approval within a reduced timeframe of under 24 months [3]Source: United States Food & Drug Administration,“GRAS Notice GRN 1140 Agency Response Letter,” fda.gov. Tate & Lyle's enzyme-modified stevia offers sweetness levels that are 200 to 300 times greater than sucrose while significantly reducing bitterness, effectively addressing a primary consumer concern associated with first-generation stevia extracts. Brazzein, a protein sourced from the West African Oubli fruit, provides heat stability and a clean sweetness profile, making it a practical option for applications such as baked goods and retorted dairy products where artificial sweeteners like aspartame and sucralose tend to degrade. Furthermore, allulose, a rare sugar that mimics the taste of sucrose but contains 90 percent fewer calories, received expanded use approvals from the FDA in 2024, with Tate & Lyle now producing it on a commercial scale. These regulatory advancements have significantly reduced the time required to bring innovative formulations to market, enabling brands to transition from artificial to natural sweeteners without compromising on taste or shelf life.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent FDA regulations and GRAS approval processes delay novel sweeteners' market entry | -0.4% | National, affects all manufacturers seeking new ingredient approvals | Long term (≥ 4 years) |

| Complex United States labeling rules increase compliance costs and reformulation challenges | -0.3% | National, disproportionate burden on small and mid-sized manufacturers | Medium term (2-4 years) |

| Taste issues of low-calorie sweeteners limit their application in certain products | -0.3% | National, most acute in bakery, confectionery, and full-flavor beverage segments | Short term (≤ 2 years) |

| Technical difficulties in replicating sugar's properties require multi-ingredient solutions in bakery and confectionery | -0.2% | National, concentrated in artisanal bakery and premium confectionery | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Food and Drug Administration (FDA) regulations and Generally Recognized as Safe (GRAS) approval processes delay novel sweeteners' market entry

The United States Food and Drug Administration's (FDA) Generally Recognized as Safe (GRAS) notification pathway requires the submission of detailed safety dossiers. These dossiers must include toxicology studies, assessments of metabolic fate, and exposure estimates. The preparation of such dossiers can cost between USD 500,000 and USD 2 million per ingredient and typically takes 18 to 36 months to complete. Once submitted, the FDA's stated 180-day review period often extends to 12 to 18 months if additional data is requested. For instance, Rebaudioside M (Reb M), a high-purity stevia glycoside, has been under FDA review since late 2024 (GRN 1184), delaying its commercial launch despite its widespread acceptance in other markets. This regulatory process tends to favor established companies such as Cargill and Tate & Lyle, which can spread compliance costs across their extensive global portfolios. In contrast, startups often face significant challenges due to limited financial resources, making it difficult to sustain the lengthy approval cycles. Furthermore, the January 2024 ban on Red Dye Number 3, which affects approximately 9,200 products, underscores how sudden regulatory changes can lead to significant reformulation costs. Such developments further discourage investment in innovative ingredients with uncertain approval timelines.

Complex United States labeling rules increase compliance costs and reformulation challenges

The FDA's updated Nutrition Facts label, which separates added sugars from total sugars, compels brands to reformulate their products to avoid potential consumer backlash. Products containing more than 10% of the Daily Value for added sugars per serving are now subject to increased scrutiny. To meet these requirements, manufacturers are incorporating sugar alcohols, such as sorbitol and xylitol, and high-intensity sweeteners to remain within the acceptable limits. However, sugar alcohols present their own labeling challenges: erythritol and xylitol can be excluded from total carbohydrate counts under specific conditions, whereas sorbitol and maltitol cannot, leading to formulation inconsistencies that benefit certain polyols. At the same time, state-level regulations introduce additional compliance complexities. For example, California's Proposition 65, officially known as the Safe Drinking Water and Toxic Enforcement Act of 1986, requires warning labels for products containing substances associated with cancer or reproductive harm. Furthermore, some artificial sweeteners are under review for potential inclusion on this list. These overlapping regulatory requirements significantly increase reformulation costs by 15-25% compared to markets governed by a single jurisdiction. This financial burden is particularly challenging for mid-sized manufacturers, which often lack the resources or dedicated regulatory affairs teams to navigate these multifaceted compliance demands.

Segment Analysis

By Product Type: Sucrose Anchors Value, High-Intensity Sweeteners Lead Growth

Sucrose accounted for 67.85% of the market share in 2025, maintaining its dominance due to its versatile functionality, including bulk, browning, moisture retention, and use as a fermentation substrate across bakery, confectionery, and dairy applications. However, high-intensity sweeteners are projected to grow at a compound annual growth rate (CAGR) of 3.84% from 2026 to 2031, marking the fastest growth among product types. This growth is driven by beverage reformulation efforts and regulatory initiatives aimed at reducing added sugars. Within the high-intensity sweeteners category, natural options such as stevia and monk fruit are increasingly replacing artificial alternatives like aspartame and sucralose, as clean-label requirements gain traction.

Stevia extract is now featured in over 14,000 global stock-keeping units (SKUs), with U.S. beverage brands accounting for 45% of its adoption. Monk fruit extract, while more expensive, offers a cleaner sweetness profile and has become the preferred choice for premium reformulations. For instance, Capri Sun achieved a 40% sugar reduction by utilizing monk fruit concentrate to maintain taste quality. Starch sweeteners and sugar alcohols serve as a middle-ground option, providing bulk and moderate sweetness at a lower cost compared to sucrose. Dextrose and high-fructose corn syrup (HFCS) continue to be widely used in processed foods, although HFCS faces reputational challenges. In 2024, Nestlé USA removed HFCS from over 60 beverage recipes.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Beverages Dominate, Bakery Accelerates

The beverages segment accounted for 44.55% of the application share in 2025, driven by its ability to reformulate products effectively. Liquid systems can incorporate high-intensity sweeteners without the textural challenges often encountered in solid foods. For instance, PepsiCo achieved 67% compliance with its target of less than 100 calories per 12-ounce serving, while Coca-Cola reported that 30% of its product volume consists of low- or no-calorie options. These achievements underscore the adaptability of beverage companies in addressing both regulatory requirements and evolving consumer preferences. The ability to pivot quickly has positioned the beverages segment as a leader in the adoption of alternative sweeteners.

However, the bakery and confectionery segment is projected to grow at the fastest rate of 3.61% during the forecast period of 2026 to 2031. This growth is attributed to manufacturers leveraging multi-ingredient sweetener systems to replicate the functional properties of sugar, such as bulk, browning, and moisture retention. Ingredients like allulose and erythritol have become integral to reduced-sugar cookie and cake formulations, offering Maillard browning and crumb structure improvements that earlier generations of polyols could not achieve. Meanwhile, dairy and desserts represent a high-value application area where sweeteners must withstand processes like pasteurization, homogenization, and cold-chain distribution. Brazzein, a protein-based sweetener known for its heat stability, has emerged as a viable option for retorted dairy products, a niche where artificial sweeteners like aspartame and sucralose often degrade under high temperatures.

By Form: Powder Leads, Liquid Gains on Dosing Precision

Powder formats accounted for a 51.40% market share in 2025, primarily due to their stability, ease of transport, and compatibility with dry-mix applications such as baking mixes, protein powders, and instant beverages. Spray-dried stevia and monk fruit extracts are the leading options within the natural high-intensity sweetener segment, while crystalline sucrose and dextrose continue to dominate traditional sweetener volumes. These powder formats are particularly favored in industries where long shelf life and ease of handling are critical factors.

In contrast, liquid sweeteners are expected to grow at a compound annual growth rate (CAGR) of 3.75% during the forecast period from 2026 to 2031. This growth is largely attributed to their increasing adoption in beverage production lines, where they offer significant advantages in precise dosing. Liquid high-fructose corn syrup (HFCS) and invert sugar syrups facilitate automated blending processes at high throughput levels, which helps reduce labor costs and ensures consistency by minimizing batch-to-batch variability. Additionally, liquid stevia extracts, despite being more expensive than their powdered counterparts, eliminate the need for a dissolution step and help reduce foam formation in carbonated beverages, making them a preferred choice in specific applications.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Conventional Dominates, Organic Gains on Clean-Label Momentum

Conventional sweeteners accounted for 82.35% of the market share in 2025, driven by their cost advantages and the presence of well-established supply chains. Organic sweeteners, on the other hand, are expected to grow at a compound annual growth rate (CAGR) of 3.65% during the forecast period from 2026 to 2031. This growth is primarily attributed to their clean-label positioning, which appeals to health-conscious consumers, and the willingness of customers to pay premium prices for natural and organic products. The organic sweeteners segment is anchored by products such as organic cane sugar, organic agave syrup, and organic stevia extract. Retailers like Whole Foods, Sprouts, and Trader Joe's play a pivotal role in driving the distribution of these products, ensuring their availability to a broader consumer base.

To achieve organic certification, manufacturers must adhere to the standards set by the United States Department of Agriculture (USDA) National Organic Program. These standards strictly prohibit the use of synthetic pesticides and genetically modified organisms (GMOs) and require third-party verification to ensure compliance. While these requirements increase ingredient costs by approximately 20 to 40 percent, they also enable brands to charge retail premiums ranging from 30 to 50 percent. This pricing strategy makes organic sweeteners a profitable option for businesses despite the higher input costs. In contrast, conventional sweeteners benefit significantly from economies of scale. Companies such as Cargill and Archer Daniels Midland (ADM) operate integrated corn wet-milling facilities that produce high-fructose corn syrup (HFCS), dextrose, and corn oil. These facilities allow fixed costs to be distributed across multiple revenue streams, enhancing cost efficiency and profitability.

Geography Analysis

The United States constitutes the entirety of the analyzed market, with regional demand influenced by obesity prevalence, regulatory measures, and retail channel dynamics. Southern and Midwestern states report the highest adult obesity rates, with 23 states recording a prevalence of 35 percent or higher in 2024. This has driven significant demand for sugar-reduction solutions in these regions. Coastal metropolitan areas, including New York, Los Angeles, San Francisco, and Seattle, lead in clean-label adoption. Natural and organic sweeteners account for 15 to 20 percent of sales in Whole Foods and specialty retailers, compared to 5 to 8 percent in Walmart and dollar stores. This disparity reflects income and education differences, as households earning over 100,000 United States Dollars (USD) annually are 2.5 times more likely to purchase organic sweeteners than those earning less than 50,000 USD.

Beverage reformulation is a key driver of volume growth in the West Coast and Northeast, where state-level soda taxes and school-district procurement policies favor low-calorie options. States such as California, Oregon, and Washington, along with several Northeastern cities, impose excise taxes on sugar-sweetened beverages. These taxes encourage manufacturers to use high-intensity sweeteners to avoid these levies. For instance, PepsiCo's acquisition of Poppi, a prebiotic soda brand valued at 1.95 billion USD, highlights this trend. Poppi contains 5 grams of sugar per can compared to 39 grams in regular Pepsi, positioning the company to attract health-conscious consumers in high-tax regions. In contrast, the Midwest and South show slower adoption of reformulated beverages, with traditional full-sugar sodas and sweet tea maintaining a dominant share in convenience and grocery channels.Regulatory measures vary significantly across states and municipalities. For example, New York City's menu-labeling requirements for chain restaurants mandate calorie counts for all menu items, accelerating reformulation efforts in foodservice sweetener applications. Similarly, California's Proposition 65, which requires warning labels for products containing substances linked to cancer or reproductive harm, has led some manufacturers to proactively remove controversial artificial sweeteners from their West Coast product lines. These localized regulations fragment the national market, compelling large manufacturers to either maintain region-specific formulations or adopt the most stringent standards nationwide to streamline supply chains.

Competitive Landscape

The United States food sweetener market demonstrates moderate concentration, with companies such as Cargill, Archer Daniels Midland, Tate & Lyle, and Ingredion dominating through integrated corn-wet-milling and stevia-extraction assets, which provide scale advantages in commodity segments. However, the high-intensity natural sweetener segment remains fragmented, with specialty suppliers like PureCircle (now part of Ingredion), Sweet Green Fields, GLG Life Tech, and Whole Earth Brands competing through proprietary extraction and purification technologies.

Vertical integration is a key strategy for incumbents. For instance, Cargill manages seed-to-sweetener stevia supply chains in Kenya and Paraguay, ensuring quality control and cost predictability. Similarly, Tate & Lyle's enzyme-modified steviol glycoside platform, which received Food and Drug Administration (FDA) Generally Recognized as Safe (GRAS) approval in October 2024, highlights how established players utilize research and development capabilities to differentiate commodity inputs.

Emerging opportunities in the market focus on rare sugars and precision fermentation platforms. Bonumose, for example, produces tagatose, a low-glycemic sugar with prebiotic properties, through enzymatic isomerization, targeting diabetic-friendly and gut-health applications. Manus Bio employs synthetic biology to ferment allulose and other rare sugars at purities exceeding 99 percent, addressing the off-flavors associated with earlier enzymatic processes. While these startups face challenges such as high capital requirements and regulatory hurdles, successful GRAS approvals could unlock USD 50 to 100 million in early-stage revenue before larger incumbents replicate their technologies.

United States Food Sweetener Industry Leaders

Cargill, Incorporated

Archer Daniels Midland Company

Ingredion Incorporated

Tate & Lyle PLC

ASR Group International, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2024: Tate & Lyle and Manus formed “The Natural Sweetener Alliance” to launch an all‑Americas sourced and manufactured, bioconverted stevia Reb M sweetener, produced at Manus’ Augusta, Georgia facility, to strengthen secure, natural sugar‑reduction solutions for food and beverage brands across the Americas

- April 2024: Ingredion, a US-based company, introduced PURECIRCLE Clean Taste Solubility Solution (CTSS), a highly soluble, clean-label stevia sweetener. This product is designed to achieve 100% sugar reduction across various food and beverage applications, reinforcing stevia's position in the US market for next-generation sweeteners.

- January 2024: North Carolina‑based Elo Life Systems raised USD 20.5 million in an oversubscribed Series A2 round to scale and commercialize its monk‑fruit‑derived high‑intensity sweetener and expand its molecular‑farming ingredient pipeline, strengthening innovation and capacity in the US food sweetener industry

United States Food Sweetener Market Report Scope

A sweetener is a substance added to food or beverages to give them the flavor of sweetness, either because it contains sugar or a sugar replacement with a sweet flavor.

The US food sweetener market is segmented by product type and application. By product type, the market is segmented into sucrose, starch sweeteners and sugar dextrose alcohols, and high-intensity sweeteners (HIS). Starch sweeteners and sugar dextrose alcohols include HFCS, maltodextrin, sorbitol, and xylitol. The other starch sweeteners and sugar alcohols include glucose syrup, glucose-fructose syrup, fructose-glucose syrup, isoglucose, fructose, mannitol, maltitol, erythritol, lactitol, isomalt. High-Intensity sweeteners include sucralose, aspartame, saccharin, cyclamate, ace-k, neotame, and stevia. The other high-intensity sweeteners (HIS) include glycyrrhizin, mogroside V, Luo Han Guo, thaumatin, and monatin. By application, the market is segmented into dairy, bakery, beverages, confectionery, soups, sauces and dressings, and other applications. For each segment, the market sizing and forecasts have been done on the basis of value (in USD).

By Product Type

| Sucrose | ||

| Starch Sweeteners and Sugar Alcohols | Dextrose | |

| High Fructose Corn Syrup (HFCS) | ||

| Maltodextrin | ||

| Sorbitol | ||

| Xylitol | ||

| Other Starch Sweeteners and Sugar Alcohols | ||

| High-Intensity Sweeteners | Artificial High-Intensity Sweeteners | Sucralose |

| Aspartame | ||

| Saccharin | ||

| Neotame | ||

| Cyclamate | ||

| Acesulfame Potassium (Ace-K) | ||

| Other Artificial HIS | ||

| Natural High-Intensity Sweeteners | Stevia Extract | |

| Monk Fruit Extract | ||

| Other Natural HIS | ||

| Other Sweeteners | ||

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Soups, Sauces, and Dressings |

| Other Applications |

By Form

| Powder |

| Liquid |

| Crystal |

By Category

| Conventional |

| Organic |

| By Product Type | Sucrose | ||

| Starch Sweeteners and Sugar Alcohols | Dextrose | ||

| High Fructose Corn Syrup (HFCS) | |||

| Maltodextrin | |||

| Sorbitol | |||

| Xylitol | |||

| Other Starch Sweeteners and Sugar Alcohols | |||

| High-Intensity Sweeteners | Artificial High-Intensity Sweeteners | Sucralose | |

| Aspartame | |||

| Saccharin | |||

| Neotame | |||

| Cyclamate | |||

| Acesulfame Potassium (Ace-K) | |||

| Other Artificial HIS | |||

| Natural High-Intensity Sweeteners | Stevia Extract | ||

| Monk Fruit Extract | |||

| Other Natural HIS | |||

| Other Sweeteners | |||

| By Application | Bakery and Confectionery | ||

| Dairy and Desserts | |||

| Beverages | |||

| Soups, Sauces, and Dressings | |||

| Other Applications | |||

| By Form | Powder | ||

| Liquid | |||

| Crystal | |||

| By Category | Conventional | ||

| Organic | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the United States food sweetener market in 2026?

The United States food sweetener market size stands at USD 12.12 billion in 2026.

What is the expected growth rate for United States sweeteners through 2031?

Aggregate value is projected to grow at a 3.22% CAGR, reaching USD 14.19 billion by 2031.

Which sweetener segment is growing the fastest?

High-intensity sweeteners, especially natural stevia and monk fruit, are forecast to expand at 3.84% per year.

Why are bakery and confectionery applications accelerating?

Multi-ingredient blends such as allulose plus erythritol replicate sugar’s bulk and browning, enabling 3.61% CAGR in bakery and confectionery sales.

How are FDA approvals shaping innovation?

Recent GRAS clearances for enzyme-modified stevia and Brazzein cut the approval timeline to about two years, allowing quicker launch of clean-label high-intensity options.