Market Size of Urea Formaldehyde Resins Industry

| Study Period | 2024 - 2029 |

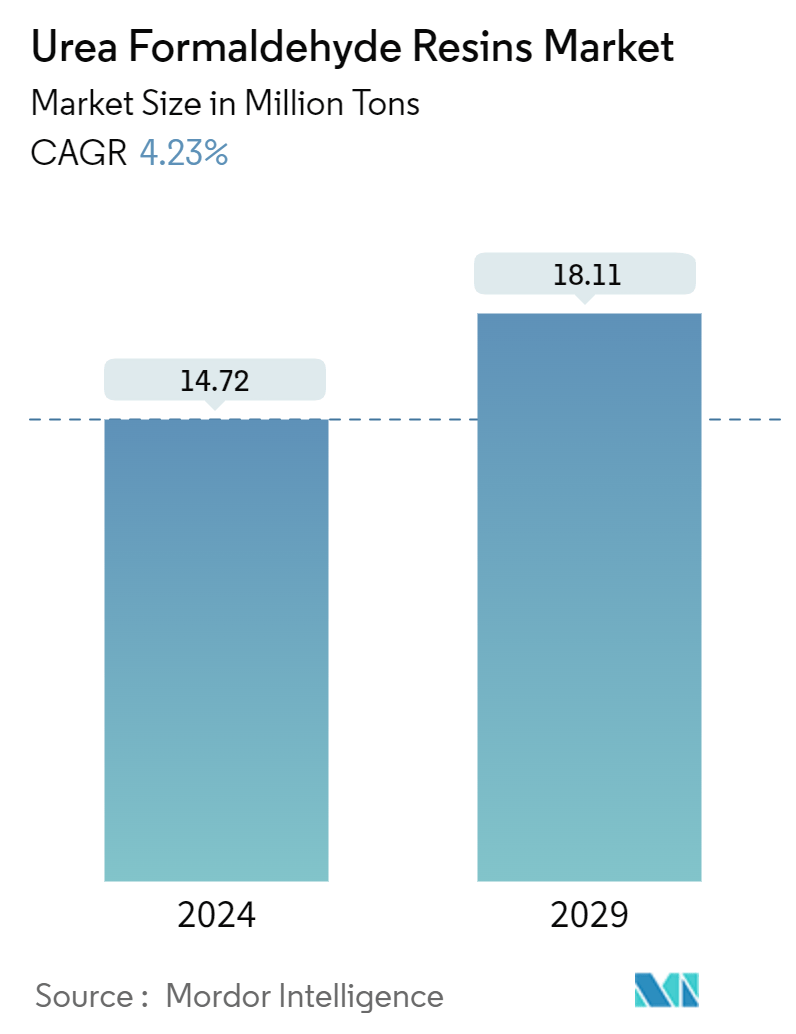

| Market Volume (2024) | 14.72 Million tons |

| Market Volume (2029) | 18.11 Million tons |

| CAGR (2024 - 2029) | 4.23 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Urea Formaldehyde Resins Market Analysis

The Urea Formaldehyde Resins Market size is estimated at 14.72 Million tons in 2024, and is expected to reach 18.11 Million tons by 2029, growing at a CAGR of 4.23% during the forecast period (2024-2029).

The COVID-19 epidemic negatively impacted the urea formaldehyde market. Global lockdowns and severe government rules resulted in a catastrophic setback, as most production hubs were shut down. Nonetheless, the market recovered in 2021 and is expected to rise significantly in the coming years.

- Over the short term, the growing demand for particle boards from the furniture sector and the increasing demand for medium-density fiberboard (MDF) are expected to drive the market's growth.

- However, health hazards regarding urea-formaldehyde resins are expected to hinder the market's growth.

- Nevertheless, the demand for good-quality resins in automobiles and electrical appliances is expected to create new opportunities for the market studied.

- Asia-Pacific dominates the market globally, with the most consumption from China and India.

Urea Formaldehyde Resins Industry Segmentation

Urea formaldehyde resins, a subset of amino resins, are crafted through the polymeric condensation of formaldehyde and urea. These resins primarily serve as binders in manufacturing various wood products, including adhered wood products, particleboard, plywood, and medium-density fiberboard. They impart several desirable traits to these products, such as a high heat distortion temperature, strong tensile strength, low water absorption, and elevated surface hardness.

The urea formaldehyde resin market is segmented by application, end-user industry, and geography. The market is segmented by application into particle board, wood adhesives, plywood, medium-density fiberboard, and other applications (plastics, adhesives, etc.). In the end-user industry, the market is segmented into automotive, electrical appliances, agriculture, building and construction, and other end-user industries (pulp and paper, etc.). The report also covers the market size and forecasts for urea-formaldehyde in 27 countries across major regions. Market sizing and forecasts are made for each segment based on volume (kilotons).

| By Application | |

| Particle Board | |

| Wood Adhesives | |

| Plywood | |

| Medium Density Fiberboard | |

| Other Applications |

| By End-user Industry | |

| Automotive | |

| Electrical Appliances | |

| Agriculture | |

| Building and Construction | |

| Other End-user Industries |

| By Geography | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

Urea Formaldehyde Resins Market Size Summary

The global urea formaldehyde resins market is poised for growth, driven by increasing demand from the construction, automotive, and agriculture sectors. The market, which experienced setbacks due to the COVID-19 pandemic, is expected to recover as these industries expand. The construction sector, in particular, is a significant contributor to market growth, with rising demand for particle boards and medium-density fiberboard (MDF) fueling the need for urea formaldehyde resins. Despite health concerns and pandemic-related challenges, the market is set to benefit from the robust performance of the building and construction industry, which extensively utilizes these resins in various applications.

Asia-Pacific leads the global market, with China and India being the largest consumers. China's substantial construction activities, driven by its large population and urbanization, significantly impact the market. The country's position as a major producer and consumer of urea formaldehyde resins is bolstered by its thriving furniture and automotive industries. The region's dominance is further supported by strong residential construction growth in both Asia-Pacific and North America, where factors such as population growth and housing demand are driving market expansion. The fragmented nature of the market sees key players like BASF SE, Hexion, and Georgia-Pacific Chemicals actively participating in shaping its future.

Urea Formaldehyde Resins Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Drivers

-

1.1.1 Increasing Demand for Medium Density Fiberboard (MDF)

-

1.1.2 Rising Demand for Particle Board in the Furniture Sector

-

1.1.3 Other Drivers

-

-

1.2 Restraints

-

1.2.1 Health Hazards Regarding Urea Formaldehyde Resins

-

1.2.2 Other Restraints

-

-

1.3 Industry Value-chain Analysis

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining Power of Buyers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products and Services

-

1.4.5 Degree of Competition

-

-

-

2. MARKET SEGMENTATION (Market Size in Volume)

-

2.1 By Application

-

2.1.1 Particle Board

-

2.1.2 Wood Adhesives

-

2.1.3 Plywood

-

2.1.4 Medium Density Fiberboard

-

2.1.5 Other Applications

-

-

2.2 By End-user Industry

-

2.2.1 Automotive

-

2.2.2 Electrical Appliances

-

2.2.3 Agriculture

-

2.2.4 Building and Construction

-

2.2.5 Other End-user Industries

-

-

2.3 By Geography

-

2.3.1 Asia-Pacific

-

2.3.1.1 China

-

2.3.1.2 India

-

2.3.1.3 Japan

-

2.3.1.4 South Korea

-

2.3.1.5 Malaysia

-

2.3.1.6 Thailand

-

2.3.1.7 Indonesia

-

2.3.1.8 Vietnam

-

2.3.1.9 Rest of Asia-Pacific

-

-

2.3.2 North America

-

2.3.2.1 United States

-

2.3.2.2 Canada

-

2.3.2.3 Mexico

-

-

2.3.3 Europe

-

2.3.3.1 Germany

-

2.3.3.2 United Kingdom

-

2.3.3.3 France

-

2.3.3.4 Italy

-

2.3.3.5 Spain

-

2.3.3.6 NORDIC Countries

-

2.3.3.7 Turkey

-

2.3.3.8 Russia

-

2.3.3.9 Rest of Europe

-

-

2.3.4 South America

-

2.3.4.1 Brazil

-

2.3.4.2 Argentina

-

2.3.4.3 Colombia

-

2.3.4.4 Rest of South America

-

-

2.3.5 Middle East and Africa

-

2.3.5.1 Saudi Arabia

-

2.3.5.2 Qatar

-

2.3.5.3 United Arab Emirates

-

2.3.5.4 Nigeria

-

2.3.5.5 Egypt

-

2.3.5.6 South Africa

-

2.3.5.7 Rest of Middle East and Africa

-

-

-

Urea Formaldehyde Resins Market Size FAQs

How big is the Urea Formaldehyde Resins Market?

The Urea Formaldehyde Resins Market size is expected to reach 14.72 million tons in 2024 and grow at a CAGR of 4.23% to reach 18.11 million tons by 2029.

What is the current Urea Formaldehyde Resins Market size?

In 2024, the Urea Formaldehyde Resins Market size is expected to reach 14.72 million tons.