Market Trends of US Engineering, Procurement, And Construction Management (EPCM) Industry

Investments in Infrastructure are Poised to Propel the EPCM Sector

Infrastructure investment in the United States, especially in the engineering, procurement, and construction (EPC) sector, is pivotal for economic growth and modernization. The country is channeling significant funds into enhancing transportation networks, public utilities, and other crucial infrastructure to keep pace with a growing population and advancing technology.

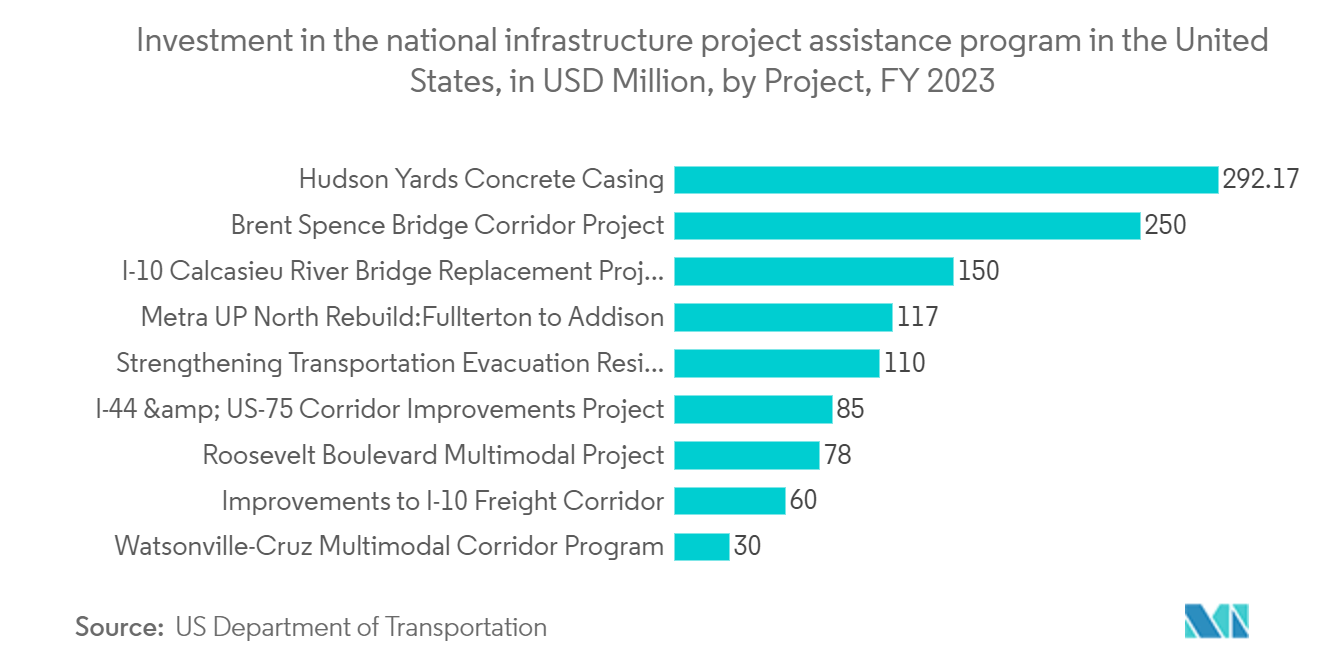

In 2023, the President and Transportation Secretary unveiled that the Biden-Harris Administration had allocated nearly USD 1.2 billion from the new National Infrastructure Project Assistance (Mega) discretionary grant program to nine national projects. These initiatives aim to bolster the economy, create well-paying jobs, fortify supply chains, enhance resident mobility, and elevate the safety of the transportation systems.

The Mega grant initiative, a product of President Biden's landmark infrastructure legislation, is tailored for projects that outstrip conventional funding programs in scale or complexity. Eligible ventures include highways, bridges, ports, and public transportation.

By 2026, the Mega program is expected to infuse a total of USD 5 billion into revamping the US infrastructure, with a focus on benefiting current and future generations. In the latest application round, the US Department of Transportation fielded requests totaling around USD 30 billion, far surpassing the available USD 1 billion in 2022. Notable projects include:

USD 292 million for Hudson Yards Concrete Casing, Section 3 (New York): This funding will complete the final section of the concrete casing, securing the right-of-way for the new Hudson River Tunnel and setting the stage for the Gateway Project. The Hudson Tunnel initiative, upon fruition, promises improved commute times, enhanced Amtrak reliability on the Northeast Corridor (NEC), and a boost to the regional economy, which houses 17% of the US population. Amtrak anticipates the project will create 72,000 jobs during construction, with a focus on union partnerships for job training.

USD 250 million for Brent Spence Bridge improvements (Cincinnati, OH, and Covington, KY): This vital freight corridor, spanning the Ohio River, witnesses over USD 400 billion in annual freight movement and is notorious for its truck bottlenecks. The Mega grant will facilitate essential upgrades to the Brent Spence Bridge and the construction of a new bridge alongside the existing one, aimed at alleviating congestion and enhancing travel time reliability, thus bolstering the regional economy.

Overall, infrastructure investment in the United States, especially in the EPC sector, is pivotal in driving economic growth and modernization. The Biden-Harris Administration's commitment is evident in allocating nearly USD 1.2 billion from the National Infrastructure Project Assistance (Mega) discretionary grant program. Noteworthy projects like the Hudson River Tunnel and Brent Spence Bridge highlight the administration's focus on bolstering transportation networks, job creation, and supply chain resilience. With the Mega program eyeing a USD 5 billion investment by 2026, the nation is poised to witness enhanced mobility, safety, and economic robustness, benefiting current and future generations.

The Power and Utilities Sector is Experiencing a Surge in Demand

In 2023, the US power and utilities sector significantly advanced its decarbonization efforts, achieving record solar and energy storage installations. This progress, bolstered by pivotal clean energy and climate legislation, continued into 2024. While the sector's fundamentals were a mixed bag, electricity sales were forecasted to dip by approximately 1.2% YoY by the end of 2023, primarily due to a mild winter. Supply chain challenges began to ease, yet persistent shortages of key materials like steel and transformers disrupted operations and drove up costs.

Many regions saw a drop in wholesale electricity prices, largely attributed to a 53% YoY decrease in natural gas costs for power generation in 2023. However, since not all utilities procure electricity from wholesale markets and fuel expenses are just one component of customer bills, the correlation with price movements may not be direct. In 2023, major electric and gas utilities collectively spent nearly USD 171 billion on grid modernization and decarbonization, setting a new record. Coupled with anticipated future spending and rising interest rates, these high capital outlays could translate to increased customer bills.

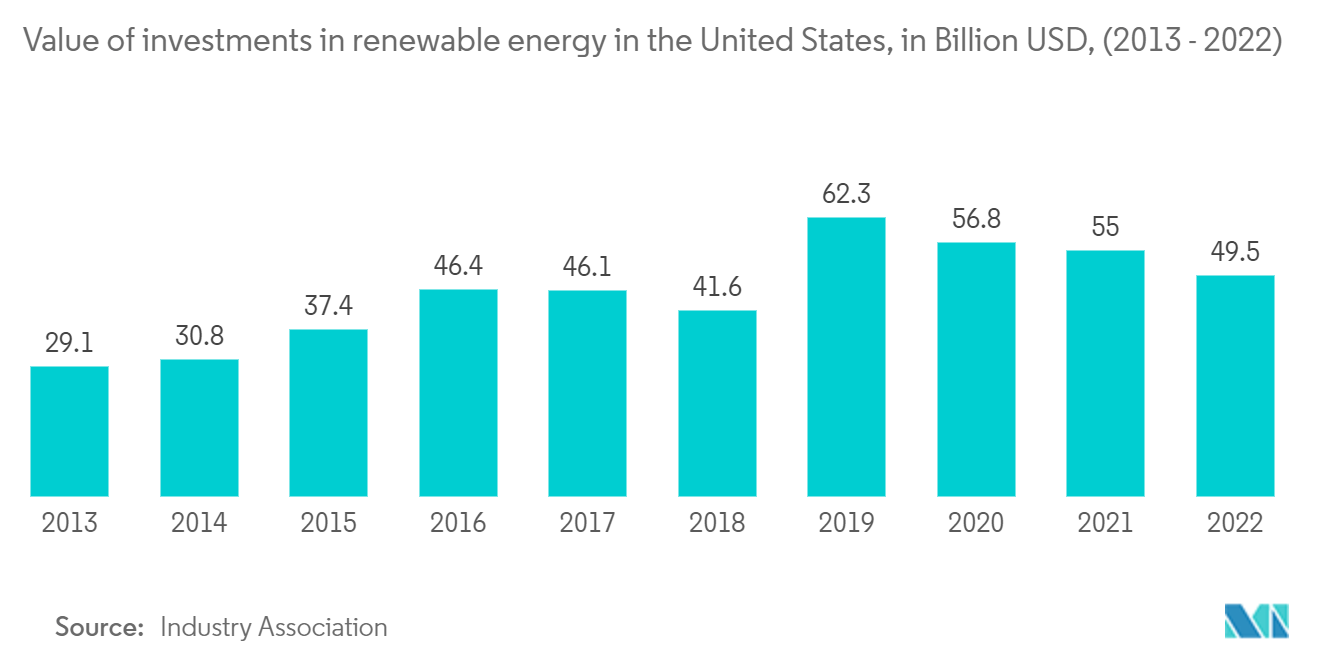

In 2024, electricity prices are anticipated to hold steady, while sales are projected to increase by around 2%. Supply chain disruptions are expected to resolve gradually. The momentum for clean energy initiatives, supported by various catalysts, is likely to persist. A growing number of US electric firms have accelerated their carbon reduction targets, aiming for an 80% cut by 2030, shifting from the previous "net zero by 2050" goal. By August 2023, on the first anniversary of the Inflation Reduction Act (IRA), investors had already earmarked over USD 122 billion for clean energy generation and an additional USD 110 billion for bolstering domestic clean energy manufacturing.

In 2023, the Infrastructure Investment and Jobs Act (IIJA) allocated billions for enhancing grid reliability, battery supply chains, EV programs, and energy efficiency. The US Energy Information Administration (EIA) expected a significant surge in utility-scale solar installations of more than doubling to 24 gigawatts in 2023, followed by an additional 36 GW in 2024. Its projections also indicated a rise in the renewable electricity share from 22% in 2023 to nearly 25% in 2024.

Overall, the US power and utilities sector made significant strides in decarbonization and clean energy adoption, supported by substantial legislative backing and record investments. Despite facing supply chain challenges and a forecasted dip in electricity sales, the sector is poised for steady electricity prices and increased sales in 2024, with continued momentum toward ambitious carbon reduction goals.

US Engineering, Procurement, And Construction Management (EPCM) Market Report Snapshots

- US Engineering, Procurement, And Construction Management (EPCM) Market Size

- US Engineering, Procurement, And Construction Management (EPCM) Market Share

- US Engineering, Procurement, And Construction Management (EPCM) Market Trends

- US Engineering, Procurement, And Construction Management (EPCM) Companies