Urea Formaldehyde Market Size and Share

Market Overview

| Study Period | 2024 - 2030 |

|---|---|

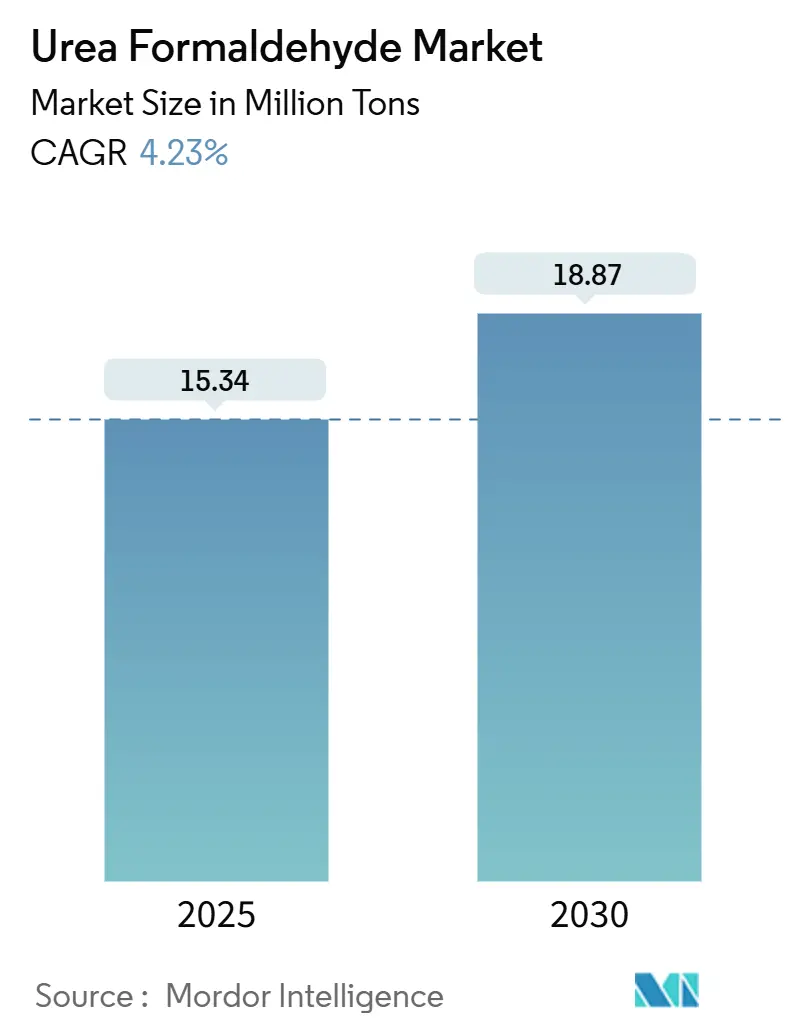

| Market Volume (2025) | 15.34 Million tons |

| Market Volume (2030) | 18.87 Million tons |

| Growth Rate (2025 - 2030) | 4.23% CAGR |

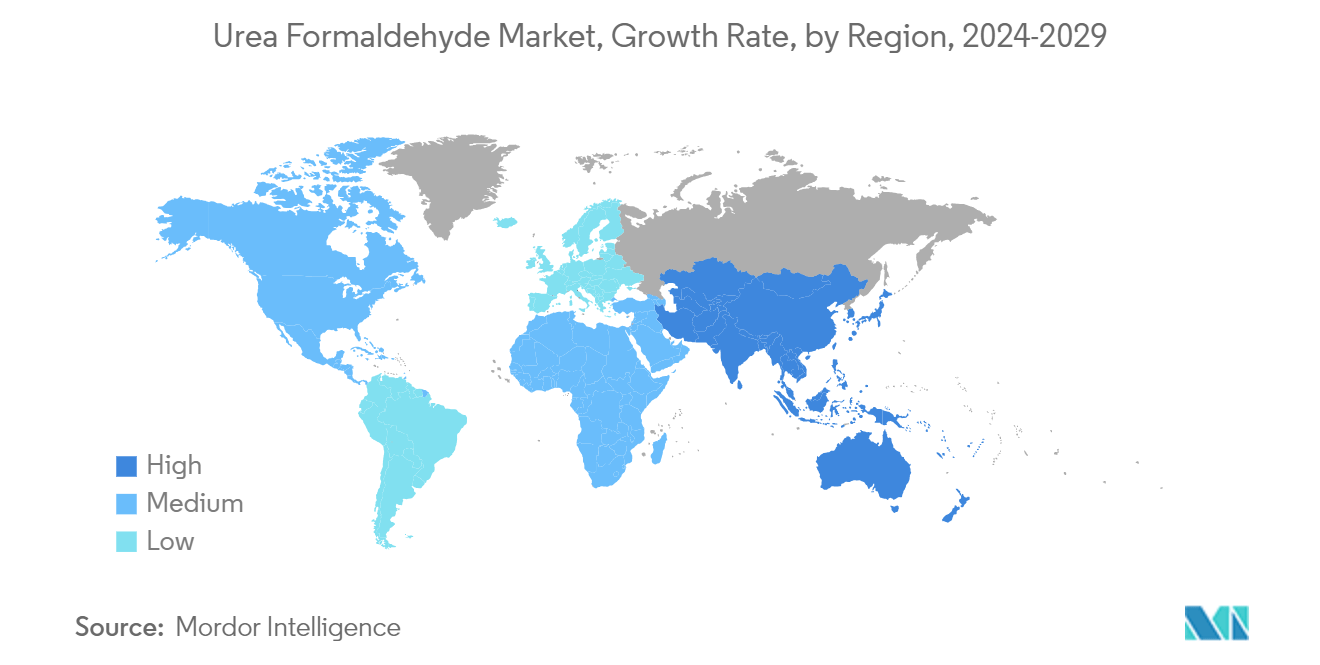

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

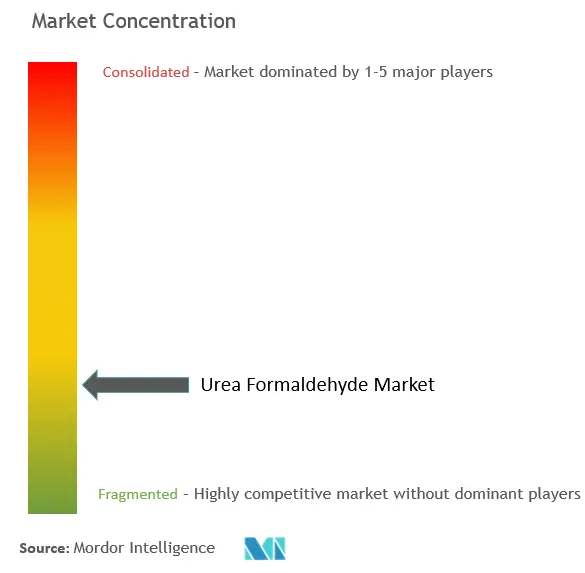

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Urea Formaldehyde Market Analysis by Mordor Intelligence

The Urea Formaldehyde Market size is estimated at 15.34 million tons in 2025, and is expected to reach 18.87 million tons by 2030, at a CAGR of 4.23% during the forecast period (2025-2030).

The COVID-19 epidemic negatively impacted the urea formaldehyde market. Global lockdowns and severe government rules resulted in a catastrophic setback, as most production hubs were shut down. Nonetheless, the market recovered in 2021 and is expected to rise significantly in the coming years.

- Over the short term, the growing demand for particle boards from the furniture sector and the increasing demand for medium-density fiberboard (MDF) are expected to drive the market's growth.

- However, health hazards regarding urea-formaldehyde resins are expected to hinder the market's growth.

- Nevertheless, the demand for high-quality resins in the automotive and electrical appliance industries is expected to create new opportunities for the market studied.

- Asia-Pacific dominates the Urea Formaldehyde Market globally, with the most consumption from China and India.

Global Urea Formaldehyde Market Trends and Insights

Building and Construction Segment Anticipated to Dominate the Market

- The building and construction sector, heavily dependent on materials like particle boards, plywood, and medium-density fiberboard, is a crucial driver of the urea formaldehyde resin market's growth.

- As construction activities ramp up, so does the demand and production of these building materials. The extensive use of urea-formaldehyde in boards and plywood underscores its importance and propels the overall growth of the urea-formaldehyde market.

- Oxford Economics forecasts a robust growth trajectory for global construction output, projecting an increase from over USD 4.2 trillion to a staggering USD 13.9 trillion by 2037, predominantly fueled by the construction powerhouses of China, the United States, and India.

- Both Asia-Pacific and North America are experiencing a surge in residential construction. Countries like India, China, the Philippines, Vietnam, and Indonesia are at the forefront in Asia-Pacific. Meanwhile, North America's residential construction is buoyed by a growing population, rising immigration, and the trend toward nuclear families.

- South Korea's construction industry is a major economic contributor and an essential source of foreign exchange and export earnings. The size of South Korea's local construction market is expanding mainly due to solid growth in private residential construction.

- The government has also planned to execute large-scale redevelopment projects to supply 830,000 housing units in Seoul and other cities by 2025. From the planned construction, Seoul will get 323,000 new houses, and 293,000 will be built near Gyeonggi Province and Incheon. Major cities like Busan, Daegu, and Daejeon will also benefit with 220,000 new houses in 4 years.

- With housing markets rising, the Asia-Pacific region, spearheaded by China and India, is set to lead the global surge in housing construction.

- China, commanding 20% of the world's construction investments, is projected to channel nearly USD 13 trillion into buildings by 2030, underscoring a bullish outlook for the niobium market.

- Recognizing its significance, the Indian government is ramping up housing construction efforts, aiming to cater to the needs of its 1.3 billion citizens.

- Highlighting India's momentum, the National Real Estate Development Corporation (NAREDCO) reports that the top 7 cities collectively completed 4.35 lakh units in 2023, with 2024 poised for a substantial uptick. Further underscoring this trend, County Group, a prominent Noida-based real estate developer, is set to unveil over 4 million sq. ft across three ambitious housing projects this year.

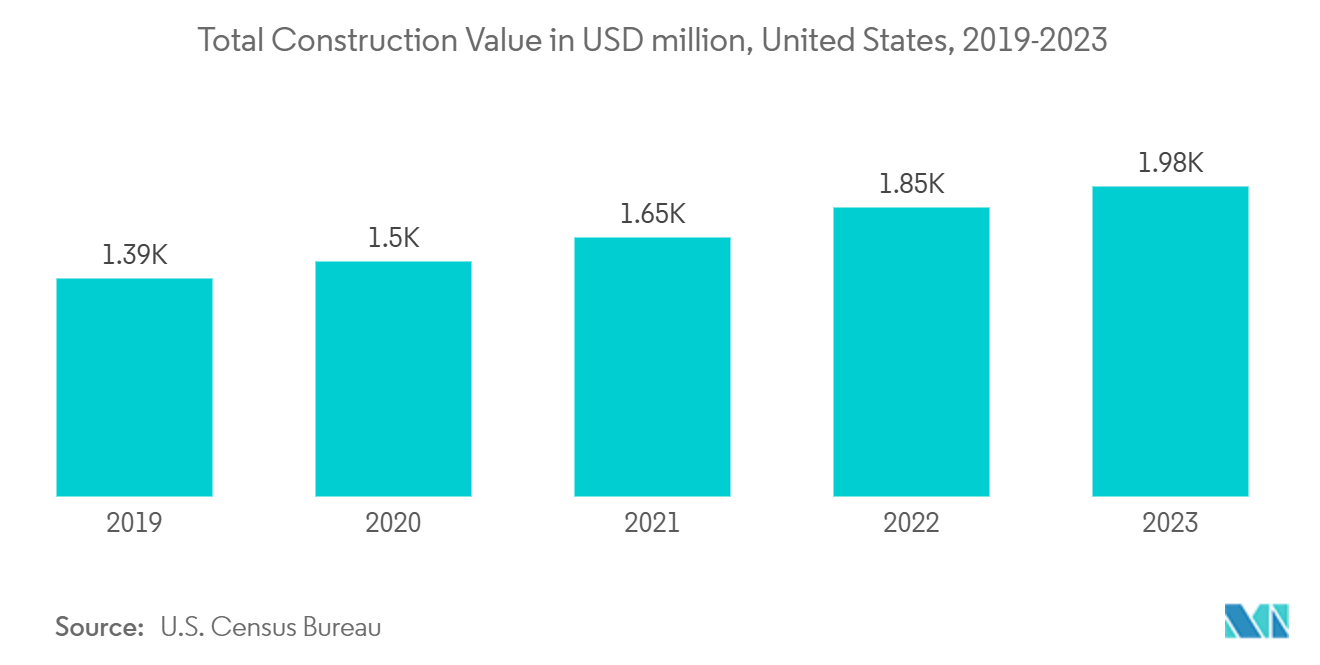

- The United States dominates the construction industry in North America, with Canada and Mexico also making substantial investments. According to the US Census Bureau, the United States saw a 4.46% increase in new housing units in 2023, reaching 1,452 thousand units, up from 1,390.5 thousand in 2022. Additionally, the annual construction value in the country hit USD 1.97 trillion in 2023, marking a 7% rise from USD 1.84 trillion in 2022.

- In Canada, government initiatives like the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada are poised to bolster the construction sector significantly. In August 2022, the Canadian government unveiled a major investment exceeding USD 2 billion for these initiatives, aiming to develop around 17,000 homes nationwide, including a substantial number of affordable units.

- Given these dynamics, the building and construction segment is poised to retain its leading position in the Urea Formaldehyde Market during the forecast period.

Asia-Pacific to Dominate the Market

- With China and India at the forefront, the Asia-Pacific region dominates the global market.

- China plays a pivotal role as the world's top producer of urea formaldehyde resins. With its growing population, China's agricultural sector is evolving to meet rising food demands. This evolution hinges on fertilizer performance and efficiency, boosting the consumption of urea formaldehyde resins.

- Boasting the world's largest construction market, China accounts for 20% of global construction investments. Projections indicate that by 2030, China is expected to invest nearly USD 13 trillion in buildings, signaling a robust market outlook. The nation's escalating housing demand is set to bolster public and private residential construction, with a notable uptick in tall buildings and hotels.

- To accelerate low-cost housing projects, Hong Kong's housing authorities have unveiled initiatives targeting the delivery of 301,000 public housing units by 2030.

- Beyond construction, urea formaldehyde resin plays a pivotal role in fiberboard production. This fiberboard finds its application in the automotive sector, shaping components like dashboards and door shells. According to the latest data released by the China Association of Automobile Manufacturers (CAAM), car production in the country it exceeded 30.16 million units in the year 2023, registering an 11.6% increase compared to the previous year. A total of 30.09 million units of passenger cars were sold in the country in 2023, registering a 12% increase compared to last year.

- According to the data released by the Society of India Automotive Manufacturing (SIAM), 4.58 million automotive vehicles were manufactured in the FY2023, compared to 3.65 million vehicles produced in 2022. The country saw a rise of around 25% in automotive production in 2023 compared to the previous year.

- India's electronics manufacturing sector is growing steadily and is driven by favorable government policies. These include 100% Foreign Direct Investment (FDI), no industrial license requirements, and a shift to automated production. In August 2023, India launched the Modified Incentive Special Package Scheme (M-SIPS) and the Electronics Development Fund (EDF), with a budget of USD 114 million to support domestic electronics manufacturing.

- Given these dynamics, the Asia-Pacific region is set to uphold its Urea Formaldehyde Market dominance throughout the forecast period.

Competitive Landscape

The global urea formaldehyde resins market is fragmented in nature. The major players in the market (not in a particular order) include Achema, BASF SE, Hexion, Kronoplus Limited, and Bakelite Synthetics.

Urea Formaldehyde Industry Leaders

-

Hexion

-

BASF SE

-

Kronoplus Limited

-

Achema

-

Bakelite Synthetics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2022: Bakelite Synthetics acquired the chemicals division of Georgia-Pacific. This acquisition encompasses 11 chemical facilities, employing around 600 individuals across the United States and South America. Through this strategic move, Bakelite Synthetics seeks to provide its customers with an expanded product portfolio and broaden its geographic footprint.

Global Urea Formaldehyde Market Report Scope

Urea formaldehyde resins, a subset of amino resins, are crafted through the polymeric condensation of formaldehyde and urea. These resins primarily serve as binders in manufacturing various wood products, including adhered wood products, particleboard, plywood, and medium-density fiberboard. They impart several desirable traits to these products, such as a high heat distortion temperature, strong tensile strength, low water absorption, and elevated surface hardness.

The urea formaldehyde resin market is segmented by application, end-user industry, and geography. The market is segmented by application into particle board, wood adhesives, plywood, medium-density fiberboard, and other applications (plastics, adhesives, etc.). In the end-user industry, the market is segmented into automotive, electrical appliances, agriculture, building and construction, and other end-user industries (pulp and paper, etc.). The report also covers the market size and forecasts for urea-formaldehyde in 27 countries across major regions. Market sizing and forecasts are made for each segment based on volume (kilotons).

| Particle Board |

| Wood Adhesives |

| Plywood |

| Medium Density Fiberboard |

| Other Applications |

| Automotive |

| Electrical Appliances |

| Agriculture |

| Building and Construction |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Particle Board | |

| Wood Adhesives | ||

| Plywood | ||

| Medium Density Fiberboard | ||

| Other Applications | ||

| By End-user Industry | Automotive | |

| Electrical Appliances | ||

| Agriculture | ||

| Building and Construction | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Urea Formaldehyde Resins Market?

The Urea Formaldehyde Resins Market size is expected to reach 15.34 million tons in 2025 and grow at a CAGR of 4.23% to reach 18.87 million tons by 2030.

What is the current Urea Formaldehyde Resins Market size?

In 2025, the Urea Formaldehyde Resins Market size is expected to reach 15.34 million tons.

Who are the key players in Urea Formaldehyde Resins Market?

Hexion, BASF SE, Kronoplus Limited, Achema and Bakelite Synthetics are the major companies operating in the Urea Formaldehyde Resins Market.

Which is the fastest growing region in Urea Formaldehyde Resins Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Urea Formaldehyde Resins Market?

In 2025, the Asia Pacific accounts for the largest market share in Urea Formaldehyde Resins Market.

What years does this Urea Formaldehyde Resins Market cover, and what was the market size in 2024?

In 2024, the Urea Formaldehyde Resins Market size was estimated at 14.69 million tons. The report covers the Urea Formaldehyde Resins Market historical market size for years: 2024. The report also forecasts the Urea Formaldehyde Resins Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: