Market Size of United States Aerospace And Defense Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

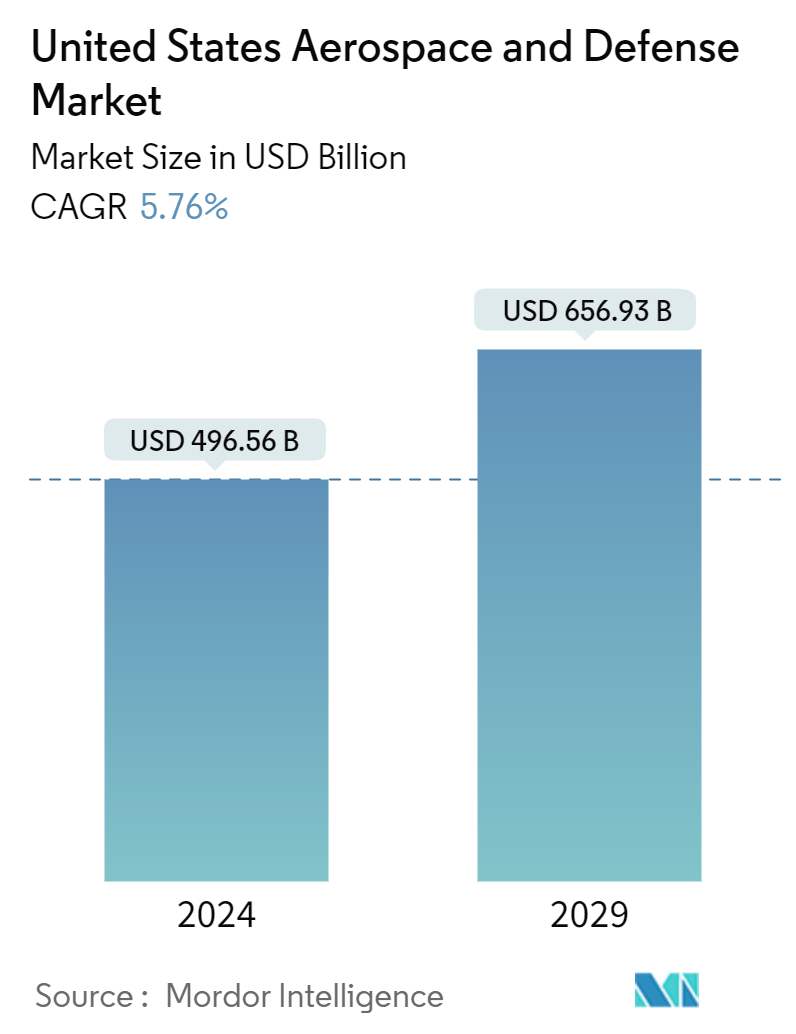

| Market Size (2024) | USD 496.56 Billion |

| Market Size (2029) | USD 656.93 Billion |

| CAGR (2024 - 2029) | 5.76 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

United States Aerospace And Defense Market Analysis

The United States Aerospace And Defense Market size is estimated at USD 496.56 billion in 2024, and is expected to reach USD 656.93 billion by 2029, growing at a CAGR of 5.76% during the forecast period (2024-2029).

The US aerospace and defense sector is one of the largest in terms of infrastructure and manufacturing activities. The market is expected to grow primarily due to the armed forces' procurement and upgrade activities to counter emerging threats. Several contracts from the military, air force, and naval force are currently underway, and many new contracts are anticipated to be dispersed during the forecast period, creating a parallel demand for defense equipment.

The US military uses multiple aircraft across the air force and naval aircraft. Owing to the increasing international conflict with China over its aggression in the South China Sea, the US is gearing up to tackle any potential issues China might create for countries with close ties with the US, like Taiwan and Japan. As a result, significant investments in upgrading the existing fleet and purchasing a new fleet equipped with efficient technologies have been witnessed over the past year.

The growing adoption of advanced technologies such as 3D printing, artificial intelligence, and big data analytics in developing aviation and defense equipment will create better opportunities in the coming years. However, issues related to the supply chain and evolving cybersecurity risks may hinder market growth.

United States Aerospace And Defense Industry Segmentation

Aerospace is the design and manufacture of aircraft, rockets, missiles, and spacecraft that operate in space. Defense equipment refers to weapons, arms, and equipment used for military purposes. The report provides an in-depth analysis of the aerospace and defense market in the US.

The US aerospace and defense market is segmented by sector and platform. By sector, the market is segmented into aviation, defense, space, and unmanned systems. The aviation segment is further segmented into commercial and general aviation, while the defense segment is further classified as army, navy, and air force. By platform, the market is segmented into land, air, sea, and space. For each segment, the market size is provided in terms of value (USD).

| Commercial and General Aviation | |||||||||||||||||||||||||||

| Market Overview | |||||||||||||||||||||||||||

| |||||||||||||||||||||||||||

| Market Trends | |||||||||||||||||||||||||||

| |||||||||||||||||||||||||||

|

| Military Aircraft and Systems | |||||||||||||||

| Market Overview | |||||||||||||||

| |||||||||||||||

| |||||||||||||||

| Market Trends | |||||||||||||||

| MRO | |||||||||||||||

| Research and Development | |||||||||||||||

| Training and Flight Simulators | |||||||||||||||

| Competitor Analysis | |||||||||||||||

| Supply Chain Analysis | |||||||||||||||

| Customer/Distributor Information | |||||||||||||||

| |||||||||||||||

|

| Unmanned Aerial Systems | |||||

| Market Overview | |||||

| |||||

| Market Trends | |||||

| Research and Development | |||||

| Competitor Analysis | |||||

| Regulatory Landscape and Future Policy Changes | |||||

|

| Space Systems and Equipment | |||||||||||||

| Market Overview | |||||||||||||

| |||||||||||||

| Market Trends | |||||||||||||

| Research and Development | |||||||||||||

| Competitor Analysis | |||||||||||||

| Regulatory Landscape and Future Policy Changes | |||||||||||||

| Customer Information | |||||||||||||

| Segmentation: Space Launch Vehicle, Spacecraft, and Ground Systems (Market Size and Forecast) | |||||||||||||

|

United States Aerospace And Defense Market Size Summary

The US aerospace and defense market is a significant sector characterized by extensive infrastructure and manufacturing activities. It is poised for growth driven by the need for armed forces procurement and upgrades to address emerging global threats. The market is experiencing a surge in contracts across military, air force, and naval forces, with a parallel demand for advanced defense equipment. The increasing international tensions, particularly with China, have prompted substantial investments in upgrading and expanding the US military fleet. The adoption of cutting-edge technologies such as 3D printing, artificial intelligence, and big data analytics is expected to create new opportunities in the development of aviation and defense equipment. However, challenges such as supply chain issues and evolving cybersecurity risks may pose obstacles to market expansion.

The US aerospace and defense industry is also witnessing significant developments in space capabilities, which are crucial for national security and military operations. The satellite manufacturing and launch sector is rapidly evolving, driven by technological advancements and the growing demand for satellite services. The establishment of the Space Force as a military branch and the increasing number of satellite launches are expected to further propel market growth. The US Air Force is at the forefront of technological advancements, with ongoing procurement of next-generation aircraft to maintain a strategic edge. The market is consolidated, with major players like General Dynamics Corporation, Lockheed Martin Corporation, and The Boeing Company leading the charge. These companies are heavily investing in research and development to enhance their product offerings and align with the evolving demands of the defense sector.

United States Aerospace And Defense Market Size - Table of Contents

-

1. MARKET SEGMENTATION

-

1.1 Commercial and General Aviation

-

1.1.1 Market Overview

-

1.1.2 Market Dynamics

-

1.1.2.1 Drivers

-

1.1.2.2 Restraints

-

1.1.2.3 Opportunities

-

-

1.1.3 Market Trends

-

1.1.4 Segmentation: Commercial Aircraft

-

1.1.4.1 Air Traffic

-

1.1.4.2 Training and Flight Simulators

-

1.1.4.3 Airport Services (Ground Support Equipment and Logistics)

-

1.1.4.4 Structures

-

1.1.4.4.1 Airframe

-

1.1.4.4.1.1 Materials (Composite, Metal and Metal Alloys, Others)

-

1.1.4.4.1.2 Adhesives and Coatings

-

-

1.1.4.4.2 Engine and Engine Systems

-

1.1.4.4.3 Cabin Interiors

-

1.1.4.4.4 Landing Gear

-

1.1.4.4.5 Avionics and Control Systems

-

1.1.4.4.5.1 Communication System

-

1.1.4.4.5.2 Navigation System

-

1.1.4.4.5.3 Flight Control System

-

1.1.4.4.5.4 Health Monitoring System

-

-

1.1.4.4.6 Electrical Systems

-

1.1.4.4.7 Environmental Control Systems

-

1.1.4.4.8 Fuel and Fuel Systems

-

1.1.4.4.9 MRO

-

1.1.4.4.10 Research and Development

-

1.1.4.4.11 Supply Chain Analysis (Design, Raw Materials, Manufacturing, Assembly, Testing, and Certification)

-

1.1.4.4.12 Competitor Analysis

-

-

-

1.1.5 Segmentation: General Aviation (includes Business Jets, Helicopter, and Personal Aircraft)

-

1.1.5.1 Air Traffic

-

1.1.5.2 Training and Flight Simulators

-

1.1.5.3 Airport Services (Ground Support Equipment and Logistics)

-

1.1.5.4 Structures

-

1.1.5.4.1 Airframe

-

1.1.5.4.1.1 Materials (Composite, Metal and Metal Alloys, Others)

-

1.1.5.4.1.2 Adhesives and Coatings

-

-

1.1.5.4.2 Engine and Engine Systems

-

1.1.5.4.3 Cabin Interiors

-

1.1.5.4.4 Landing Gear

-

1.1.5.4.5 Avionics and Control Systems

-

1.1.5.4.5.1 Communication System

-

1.1.5.4.5.2 Navigation System

-

1.1.5.4.5.3 Flight Control System

-

1.1.5.4.5.4 Health Monitoring System

-

-

1.1.5.4.6 Electrical Systems

-

1.1.5.4.7 Environmental Control Systems

-

1.1.5.4.8 Fuel and Fuel Systems

-

1.1.5.4.9 MRO

-

1.1.5.4.10 Research and Development

-

1.1.5.4.11 Supply Chain Analysis

-

1.1.5.4.12 Competitor Analysis

-

-

-

-

1.2 Military Aircraft and Systems

-

1.2.1 Market Overview

-

1.2.2 Defense Spending and Budget Allocation Details

-

1.2.2.1 Army

-

1.2.2.2 Navy and Marine Corps

-

1.2.2.3 Air Force

-

-

1.2.3 Market Dynamics

-

1.2.3.1 Drivers

-

1.2.3.2 Restraints

-

1.2.3.3 Opportunities

-

-

1.2.4 Market Trends

-

1.2.5 MRO

-

1.2.6 Research and Development

-

1.2.7 Training and Flight Simulators

-

1.2.8 Competitor Analysis

-

1.2.9 Supply Chain Analysis

-

1.2.10 Customer/Distributor Information

-

1.2.11 Segmentation: Combat Aircraft

-

1.2.11.1 Structures

-

1.2.11.1.1 Airframe

-

1.2.11.1.1.1 Materials (Composite, Metal and Metal Alloys, Others)

-

1.2.11.1.1.2 Adhesives and Coatings

-

-

1.2.11.1.2 Engine and Engine Systems

-

1.2.11.1.3 Landing Gear

-

-

1.2.11.2 Avionics and Control Systems

-

1.2.11.2.1 General Avionics

-

1.2.11.2.2 Mission Specific Avionics

-

-

1.2.11.3 Missiles and Weapons

-

-

1.2.12 Segmentation: Non-Combat Aircraft

-

1.2.12.1 Structures

-

1.2.12.1.1 Airframe

-

1.2.12.1.1.1 Materials (Composite, Metal and Metal Alloys, Others)

-

1.2.12.1.1.2 Adhesives and Coatings

-

-

1.2.12.1.2 Engine and Engine Systems

-

1.2.12.1.3 Landing Gear

-

-

1.2.12.2 Avionics and Control Systems

-

1.2.12.2.1 General Avionics

-

1.2.12.2.2 Mission Specific Avionics

-

-

1.2.12.3 Missiles and Weapons

-

-

-

1.3 Unmanned Aerial Systems

-

1.3.1 Market Overview

-

1.3.2 Market Dynamics

-

1.3.2.1 Drivers

-

1.3.2.2 Restraints

-

1.3.2.3 Opportunities

-

-

1.3.3 Market Trends

-

1.3.4 Research and Development

-

1.3.5 Competitor Analysis

-

1.3.6 Regulatory Landscape and Future Policy Changes

-

1.3.7 Segmentation

-

1.3.7.1 Commercial

-

1.3.7.2 Military

-

-

-

1.4 Space Systems and Equipment

-

1.4.1 Market Overview

-

1.4.2 Market Dynamics

-

1.4.2.1 Drivers

-

1.4.2.2 Restraints

-

1.4.2.3 Opportunities

-

-

1.4.3 Market Trends

-

1.4.4 Research and Development

-

1.4.5 Competitor Analysis

-

1.4.6 Regulatory Landscape and Future Policy Changes

-

1.4.7 Customer Information

-

1.4.8 Segmentation: Space Launch Vehicle, Spacecraft, and Ground Systems (Market Size and Forecast)

-

1.4.9 Segmentation: Satellites

-

1.4.9.1 By Subsystem

-

1.4.9.1.1 Command and Control System

-

1.4.9.1.2 Telemetry, Tracking, Commanding and Monitoring (TTCM)

-

1.4.9.1.3 Antenna System

-

1.4.9.1.4 Transponders

-

1.4.9.1.5 Power System

-

-

1.4.9.2 By Application

-

1.4.9.2.1 Military

-

1.4.9.2.2 Commercial

-

-

-

-

United States Aerospace And Defense Market Size FAQs

How big is the United States Aerospace And Defense Market?

The United States Aerospace And Defense Market size is expected to reach USD 496.56 billion in 2024 and grow at a CAGR of 5.76% to reach USD 656.93 billion by 2029.

What is the current United States Aerospace And Defense Market size?

In 2024, the United States Aerospace And Defense Market size is expected to reach USD 496.56 billion.