Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

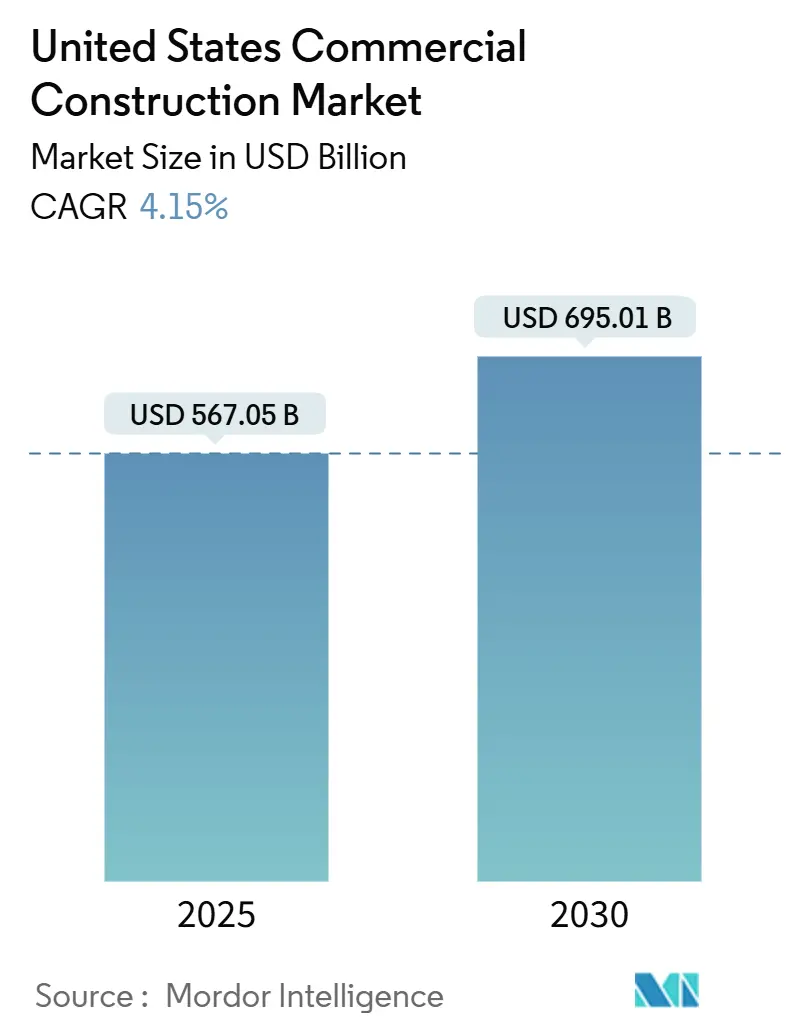

| Market Size (2025) | USD 567.05 Billion |

| Market Size (2030) | USD 695.01 Billion |

| Growth Rate (2025 - 2030) | 4.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Commercial Construction Market Analysis by Mordor Intelligence

The US Commercial Construction Market size is estimated at USD 567.05 billion in 2025, and is expected to reach USD 695.01 billion by 2030, at a CAGR of 4.15% during the forecast period (2025-2030). Sustained spending on data centers, large-scale logistics hubs, and infrastructure upgrades is underpinning growth even as financing costs and material inflation stay elevated. Rising e-commerce volumes continue to trigger record warehouse demand, while office owners redirect capital into hybrid-ready retrofits to offset persistently high vacancy. Federal funding from the Infrastructure Investment and Jobs Act (IIJA) is unlocking long-term transit, airport, and bridge programs that complement dominant private investment flows. Technology adoption across artificial intelligence (AI) project controls, modular fabrication, and embodied-carbon tracking is narrowing delivery schedules and helping contractors protect margins.

Key Report Takeaways

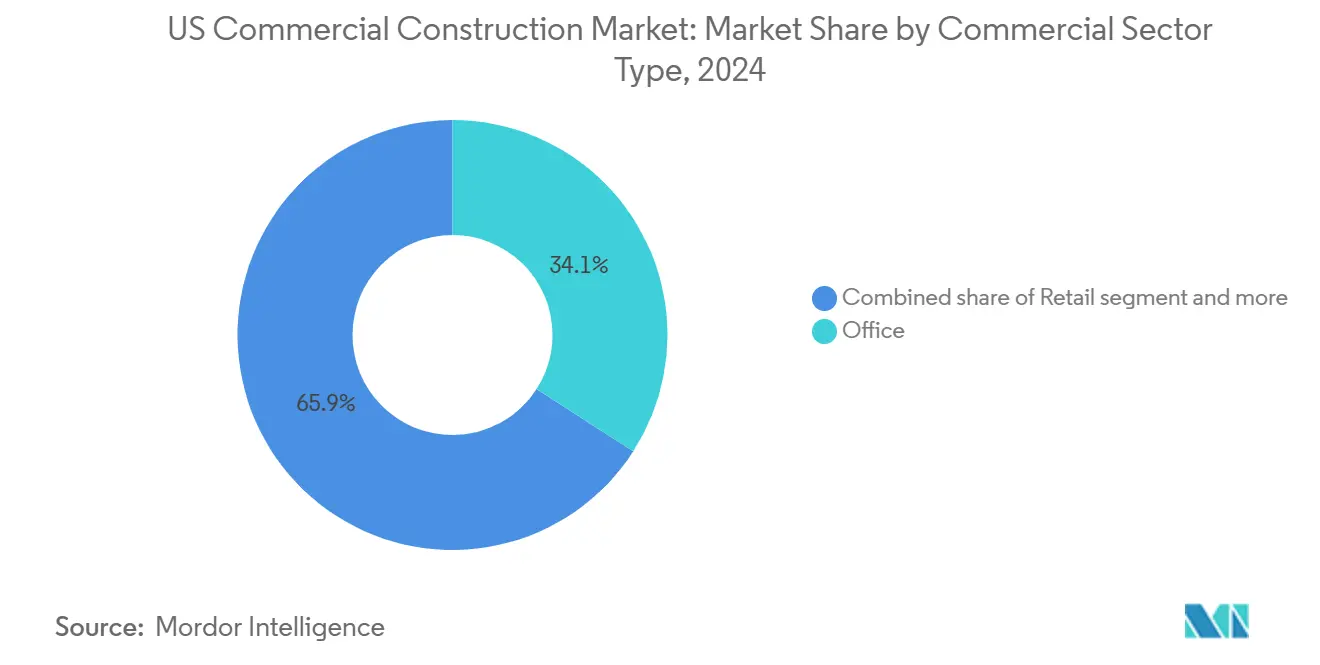

- By commercial sector, office construction held 34.1% of the United States commercial construction market share in 2024; the industrial & logistics segment is projected to register the fastest 5.21% CAGR through 2030.

- By construction type, new construction represented 67.3% revenue in 2024, while renovation work is expected to accelerate at a 5.05% CAGR through 2030.

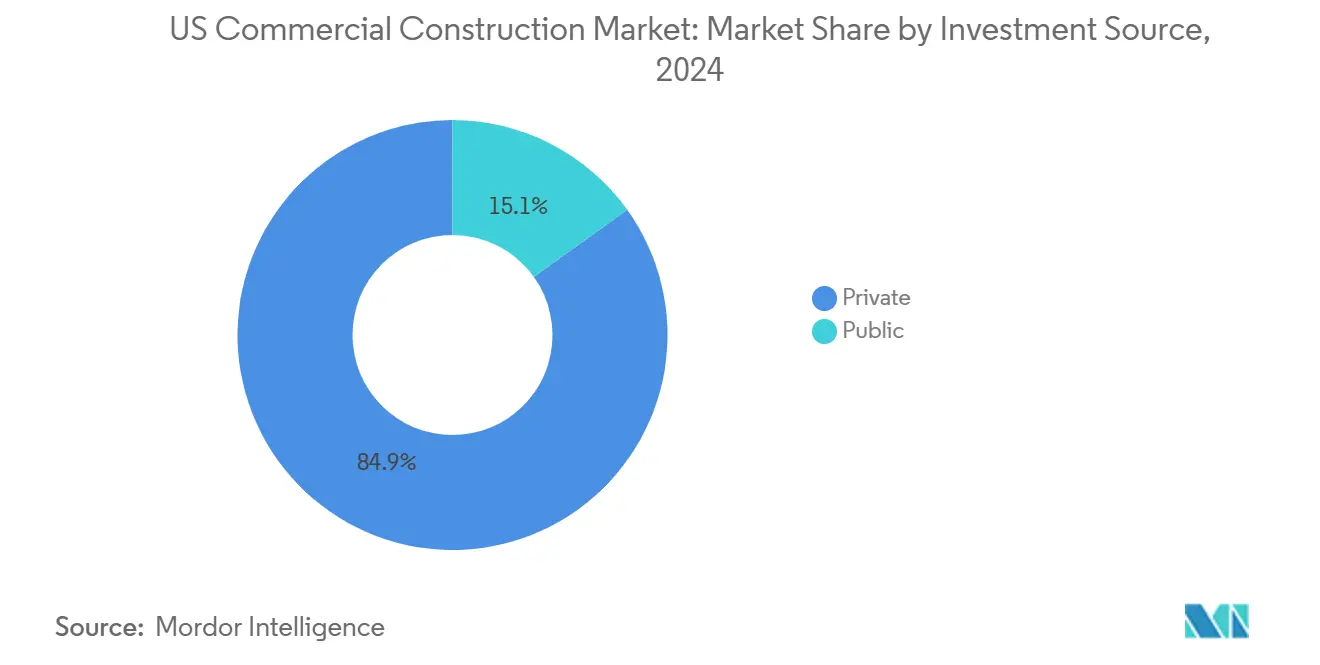

- By investment source, private capital accounted for 84.9% of 2024 activity; public sector spending is forecast to rise at a 5.41% CAGR as IIJA programs ramp up.

- By state, Texas led with 16.5% of the United States' commercial construction market size in 2024, whereas Florida is set to be the fastest-growing state at a 5.30% CAGR to 2030.

United States Commercial Construction Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data center growth driven by AI and cloud computing infrastructure | +1.5% | National, with concentration in Virginia, Texas, Georgia | Long term (≥ 4 years) |

| E-commerce expansion fueling warehouse and fulfillment center build-outs | +1.2% | Global, concentrated in Texas, California, Florida logistics hubs | Medium term (2-4 years) |

| Public investment in transit and civic infrastructure | +0.9% | National, with emphasis on high-density metropolitan areas | Long term (≥ 4 years) |

| Office retrofit and redevelopment for hybrid-ready workplaces | +0.8% | Urban markets nationwide, strongest in gateway cities | Short term (≤ 2 years) |

| Green building and ESG focus driving certified development | +0.7% | National, with premium in California, New York, Washington | Medium term (2-4 years) |

| Hospitality and mixed-use project recovery from travel demand | +0.6% | Urban centers and tourism destinations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Center Construction Reaches Historic Proportions

Soaring AI training loads and multicloud adoption have triggered unprecedented data-center builds that now absorb 25% of all commercial power demand additions nationwide. Investment surged 43.1% through November 2024 to USD 31.5 billion, led by hyperscale projects such as the USD 17 billion campus in Coweta County, Georgia. Power deficits exceeding 50% of utility capacity in legacy hubs are pushing developers toward adjacent states, and many are exploring on-site gas turbines or small modular reactors to secure a resilient supply. Electrical gear and liquid-immersion cooling account for nearly one-quarter of total build cost, reshaping subcontractor scopes. Because AI compute demand shows no sign of tapering, large-scale campuses are expected to remain a primary growth lever for the United States' commercial construction market over the long term.

E-commerce Expansion Drives Logistics Infrastructure Boom

Strong e-commerce sales keep pushing the United States' commercial construction market toward larger and more automated distribution assets. Amazon alone invested USD 2 billion in industrial properties during 2024, doubling its logistics network footprint to support same-day delivery and parallel data-center rollout. Third-party logistics (3PL) groups now account for roughly 35% of industrial leasing, prompting developers to design multi-story facilities around robotics, high-bay racking, and AI-powered inventory controls. Nearly one-quarter of industrial-zoned parcels acquired since 2022 have been earmarked for data centers rather than traditional warehousing, illustrating the blending of logistics and digital infrastructure. Land availability near Tier-1 power substations in Texas and Northern Virginia is shrinking, supporting sustained rental growth and a deep pipeline of speculative projects. As operators chase faster delivery promises, end-to-end supply-chain realignment keeps demand for new fulfillment facilities elevated[1]Stephanie Moot, “Quarterly E-Commerce Retail Sales: 2025 Q1,” U.S. Census Bureau, census.gov.

Public Infrastructure Investment Accelerates Regional Development

Public infrastructure investment is emerging as a cornerstone for advancing regional development across the United States. IIJA allocations have already funded more than 56,000 transportation projects, and federal highway construction outlays are forecast to reach USD 126 billion in 2025, up 16% from 2024. Mega-projects such as the USD 16.1 billion Gateway rail tunnel and the USD 2 billion Baltimore bridge replacement are awarding multi-year contracts to joint ventures that pool heavy civil expertise. The Federal Highway Administration’s Bridge Investment Program is channeling USD 5 billion toward large bridge rehabilitations, spurring regional demand for steel fabrication, precast components, and specialty geotechnical services. This public pipeline offers contractors counter-cyclical volume as private developers navigate tighter credit markets, thereby supporting a stable baseline for the United States commercial construction market through 2030.

Office Retrofit Surge Addresses Hybrid Work Transformation

The shift to hybrid work has driven significant changes in office design, as employers adapt to evolving workplace needs. Employers continue to reconfigure workspace footprints as hybrid policies stabilize at roughly three in-office days per week. Premium retrofit budgets averaged USD 303 per square foot in San Francisco during 2024, up 4% year-on-year, as landlords replaced large conference rooms with smaller team suites and technology-rich collaboration zones. High-rise vacancy remains at 25% above pre-pandemic targets, prompting major owners such as Sage Realty and Boston Global Investors to invest more than USD 350 million collectively in amenity-heavy repositionings that attract flight-to-quality tenants. The renovation focus has lifted design-build demand and shortened project schedules, supporting faster revenue recognition for contractors. With flexible layouts now a leasing prerequisite, retrofit spending is projected to stay resilient even if new office starts soften through mid-decade.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortages and wage pressure slowing project delivery | -1.1% | National, most acute in Southeast and Southwest growth markets | Short term (≤ 2 years) |

| High material and freight inflation compressing margins | -0.9% | National, with regional variations in transportation costs | Medium term (2-4 years) |

| Tight lending conditions and rising interest rates hindering financing | -0.8% | National, particularly affecting speculative development | Short term (≤ 2 years) |

| Permitting delays and zoning restrictions prolonging pre-construction | -0.6% | Most severe in California, New York, coastal metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortage Crisis Intensifies Across All Skill Levels

The skilled labor shortage in the U.S. commercial construction market has reached critical levels, posing significant challenges to the industry's growth and efficiency. The industry needs 439,000 additional craft professionals by 2025, yet registered apprenticeship completions total only 40,000 annually, widening the talent gap. Firms report 88% difficulty in hiring, especially for entry-level roles, driving unskilled wage gains of nearly 3.5% compared with sub-2.5% for seasoned trades. Contractors now offer signing bonuses, fast-tracked training, and flexible schedules to stem attrition, but these measures increase overhead and threaten bid competitiveness. Delays tied to thin crews are extending project durations by 5–7 weeks on average, which compounds schedule risk on fixed-price contracts. Without a sizeable pipeline of new entrants, labor scarcity is expected to weigh on the United States' commercial construction market through at least 2027.

Material Cost Inflation Reaches Critical Levels

Material cost inflation has reached unprecedented levels, significantly impacting the U.S. construction industry. Between December 2024 and January 2025, input costs jumped by 1.4%, bringing the total inflation since early 2020 to a staggering 40.5%. With concrete consumption on the rise due to IIJA-funded bridge projects, new 25% tariffs on cement from Canada and Mexico threaten to push ready-mix prices even higher. In 2024, structural steel prices surged by 11.2%, and experts predict further increases of up to 20% in 2025, driven by tariffs. Meanwhile, duties on Canadian softwood soared to 34.5%, leading to a 17.2% year-on-year spike in lumber prices. In response, contractors are locking in materials early and scouting alternative suppliers. However, they still grapple with margin pressures, as escalation clauses often fall short of covering the full extent of price volatility. As a result, this sustained inflation poses a significant challenge to the outlook of the U.S. commercial construction market. The industry must navigate these cost pressures carefully to maintain project viability and long-term growth.

Segment Analysis

By Commercial Sector Type: Industrial & Logistics Solidifies Growth Leadership

Office buildings captured 34.1% of the United States commercial construction market share in 2024, sustaining the largest individual slice even amid hybrid work disruption. Conversely, the industrial & logistics segment is forecast to post a 5.21% CAGR, making it the quickest-growing contributor to the United States commercial construction market. Developers delivered 322 million sq ft of new warehouse capacity in 2024, although net absorption of 125 million sq ft nudged national vacancy to 6.9%, the highest in more than a decade. Dallas-Fort Worth and Atlanta remained top leasing destinations, while Houston and Nashville rose as cost-efficient alternatives. Large 3PLs and retailers are insisting on renewable-energy-ready designs, automated picking lines, and higher clear heights, which collectively lift average construction cost per sq ft by 8–10%. Near-shoring of supply chains to the Mexico border is also stimulating speculative cross-docks along I-35 and I-10 corridors, locking in demand through 2030[2]Kevin B. Jones, “Warehouse and Distribution Center Energy Use Trends,” Journal of Construction Engineering and Management, ascelibrary.org.

Life-science conversions provide another demand outlet as office landlords adapt empty floors into wet-lab space that commands rents 1.5–2.5× traditional offices. Specialized MEP requirements and regulatory compliance necessities push construction premiums but also generate higher fee opportunities for contractors. Retail development remains subdued; however, high-street sites in Sun Belt metros still record selective ground-up projects anchored by experiential offerings. Collectively, the scale and diversity within industrial & logistics remain the primary engine driving the United States commercial construction market over the forecast horizon.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Construction Type: Renovation Accelerates as Adaptive Reuse Gains Favor

New construction accounted for 67.3% of 2024 spending, yet renovation work is projected to grow at a 5.05% CAGR, outpacing green-field starts within the United States commercial construction market size. Retrofit projects cut delivery schedules by up to 30% and embody roughly 40% less carbon than demolish-and-rebuild alternatives, aligning with new LEED v5 decarbonization targets. For landlords, conversions from legacy offices to residential or life-science uses can shave at least 50% off total project cost while unlocking premium rents. Cities such as Seattle and Boston now offer tax abatements or deferrals to encourage adaptive reuse, boosting the renovation pipeline.

Architectural firms report a larger share of billings arising from retrofit assignments, and contractors are deploying digital twin scans and off-site prefabrication to compress retrofit timelines further. Although supply-chain disruptions favor shorter-lead-time renovations, new construction remains essential for purpose-built data centers, logistics mega-sheds, and public transit terminals. Balancing both opportunities, diversified builders are better positioned to capture the full addressable United States commercial construction market.

By Investment Source: Public Funding Ramps Up but Private Capital Still Dominates

Private developers captured 84.9% of the United States' commercial construction market share in 2024, confirming their central role in financing offices, logistics hubs, and data-center campuses. Most large sponsors continued to draw on relationship lending and institutional equity even as higher interest rates added several basis points to debt spreads. Tight credit conditions prompted some owners to pause speculative ground-breaks, yet record digital-infrastructure allocations kept overall private outlays resilient. Developers also accelerated design-build and modular strategies to compress schedules and protect contingency budgets.

Public spending, although smaller in absolute terms, is projected to expand at a 5.41% CAGR through 2030, steadily raising its portion of the United States' commercial construction market size. The Infrastructure Investment and Jobs Act will lift federal highway and bridge work to USD 126 billion in 2025, creating a dependable multiyear pipeline for civil contractors. States are matching federal grants with bond issuances, while cities increasingly turn to public-private partnerships to manage risk on large transit and airport schemes. As these programs ramp up, contractors that mix public frameworks with private repeat clients are best positioned to smooth revenue cycles and capture growth on both sides of the funding spectrum.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Texas remains the largest state contributor, holding 16.5% of the United States' commercial construction market in 2024 on the back of USD 40 billion in state transportation projects and a USD 3 billion expansion at Dallas–Fort Worth International Airport. Dallas-Fort Worth and Houston serve as national data-center and logistics magnets, strengthened by favorable tax regimes and abundant land. Florida delivered the fastest 5.30% CAGR outlook thanks to population inflows, tourism recovery, and strategic port and airport modernizations that broaden its economic base. Miami, Orlando, and Tampa each unveiled multi-billion-dollar mixed-use districts that blend hospitality, retail, and residential elements, sustaining contractor backlogs[3]Marc Williams, “2025 Unified Transportation Program,” Texas Department of Transportation, txdot.gov .

Technology investments and stringent sustainability mandates shape California’s spend profile. Active projects include the USD 2.6 billion Terminal 3 modernization at San Francisco International Airport, targeting LEED Platinum status. However, permitting complexities and high labor costs temper growth, driving some developers to Phoenix and Reno alternatives. New York and Illinois concentrate on civil upgrades such as the USD 1.1 billion Kensico–Eastview Tunnel and Chicago’s rail-yard overbuilds, favoring firms with deep urban-infrastructure expertise.

Secondary markets including Georgia, North Carolina, and Colorado are scaling quickly as data-center operators and life-science tenants search for lower electricity rates and workforce availability. Together, these geographic shifts help diversify activity and sustain expansion across the broader United States commercial construction market.

Competitive Landscape

The US Commercial Construction Market remains consolidated, defining feature as contractors chase scale and bandwidth for mega-projects. Turner Construction overtook Bechtel in 2024 revenue, leveraging acquisitions such as Ireland-based Dornan Engineering to deepen process-piping and clean-room capabilities for advanced-technology clients. ACS Group merged Flatiron and Dragados into a USD 17.2 billion backlog powerhouse, positioning the Spanish conglomerate as the second-largest civil player in the United States. These moves underscore how balance-sheet strength and self-perform depth influence bidding success on IIJA and hyperscale contracts.

Technology investment is another differentiator. Bouygues forged a strategic alliance with Amazon Web Services to roll out a generative-AI contract-management platform that accelerates claims resolution. Similarly, Armstrong World Industries teamed with McKinstry to launch Overcast Innovations, delivering prefabricated ceiling grid systems that cut installation time by up to 70%. Firms that embed AI scheduling, digital twins, and modular kitting realize faster cycle times and stronger risk controls, enhancing margin resilience.

Labor strategy also shapes competitiveness. Bechtel signed USD 9 billion in EPC agreements for NextDecade’s LNG export complex, bundling craft labor demand under multi-year workforce development programs. Balfour Beatty secured an USD 889 million Interstate 30 redesign by integrating apprenticeship commitments that met local hiring goals. Such integrated labor pipelines relieve skilled-trade scarcity and improve proposal scores, further concentrating awards among digitally advanced, talent-focused majors. The top 10 firms together command roughly 55% of national revenue, signifying a moderately consolidated environment.

United States Commercial Construction Industry Leaders

Turner Construction Company

Bechtel Corporation

Fluor Corporation

Kiewit Corporation

Skanska

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: NextDecade signed USD 9 billion contracts with Bechtel for construction of LNG sites, representing one of the largest energy infrastructure awards in recent years and highlighting the scale of investment in domestic energy production capabilities.

- June 2025: Amrize debuted as an independent, publicly traded company following a 100% spin-off from Holcim, with USD 11.7 billion revenue for 2024 and operations across more than 1,000 North American sites, underscoring accelerating consolidation in the building-materials arena.

- April 2025: Balfour Beatty secured a USD 889 million contract from the Texas Department of Transportation to reconstruct a 2.3-mile stretch of Interstate 30 in Dallas, adding six general-purpose lanes and improving regional mobility.

- February 2025: ACS Group completed the combination of Flatiron and Dragados North American operations, creating the second-largest U.S. civil engineering firm with a USD 17.2 billion backlog and revenue of USD 6.1 billion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States commercial construction market as all spending tied to erecting, expanding, or refurbishing income-generating non-residential buildings, office towers, shopping centers, logistics hubs, industrial plants, hotels, and medical complexes, booked at contract award inside U.S. borders. We value each project at the contract amount in the year work commences, giving buyers a clear, like-for-like baseline.

Scope exclusion: civil infrastructure such as roads, bridges, utilities, and energy facilities sits outside this definition.

Segmentation Overview

- By Commercial Sector Type

- Office

- Retail

- Industrial and Logistics

- Others

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By States

- Texas

- California

- Florida

- New York

- Illinois

- Rest of US

Detailed Research Methodology and Data Validation

Primary Research

Our team spoke with general contractors, specialty subcontractors, project financiers, and state permitting officials across Sunbelt, Midwest, and Coastal hubs. Their insights on bid rates, contingency buffers, and start dates sharpened assumptions drawn from desk work.

Desk Research

We began with public datasets from the U.S. Census Bureau Value of Construction Put in Place files, Bureau of Labor Statistics cost indices, BEA fixed-asset accounts, Federal Reserve lending surveys, and briefs from AIA, NAIOP, and AGC. Mordor analysts then mined company 10-Ks, investor decks, and municipal bond prospectuses to map future pipelines and refine cost splits. Paid portals, D&B Hoovers and Dow Jones Factiva, supplied contractor financials and award notices. This roster is illustrative; many other feeds supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down model converts quarterly Census spending and permit statistics into the 2024 revenue baseline, then cross-checks results with selective bottom-up rollups, sampled contract values multiplied by representative floor area. Key drivers we track include class-A office vacancy, e-commerce share of retail sales, steel rebar prices, state capital budgets, and data-center megawatt additions. Multivariate regression links these indicators to historic spend and projects results through 2030, adjusting weights whenever bottom-up checks deviate by more than two percent.

Data Validation & Update Cycle

Each model passes anomaly scans, peer review, and a senior sign-off. Figures refresh every year, with interim updates whenever new legislation, price shocks, or mega-project news materially shift inputs.

Why Mordor's US Commercial Construction Baseline Earns Buyer Confidence

Published estimates often diverge because firms select different building lists, soft-cost mark-ups, and refresh cadences. Gaps we observe elsewhere include narrower project scope, uniform escalation factors, and reliance on announced work without cancellation tests; our six-variable model and frequent updates avoid these pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 567.05 B | Mordor Intelligence | - |

| USD 585.20 B | Regional Consultancy A | Renovation activity excluded; uniform escalation applied |

| USD 570.30 B | Trade Journal B | Counts announced projects only; ignores cancellation risk |

| USD 104.42 B | Global Consultancy C | Focuses on major CBDs; omits industrial and healthcare builds |

2024 value used where 2025 figure is unavailable.

These contrasts show that once scope and cost logic are leveled, Mordor's disciplined variable tracking yields a balanced, transparent baseline that decision-makers can replicate and stress-test quickly.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the United States commercial construction market?

The market was valued at USD 544.42 billion in 2024 and is projected to reach USD 567.05 billion in 2025.

Which segment is growing the fastest?

Industrial & logistics facilities are forecast to expand at a 5.21% CAGR through 2030 thanks to e-commerce and reshoring dynamics.

How significant is public funding in this market?

Public projects represent 15% of 2024 spend, but IIJA allocations are pushing public outlays to a 5.41% CAGR, gradually lifting their share.

Why are renovation projects gaining traction?

Retrofits and adaptive reuse cut delivery times by up to 30%, reduce embodied carbon, and qualify for new LEED v5 incentives, making them attractive amid high material inflation.

What are the main challenges contractors face today?

Skilled labor shortages, volatile material costs, and tighter lending standards are the most immediate headwinds impacting project schedules and profitability.

Which states offer the strongest growth prospects?

Texas leads in absolute activity, while Florida shows the fastest projected 5.30% CAGR on the back of population growth and infrastructure upgrades.