Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

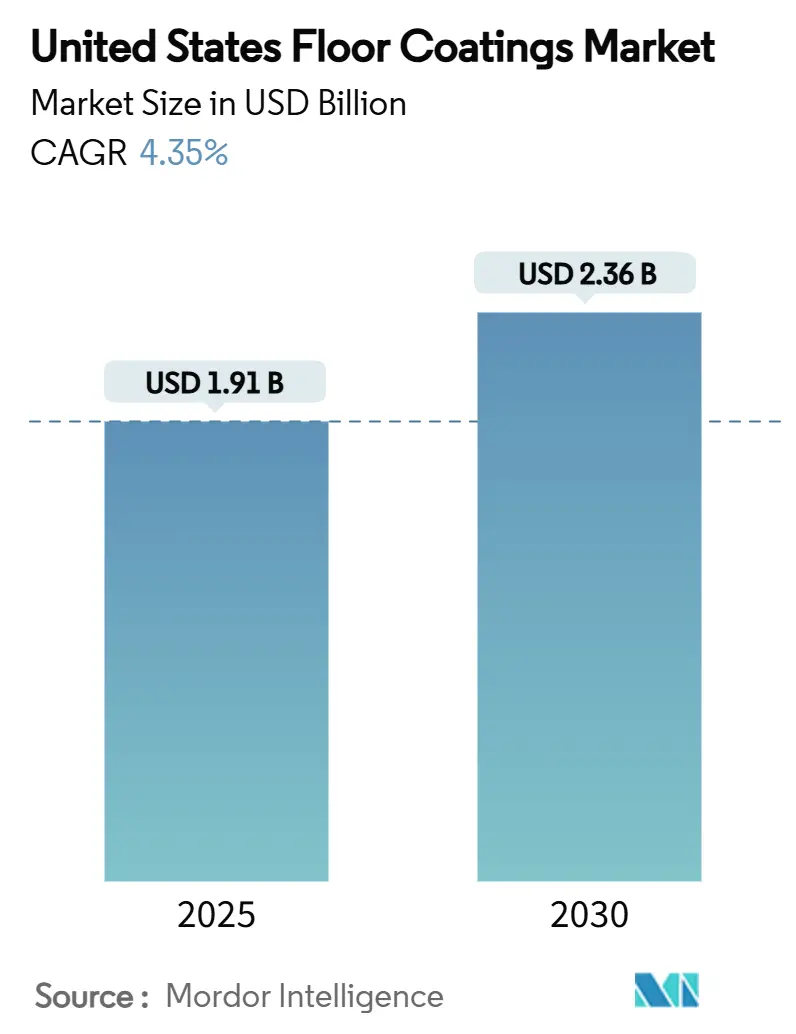

| Market Size (2025) | USD 1.91 Billion |

| Market Size (2030) | USD 2.36 Billion |

| Growth Rate (2025 - 2030) | 4.35% CAGR |

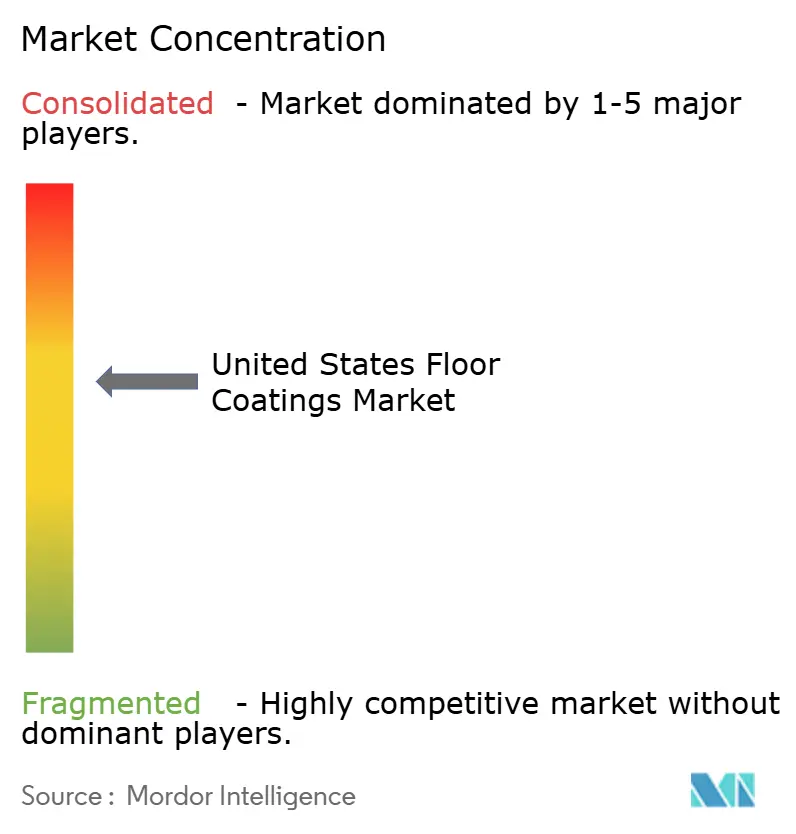

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Floor Coatings Market Analysis by Mordor Intelligence

The United States Floor Coatings Market size is estimated at USD 1.91 Billion in 2025, and is expected to reach USD 2.36 Billion by 2030, at a CAGR of 4.35% during the forecast period (2025-2030). This outlook is underpinned by an 8.6% jump in total construction starts expected in 2025, buoyed by lower borrowing costs and robust spending on data centers, healthcare facilities, and electric-vehicle (EV) plants. Demand centers on high-performance resinous systems that satisfy electrostatic-discharge (ESD) and antimicrobial standards while complying with increasingly stringent volatile-organic-compound (VOC) rules. Epoxy retains its foothold because of proven durability, but polyaspartic technologies are gaining from faster cure times that shorten facility shutdowns. Concrete remains the dominant substrate, yet engineered-wood adoption in sustainable designs is lifting specialist coating requirements.

Key Report Takeaways

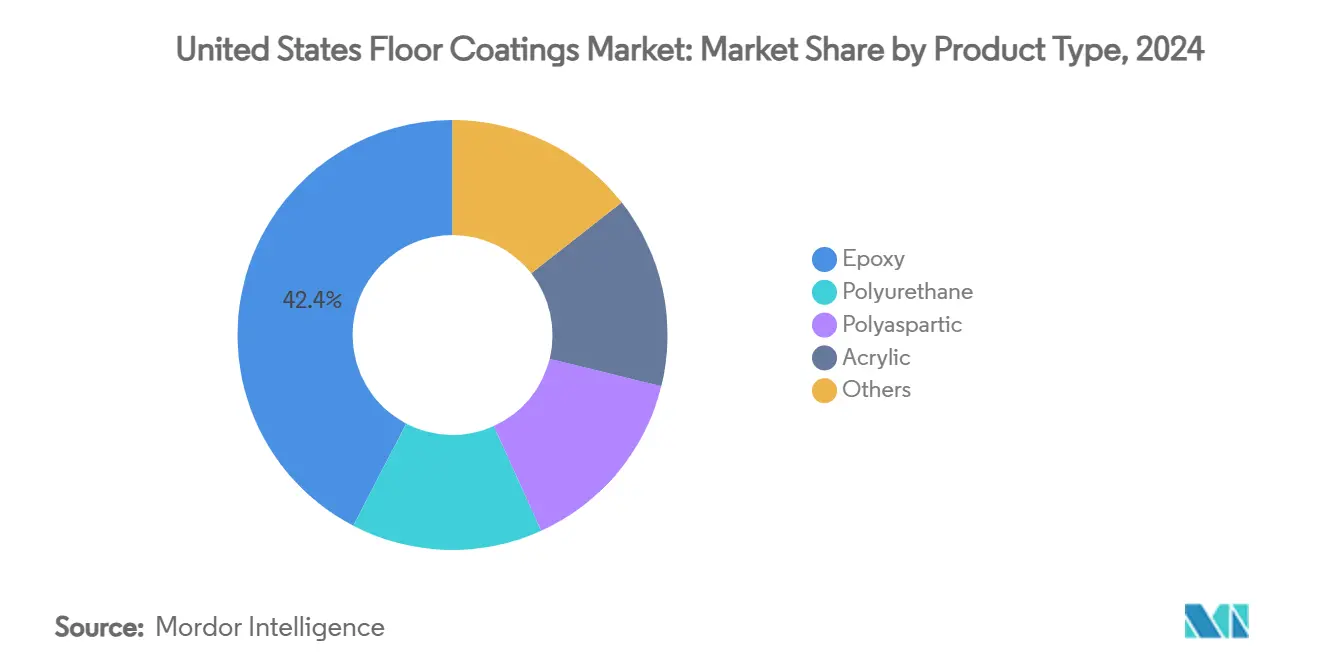

- By product type, epoxy commanded 42.35% of the United States Floor Coatings market share in 2024, while polyaspartic systems are projected to grow at a 5.78% CAGR through 2030.

- By floor material, concrete accounted for 68.81% of the United States Floor Coatings market size in 2024, with wood substrates advancing at a 5.42% CAGR between 2025–2030.

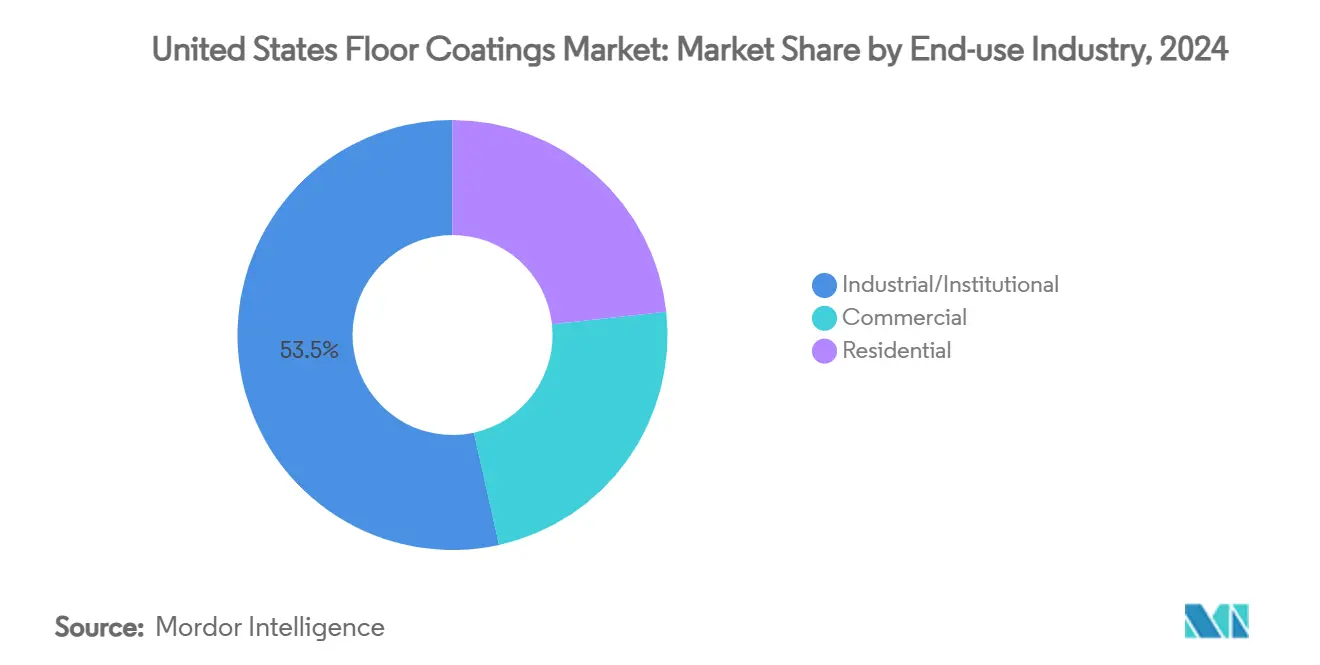

- By end-use industry, the industrial/institutional segment held 53.47% share of the United States Floor Coatings market size in 2024 and is set to expand at a 4.59% CAGR over the same period.

United States Floor Coatings Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Growth in Commercial and Industrial Construction | +1.2% | National, concentrated in Texas, Southeast | Medium term (2-4 years) |

| Rising Adoption of Epoxy Systems for Durability | +0.8% | National, stronger in industrial corridors | Long term (≥ 4 years) |

| Demand for Aesthetic Decorative Coatings in Remodeling | +0.6% | National, urban centers leading | Short term (≤ 2 years) |

| Shift Toward Low-VOC, High-solids Formulations | +0.4% | California, Northeast states | Medium term (2-4 years) |

| EV Gigafactory and Data-center Builds Need ESD Flooring | +0.5% | Texas, Southeast, Midwest | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Growth in Commercial and Industrial Construction

The United States' commercial construction's projected 8.6% growth in 2025 creates a multiplier effect for floor coatings demand, particularly in sectors requiring specialized performance characteristics. The Texas construction industry maintains nearly USD 40 Billion in ongoing and upcoming projects through TxDOT, including a USD 3 Billion expansion at Dallas-Fort Worth International Airport. This infrastructure surge extends beyond traditional applications, as the U.S. Bureau of Labor Statistics identifies power generation and electrical contractor segments as key employment growth areas, directly correlating with increased demand for conductive and dissipative floor coatings in energy infrastructure projects[1]“Employment Projections for Construction Trades, 2023-2033,” U.S. Bureau of Labor Statistics, bls.gov. The construction industry's 4.7% employment growth projection through 2033 indicates sustained demand for flooring installations, though labor constraints may shift preferences toward faster-curing polyaspartic systems. Healthcare construction's 27% share of anticipated projects benefits antimicrobial coating segments, as post-pandemic facility design prioritizes infection control surfaces.

Rising Adoption of Epoxy Systems for Durability

Epoxy’s 42.35% share in 2024 reflects its chemical resistance and lifecycle performance, qualities prized in advanced manufacturing where thermal cycling and heavy loads are routine. Domestic output is growing as anti-dumping actions redirect sourcing toward U.S. plants, trimming lead times but lifting input costs. Innovations such as bio-based resins align with sustainability goals without sacrificing film integrity. Clean-room settings in automotive battery and aerospace assembly continue to specify epoxy floors for their ability to meet both Electrostatic Discharge (ESD) and sanitary standards.

Demand for Aesthetic Decorative Coatings in Remodeling

The residential remodeling market's recovery from interest rate pressures creates demand for decorative floor coatings that combine aesthetic appeal with functional performance. Industry leaders from Mohawk, Shaw, and Mannington emphasized the importance of preparing for demand recovery as secondary home sales improve, with 90% of transactions involving existing homes that typically require flooring updates. Decorative concrete coatings benefit from homeowners' preference for low-maintenance surfaces replicating natural materials while offering superior durability and stain resistance. The Surfaces 2024 expo highlighted innovations in digital printing technology for flooring, enabling realistic wood and stone textures that expand decorative coating applications beyond traditional industrial uses. Consumer preferences increasingly favor sustainable options, with waterborne formulations gaining traction due to reduced environmental impact and improved indoor air quality. Integrating antimicrobial properties into decorative systems addresses health-conscious consumers' concerns while maintaining aesthetic appeal, creating differentiation opportunities for manufacturers targeting the residential remodeling segment.

Shift Toward Low-VOC, High-solids Formulations

Regulatory pressure from state-level VOC limits drives formulation innovation toward high-solids systems that maintain performance while meeting environmental compliance requirements. California's floor coating VOC limit of 100 grams per liter, effective since 2017, established the benchmark that other states increasingly adopt, with Michigan and Colorado implementing similar restrictions in 2024. The South Coast Air Quality Management District's Rule 1113 sets even stricter limits at 50 grams per liter, forcing manufacturers to develop waterborne and high-solids technologies that deliver comparable performance to traditional solvent-based systems. Sherwin-Williams' emphasis on producing coatings that meet stringent VOC standards while collaborating with industry stakeholders to refine regulations demonstrates how leading manufacturers are positioning for regulatory compliance as a competitive advantage. The transition to low-VOC formulations creates technical challenges in maintaining film formation, adhesion, and durability properties, requiring significant R&D investment that favors larger manufacturers with extensive technical resources.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Epoxy and Raw-material Prices | -0.7% | National, import-dependent regions | Short term (≤ 2 years) |

| Stricter State VOC Limits Raise Compliance Costs | -0.4% | California, Northeast states | Medium term (2-4 years) |

| Shortage of Certified Resinous-flooring Applicators | -0.3% | National, acute in growth regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Epoxy and Raw-material Prices

Raw material price volatility creates margin pressure and project cost uncertainty that constrains market growth, particularly as anti-dumping investigations reshape epoxy resin supply chains. The U.S. International Trade Commission's determination that the domestic industry suffers material injury from subsidized imports from South Korea, Taiwan, and Thailand resulted in potential duties that could increase input costs for floor coating manufacturers. The concentration of epoxy production in Asia creates supply chain vulnerabilities that manifest as price volatility during geopolitical tensions or logistics disruptions. Smaller coating manufacturers face particular challenges in managing input cost fluctuations, as they lack larger competitors' purchasing power and supply chain diversification. The shift toward domestic epoxy production, while reducing import dependence, may result in structurally higher costs due to smaller production scales and higher labor costs compared to Asian facilities.

Stricter State VOC Limits Raise Compliance Costs

Evolving VOC regulations create compliance costs that disproportionately impact smaller manufacturers while driving industry consolidation toward companies with extensive R&D capabilities. California's leadership in establishing stringent VOC limits forces national manufacturers to develop dual product lines or reformulate entire portfolios to meet the most restrictive requirements, increasing development costs and inventory complexity[2]“2024 Architectural & Industrial Maintenance Coatings VOC Limits,” California Air Resources Board, carb.ca.gov. The patchwork of state regulations creates compliance challenges for contractors operating across multiple jurisdictions, with products approved in one state potentially violating limits in another. Reformulation costs to achieve low-VOC performance often require premium raw materials and advanced manufacturing processes, creating price premiums that can reduce market penetration in price-sensitive applications. The technical challenges of maintaining film formation, adhesion, and durability properties in low-VOC formulations require significant R&D investment that favors larger manufacturers with extensive technical resources.

Segment Analysis

By Product Type: Polyaspartic Growth Challenges Epoxy Dominance

Epoxy retained a 42.35% United States floor coatings market share in 2024 thanks to its entrenched performance record in factories, warehouses, and aviation hangars. Polyaspartic systems, however, are projected to expand at a 5.78% CAGR, propelled by overnight-curing capability that limits facility downtime, low to zero VOC profiles, and elasticity that tolerates substrate movement. The United States floor coatings market size for epoxy remains healthy, yet its expansion is moderating as users weigh lifecycle savings against longer application windows. Polyurethane coatings straddle cost and performance, especially where chemical resistance outstrips acrylics but budgets preclude premium solutions. Graphene-enhanced and bio-based chemistries in the “Others” segment promise niche traction in ESD-sensitive and Leadership in Energy and Environmental Design (LEED)-driven projects, respectively.

Sustained industrial upgrades, notably at EV battery plants and chemical processing hubs, keep epoxy relevant, while retail chains and stadium operators gravitate to polyaspartic overlays that can reopen floors within a single shift. Manufacturers able to supply both chemistries offer contractors the flexibility to choose system packages based on project timelines and environmental constraints. Supply-chain security, particularly for amine hardeners derived from imported feedstocks, remains a strategic concern shared across all resin systems.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Floor Material: Wood Substrates Drive Innovation

Concrete retained 68.81% of 2024 demand, reflecting its ubiquity in slabs-on-grade and elevated decks where protective coatings extend service life. That said, the United States floor coatings market size for wood substrates is on a 5.42% CAGR track as architects adopt engineered lumber for carbon-reduction targets. Engineered-wood flooring captured 74% of hardwood sales in 2024, underscoring the appetite for coatings that manage moisture ingress while showcasing natural grain. United States floor coatings market share gains in this segment reward suppliers offering breathable yet durable waterborne urethanes.

Wood-friendly chemistries must allow vapor diffusion to avoid cupping and gaps, forcing formulators to balance permeability with abrasion resistance. Commercial spaces such as boutique retail and hospitality venues represent the vanguard of this shift, as operators value both the aesthetic warmth of timber and the maintainability of resinous finishes. Metal, ceramic, and composite substrates remain specialized niches that nonetheless demand primers tailored to high-energy surfaces.

By End-use Industry: Industrial Facilities Lead Demand

Industrial and institutional buildings captured 53.47% of total 2024 sales, and their 4.59% CAGR through 2030 indicates that specification sophistication is rising faster than in other sectors. Clean-process manufacturing lines in electronics, aerospace, and biopharma insist on coatings that fuse ESD control, chemical resistance, and antimicrobial functionality. The United States floor coatings market size tied to data-center corridors in Texas and the Midwest is accelerating as operators roll out hyperscale campuses requiring conductive raised floors.

Commercial venues benefit from the 8.6% construction-start surge, with healthcare and office retrofits motivating antimicrobial and decorative overlays. Residential remodeling lags yet holds latent upside once mortgage rates normalize, particularly for garages and basements retrofitted with waterborne epoxies or flake-broadcast polyaspartic systems. Institutional budgets for schools and municipal buildings remain sensitive to capital-outlay cycles; nonetheless, deferred maintenance translates into resurfacing projects that favor turnkey resin packages compatible with rapid project schedules.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Competitive Landscape

The United States Floor Coatings market is moderately consolidated with the presence of major players, such as the Sherwin-Williams Company, BASF, PPG Industries Inc., Sika AG, and RPM International Inc. Sherwin-Williams posted USD 18.44 Billion in global coatings revenue for 2023 and further solidified its resinous-flooring portfolio by acquiring Dur-A-Flex. PPG pursued a channel strategy, partnering with Shaw Industries’ Patcraft brand to tap established commercial-flooring specifiers. RPM International, via its Carboline and Stonhard units, leverages differentiated chemistries to serve industrial niches. Price competition intensifies during resin cost spikes, yet large players hedge with multi-year supply accords. Installer capability is an increasingly strategic lever. All three leading suppliers run certification academies that teach surface prep, moisture mitigation, and multi-layer installation, thereby locking in brand loyalty among contractors.

United States Floor Coatings Industry Leaders

The Sherwin-Williams Company

Sika AG

BASF

PPG Industries Inc.

RPM International Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: DYCO, a subsidiary of the ICP Group in Massachusetts, launched DYCO Court & Floor, a new 100% acrylic, medium-textured anti-slip coating for commercial and residential recreational surfaces, porches, steps, walkways, and more. This coating can be used over asphalt, concrete, and previously coated surfaces.

- July 2024: The Sherwin-Williams Company launched a dedicated line of comprehensive floor coatings for clean and dry rooms within electric vehicle (EV) battery manufacturing facilities. These floor coatings will be available for the United States and other countries.

United States Floor Coatings Market Report Scope

Floor coatings are durable, protective layers applied to surfaces subjected to extreme wear or corrosion. Warehouses, chemical plants, and production floors are typical applications-resin Type, Floor Material, End-User Industry, and Geography segment of the market. By Resin Type, the market is segmented into epoxy, polyaspartics, acrylic, polyurethane, and other resin types (polyester, vinyl ester). By Floor Material, the market is segmented into wood, concrete, and other floor materials. By End-User Industry segments the market into Industrial, Decorative, and Car Parks. The report offers market size and forecasts for revenue (USD million) for all the above details.

By Product Type

| Epoxy |

| Polyurethane |

| Polyaspartic |

| Acrylic |

| Others |

By Floor Material

| Concrete |

| Wood |

| Others |

By End-use Industry

| Industrial/Institutional |

| Commercial |

| Residential |

| By Product Type | Epoxy |

| Polyurethane | |

| Polyaspartic | |

| Acrylic | |

| Others | |

| By Floor Material | Concrete |

| Wood | |

| Others | |

| By End-use Industry | Industrial/Institutional |

| Commercial | |

| Residential |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the estimated value of the United States Floor Coating sales in 2025?

Sales are pegged at USD 1.91 Billion, with expansion projected through 2030.

What compound annual growth rate is forecast between 2025 and 2030?

Total sales are projected to advance at a 4.35% CAGR over the five-year period.

Which resin type shows the fastest growth momentum?

Polyaspartic formulations lead with a 5.78% CAGR, driven by rapid cure times and low-VOC profiles.

What makes polyaspartic systems attractive for commercial projects?

These coatings cure and accept traffic within hours, minimizing facility downtime while meeting stringent environmental limits.

How do state VOC limits affect formulation strategies?

States such as California cap VOC content at 100 g/L or 50 g/L under South Coast Rule 1113, forcing suppliers to invest in high-solids and waterborne chemistries.