Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

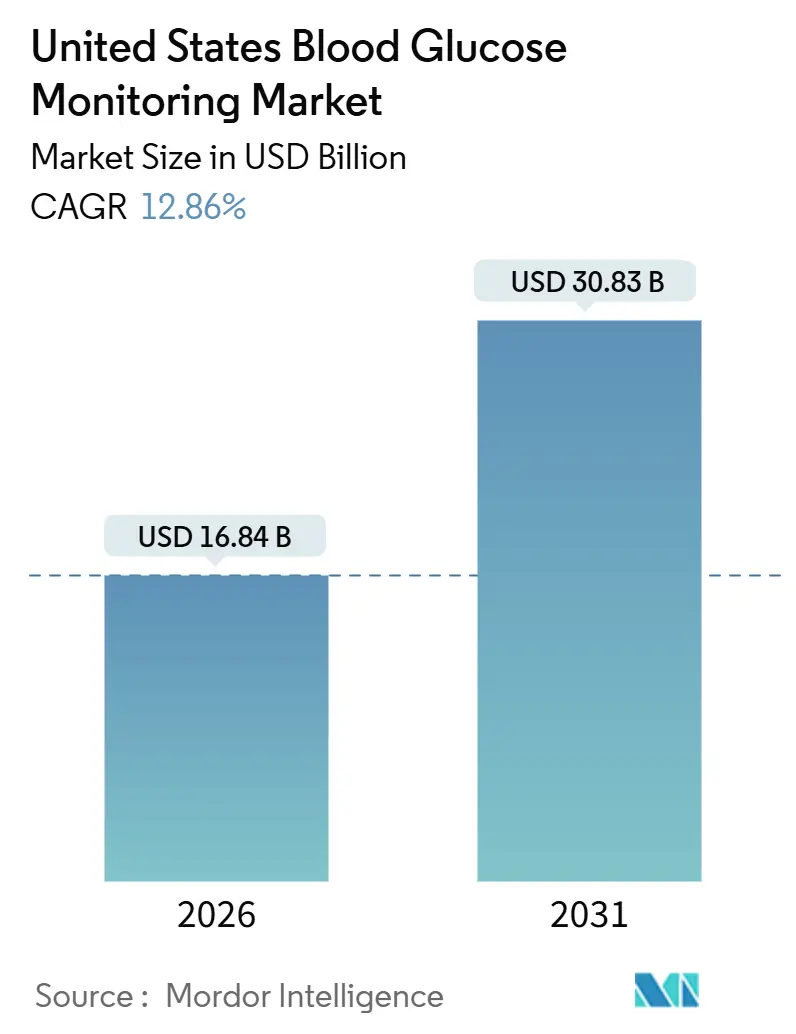

| Market Size (2026) | USD 16.84 Billion |

| Market Size (2031) | USD 30.83 Billion |

| Growth Rate (2026 - 2031) | 12.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Blood Glucose Monitoring Market Analysis by Mordor Intelligence

The United States Blood Glucose Monitoring Market size is estimated at USD 16.84 billion in 2026, and is expected to reach USD 30.83 billion by 2031, at a CAGR of 12.86% during the forecast period (2026-2031).

Robust Medicare reimbursement, over-the-counter continuous glucose monitor (CGM) approvals, and patient-assembled closed-loop ecosystems are accelerating adoption far beyond incremental sensor upgrades. Medicare’s April 2023 expansion alone unlocked coverage for an estimated 3.7 million insulin users and catalyzed a 340% surge in CGM claims within 12 months. Device innovators capitalized by extending sensor wear to 365 days, lowering the per-day cost to USD 1.10, and expanding access for Medicaid and self-pay customers. Semiconductor vertical integration, such as Abbott’s USD 465 million Kilkenny plant, is buffering supply-chain shocks, while interoperable frameworks are fragmenting vendor lock-in and promoting cross-platform pump-sensor pairings. Headwinds persist, including 26-week application-specific integrated circuit lead times and a 22% patient segment wary of cloud-based data sharing; however, tailwinds from employer wellness mandates and state Medicaid parity decisions continue to outweigh these headwinds.

Key Report Takeaways

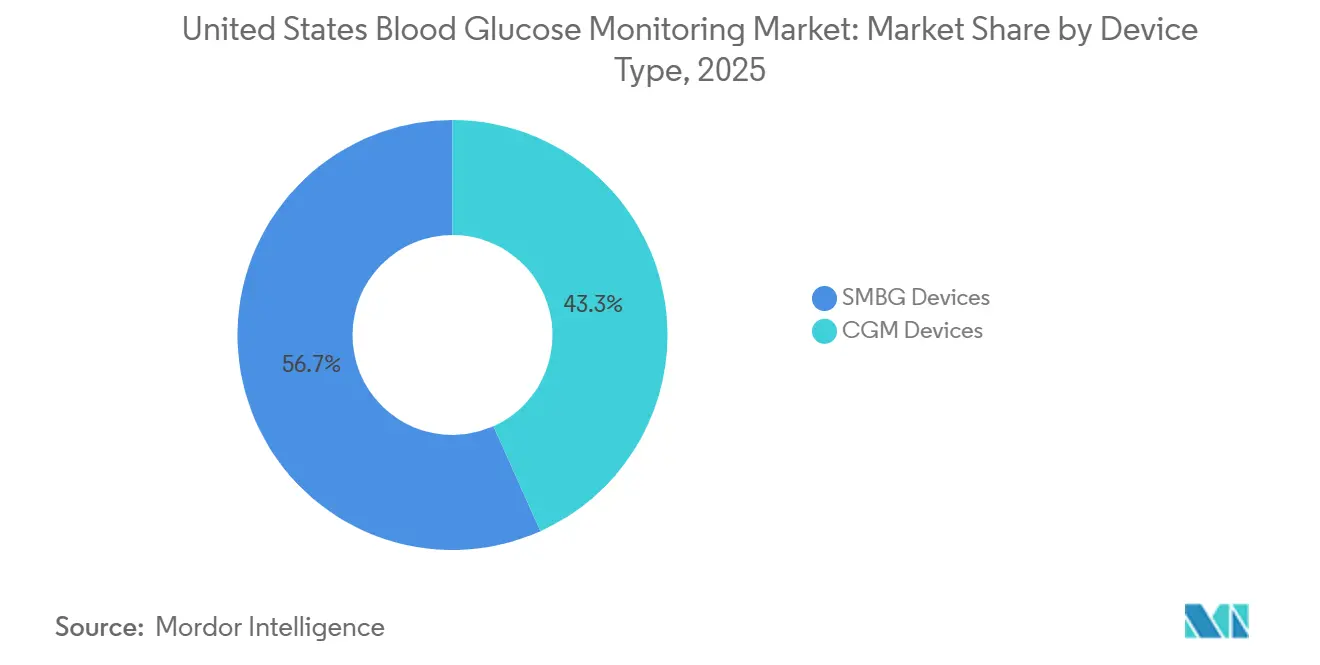

- By device type, self-monitoring blood glucose systems led with 56.71% of United States blood glucose monitoring market share in 2025; CGM devices are forecast to compound at 13.69% through 2031.

- By patient type, Type 2 diabetes contributed 62.27% of the 2025 revenue, while Type 1 diabetes is projected to post the fastest growth, with a 14.46% CAGR, through 2031.

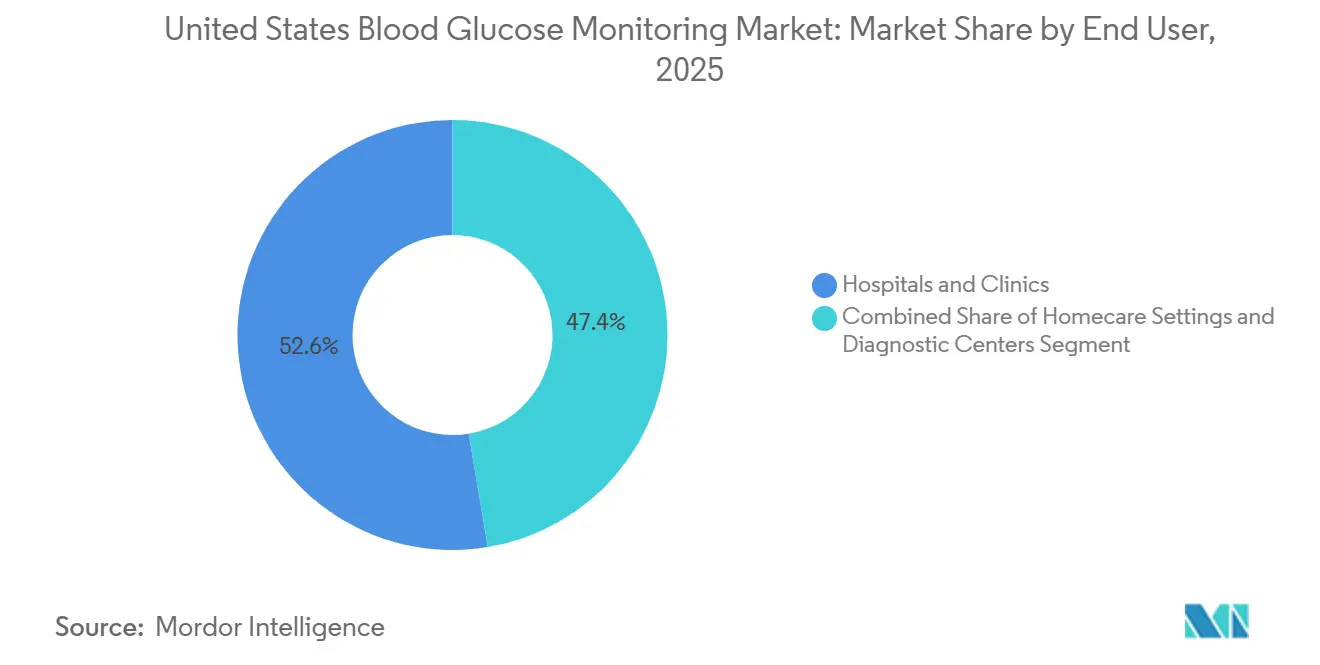

- By end-user, hospitals and clinics accounted for 52.63% of the United States blood glucose monitoring market size in 2025, and diagnostic centers are projected to advance at a 15.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Blood Glucose Monitoring Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes Prevalence | +2.5% | Southern states with obesity rates above 35% | Long term (≥ 4 years) |

| Technological Advances in CGM | +3.1% | Urban academic centers and tech-literate Type 1 communities | Medium term (2-4 years) |

| Medicare Reimbursement Expansion | +2.3% | Florida, Arizona, Pennsylvania with Medicare enrollment exceeding 20% | Short term (≤ 2 years) |

| Employer-Sponsored Wellness Mandates | +1.2% | Fortune 500 self-insured programs focusing on prediabetic workforces | Medium term (2-4 years) |

| Interoperable “DIY Looping” Ecosystems | +1.7% | Type 1 clusters in urban hubs with active patient advocacy | Medium term (2-4 years) |

| Telehealth CPT Codes for Remote Monitoring | +1.4% | Rural counties with limited endocrinology access | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising Diabetes Prevalence

CDC reported that 38.4 million Americans, or 11.6% of the population, lived with diabetes in 2025, while prevalence among adults 65+ climbed to 29.2%.[1]Centers for Disease Control and Prevention, “National Diabetes Statistics Report 2025,” cdc.govThe burden is disproportionately heavy in Alabama, Mississippi, and Louisiana, where obesity exceeds 35% and endocrinology resources are sparse, spurring telehealth-enabled CGM demand. Direct medical costs totaled USD 307 billion in 2024; however, CGM uptake among Type 2 basal insulin users remained below 8%, highlighting untapped expansion opportunities. Prediabetes affects 97.6 million adults, and 70% risk of progressing to Type 2 within a decade, feeding a pipeline that sustains device volumes. Employer plans now reimburse CGM for prediabetic staff to avert downstream expenses, broadening the user base. Consequently, continuous monitoring is shifting from episodic testing toward universal surveillance across risk cohorts.

Technological Advances in CGM

Four sensor platforms received FDA clearance between March and September 2024, including Dexcom’s OTC Stelo, Abbott’s Lingo, Medtronic’s Simplera, and Senseonics’ 365-day Eversense. One-year implantability reduces adhesive dermatitis, which previously caused 18% of discontinuations within six months. Abbott’s partnership with Medtronic to embed Libre sensors into MiniMed pumps underscores the strategic importance of interoperability, enabling patients to assemble personalized hybrid solutions. Dexcom priced Stelo at USD 99 for a two-sensor month, demonstrating that retail shelves can reach the 30 million prediabetic Americans lacking prescription coverage. As wear duration stretches from 14 days to 365 days, per-day costs decrease toward USD 1, unlocking Medicaid and cash-pay segments that have been long tethered to USD 0.15 test strips.

Medicare Reimbursement Expansion

CMS lifted the intensive-insulin restriction in April 2023, extending CGM reimbursement to basal-insulin users and severe hypoglycemia cases, instantly adding 3.7 million beneficiaries.[2]Centers for Medicare & Medicaid Services, “National Coverage Determination for Continuous Glucose Monitors,” cms.gov A Health Affairs review revealed that Florida, Arizona, and Pennsylvania accounted for 38% of incremental CGM claims, likely due to the presence of dense retiree populations. The standard USD 150 monthly payment created a USD 6.7 billion addressable pool, sparking vendor DTC campaigns. Fourteen Medicaid programs had mirrored the policy by 2025, although prior-authorization delays averaged 28 days. Hospital discharges now routinely include CGM prescriptions; a 2024 JAMA study linked this practice to a 41% drop in 30-day hypoglycemia ER visits. Early sales data suggest Medicare members represent the fastest-growing CGM cohort through 2026.

Interoperable “DIY Looping” Ecosystems

The FDA’s iCGM, ACE pump, and AID controller classes enable patients to pair devices from different brands, potentially leading to an estimated 15,000 U.S. DIY loopers by 2025. Tandem’s January 2024 cross-vendor integration of Abbott’s Libre 2 Plus with the t:slim X2 pump commercialized this modular vision. A Diabetes Care cohort study documented a jump in time-in-range from 68% to 76% and a 54% decrease in severe hypoglycemia among loopers, rivaling the annual savings of USD 10,000 compared to commercial systems.[3]American Diabetes Association, “Standards of Care in Diabetes 2024,” diabetesjournals.org Community developers iterate algorithms within weeks, forcing incumbents to accelerate product cycles or cede tech-savvy Type 1 users. The framework decouples sensor, pump, and algorithm approvals, unlocking innovation but intensifying competitive churn.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of CGM Devices | -1.6% | Rural counties and 27 million uninsured or 44 million underinsured Americans | Short term (≤ 2 years) |

| Economic Reuse of Test Strips | -1.1% | Low-income households and Medicaid populations | Long term (≥ 4 years) |

| Data-Privacy Hesitancy with Cloud Platforms | -0.9% | Elderly Medicare cohorts and privacy-conscious users | Medium term (2-4 years) |

| Semiconductor Sensor Supply Risk | -1.0% | Supply chain concentrated in Taiwan, Malaysia and Ireland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of CGM Devices

Out-of-pocket CGM costs range from USD 1,200 to USD 2,400 annually, compared to USD 180 to USD 360 for SMBG, a six-fold premium that dissuades uninsured and high-deductible plan members. Survey work revealed that 34% of Type 2 users abandoned CGM within 90 days due to cost concerns, reverting to bulk-purchased strips at USD 0.15 each. Rebates negotiated by pharmacy benefit managers seldom reach the checkout counter, preserving the sticker shock of USD 300-400 per month. Dexcom’s USD 99 Stelo cuts the list price but shifts the full cost to consumers, limiting its reach. Rural counties with fewer than 50,000 residents post CGM adoption rates 62% below urban peers, magnifying health inequity.

Semiconductor Sensor Supply Risk

CGM ASICs are mostly fabricated in Taiwan, and 2024 lead times doubled to 26 weeks as foundries prioritized automotive chips. Medtronic’s Simplera clearance was delayed five months, missing the Medicare open-enrollment window. Deloitte modeled a four-week wafer outage translating into 18-22% sensor shortfalls, compelling rationing toward federally covered patients. Abbott’s Kilkenny facility mitigates risk yet will not operate at scale until late 2027. Roche's USD 550 million Indianapolis expansion follows the same onshoring logic.

Segment Analysis

By Device Type: CGM Sensors Displace Legacy Glucometers

Self-monitoring systems captured 56.71% of the United States blood glucose monitoring market share in 2025, driven by three-year hospital contracts that bundled meters and strips at USD 0.80-1.20 per test. Test strips dominate revenue because basal insulin users typically burn through 730-1,095 strips annually, and proprietary chemistries help keep customers loyal. Lancet's face commoditization, with generic units at USD 0.02 eroding branded margins. Conversely, CGM sensors are slated to post a 13.69% CAGR through 2031, fueled by 365-day implantables and OTC channels. Sensors account for about 72% of CGM revenue due to their steady replacement cadence, while transmitters are subsidized to secure subscription economics.

Glucometers persist in critical-care wards because the CGM mean absolute relative difference of 9-12% is outside the ±5% insulin-dosing tolerance FDA set in 2024. The reuse of strips and lancets still undercuts sensor economics in low-income homes, despite infection control warnings. The transition from 14-day to 365-day sensors reduces the daily cost and mitigates adhesive-related dropout, which is observed in 18% of patients within six months. Dexcom’s Stelo exploits prediabetes retail channels, while safety-engineered hospital lancets maintain a 40% premium due to OSHA mandates.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Patient Type: Type 1 Momentum Outpaces Type 2 Volume

Type 2 diabetes generated 62.27% revenue in 2025, but adoption of CGM among basal-insulin users remained below 12% before Medicare’s rule change. The American Diabetes Association now recommends CGM for every insulin regimen, yet primary-care inertia and cost hurdles slow translation into prescriptions. Type 1 patients total only 1.9 million but are adopting closed-loop technology at a rapid clip, driving a 14.46% forecast CAGR. DIY looping boosted time-in-range to 76% and cut severe hypoglycemia 54%, prompting insurers to reclassify CGM as standard-of-care.

Gestational diabetes represents the smallest slice, yet ACOG’s 2024 guidelines encourage CGM for insulin-treated pregnancies to reduce macrosomia, opening a nascent niche. Type 1 adoption exceeds 60% in urban centers where patient advocacy networks are robust. Type 2 uptake will accelerate as cost declines converge with employer wellness incentives, but SMBG will remain entrenched in diet- or oral-drug-managed populations. Gestational monitoring remains episodic, but it could shift to continuous monitoring if longitudinal outcome trials demonstrate lower neonatal ICU stays.

By End User: Diagnostic Centers Accelerate in Outpatient Pathways

Hospitals and clinics held 52.63% of United States blood glucose monitoring market size in 2025, benefiting from Joint Commission mandates for point-of-care testing and capitated readmission avoidance. FDA guidance now allows CGM in non-ICU beds, enabling remote nurse monitoring and trimming labor by USD 18 per patient-day. Diagnostic centers are expected to record a 15.13% CAGR as A1C testing bundles with same-day CGM initiation are favored by Medicare Advantage plans. Home care is the second-largest channel, leveraging telehealth CPT codes that reimburse clinicians USD 150-250 monthly for remote data reviews.

Electronic-health-record integration is a bottleneck; only 40% of hospitals had seamless CGM feeds in 2025. Quest and LabCorp's “test-to-treat” pilots reduce therapy initiation to seven days, demonstrating diagnostic-center agility. Rural broadband gaps still hamper home-upload models for 15% of households. Hospitals are piloting CGM-driven hypoglycemia early-warning systems that reduced code-blue events by 31% at Johns Hopkins in 2024. Diagnostic centers are therefore poised to capture a growing slice of the United States blood glucose monitoring market share as payers steer volume to controlled outpatient environments.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Florida, Arizona, and Pennsylvania collectively significant share of incremental CGM claims in the first year following Medicare’s coverage expansion, reflecting Medicare enrollment ratios above 20%. Southern states have prevalence rates exceeding 14% but lag in adoption, as Alabama and Mississippi each have fewer than three endocrinologists per 100,000 residents, compared to eight in Massachusetts. Medicaid prior authorization in Texas, Georgia, and North Carolina extends CGM approval by an average of 28 days, constraining penetration despite a high disease burden.

California, New York, and Texas account for 32% of national diabetes cases; all expanded Medicaid CGM coverage in 2024-25, but denial rates remain elevated, at 41% for initial Texas submissions. Integrated Midwest health systems such as Kaiser Permanente harmonize protocols across inpatient and outpatient sites, balancing SMBG and CGM utilization. Rural counties with limited broadband access experience a 62% lower CGM uptake and rely heavily on Bluetooth-only sensors, which lack real-time cloud uploads but satisfy patient privacy concerns.

Urban academic centers in Boston, San Francisco, and New York boast a CGM use rate of over 70% among Type 1 patients, driven by an early-adopter culture and alignment with insurers. Abbott, Dexcom, and Medtronic focus DTC campaigns in these Medicare-dense metros, leaving Medicaid-heavy rural zones understimulated. Without targeted investments in broadband and physician education, geographic inequity in the United States' blood glucose monitoring market is expected to widen through 2031.

Competitive Landscape

Abbott, Dexcom, and Roche collectively held a significant revenue share in 2025, positioning the United States blood glucose monitoring market as moderately concentrated. Abbott’s Kilkenny plant scales to 10 million Libre sensors annually, hedging ASIC dependence and supporting U.S. demand spikes. Dexcom’s G7 narrowed the mean absolute relative difference to 8.2%, enhancing competitive differentiation, while its OTC Stelo tapped a prediabetes audience that had been historically outside the reach of prescription products. Roche’s USD 550 million Indianapolis expansion underscores a capacity-first defense as Medicare’s flat USD 150 monthly reimbursement caps price competition.

Medtronic plans to spin off its USD 2.5 billion diabetes unit by April 2026, freeing capital for acquisitions and algorithm innovation. Senseonics’ Eversense 365 removes adhesive dermatitis pain points, and Ascensia is targeting elderly users with fragile skin. LifeScan’s October 2025 Chapter 11 restructuring wiped out 75% of its debt, yet it underscores the margin squeeze on strip-centric models. Patent filings reveal 127 active CGM sensor claims by Abbott, 94 by Dexcom, and 61 by Medtronic, with future differentiation likely shifting toward data analytics rather than hardware.

Litigation over electrochemical glucose-oxidase chemistry may intensify, but the FDA interoperability framework dilutes proprietary ecosystems, leveling the playing field toward algorithm-rich platforms. White-space persists in gestational diabetes and employer wellness, where adoption remains <12%. Vendors able to integrate sensor data into payer-approved chronic-care platforms stand to gain incremental United States blood glucose monitoring market share through 2031.

United States Blood Glucose Monitoring Industry Leaders

Abbott Diabetes Care

Dexcom Inc.

Lifescan

Roche Holding AG

Ascensia Diabetes Care

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: LifeScan received U.S. Bankruptcy Court approval for its Chapter 11 reorganization, eliminating more than 75% of debt and securing USD 200 million in exit financing

- November 2024: Abbott opened a USD 465 million FreeStyle Libre sensor plant in Kilkenny, Ireland, with 10 million-unit annual capacity.

- September 2024: FDA cleared Senseonics’ Eversense 365, the first 365-day implantable CGM, commercialized by Ascensia Diabetes Care.

- August 2024: Abbott and Medtronic partnered to integrate Libre sensors with MiniMed automated insulin delivery systems.

United States Blood Glucose Monitoring Market Report Scope

Blood glucose monitoring tests the concentration of glucose in the blood (glycemia). Particularly important in diabetes management, a blood glucose test is typically performed to determine the fluctuation in blood glucose level and to take or alter the medication accordingly, especially for insulin users. Achieving optimum glycemic results can be very difficult without frequent monitoring of blood glucose levels. The United States blood glucose monitoring market is segmented by type (self-monitoring blood glucose devices and continuous blood glucose monitoring devices) and components (glucometer devices, test strips, lancets, sensors, and durables). The report offers the value (in USD million) and volume (in unit million) for the above segments.

By Device Type

| SMBG Devices | Glucometers |

| Test Strips | |

| Lancets | |

| CGM Devices | Sensors |

| Durables |

By Patient Type

| Type 1 Diabetes |

| Type 2 Diabetes |

| Gestational Diabetes |

By End-user

| Hospitals & Clinics |

| Homecare Settings |

| Diagnostic Centers |

| By Device Type | SMBG Devices | Glucometers |

| Test Strips | ||

| Lancets | ||

| CGM Devices | Sensors | |

| Durables | ||

| By Patient Type | Type 1 Diabetes | |

| Type 2 Diabetes | ||

| Gestational Diabetes | ||

| By End-user | Hospitals & Clinics | |

| Homecare Settings | ||

| Diagnostic Centers | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the United States blood glucose monitoring market?

The market was valued at USD 16.84 billion in 2026 and is on track to reach USD 30.83 billion by 2031.

Which device segment is growing fastest?

Continuous glucose monitor devices are expected to post a 13.69% CAGR through 2031, outpacing legacy glucometers.

How does Medicare coverage affect CGM adoption?

Medicare’s 2023 expansion added 3.7 million eligible insulin users, driving a 340% jump in claims within a year.

Which patient group shows the highest CGM adoption rate?

Type 1 diabetes patients in urban academic centers have adoption levels exceeding 60% due to closed-loop therapy demand.

What supply-chain risk threatens sensor availability?

Extended 26-week lead times for semiconductor ASICs could trim sensor output by up to 22% during a four-week wafer interruption.