Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

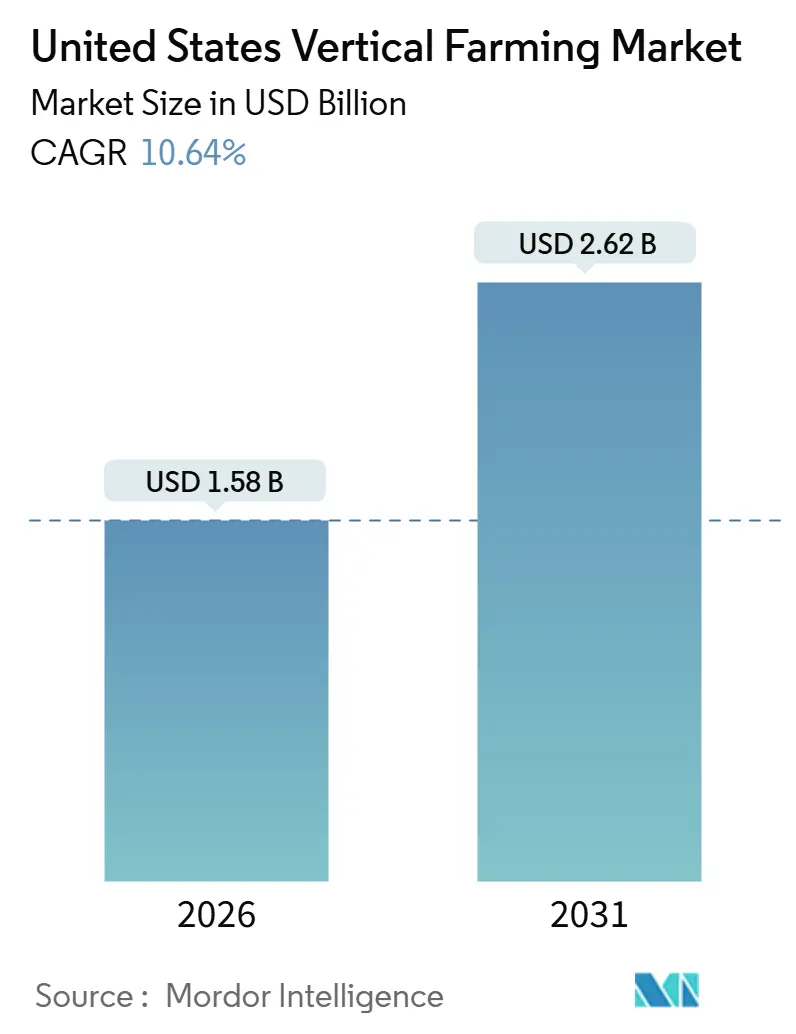

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 10.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Vertical Farming Market Analysis by Mordor Intelligence

The United States vertical farming market size is estimated to be USD 1.58 billion in 2026 and is projected to grow to USD 2.62 billion by 2031, registering a CAGR of 10.64% during the forecast period. The market's growth is driven by increasing consumer demand for pesticide-free produce, water scarcity regulations in the Southwest, and military commissary contracts, which are expanding the total addressable market despite a tightening in venture capital funding. Profitability in the market is heavily influenced by electricity costs, prompting operators to adopt renewable microgrids and dynamic power-purchase agreements to manage spot-price fluctuations, which ranged from USD 30 to USD 400 per megawatt-hour in California during 2023 and 2024. Competition in the market remains intense. Bowery Farming exited the market in November 2024, while AeroFarms underwent restructuring under Chapter 11 in 2023. In August 2025, 80 Acres Farms merged with Soli Organic to achieve greater scale. The next investment cycle in the United States vertical farming market is anticipated to focus on consolidation, modular shipping-container vertical farms, and edge-computing vision systems, which enable the production of premium crops such as berries and tomatoes.

Key Report Takeaways

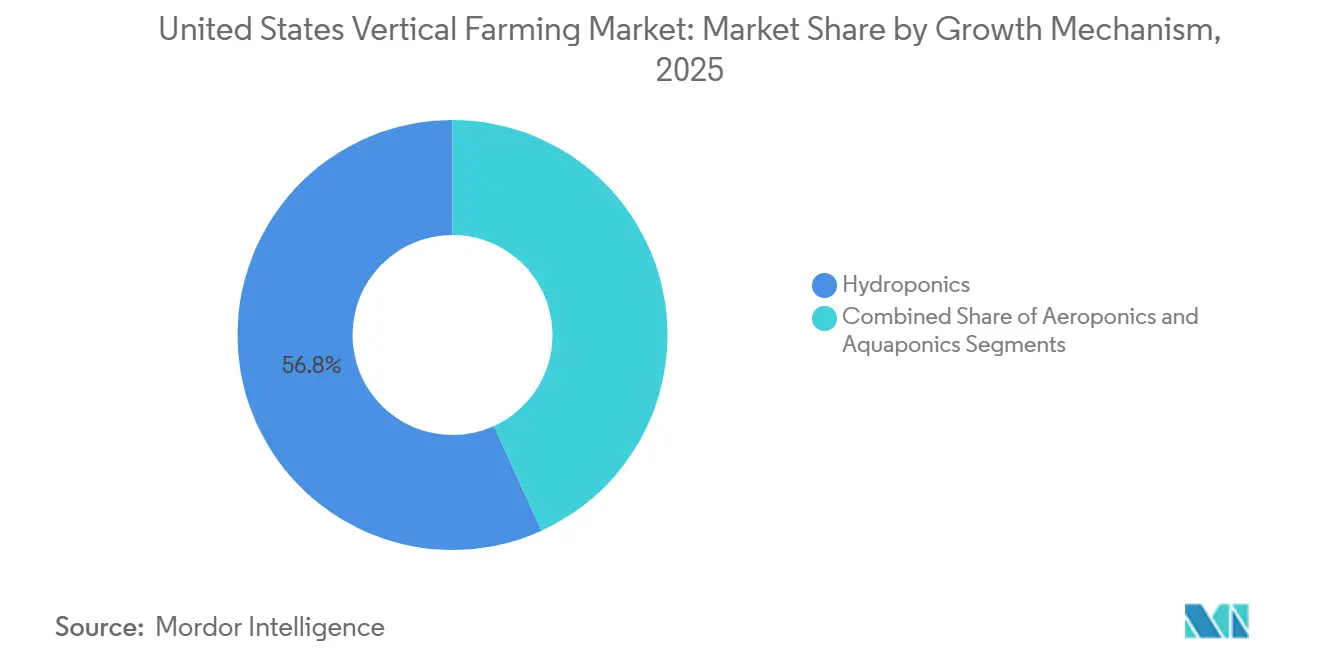

- By growth mechanism, hydroponics led the United States vertical farming market with 56.8% of the market share in 2025, while aeroponics is forecast to expand at a 16.0% CAGR through 2031.

- By structure, building-based facilities accounted for 68.6% of the United States vertical farming market size in 2025, whereas shipping-container vertical farms are projected to grow at a 12.2% CAGR through 2031.

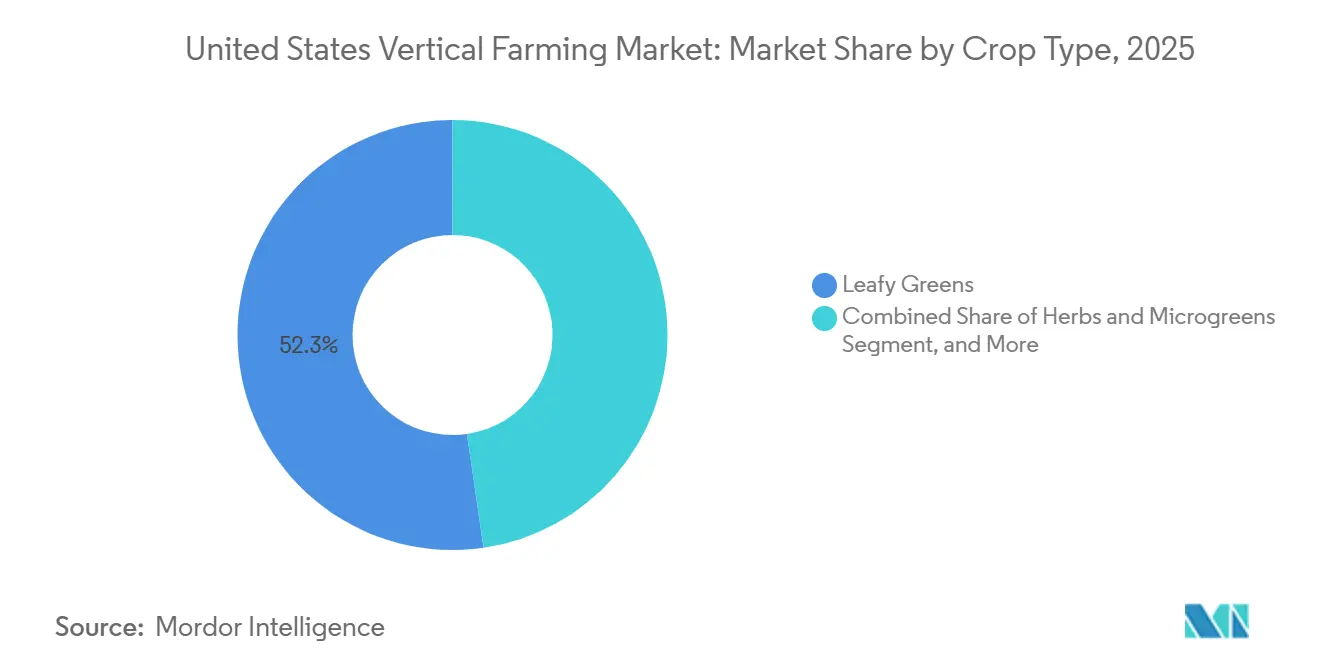

- By crop type, leafy greens accounted for 52.3% of the United States vertical farming market share in 2025, and fruits and berries are advancing at a 10.3% CAGR over the forecast period 2031.

- By component, hardware accounted for a 63.7% share of the market in 2025, and software is advancing at a 12.4% CAGR over the forecast period 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Vertical Farming Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for locally-grown pesticide-free produce | +2.0% | National, concentrated in Northeast corridor, California, and Pacific Northwest urban centers | Medium term (2-4 years) |

| Urban focus on food-mile reduction and freshness | +1.7% | Metropolitan areas with population density above 1,000 people per square mile | Short term (≤ 2 years) |

| Water-efficient agriculture amid drought policies | +1.4% | California, Arizona, Nevada, other Southwest states under Stage 2 or higher drought declarations | Long term (≥ 4 years) |

| Dynamic renewable-microgrid contracts cut power costs | +1.6% | States with renewable portfolio standards above 30% and time-of-use rate structures | Medium term (2-4 years) |

| Edge-computing vision systems unlock high-value fruit crops | +1.2% | National, early adoption in premium retail supply chains | Long term (≥ 4 years) |

| Defense-base supply contracts secure long-term off-take | +0.6% | Proximity to military installations with active commissary networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Locally-Grown Pesticide-Free Produce

Consumer willingness to pay price premiums for pesticide-free salads has established a stable revenue stream for operators in the United States vertical farming market. Hydroponics accounted for 61% of national tomato production, 67% of cucumber production, and 66% of lettuce production [1]Source: U.S. Department of Agriculture Economic Research Service, “Controlled Environment Agriculture Statistics,” ers.usda.gov. Plenty Unlimited utilized Walmart’s equity investment to distribute greens to over 430 Albertsons stores in California by January 2025. Additionally, shrink rates that are 15–20% lower than those of field-grown produce have converted trial listings into long-term supply contracts. Little Leaf Farms expanded to over 8,000 retail locations after securing a USD 250 million credit facility in October 2024, highlighting that the future growth of the United States vertical farming market will depend on retailers’ efforts to improve per-foot gross margins.

Water-Efficient Agriculture Amid Drought Policies

Stage 2 drought declarations in California and the 2024 allocation cuts under the Colorado River Compact have necessitated the incorporation of water-saving measures into investment models. Hydroponics reduces water usage by 99% compared to traditional farming methods, while aeroponics further decreases consumption by 95% through the application of micronutrient misting at frequent intervals. The United States Department of Agriculture Natural Resources Conservation Service has awarded Ponix Systems USD 4.9 million to expand hydroponic lettuce production. However, life-cycle analyses indicate that energy demand for hydroponic lettuce is 162 megajoules per kilogram, compared to 10.7 megajoules for field-grown lettuce. In response, operators within the United States vertical farming market are adopting closed-loop irrigation systems and procuring renewable energy to ensure water savings do not exacerbate electricity cost disparities.

Dynamic Renewable-Microgrid Contracts Cut Power Costs

Electricity constitutes 30% to 50% of operating costs, making power hedging a critical factor in determining profitability within the United States vertical farming market. Bowery Farming’s 150-kilowatt solar array and 200-kilowatt-hour battery reduce carbon dioxide emissions by 204.1 metric tons annually and generate USD 500,000 in net-present-value savings through time-of-use pricing arbitrage. In Texas, the Electric Reliability Council of Texas (ERCOT) market offers negative pricing during periods of oversupply, enabling farms to align photosynthetic activity with the lowest energy costs. The United States Department of Energy is providing loan guarantees for controlled-environment agriculture projects that incorporate dispatchable demand response, shifting lender evaluation criteria from revenue growth to megawatt-hour elasticity [2]Source: U.S. Department of Energy, “Agricultural Energy Efficiency,” energy.gov. If implemented on a national scale, microgrids could bring the United States vertical farming market closer to cost parity with traditional field-grown produce.

Defense-Base Supply Contracts Secure Long-Term Off-Take

The United States Department of Defense has designated hydroponic lettuce as an eligible product, ensuring consistent demand and protecting producers from retail price competition [3]Source: U.S. Government Accountability Office, “Federal Food Purchases,” gao.gov. Babylon Micro-Farms received a USD 49,898 Small Business Innovation Research contract from the United States to pilot modular units on military bases. These public sector agreements include inflation-adjustment clauses, which help stabilize debt-service coverage. Additionally, the 2024 Salinas Valley Escherichia coli outbreak highlighted vulnerabilities in traditional field supply chains, prompting military commissaries to collaborate with local vertical farming partners. This shift continues to support demand in the United States vertical farming market, even during periods of reduced consumer spending.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economically viable crop range remains narrow | −1.6% | National, acute in markets competing against California and Arizona field output | Short term (≤ 2 years) |

| Electricity-price volatility hurts margins | −1.4% | States without renewable standards or industrial tariffs | Medium term (2-4 years) |

| Lithium-ion storage bottlenecks delay renewable adoption | −0.8% | National, supply chain chokepoints in battery cell manufacturing | Long term (≥ 4 years) |

| Talent poaching by semiconductor fabs inflates automation labor costs | −0.7% | Arizona, Texas, Ohio, regions with major chip fabs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economically Viable Crop Range Remains Narrow

Leafy greens contribute positively to margins due to their 30- to 45-day growth cycles and retail prices ranging from USD 4.41 to USD 8.82 per Kg, which help offset energy costs that are 20–30 times higher than traditional field production. These shorter cycles allow for quicker turnover and reduced exposure to prolonged operational risks. In contrast, crops like strawberries and tomatoes require longer growth cycles of 60 to 90 days, which ties up working capital and increases biological risks, such as susceptibility to pests and diseases over extended periods. The 2023 bankruptcy of AppHarvest, partly attributed to USD 60 million in electricity debt for a 60-acre tomato facility, highlights the consequences of poorly aligned crop selection and the financial strain of energy-intensive operations. Many growers in the United States vertical farming market remain vulnerable to risks such as retailer delistings and single-pathogen outbreaks due to a lack of diversified crop portfolios, which could otherwise mitigate these challenges and enhance operational resilience.

Talent Poaching by Semiconductor Fabs Plants Inflates Automation Labor Costs

Intel and Taiwan Semiconductor Manufacturing Company are recruiting over 2,000 electrical and mechanical engineers in Arizona and Ohio, offering annual salaries ranging from USD 80,000 to USD 120,000, along with equity. In comparison, salaries in the agriculture sector range from USD 50,000 to USD 70,000. Vertical farms require comparable automation expertise to integrate programmable logic controllers and sensor networks. These automation systems are critical for optimizing operations, reducing manual intervention, and ensuring consistent production quality. Local Bounti achieved a 19% improvement in labor productivity after implementing computer-vision robots, but filed a patent to protect its intellectual property amid increasing competition for wages. The shortage of skilled talent is driving up ramp-up costs across the United States vertical farming market, further emphasizing the need for advanced automation and efficient workforce management strategies.

Segment Analysis

By Growth Mechanism: Hydroponics Holds Sway as Aeroponics Accelerates

Hydroponic systems accounted for 56.8% of the United States vertical farming market share in 2025, bolstering lender confidence due to turnkey suppliers and extensive horticultural data that mitigate ramp-up risks. These systems support crops such as tomatoes, cucumbers, and lettuce through nutrient baths, which reduce commissioning costs and simplify food safety audits. Commercial software solutions from providers like Hortimax and Priva streamline nutrient dosing, making hydroponics the preferred choice for new entrants in the United States vertical farming market. Economies of scale in LED procurement and nutrient formulations contribute to profitability, and the segment's maturity ensures hydroponics will remain the primary revenue driver in the United States vertical farming market through 2031.

Although aeroponics represents a smaller revenue share, it is projected to grow at a 16.0% CAGR through 2031, nearly 50% faster than the overall United States vertical farming market. Misting systems in aeroponics deliver nutrients with an absorption efficiency of 98%, reduce growth cycles by approximately 30%, and lower microbial risks in the root zone. AeroFarms reports 95% water savings compared to hydroponics, and validation from the National Aeronautics and Space Administration enhances its technical credibility. As sustainability certifications gain importance, aeroponics is well-positioned to capture a growing share of the United States vertical farming market, particularly for high-margin crops such as spinach, kale, and microgreens.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Structure: Building-Based Platforms Dominate While Containers Climb

Building-based vertical farms accounted for 68.6% of the United States vertical farming market size in 2025. This dominance is attributed to centralized chillers, shared utilities, and multi-tier racks, which optimize crop output per square foot. Gotham Greens’ network of thirteen facilities demonstrates how rooftop integrations reduce last-mile freight costs and secure premium shelf space. Additionally, industrial vacancy rates of 4% to 5% present opportunities for conversions at costs below replacement value, making building-based assets a preferred choice for large institutional investors seeking exposure to the United States vertical farming market.

Shipping-container vertical farms are projected to grow at a 12.2% CAGR, providing entrepreneurs with a cost-effective entry point into the United States vertical farming market. For instance, Freight Farms’ Greenery S module can produce up to 4 metric tons of leafy greens annually, with a bill of materials ranging from USD 150,000 to USD 200,000. This allows small operators to test market demand before scaling operations. Municipalities and school districts are increasingly adopting container units for food security initiatives, while defense installations are exploring containerized farms to localize their supply chains. As financial institutions become cautious about funding large-scale greenfield projects, container solutions are poised to capture a growing niche within the overall expansion of the market.

By Crop Type: Leafy Greens Lead as Fruits and Berries Surge

Leafy greens accounted for 52.3% of the projected 2025 revenue, representing the core of the United States vertical farming market's proven unit economics. The combination of 45-day crop cycles and strong consumer demand enables growers to achieve positive adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA), even in regions with volatile power prices. Little Leaf Farms’ 40-acre greenhouse in Pennsylvania is projected to drive annual retail sales to approximately USD 200 million, demonstrating the scalability of lettuce and arugula production. Supermarket buyers prioritize low shrink rates and consistent year-round quality, ensuring leafy greens remain the largest segment of the United States vertical farming market.

Fruits and berries are projected to grow at a compound annual growth rate (CAGR) of 10.3% through 2031, supported by retail prices that are three to five times higher than those of lettuce. Oishii’s New Jersey facility employs bumblebee pollination and computer-vision monitoring to achieve premium Brix levels, showcasing the scalability of strawberries in climate-controlled environments. While 60- to 90-day crop cycles tie up working capital, edge-computing technology optimizes harvest timing to protect margins. As pollination techniques advance, fruits are projected to contribute additional value and diversify revenue streams within the United States vertical farming market, particularly for operators adept at managing energy costs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Component: Software Becomes the Margin Differentiator

Hardware captured 63.7% of the United States vertical farming market share in 2025, mirroring the heavy upfront spending on light-emitting diode arrays, climate-control systems, irrigation lines, and battery storage, which together can reach USD 400,000 per megawatt of installed grow-light capacity. Bowery Farming’s 150-kilowatt solar array and 200-kilowatt-hour battery underscore the continued dominance of physical equipment in collateral valuations when lenders size construction loans, while turnkey packages from Priva and Hortimax continue to commoditize margins for lighting, heating, ventilation, air conditioning, and irrigation to single digits.

Software is projected to grow at a compound annual growth rate (CAGR) of 12.4% through 2031, driven by proprietary algorithms that optimize lighting schemes, nutrient mixes, and harvest timing, thereby improving yields and labor efficiency beyond the capabilities of standard equipment. Local Bounti improved labor productivity by 19% and reduced unit labor costs by 17% in 2025 after deploying computer-vision quality control. It then filed patents to secure its training data and inference models. Amazon Web Services Greengrass now runs machine-learning models on-site, eliminating latency and bandwidth fees while guiding light cycles and robotic pickers in real time. The United States Department of Agriculture National Institute of Food and Agriculture validated this direction with a USD 175,000 grant for autonomous monitoring software, signaling that code rather than steel will decide which growers refinance construction debt at investment-grade spreads.

Geography Analysis

BrightFarms Inc. (Cox Enterprises, Inc. )’s establishment of 1.5 million-square-foot hubs in Texas and Georgia highlights a strategic focus on central-continental logistics. These locations place two-thirds of the United States' population within a one-day drive and leverage favorable industrial electricity tariffs, enhancing competitiveness in the United States vertical farming market. In the Northeast, population density supports rooftop greenhouse initiatives by Gotham Greens Holdings, LLC, where higher retail price points and extended winter periods strengthen the economic rationale for local hydroponic farming.

California and the broader Southwest present a mix of opportunities and challenges. Chronic drought conditions increase the appeal of water-efficient cultivation methods, while extensive field production can sometimes pressure vertical farm pricing. Plenty Unlimited Inc.’s Compton facility, for instance, ships approximately 2,040 metric tons of produce annually to 430 Albertsons stores. However, the company closed its South San Francisco research site in 2023 to reduce costs. Meanwhile, municipal regulators are debating whether to classify vertical-farm water usage as industrial rather than agricultural, a decision that could significantly impact the feasibility of expansion in regions reliant on the Colorado River basin.

Midwestern and Southern states are emerging as key growth areas for the United States vertical farming market, driven by lower land costs and access to grid reliability programs. Companies like 80 Acres Farms, Inc. and Soli Organic have expanded their networks across states such as Ohio and Arkansas, benefiting from industrial leases that are approximately 30% cheaper than those in coastal areas. Additionally, the 2024 Agriculture Improvement Act allocated USD 20 million for urban indoor agriculture research, with grants distributed through land-grant universities concentrated in these regions. Policy support and energy cost advantages position interior states to accommodate the next wave of capacity expansion, as established operators increasingly focus on adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) rather than solely pursuing revenue growth.

Competitive Landscape

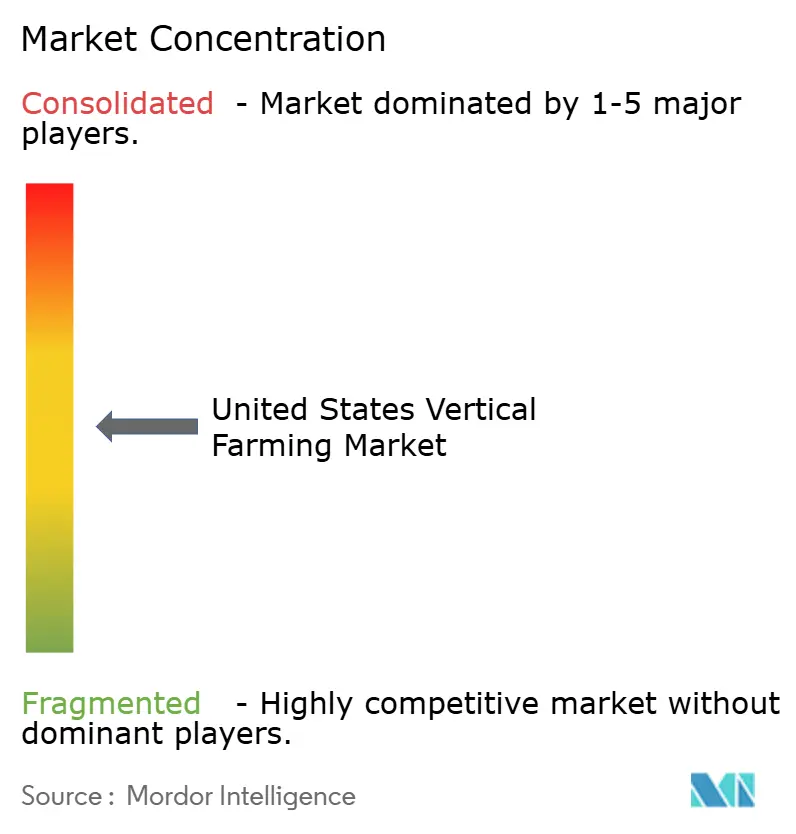

The five largest players, AeroFarms, Inc., Bowery Farming, Inc., Gotham Greens Holdings, LLC, Plenty Unlimited Inc., and 80 Acres Farms, Inc., accounted for a significant market share in 2025, making the United States vertical farming market moderately concentrated despite notable exits. AeroFarms, Inc.’s Chapter 11 restructuring and AppHarvest’s 2023 bankruptcy removed heavily funded competitors. However, remaining players swiftly acquired distressed assets at discounted prices. Consolidators like BrightFarms, backed by Cox Enterprises, leverage patient capital and extensive real estate networks, providing advantages in site selection and utility negotiations.

Technology and cost efficiency now play a critical role in achieving a competitive edge. Local Bounti Corporation enhanced labor productivity by 19% through the use of proprietary robotics and secured patents to protect algorithms that optimize climate control and harvest timing. In February 2025, 80 Acres Farms, Inc. raised USD 115 million from General Atlantic and Siemens Financial Services to fund the integration of genetics following its acquisition of Plantae Biosciences. Meanwhile, Plenty Unlimited Inc. entered a USD 680 million joint venture with Mawarid Group to expand into the Middle East, diversifying revenue streams beyond domestic retail channels.

Regulatory developments also influence market dynamics. The Food and Drug Administration’s water-testing rules, effective July 2024, impose less stringent requirements on controlled environments compared to traditional field farms. This regulatory advantage reduces compliance costs for vertical farming operators, potentially concentrating market power among well-capitalized companies. The competitive landscape is shifting toward regional hub models that optimize logistics and electricity costs. Smaller niche firms are focusing on specialty crops and underserved geographies. Ultimately, scale, cost efficiency, and strategic positioning will determine which companies emerge as dominant players following the next wave of consolidation in the United States vertical farming market.

United States Vertical Farming Industry Leaders

Bowery Farming, Inc.

AeroFarms, Inc.

Gotham Greens Holdings, LLC

Plenty Unlimited Inc.

80 Acres Farms, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Canadian agritech company Growcer has acquired the assets of U.S.-based Freight Farms following Freight Farms' bankruptcy filing. This acquisition ensures continuity for hundreds of container farm operators, as Growcer has taken over the technology, intellectual property, and support services. Growcer has committed to supporting the existing community and fostering a sustainable future for the industry.

- May 2025: Illinois State University (ISU) has established a vertical farm within a repurposed shipping container, showcasing a sustainable approach to urban agriculture. The facility utilizes hydroponics, LED lighting, and 95% less water compared to traditional farming methods to grow thousands of plants year-round. It also offers students practical training in agricultural technology, food security, and environmentally sustainable food production.

- March 2025: The United States-based vertical farming company, 80 Acres Farms, Inc., expanded its national presence by acquiring three indoor vertical farms and associated intellectual property (IP) from its competitor, Kalera, Inc. This acquisition is projected to enhance 80 Acres Farms' production capacity, strengthen its market position, and provide access to advanced technologies developed by Kalera, Inc.

United States Vertical Farming Market Report Scope

Vertical farming is an agricultural practice that involves growing crops in vertically stacked layers, typically within controlled indoor environments. This production system optimizes plant growth by regulating factors such as light, temperature, humidity, and nutrients, and commonly employs soilless cultivation techniques including hydroponics, aquaponics, and aeroponics.

The United States vertical farming market is segmented by growth mechanism (aeroponics, hydroponics, and aquaponics), structure (building-based vertical farms, warehouse-based vertical farms, and shipping container vertical farms), crop type (leafy greens, herbs and microgreens, fruits and berries, and flowers and ornamentals), and component (hardware, software, and others). The report provides market size and forecasts in terms of value (USD) for all the aforementioned segments.

By Growth Mechanism

| Aeroponics |

| Hydroponics |

| Aquaponics |

By Structure

| Building-based Vertical Farms |

| Warehouse-based Vertical Farms |

| Shipping-Container Vertical Farms |

By Crop Type

| Leafy Greens |

| Herbs and Microgreens |

| Fruits and Berries |

| Flowers and Ornamentals |

By Component

| Hardware |

| Software |

| Others |

| By Growth Mechanism | Aeroponics |

| Hydroponics | |

| Aquaponics | |

| By Structure | Building-based Vertical Farms |

| Warehouse-based Vertical Farms | |

| Shipping-Container Vertical Farms | |

| By Crop Type | Leafy Greens |

| Herbs and Microgreens | |

| Fruits and Berries | |

| Flowers and Ornamentals | |

| By Component | Hardware |

| Software | |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the United States vertical farming market in 2031?

The market is projected to reach USD 2.62 billion by 2031, representing a 10.64% compound annual growth rate from 2026.

Which growth mechanism is expanding fastest in United States controlled-environment agriculture?

Aeroponics leads with a 16.0% CAGR through 2031, outpacing the overall market due to higher nutrient-absorption efficiency and shorter crop cycles.

How are electricity costs affecting profitability in indoor farming?

Power accounts for up to half of operating expenses and volatility can swing margins sharply, prompting farms to adopt renewable microgrids and dynamic pricing contracts.

Why are leafy greens still the dominant crop in indoor agriculture?

Leafy greens have 30- to 45-day cycles, stable retail demand, and can absorb energy costs better than longer-cycle fruiting crops, keeping them at 52.3% revenue share.